What You Need to Know

In a time of uncertainty, we believe that quality is the key to investing in equities. But to consistently find companies that meet high-quality standards requires research, judgment and investing skill. In this paper, we identify the characteristics that can help guide investors to high-quality businesses, and present different investment approaches designed to capture these companies in equity portfolios.

When buying a car, a washing machine or a piece of furniture, verifying the product’s quality is usually high on a shopper’s checklist. The same goes for stocks. Just as a big-ticket purchase is expected to function well for years, the companies in an equity portfolio should also stand the test of time.

But how can an investor know if the stocks held in a portfolio are truly durable? It’s not as simple as searching for consumer reviews about a TV. Instead, you need to find out how a fund manager evaluates the business attributes of the underlying companies and chooses the stocks for your portfolio. Dominant businesses, competitive advantages, innovation and management skill are just some of the features that define high-quality businesses that can deliver dependable cash flows over time.

Quality Features Underpin Long-Term Return Potential

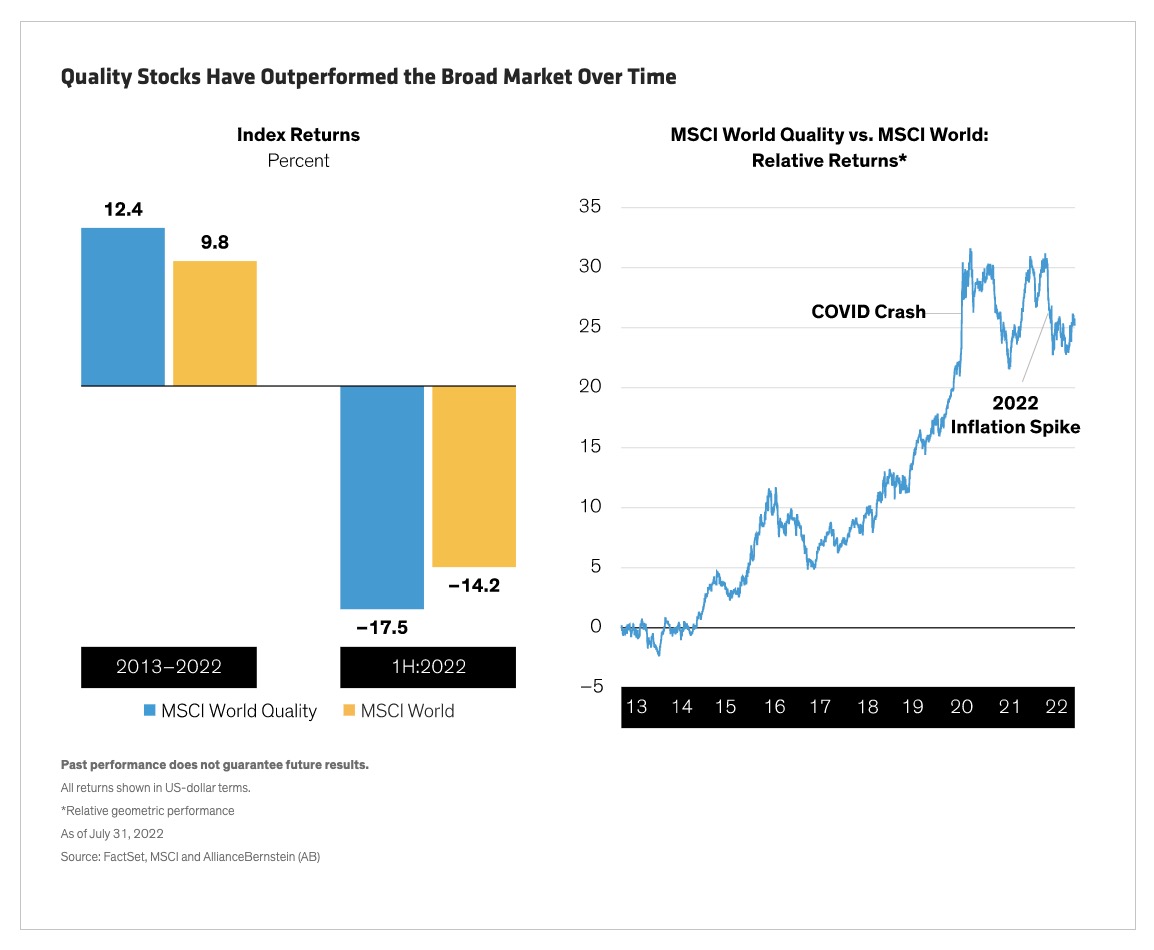

Quality in stocks can be measured in different ways. Yet the characteristics of resilient companies have something in common—they tend to underpin consistent, long-term equity return potential. Over the last decade, the MSCI World Quality Index returned 12.4% annualized, outperforming the MSCI World Index (Display). And during past market crises, quality stocks usually fell less than the broader market, a pattern that we’ve observed over longer time periods and in both US and global stock markets.

Yet no equity portfolio is immune from weak spells, and even high-quality stocks may falter from time to time. In the first half of 2022, stocks tumbled as surging inflation, rising interest rates, Russia’s invasion of Ukraine and China’s COVID-19 lockdowns threatened to tip the world economy into recession. Quality stocks fell by 17.5%, underperforming the broader market.

But following past crises, quality stocks have rebounded over time. When it comes to equities, we believe the long-term benefits of quality stocks aren’t necessarily illustrated by short-term return patterns. In our view, the early 2022 performance of quality stocks was an aberration, driven by an extreme confluence of extraordinary events. When the dust settles, we believe the benefits of a quality-focused approach will reassert themselves. In this paper, we aim to show how investors can find companies that provide exposure to quality, which should ultimately reward them through a challenging period ahead.

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein