Dividends and dividend-paying stocks are getting renewed attention in recent months. This brief white paper seeks to survey the dividend paying stock questions and issues and provide some observations and historical data.

Dividend policy is a matter of capital structure in that companies use dividends to repatriate cash to shareholders or choose not to pay dividends in order to reinvest in their business. Some companies even borrow to sustain or increase dividends as part of a decision to include more debt in their capital structures, others just to sustain dividends in down years.

In general, mature, slower-growing companies tend to pay regular dividends, while younger, faster-growing companies would rather reinvest the money toward growth. Some market pundits claim that dividends are irrelevant to the overall performance of a stock. On the theoretical side, Franco Modigliani and Merton Miller posited in their famous article on the “irrelevance” of dividend policy, that the underlying expected earnings and cash flow of companies, not their dividend payouts, determine market values. However, back-tested history indicates that public companies with dividends (especially rising dividends) produce higher overall returns for their shareholders and experience lower volatility over a long-term investment horizon. Rising dividends over an extended period indicates efficient capital management, as well as sufficiently strong cash flow and profits to support the growing dividend payouts.

Rising dividends over the long-term indicates that a company is able to withstand changing economic conditions. A company that can effectively get through the up-anddown cycles of the market and maintain its rising dividends clearly is well-managed and will provide dividend income, dividend growth and asset appreciation. Like so many things in stock market analysis, there are no standards in dividend analysis. However, many would argue that a company that can maintain a 25-year record of consecutive dividends without a cut is a Dividend Aristocrat. Reinvesting rising dividends from good quality growing companies can have a significant positive impact on a portfolio. Didn’t Albert Einstein coin the phrase that compound interest is the eighth wonder of the world?

Dividend paying stocks provide a way for investors to get paid during rocky market periods, when capital gains are hard to achieve. Dividend-paying stocks, on average, tend to be less volatile than non-dividend paying stocks. And a dividend stream, especially when reinvested to take advantage of the power of compounding, can help build wealth over time. However, dividends do have a cost. A company cannot payout dividends to shareholders without affecting its market value. Cash that a company pays out to shareholders is cash that is no longer part of the asset base of the corporation. This cash can no longer be used to reinvest and grow the company. A stock price adjusts downward when a dividend is paid.

Dividends are an underappreciated factor in equity investing, especially when investors are anxious about the global growth outlook (as is the case today). Like earnings, dividend payments are sensitive to the economic cycle, but less so, with companies typically reluctant to cut dividends in anything but exceptional circumstances. A tilt toward dividend payers should provide ballast to portfolios in a volatile equity market and offer scope for outperformance against traditional equity benchmarks.

Dividends have always played an important role in the total return for equities. Indeed, reinvested dividends have accounted for approximately 40% of aggregate total return for equities. The dividend yield on global equities has averaged 2.3% since the start of the century, although that is below the long-term norm, but consistent with historically low bond yields. High-dividend yielding stocks outperformed during the past three U.S. recessions, underscoring their benefit in weaker economic conditions and they have outperformed significantly year-to-date as well. While high-dividend-yielding stocks underperformed badly in price terms during the last economic expansion and from the March 2020 low until late-last year, relative performance on a total return basis over the past two decades had been reasonably stable.

Dividends historically have been more stable than earnings, which is an important attribute as global economic growth downshifts: Dividends payments dipped only marginally during the 1990-1991 recession, while earnings fell sharply. Dividend payments were cut more materially during the Great Recession (especially for financials) and during the pandemic, but much less than earnings. The annual growth rate of dividends is much less volatile than that of earnings. While for the most of the past three decades dividends and earnings have grown at a similar pace, the variation in the annual dividend growth has been less than half that of earnings. Companies are reluctant to cut dividends even in an economic downturn for fear of signaling a lack of confidence in their underlying business outlook. Accordingly, the dividend payout ratio rises during recessions and often when earnings growth is lackluster. Currently, the dividend payout ratio is towards the lower-end of its historical range and has ample room to rise as economic growth weakens. The low dividend payout ratio implies that there is little absolute downside risk to the level of dividend payments in the absence of a deep economic recession, which we do not expect.

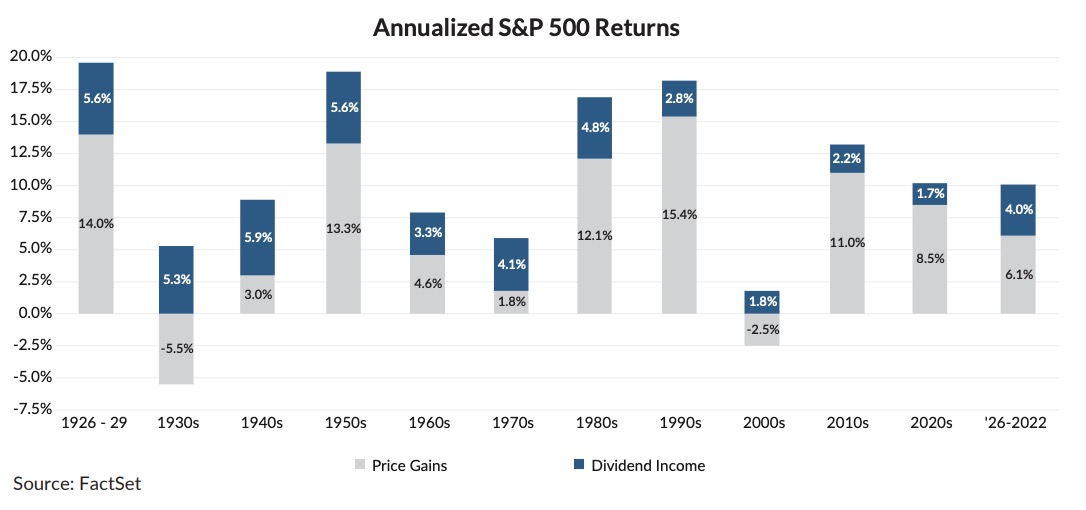

As noted earlier, over the nearly 100 years since the S&P 500 was created, more than 40% of the total return from that average has come from dividends (see below). Of course, it varies significantly from year to year, and decade to decade.

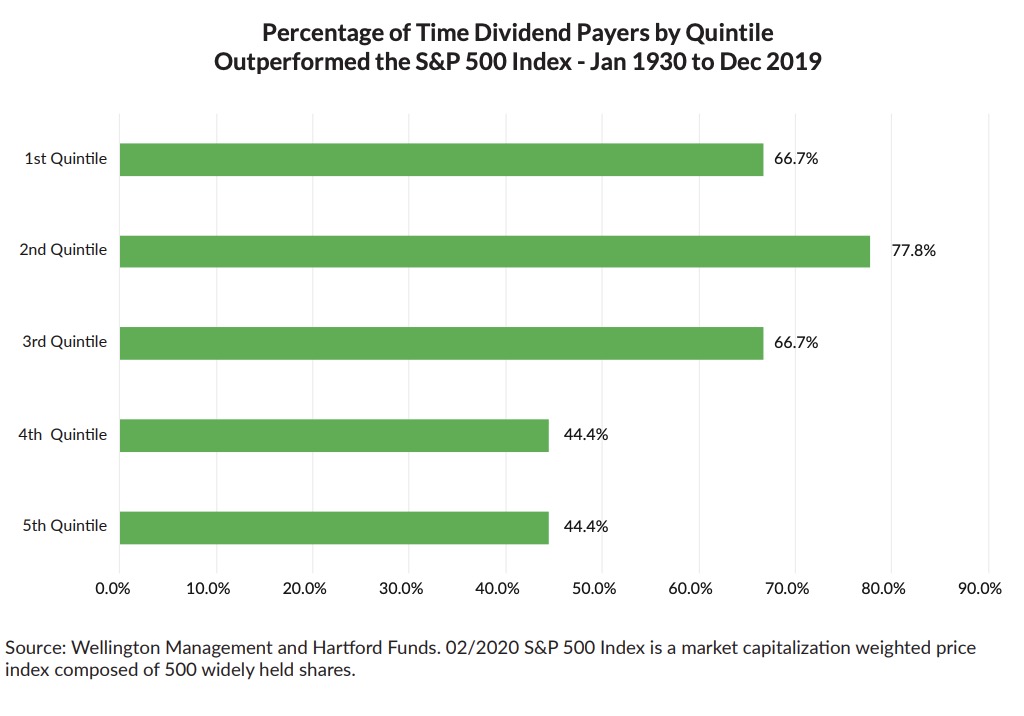

Many studies show that the highest yielding stocks are not necessarily the best performers as a very high dividend might suggest a financial or operational problem that can lead to a dividend cut and a decline in stock price. In fact, the second highest dividend quintile has historically had the best total return. (See below.)

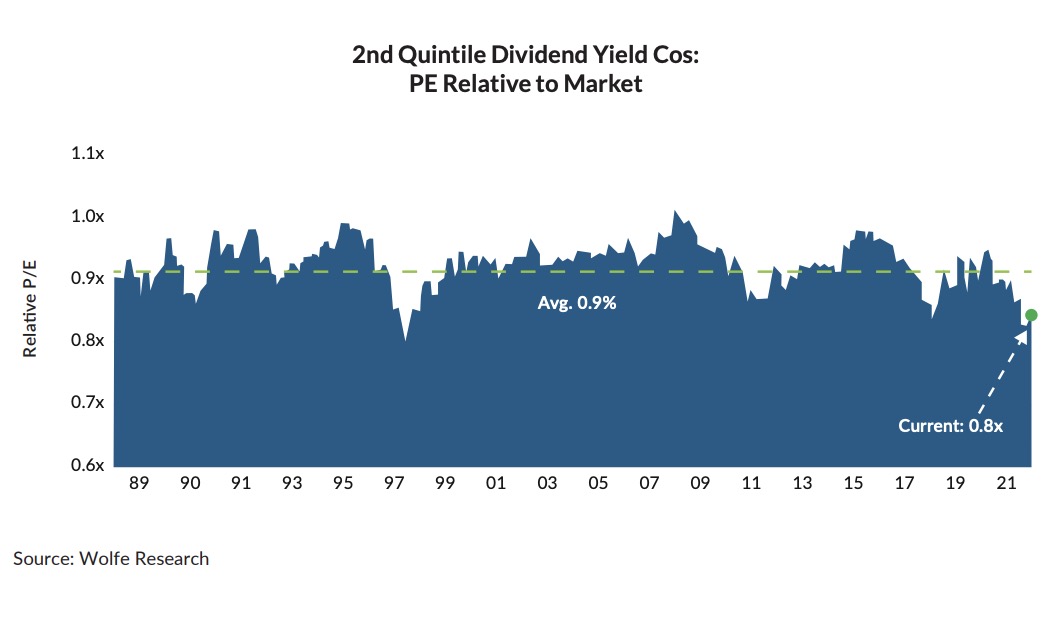

The chart below from Wolfe Research shows that this second quintile of dividend yields is currently selling cheap relative to history.

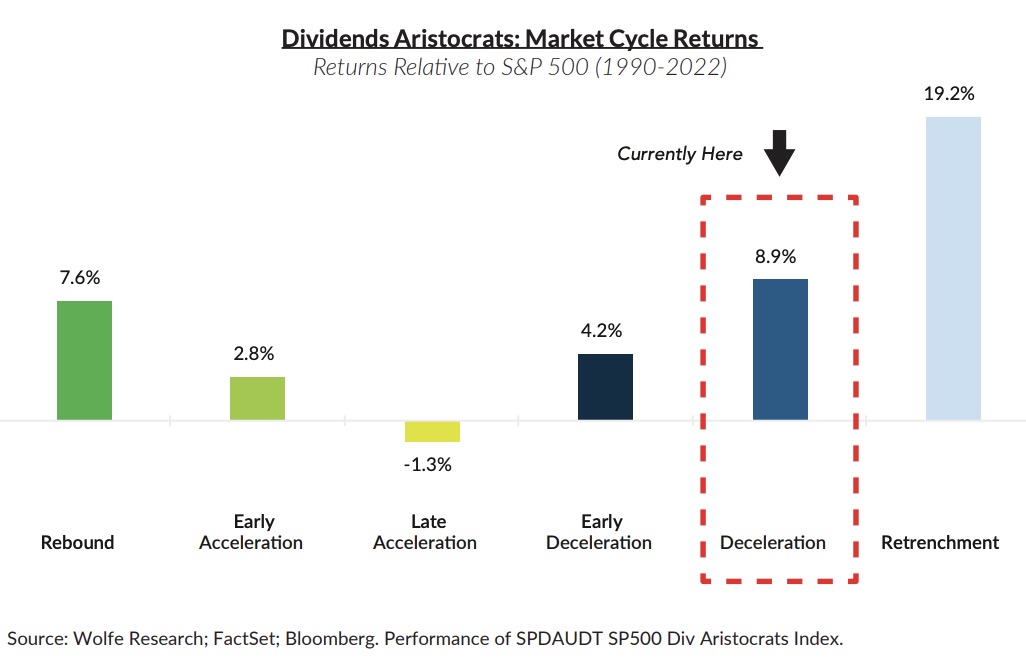

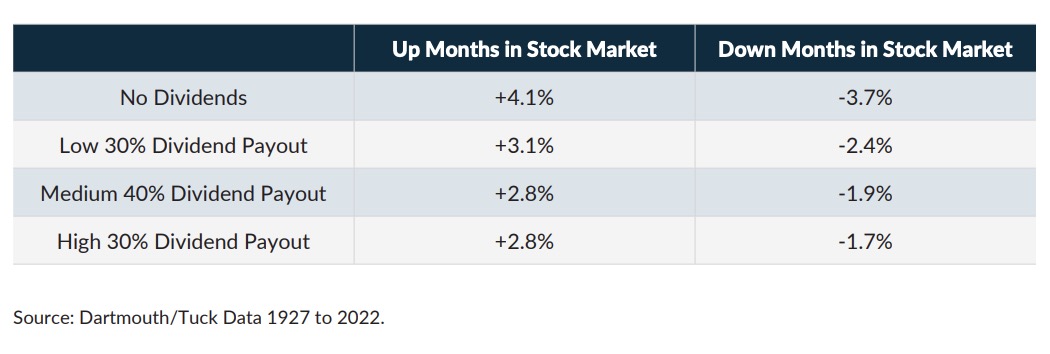

The best performance from dividend stocks tends to come at the most difficult period for the economy and stock market as illustrated below.

Dividend paying stocks tend to have their best relative performance in down months for the stock market, and their worst relative performance during up months.

What are the pros and cons of dividend investing? And the most common misperceptions?

Pros of Dividend Investing

1. Dividends may offer tax advantages (i.e., qualified dividends may be taxed at a capital gains tax rate, not ordinary income.)

2. Dividends can increase the rate of compounding through reinvestment.

3. Dividends may provide stable income and dividend growth can provide a hedge against inflation.

Cons of Dividend Investing

1. High dividends may mean slow growth (no good reinvestment opportunities).

2. Dividends can be cut or discontinued.

3. A dividend investing strategy may miss important segments of the market.

Some Common Myths

1. Dividend stocks are safe – not necessarily. Companies can go to excess to maintain a dividend resulting in significant negative financial consequences.

2. The highest yielding stocks are best – there are many studies that show the second highest quintile of dividend payouts contain the best performers. (Too many companies in the highest quintile end up cutting dividends.)

3. Dividend payouts limit growth – the best managed companies have figured out the balance between returning value to shareholders via dividends (or stock buybacks) and reinvesting for growth.

Dividends should provide some downside protection for equity portfolios in the coming months as global growth weakens, and portfolios tilted toward higher-dividend payers are well positioned to outperform and experience lower volatility than broad benchmarks. Beyond the near-term, dividends are also likely to play a more important role in equity total returns than has been the case in recent decades. In fact, we expect dividends to account for the majority of equity total returns in the next decade for most markets and their benchmarks as the tailwinds of three decades of strong real earnings growth and rising P/E ratios fade.

During the last couple of decades, when stock returns were generally robust, dividend considerations faded in market discussions. Assuming long-term returns (next 10+ years) for stocks will be below what investors have enjoyed over the last couple of decades (see our white paper published in March titled “Accepting Average: The Likelihood of Future Mediocre Returns”), dividends are likely to become a more important part of the total return of individual stocks and the market as a whole.

Crossmark Global Investments, Inc. (Crossmark) is an investment adviser registered with the Securities and Exchange Commission that provides discretionary investment management services to mutual funds, institutions, and individual clients. Information and recommendations contained in market commentaries and writings are of a general nature and are not intended to be construed as investment, tax or legal advice. Investment advice can be provided only after the delivery of Crossmark’s firm Brochure and Brochure Supplement (Form ADV Parts 2A and 2B) and Form CRS, and once a properly executed investment advisory agreement has been entered into by the client.

All Investments are subject to risks, including the possible loss of principal. All investments are subject to risks, including the possible loss of principal.

Equity investments generally involve two principal risks—market risk and selection risk. The value of equity securities will rise and fall in response to general market and/or economic conditions (equity market risk). The value of any individual equity security will rise and fall in response to the market’s perception of the issuer’s revenues, earnings, balance sheet, credit worthiness, business plan, and overall perception of the viability of the issuer’s business (selection risk).

These materials reflect the opinion of Crossmark on the date of production and are subject to change at any time without notice. Where data is presented that was prepared by third parties, the source of the data will be cited, and we have determined these sources to be generally reliable. However, Crossmark does not warrant the accuracy of the information presented.

This content may not be reproduced, copied or made available to others without the express written consent of Crossmark

NOT FDIC INSURED - MAY LOSE VALUE - NO BANK GUARANTEE

© Crossmark Global Investments

Read more commentaries by Crossmark Global Investments