As surging natural gas prices stoke inflation throughout Europe, policymakers are responding to both reduce the economic damage of high energy prices and clamp down on blistering inflation rates. It’s a challenging balance to strike, and the arrival of cooler weather won’t make the task any easier.

UK prime minister Liz Truss has come to power in an environment that would challenge even the most adept policymaker. Surging natural gas prices are pushing inflation to levels not seen in generations, punishing households. Last month’s inflation forecasts from the Bank of England (BoE) show prices rising more than 13% this year and staying above target for almost two years. Forecasts also show the economy falling into recession in the coming months as real, or inflation-adjusted, incomes collapse.

UK Price Caps Should Put Some Dent in Inflation

Against that backdrop, Truss announced a price cap on natural gas to shelter households from the 80% increase scheduled for next month and more price resets slated for January and April 2023. The government will most likely borrow to bridge the gap between market prices and the capped price, with even conservative estimates near £200 million.

What are the macroeconomic and monetary policy implications of such a large program?

We expect the cap to make a dent in inflation. With no action, UK inflation could easily have topped 15% this year. With the cap, we expect inflation to end the year around 10%, though that’s still much too high. Inflation will also likely fall much more quickly in 2023 than it would have; we forecast a 3.0% rate in December 2023. For 2024 and beyond, much depends on European natural gas prices and whether the price cap is extended—both are impossible to forecast this far in advance.

Still Plenty of Room for Tighter BoE Monetary Policy

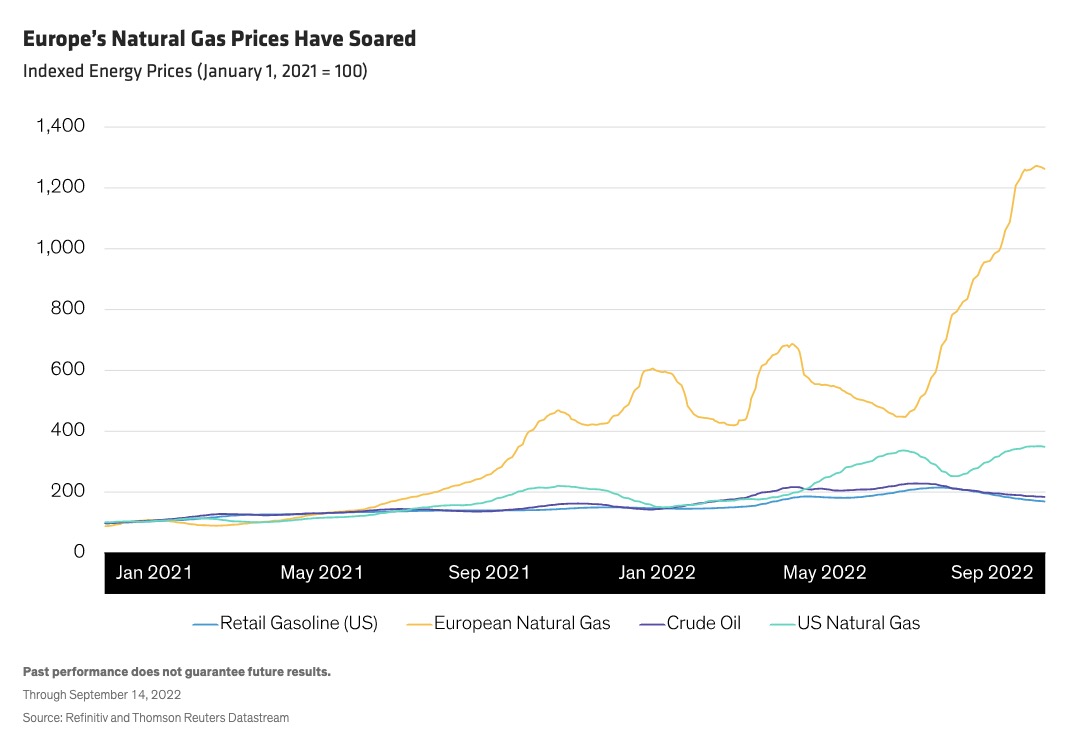

What about economic growth? We think the gas price cap will ease, but not eliminate, household pain. Even with the cap, natural gas costs almost 10 times today what it did at the start of 2021—a run-up that’s much more pronounced than other global commodity price increases (Display).

Given the magnitude of the shock, we still expect a recession in the UK, though perhaps a milder one than would otherwise have been the case. Goods production has already stagnated—it’s only services that have kept gross domestic product afloat lately. That situation will change as persistently negative real income eats into household spending.

Even though the gas price caps will tamp down inflationary pressures, we still see plenty of scope for tighter BoE monetary policy—the difference between 15% and 10% inflation isn’t nearly enough to prevent a sensible central bank from raising interest rates.

The restraint on the BoE to date has been the potential for a deep recession and sharply weakening labor market. The price caps make a severe recession less likely, in our view freeing the central bank’s hands to more aggressively contain inflation expectations and bring inflation to heel sooner. We expect at least another 125 to 150 basis points of rate hikes in this cycle, with forecast risks tilted higher.

Eurozone: Broader Gas-Supply Disruption Is a Risk

The pain from lofty natural gas prices is similarly severe in the eurozone. For now, we believe a mild recession is most likely, with the basic analysis similar to that of the UK. Falling real incomes will limit consumption and production, slowing the economy.

The European Central Bank will nonetheless continue to raise rates as inflation climbs. Europe’s fiscal support has been less comprehensive than in the UK—not surprising, given the more fractious politics involved. However, we believe that policymakers will do what they can over time to reduce the negative impact of rising gas prices on households and critical businesses.

The more worrisome scenario for Europe remains its direct dependence on Russian gas imports. If the war disrupts that supply enough that severe fuel rationing becomes necessary—especially with the onset of winter—the outlook will become much bleaker and a deeper recession more likely. Sum it all up, and while Europe’s weather may still be warm, the economy is cooling fast. Policymakers are doing what they can to ease the pain, but it’s shaping up to be a very difficult winter.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein