After peaking at nearly 3.5% in mid-June, the 10-year US Treasury yield fell around 90 basis points over the following 6 weeks to 2.6%. Since, however, it has climbed steadily to about 3.2% as of September 8. Both ascents were accompanied by the warnings that the long bond bull market is over—that the secular trend begun in the early 1980s has reversed—partly because of persistent inflation.[1] But it’s not clear that recent or current inflation provide useful information about the future direction of longer-term interest rates.

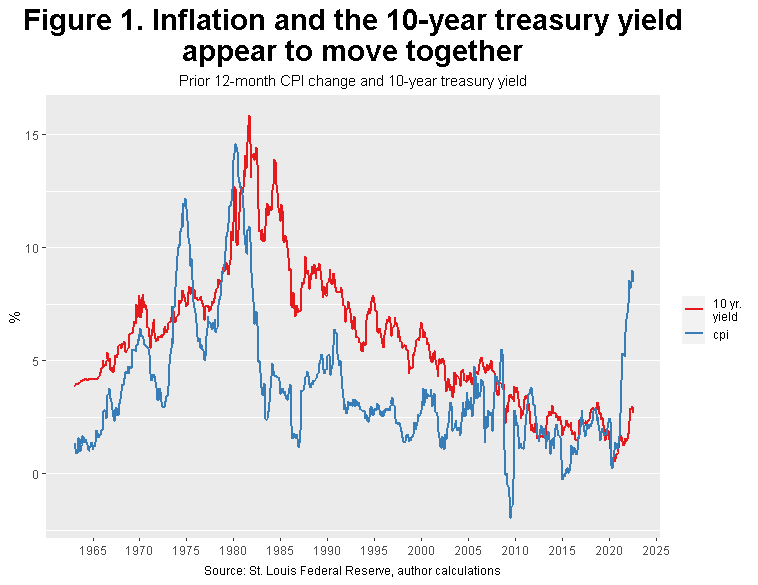

Superficially, there’s a relationship between inflation, for which I use the 12-month percentage change in the Consumer Price Index (CPI), and the yield on the 10-year treasury. Both appear to move up until the peak in inflation and rates in 1982 and fall steadily through the late 1980s when CPI changes became trendless (Figure 1). Yields continued to decline, though not without interruption. There are plenty of potential breaks that never matured into full-blown trend changes. These argue for humility when forecasting.

There’s good theoretical reason to expect inflation and yields to move together. If inflation were predicted to persist, nominal interest rates at all maturities should go up according to the Fisher identity, which holds that the ex ante nominal rate should equal real rates plus expected inflation. The complication is that expectations are fluid.

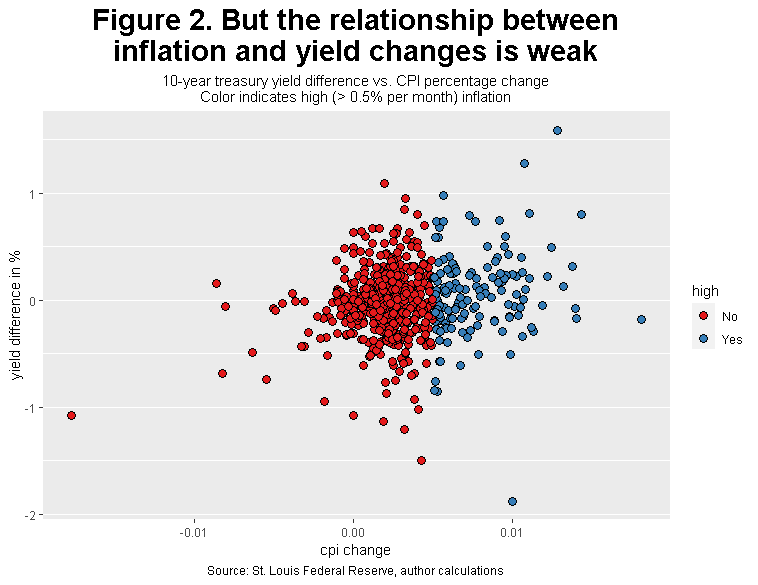

Perhaps that’s why the correlation between the contemporaneous change in 10-year treasury yields and inflation is a modest 0.19 with a 95% confidence interval of 0.11 to 0.26, meaning the true value could be as low as 0.11, though its likely higher.

This ambiguous relationship holds both when inflation is high—somewhat arbitrarily, greater than 0.5% per month—and when its low (Figure 2). In fact, when inflation is high (the blue points), its correlation with yield changes isn’t different from zero, statistically. That both sets of points in Figure 2 mostly resemble a shapeless cloud should probably give the tactical asset allocator using inflation to inform interest rate bets pause.

We can be more rigorous about this. Analysts sometimes assess predictive usefulness with Granger causality tests, named after Nobel-winning econometrician Clive Granger. The Granger test answers a simple question: does using X to help predict Y do a better job than relying only on past values of Y? If so, we say that X “Granger causes” Y. Granger causality doesn’t mean that X causes Y in the usual sense, rather it means that X helps to forecast Y (perhaps because both are related to a third variable).

Does inflation help predict monthly changes in the 10-year yield? No, it doesn’t appear to. At customary significance levels we “can’t reject” the hypothesis of no Granger causality.[2] That is, there isn’t sufficient evidence to say that inflation helps to predict the 10-year yield better than past values of yield alone, a conclusion which holds for lags out to 12 months. I’m also unable to reject the hypothesis that inflation expectations (using the University of Michigan Surveys of Consumers series[3]) don’t Granger cause treasury yield changes.

An investment strategy predicated on using inflation—actual or expected, contemporaneous or lagged— to predict interest rate movements is probably resting on thin statistical ice.

There are of course many ways to test relationships between time series. A different specification or more sophisticated—and complicated—approach may yield different conclusions. But simple Granger test results are suggestive. They counsel caution when making inflation-based interest-rate predictions.

That said, if inflation isn’t tamed, nominal rates, including the 10-year treasury yield, should rise as required by the Fisher identity. Bond bears will likely feel vindicated.

But it’s worth keeping in mind that because inflation hard to predict—its motion could be described as a random walk[4]—so too are nominal rates. Those who want to know if the long bond bull market is dead may have to consult variables other than past and current inflation for answers.

(1) For example: Masters, B. (2022, May 18). PIMCO: Navigating the end of the bond bull market. Retrieved September 7, 2022, from https://www.ft.com/content/2cb8d56a-2a0c-40f7-9977-a3ab8078a191

(2) The “p-value” for inflation is 0.06, thus we “fail to reject” the hypothesis of no Granger causality at a 5% significance level. This is the case whether inflation is defined as CPI, “core” CPI (excluding food and energy costs), or the personal consumption expenditures (PCE) deflator.

(3) University of Michigan, University of Michigan: Inflation Expectation [MICH], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MICH, September 7, 2022.

(4) If a time series contains a random walk, its value in one period is equal to its value in the last period plus a white noise error. The error is what makes the variable’s motion random.

The author is an applied economist and portfolio strategist at Armstrong Advisory Group in Needham Massachusetts

ARMSTRONG ADVISORY GROUP – SEC REGISTERED INVESTMENT ADVISOR

The information contained herein including any expression of opinion, has been obtained from or is based upon, sources believed to be reliable, but is not guaranteed as to accuracy or completeness. This is not intended to be an offer to buy, sell or hold or a solicitation of an offer to buy, sell or hold the securities, if any referred to herein.

© Armstrong Advisory Group

Read more commentaries by Armstrong Advisory Group