Too many people spend money they earned to buy things they don't want to impress people they don't like.

Our megatrend approach in 30 seconds

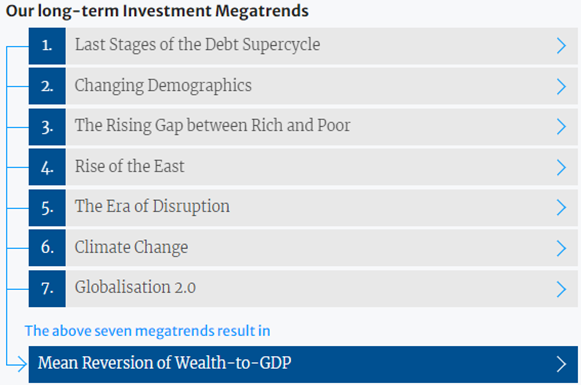

We have a long and proud history of investing thematically and believe you can remove a great deal of volatility in your portfolio, if you do so. In simple terms, the climate is changing, whether the rate of inflation is 1%, 5% or 10%. If you go to our website and click on Thematic, this image will pop up:

Exhibit 1: Seven megatrends as identified by Absolute Return Partners Source: Absolute Return Partners LLP

The aggregate result

As you can see, we have identified seven megatrends which, between them, drive our investment strategy. At the bottom of the chart, we have listed another one – Mean Reversion of Wealth-to-GDP – however, this is not a megatrend, but what we consider the aggregate result of the seven megatrends in question.

Wealth has grown excessively all over the world for the past 30 years or so. Apart from causing significant social problems (look at megatrend #3 above), wealth cannot grow faster than GDP in the long run. There are some very well-defined, mathematical reasons why the two cannot outgrow each other, and it works both ways, but I shall not go into any detail this month why that is, as it is a lengthy and rather complex issue. Suffice to say, over the last 2-300 years, or as far back as the data allows us to go, every time wealth-to-GDP has deviated much from its long-term mean value, it has reverted to the mean. There is not a single exception to that rule.

The present situation

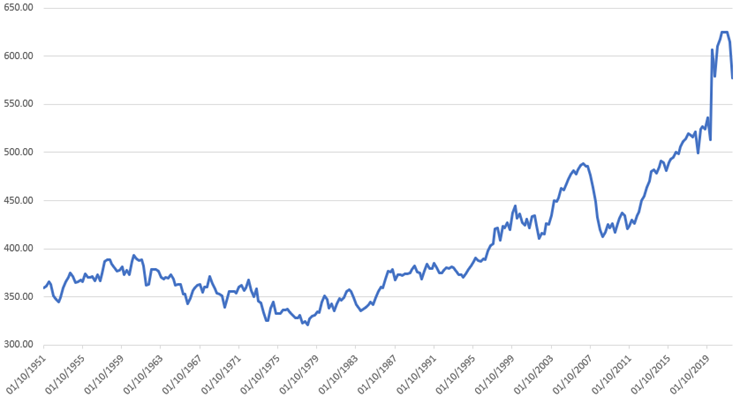

Because US wealth has grown so dramatically since the mid-1990s, US wealth-to-GDP is now well above its long-term mean value, which is 380-390% (Exhibit 2). US wealth-to-GDP peaked in 3Q21 at 625%. Losses in financial markets have since reduced total wealth-to-GDP in the US to 578%, which is a meaningful drop, yet a drop in the ocean if (when) we are going back to 380% again. All this implies that, at some point, US household wealth will drop more than 30% unless the correction takes place through the denominator, i.e. if GDP continues to grow whilst wealth stays flattish. It goes without saying that it could also be a combination of the two.

Exhibit 2: US wealth-to-GDP

Source: Federal Reserve Bank of St. Louis

So far, the drop in US household wealth is a consequence of falling equity prices and rising bond yields. Property prices have, on average, held up well so far and have therefore limited the fall in household wealth, but that could be about to change. In August, US foreclosures rose 14% month-on-month and 188% year-on-year (source: The World Property Journal). According to Freddie Mac, U.S. mortgage rates are now above 6% for the first time since late 2008. Inventories remain low, and that will limit the decline in property prices (as per Freddie Mac), but rising mortgage rates will almost certainly dampen demand and put downward pressure on US property prices in the months to come.

The composition of US wealth

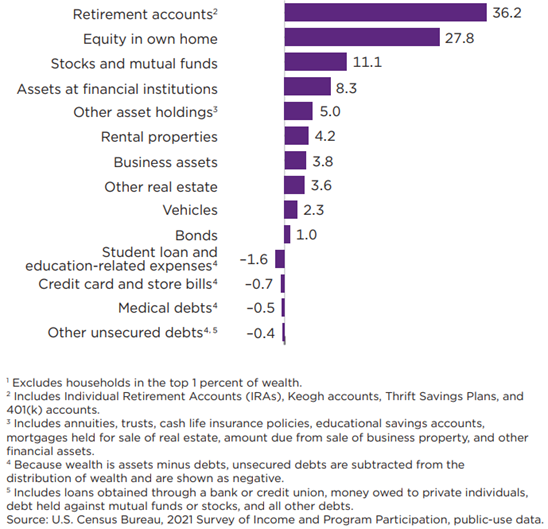

If US property prices start to decline, it will have a meaningful impact on US wealth. As you can see in Exhibit 3, between primary property, rental property and other types of real estate investments, property accounts for almost 36% of total wealth in the US. If US property prices were to decline 10%, $5Tn will be knocked off US wealth, and that will reduce wealth-to-GDP over there by approx. 25%.

Another point worth mentioning re Exhibit 3 is the low allocation to bonds. In fact, the 1% of US wealth invested in bonds only includes direct investments in bonds. Investments in bonds through retirement accounts (or, as we call them here in Europe, pension funds) are not included. For the same reason, the 36% invested in various types of property is not inclusive of property investments made by pension funds. As almost all of them make substantial allocations to property, the de facto exposure to property is well over 40%.

Exhibit 3: Composition of US wealth by asset type, 2020

Source: US Census Bureau

Why I focus on the US

You may wonder why I have made no mention of any other countries so far, and the reason is simple. Wealth statistics are more easily available in the US and the history much longer. In the EU, for example, statistics only go back to the 1990s. Although this is the primary reason I make no mention of any other countries in this paper, I should point out that wealth-to-GDP is not as rich elsewhere, as it is in the US. In most of Europe, for example, we are currently 10-15% above the long-term mean value, not 30% above as the Americans are.

In that context, let me make an important point. The mean value of wealth-to-GDP is not exactly the same in every country, but it is long-term stable everywhere, assuming the country in question is a free-market, capitalist economy. The reason wealth-to-capital it is not the same everywhere is quite simple. Think of wealth as capital and GDP as output. Wealth-to-GDP is thus a measure of how much capital it takes to generate $1 of output, i.e. it is a measure of capital efficiency. And because capital efficiency varies from country to country, wealth-to-GDP also varies.

Therefore, as the US is the most capital-efficient country in the world, it has the lowest wealth-to-GDP mean value. As I said earlier, the long-term mean value of US wealth-to-GDP is modestly below 400%. The fact that it is now 578% therefore suggests that, in the US, capital is not nearly as efficient as it once was.

Another way to measure the efficiency of capital in an open, capitalist economy is through the debt-to-GDP ratio, which is a measure of how much debt it takes to generate $1 of output. The more debt it takes, the less efficient the economy is. This links back to the first of ’our’ seven megatrends – Last Stages of the Debt Supercycle. In the early stages of all debt supercycles, debt-to-GDP is about 1, i.e. $1 of debt will generate $1 of output. As the debt supercycle matures, more and more debt shall be required to generate $1 of output.

All prior debt supercycles have collapsed when only $0.20-$0.25 of output is generated for every $1 of debt, and I note that both the US and China are approaching this ratio. Both are now below $0.30. The last debt supercycle to collapse was the one in Japan around 1990, and the next one to collapse will most likely be either the one in China or the one in the US – most likely the one in the US, as China is not an open, free-market, capitalist economy, meaning that the rule set is different. This is a fascinating topic which I have covered in this paper. If you subscribe to ARP+ and haven’t read it yet, I strongly recommend you do so.

Final few words

Some people have accumulated spectacular wealth in recent years, leading to an industrial-era, all-time high gap between rich and poor. However, as the rise in aggregate wealth has dramatically outpaced overall economic growth, there will be a price to pay, and that price will be painful. Unfortunately, the underlying economic theory says nothing about the timing of it. All I can promise is that wealth-to-GDP will, whether we like it or not, revert to its long term mean value sooner or later.

Over the last few years, I have come across many arguments why things are different this time, arguments that mostly are rooted in the higher productivity brought about as a result of the digital era. If that is the case, please explain to me why wealth-to-GDP was about 380% in the US in the early days of the industrial revolution some 250 years ago and still 380% as recently as the early 1990s, when productivity was immeasurably higher than it was in the second half of the 18th century. I will happily listen to your arguments but can assure you that the economic theory behind all of this states very clearly that wealth-to-GDP is long-term stable independently of the degree of economic development.

And it is precisely for that reason that we zoom in on uncorrelated investment strategies at Absolute Return Partners. Unfortunately, they don’t offer full protection on rainy days. During market crises, all risk assets temporarily correlate to 1 but, as the dust settles and logic returns, it is uncorrelated investments that offer the best protection.