Corporate profit margins finished 1999 at just a shade under 6% of U.S. GDP. That year, Warren Buffett wrote a piece in Fortune stating that 6% was the upper limit of where profits could sustainably reside.

In 2021, margins exceeded 9% of GDP—surpassing even those levels preceding the Wall Street Crash of 1929. While we make no claims to timing markets at Kailash Concepts, we believe the high-water mark for margins may be here.

History is clear that margins are subject to various economic cycles and mean reversion. In downtimes, margins can amplify negative sentiment and exacerbate the "hangover" after such periods. In good times, they can foster irrational euphoria.

In his Fortune article, Buffett noted that between 1964 and 1981, the GDP grew 370% and the number of companies in the Fortune 500 sextupled. And yet, the price of the Dow Jones barely moved. The culprit? The lethal combination of shrinking margins (from 5.9% to 3.5%) and skyrocketing interest rates (from 4% to 14%) fueled investor pessimism. By Jan. 1, 1982, the combined market cap of all U.S. securities was just 36% of that year's GDP.

The outlook soon brightened. From 1982 to 1998, the S&P would compound at 18% a year and deliver a 1,656% return to investors. Soaring profit margins, falling interest rates, and modest GDP growth were the key economic drivers of the market's outstanding performance.

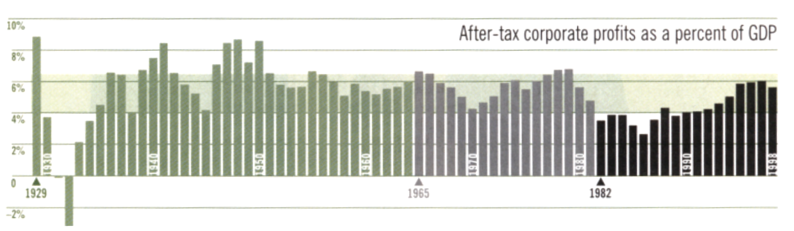

The chart below comes from Buffett's 1999 missive. It shows the after-tax profits of corporate America from 1929 to 1998. From 1951 to 1981 (after the 1929 crash, Depression, and wartime profits boom), margins generally stayed between 4% and 6.5%.

Source: Fortune Magazine; Data from 12/31/1929 - 12/31/1998

In the chart below from our piece Economic Cycles and Mean Reversion, we supplemented Buffett's numbers with data from 1999 to 2021.

As it turns out, Buffett was incorrect that margins of 6% or more are unsustainable for an extended period. But his rationale for this opinion was fascinating — and enlightening.

He didn't arrive at the 6% figure simply by observing the ranges that typified post-WWII America. Rather, his views were grounded in the idea that margins depend on competition and public policy. That's where Buffett looks quite prescient. He wrote …

"If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems–and in my view a major reslicing of the pie just isn't going to happen."

Over the past 10 years, investors have gorged on an ever-growing portion of the pie. And over that horizon, we have seen social discord in this country unlike any time we can recall. This hardly seems like the ideal environment to sustain 9% profit margins.

To put it another way, the social cost of margins staying at 1929 or 2021 levels seems perilously high. Nonetheless, many investors remain blissfully unaware of these dangers, extrapolating forward the extraordinary margins of the past 12 years. It's a mirror image of the pessimism that obscured investors' views in 1982.

All of which, we are certain, comes as no surprise to Buffett, who described "looking into the rear-view mirror instead of through the windshield" as investors' "unshakable habit."

When it comes to profit margins, mean reversion is coming sooner or later. And it may well be sooner. Equity holders should proceed with the utmost caution.

Dr. Sanjeev Bhojraj is a portfolio manager and co-founder of L2 Asset Management. He is widely published in journals in finance and accounting and specializes in behavioral finance. Dr. Bhojraj is a Chaired Professor in Asset Management and the co-director of the Parker Center for Investment Research at Cornell University’s Business School. He has a Ph.D., ACA, ACMA, and B.Com.

Matt Malgari is a portfolio manager, Managing Member, and co-founder of L2 Asset Management. Matt spent 14 years at Fidelity Investments as an Assistant Portfolio Manager on its $70 billion Diversified International Fund, sector analyst, diversified analyst, and trader. In 2010, Matt became the Managing director of Equity Research for Knight Capital Group. He received his MBA from Cornell University and a BA from Middlebury College.

© Kailash Concepts Research, LLC

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research