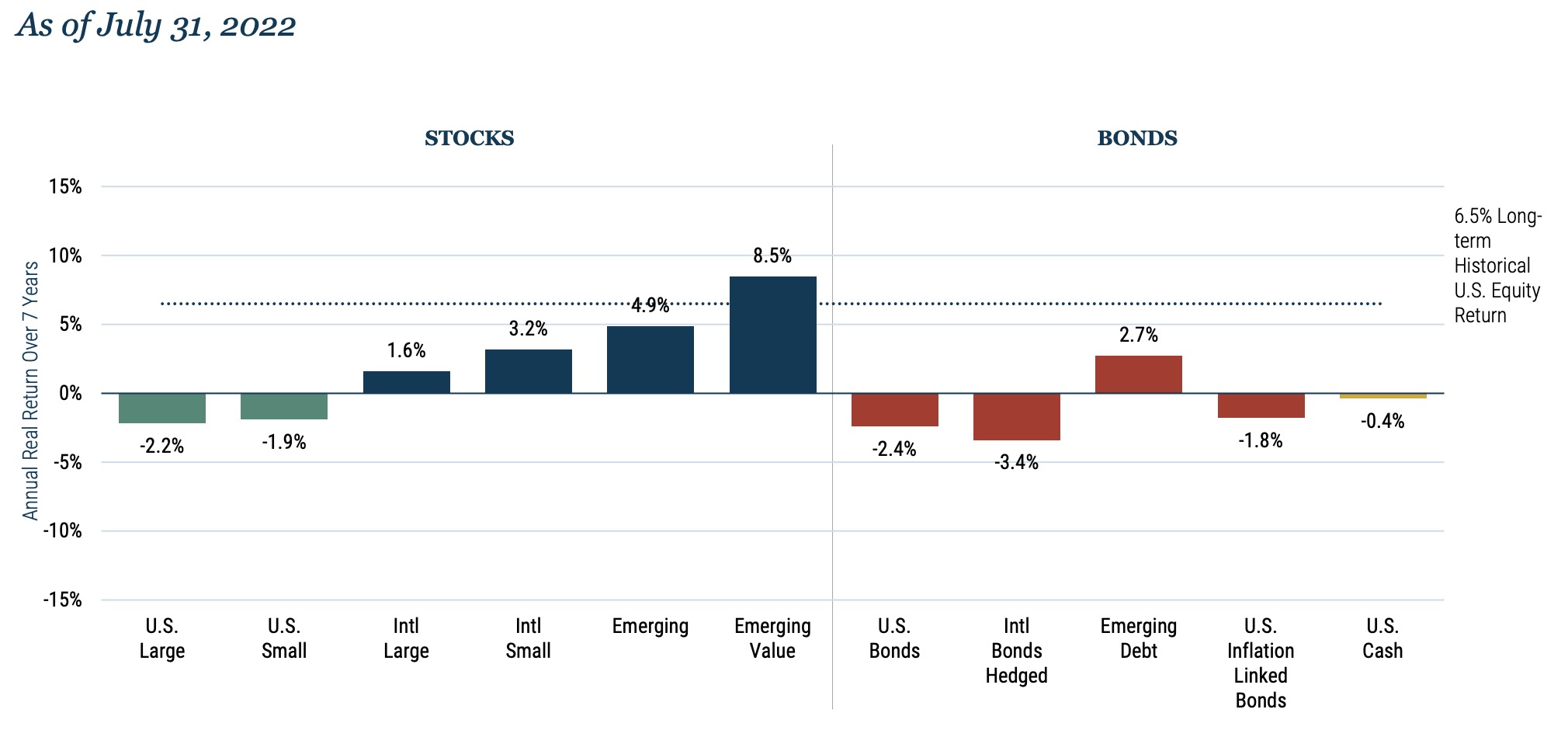

Rick Friedman from GMO’s Asset Allocation team offers the following comments about the updated forecasts:

"This year’s sharp decline in stock prices and rise in interest rates (and credit spreads) improved the outlook for stock and bonds. The second quarter selloff made it a more attractive time to take risk though July’s strong equity performance, particularly in U.S. Growth, tempered our forecasts."

"Despite valuation compression across all countries, U.S. equities remain expensive relative to their history and other countries. We still prefer non-U.S. equities to U.S. and find Value especially attractive outside the U.S. in places like Japan and Emerging ex-China. That said, we believe the cheapest parts of the U.S. market have become more attractive."

"Even though Value has meaningfully outperformed Growth this year, Value stocks still trade at abnormally wide discounts across regions and sectors. GMO’s Equity Dislocation strategy seeks to exploit what we believe will be a narrowing in these extreme valuation gaps."

Source: GMO *The chart represents local, real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forwardlooking statements. U.S. inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

© GMO