Our last update was on the 13th of July. We asked, “Does the third quarter mean a new start to the year?” Well, it looks like we have a partial answer as we enter August. The S&P 500 rose 9.11% after dropping -8.39% in June. Year to date now the S&P 500 is down -13.34% after hitting a low of -23.07% on June 16th. One month does not mean the end of the year long misery but for now it means a break.

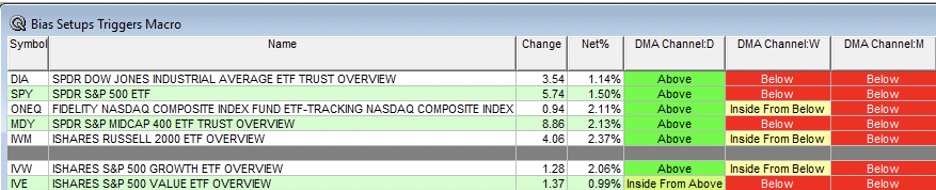

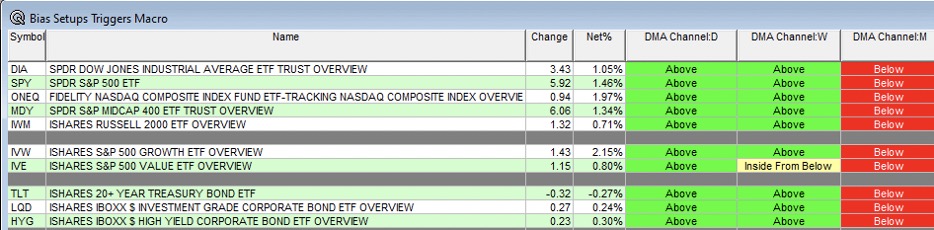

In our last Bias Indicator update on the major equity indexes the only period that had strength was the Daily (see July 13th Table). Now the weekly is in great shape as well as all U.S. Equity Indexes are above their weekly DMA Channels (see July 29th Table).

July 13th Table

July 29th Table

The trick in August is going to be getting the indexes into their monthly DMA Channel first and then above the channel. The SPDR S&P 500 via SPY will need to move above $429.52 during August to get into its channel. That may be a challenge but last month getting above the weekly DMA Channel seemed to be a challenge.

The reality is that it may take a couple more months to get back above the monthly DMA Channel. So far the S&P 500 has been below the monthly DMA Channel over the last four months. This equals the 2011 draw down of four months below the monthly DMA Channel.

Once we enter a fifth month below the monthly DMA Channel then we enter the 2000 to 2002 period and 2007 to 2009 as the only periods with a longer duration below the monthly DMA Channel. Worse would be a failure of the weekly DMA Channel which is a possibility as we enter the difficult August through September time period. More on this period in our next update.

We recommended Salesforce (CRM) in an article that was published on June 13th at a price of $166.03. It closed Friday, July 29th at $184.02 up $10.61 which is 10.83% while in the same period the S&P 500 is up 10.15% and the Technology Select Sector SPDR ETF (XLK) is up 15.12%.

Last month we showed the chart of Growth vs Value ETFs . Growth was represented by IVW and value by IVE. All year long the story has been about value beating growth. But we have turned the corner on that trade. We suggested to trade IVE for IVW and that has worked out well so far. Here is our updated chart from Erlanger Chart Room (ECR) that enables me to see the outperformance of IVW.

The chart above shows the relative strength of IVW against IVE. When the blue line is heading higher growth is beating value. We also throw in a 20 day simple moving average to track the degree of outperformance so when the blue line is above the red moving average then IVW is beating IVE.

Last, we create a spreader of the relative strength and the moving average and when it is green we have out performance. As you can see, IVW continues to outperform IVE.

Over the last seventeen weeks, the S&P 500 has now risen five weeks and has risen two weeks in a row for the first time since March with this latest week. This upcoming week will be a pivotal week to see if the indexes can extend the streak to three up weeks in a row.

In our last update we introduced our indicator called the Erlanger Big Barf (EBB). It had closed above zero which was a good sign of more potential upside. The EBB tracks the relationship of the S&P 500 against the CBOE Volatility Index. It will move higher if the S&P 500 rises and the VIX falls.

The EBB will also fall if the S&P 500 falls and the VIX rises. The VIX closed on Friday at 21.33 from 24.64 on July 13th update. A test of 20 to remains a key level to see if we can get into the teens.

The daily EBB Is now at 11.80. Meanwhile the weekly EBB is now positive at 3.80 which in mid July was in the red. The monthly is still negative and like the weekly DMA Channel we will need to get it into positive territory.

The S&P 500 is much like the little blue engine from the childhood book The Little Engine That Could. The little blue engine was climbing a big hill and kept saying, “I think I can, I think I can”. The S&P 500 like the little blue engine as it has a big hill to climb that began at 3666 on June 16th. Currently, the S&P 500 has gotten to 4130.29 with the peak at 4796.56 on the first trading day of the year.

In childhood fairytales, the end result is a positive outcome and in the case of the little blue train it made it over the hill. It remains to be seen if the S&P 500 can have a childhood fairytale ending this fall or it turns into a Stephen King nightmare.

© Erlanger Research

Read more commentaries by Erlanger Research