Gold Mining Stocks Just Flashed a Bullish Signal

Membership required

Membership is now required to use this feature. To learn more:

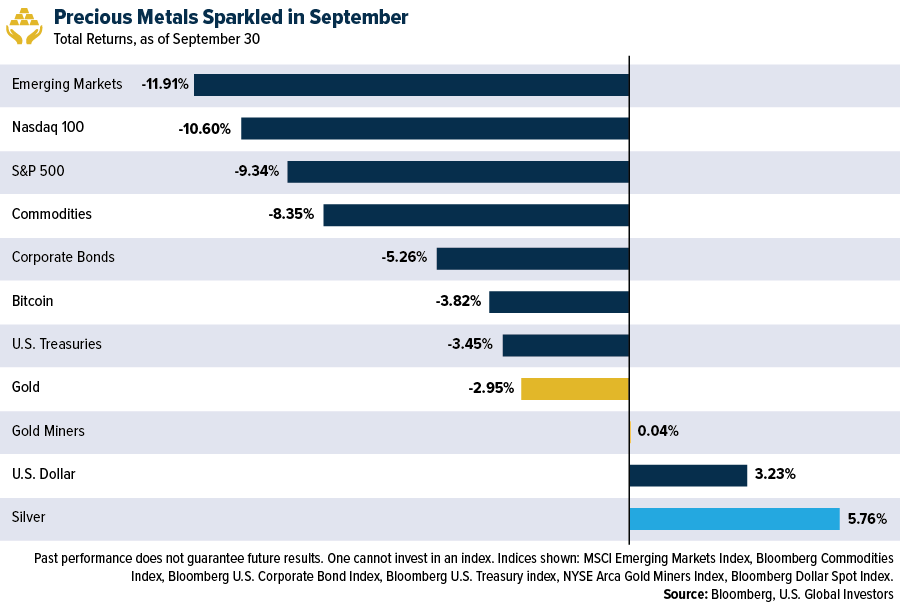

View Membership BenefitsGold fell for the sixth straight month in September, a losing streak we haven’t seen since 2018, as the Federal Reserve undertakes its most aggressive rate hike cycle in recent memory. The central bank has added close to 250 basis points (bps) so far this year in its fight against inflation, and many asset classes, from stocks to bonds to Bitcoin, have the bruises to show for it.

Gold is no exception, though it’s managed to hold up better than most investments, despite higher rates and an historically strong dollar, the precious metal’s longtime adversary. As of today, the S&P 500 has lost 22% for the year, while gold is down only 7%.

If you didn’t already know that September has often been the worst month for stocks, you probably know it now. This past September did not disappoint. The S&P 500 gave back more than 9%, marking the worst month since March 2020 and worst September since 2008.

Emerging markets tanked as well during the month, with index heavyweights Taiwan Semiconductor, Tencent, Samsung Electronics and Alibaba all falling between 15% and 20%.

Once again, gold and other precious metals were a bright spot. Although the metal cooled by nearly 3%, it was enough to beat U.S. Treasury and corporate bonds, domestic and oversea stocks, commodities and Bitcoin. In the bloodbath that was September, gold’s traditional role as a diversifier and haven was clear to see.

Silver turned in an even better showing, rising 5.7% on anticipated growth in industrial demand. The white metal is used in solar panels, the production and installation of which are set to increase dramatically following August’s passage of the Inflation Reduction Act, the largest-ever federal investment in renewable energy. The two best performing S&P 500 stocks in the third quarter were wind and solar companies Enphase Energy (+50%) and Constellation Energy (+45%).

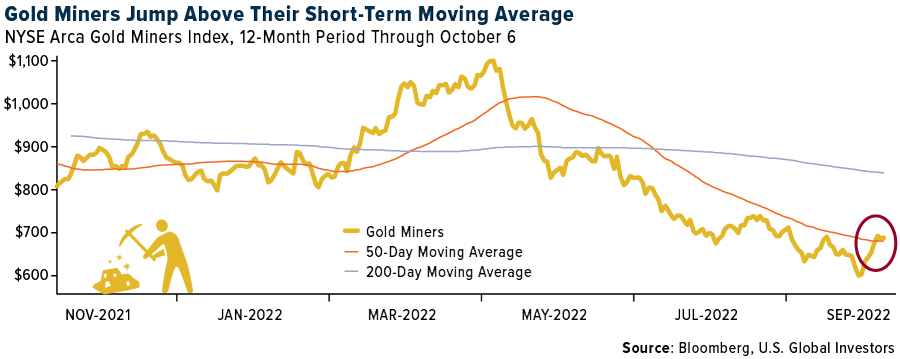

Gold Miners Break Out of Downward Trend

Meanwhile, gold and silver miners, as tracked by the senior NYSE Arca Gold Miners Index, were essentially flat for the month, breaking a five-month losing streak. The industry has had a challenging year. Down 21% year-to-date, mining stocks are on track for their worst year since 2015, when they fell 25.5%.

But the worst may be behind them. Since hitting a 52-week low on September 26, mining stocks have risen about 18% and today notched their second straight week of positive gains.

Looking ahead, the group appears to be teeing up for further growth. Having broken out of a downward trend going back to April, the index crossed above its 50-day moving average this week, which I see as a bullish signal.

Retail Investors Prefer Physical Gold Coins to ETFs

In getting exposure to gold, U.S. retail investors seem to favor physical bullion over ETFs. Gold-backed ETFs around the world experienced widespread outflows in September, the fifth straight month of drawdowns. Outflows were most pronounced in North America, where investors yanked out approximately 60 tonnes of gold, the equivalent of $3.2 billion, according to the World Gold Council (WGC). Nevertheless, total global holdings (3,548.5 tonnes, or $191.1 billion) are still slightly up from the start of the year, likely because gold continues to perform well in non-U.S. dollar currencies.

At the same time, it’s been a great year for gold coin sales in the U.S. The WGC reports that the combined sales of the U.S. Mint’s gold American Eagle and American Buffalo coins topped 1.3 million ounces in the nine-month period through September, a 7% increase over the same period last year and the highest total in 22 years.

What to make of this? Why have gold-backed ETFs sold off while gold coins have flown off shelves, so to speak?

It’s anyone’s guess, but I believe tangibility plays a large role here. In the past two to three years, world governments and central banks have printed more money than in any other time in history. Investors may rightfully be seeking ownership of hard, tangible assets that 1) are not issued by any central authority, 2) are no one’s liability and 3) cannot be created out of thin air.

As always, I recommend a 10% in gold, with 5% in physical bullion such as American Eagle coins, and another 5% in high-quality gold mining stocks, mutual funds and ETFs.

Index Summary

- The major market indices finished up/down/mixed/flat this week. The Dow Jones Industrial Average gained/lost x%. The S&P 500 Stock Index rose/fell x%, while the Nasdaq Composite climbed/fell x%. The Russell 2000 small capitalization index gained/lost x% this week.

- The Hang Seng Composite gained/lost x% this week; while Taiwan was up/down x% and the KOSPI rose/fell x%.

- The 10-year Treasury bond yield rose/fell x basis points to x%.

Airlines & Shipping

Strengths

- The best performing airline stock for the week was Turkish Air, up 19.3%. The summer saw a great mix of international and domestic leisure travel, and business travel started to return in mid-August. International travel was down 70% (2022 versus 2019) earlier in the year, but, as travel restrictions subsided, international recovered to down 13% in August. Business travel began rebounding in late August.

- Shipping container volumes for key ports Melbourne, Sydney, Brisbane, and Fremantle were up 13% in aggregate for the month of August 2022. The volumes rebounded strongly after the largely flat volumes seen in July 2022.

- Canada has dropped its remaining travel restrictions, including testing and quarantine requirements for Covid. Throughput at Canadian security checkpoints has started to pick up again and is approximately 90% recovered (same as U.S. TSA throughput) compared to approximately 85% before the announcement.

Weaknesses

- The worst performing airline stock for the week was SAS, down 13.6%. Labor unions and some U.S. lawmakers are pressing airlines not to resume stock buybacks after a Covid assistance prohibition expires this week. Representative Peter DeFazio, a Democrat who chairs the House Transportation and Infrastructure Committee, is holding a hearing on Thursday on investing in transportation workers that will discuss the issue. DeFazio is circulating a letter to colleagues seen by Reuters that urges airlines to “refrain from initiating stock buybacks… at least until air carriers are able to publish and fulfill schedules that meet demand; staff flights and key personnel positions appropriately; and return service to every community.” Aviation unions launched a campaign in August to pressure airlines against stock buybacks.

- Shipping rates decreased 11.3% this week and 23.5% year-over-year on North American routes to the West Coast and decreased 4.6% this week and 1.3% year-over-year to the East Coast. Rates on European routes were down 4.4% this week and 25.9% year-over-year to northern European locations, and down 5.7% this week and 32.2% year-over-year to those around the Mediterranean.

- The latest IATA data shows global passenger traffic declined by one point to -26% versus 2019 in August, with the biggest decline of two points in the Middle East while European passenger volumes dipped one point to -18% of 2019 levels. Global capacity was largely stable at -23% versus 2019 with Europe at -16%. Global load factors recovered to 82% but were still four points below 2019 with Europe at 86%.

Opportunities

- As Aeromexico, Avianca, and LATAM emerge from bankruptcy, restructured networks appear to improve the attractiveness of Copa Airline’s hub. Copa and Aeromexico have mostly restored markets at primary hubs to pre-pandemic levels. In contrast, Avianca and LATAM have reduced both markets and frequencies. Avianca exited bankruptcy with plans to convert from a full-service airline to an LCC to better compete with the rise of ULCCs, which should improve the relative attractiveness of Copa’s product.

- MSC Mediterranean Shipping Company, the largest container line in the world, is to launch its own air cargo service in early 2023, joining rivals Maersk and CMA CGM as top ocean carriers, adding airline units to diversify their service capabilities. As the latest of the three cash-rich European shipping lines to invest in the air cargo sector, the Swiss-Italian company will gain intercontinental airlift capacity for its own and third-party freight and parcel shipments.

- For airlines, October is the best month, from a relative perspective, as the group has historically outperformed at least 77% of the time. In addition, the fourth quarter has historically been the best quarter, with airline stocks outperforming the S&P 500 an average of 64% of the time. Demand commentary remains strong, but a recovery in the corporate channel is key for fourth quarter 2022 revenue guidance ranges, as the quarter has less peak leisure weeks than the third quarter.

Threats

- According to Credit Suisse, after slightly better-than-expected Mexican traffic levels in August (although still weak), the group expects weaker levels during September amid the low seasonality following the summer season. It is worth noting that, historically, airlines tend to decrease capacity significantly and load factors tend to weaken from August to September. This tendency is more visible for leisure destinations with double-digit month-over-month airline capacity decreases, while business destinations show less elasticity with lower decreases.

- Morgan Stanley believes UPS is due for a reset (similar to what recently happened at FedEx). Post FedEx’s earnings miss/warning last week, the group now believes normalized earnings per share (EPS) at UPS would be $8-$9 versus $10 before and compared to the pre-pandemic level of $7.50 (giving UPS some credit for operational improvement and healthcare segment gains).

- Global aircraft orders fell sharply in August after a strong July, as the industry stalled on its bumpy recovery from the pandemic. Only 30 commercial aircraft orders were placed in the month, down from 531 in July when a flurry of activity during the Farnborough International Airshow helped propel the industry to the best month since 2014. Orders were placed for 13 single-aisle and 17 wide-body aircraft in August, according to trade body ADS.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 12.1%. The best performing country in Asia this week was South Korea, gaining 3.6%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 0.2%. The South Korean won was the best performing currency in Asia this week, gaining 1.7%.

- Turkish equites once again recorded surprisingly strong gains while this week the country’s economic situation is fragile. Bloomberg reported that prices have increased 83.45% on a year-over-year basis. The spike in equites is supported by domestic retail buying and small inflows by foreign investors.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Russia, gaining 0.6%. The worst performing country in Asia this week was Thailand, losing 0.6%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 3.5%. The India rupee was the worst performing currency in Asia this week, losing 1.1%.

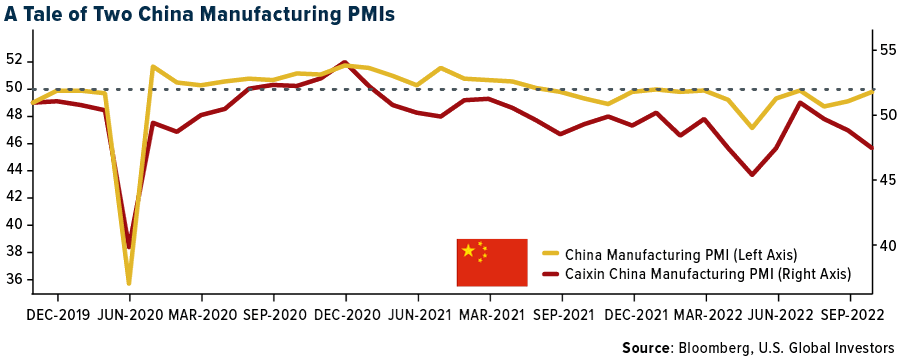

- Manufacturing PMIs in China once again are moving in opposite directions. The China Manufacturing PMI, which measures production activity among larger, state-owned companies, crossed above the 50 mark, while the Caixin China Manufacturing PMI, which measures production activity among smaller, private firms, fell deeper into contractionary territory. Hong Kong September Manufacturing PMI slipped to 48.0 from a preliminary reading of 51.2.

Opportunities

- China’s most important political meeting is scheduled for October 16, when the National Congress of the Chinese Communist Party will gather. The party will announce its five-year plan for the country’s economic growth, and during the meeting it is expected that President Xi will be re-elected for the next term. Many observers speculate that after the meeting is complete, China’s zero-Covid policy could be relaxed.

- CLSA, a global research broker with an Asia focus, believes the China healthcare sector will outperform, following an improving trend in China’s overall healthcare policy (and senior politicians in the Communist Party appearing to be paying closer attention to economic development). Lasty, CLSA said that the healthcare industry is entering a new round of a major product cycle with innovative drugs accounting for a majority of the projects.

- At the end of September, leaders from Poland, Norway and Denmark celebrated the opening of a new pipeline that will carry gas from the Norway via Denmark to Poland. Poland, like many other countries in central emerging Europe, depended on gas imports from Russia and the Polish government for years worked on diversifying the country’s gas imports, (opening an LNG port on the Baltic Sea and starting construction of the Baltic pipeline years back). The country has been cut off from Russian gas in April but will have no gas shortage in the winter.

Threats

- Reuters data shows that portfolio outflows continued in the month of September. Total outflows from emerging markets in the month of September stood at $2.9 billion and $12.7 billion year-to-date. Goldman Sachs has also been discussing a broader exodus from Asia ex-China of $111 billion year-to-date, exceeding $93 billion during the 2008 financial crisis.

- China is once again reporting a high number of Covid cases. This brings cases to a one-month high, climbing above 1,000, and likely driven by people traveling during the week-long holiday. Shanghai reported 11 new cases and a further spike in cases is expected due to travel during the Golden Week.

- Greece, Hungary, Italy, Romania, Spain, and the United Kingdom have implemented a windfall tax. The Czech Republic and Poland have published proposals to enact a windfall tax and Spain published a proposal to enact a second windfall tax, because the first one was diluted by a series of exclusions that left many energy providers out of its scope. Belgium, Finland, Germany, Ireland, the Netherlands, and Slovakia have either officially announced, or shown intentions to, implement a windfall tax, according to an article “What European Countries Are Doing about Windfall Profit Taxes,” published on October 4, written by Cristina Enache.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was crude oil, rising 16.42%. The 33rd OPEC+ ministerial meeting reconfirmed its existing plan and downwardly adjusted overall production by 2 million barrels per day (MMBbl/day) for the month of November from August 2022, the largest since 2020. The ministerial post-meeting statement cites concerns over uncertainties around the global economic and oil market outlook, and the need to enhance long-term guidance for the oil market. OPEC+ also extended the duration of the Declaration of Cooperation until December 31, 2023, adjusting the frequency of monthly meetings to every two months.

- The London Metal Exchange (LME) is launching a discussion paper that marks the first step toward a potential ban on new supplies of Russian metals, reports Bloomberg – and according to people familiar with the matter. Any move by the LME to block Russian supplies could have significant ramifications for the global metals markets, the article continues, as the country is a major producer of aluminum, nickel, and copper.

- According to Goldman Sachs, despite broader concerns around the state of global oil demand, refining equities have outperformed the Energy Select Sector SPD Fund (XLE) by 6% and the S&P 500 by 8% week-to-date. In its view, this is a function of 1) more bullish weekly inventory stats than consensus anticipated, with draws across crude, gasoline, and distillate, and 2) a recent strengthening in both Mid-Con and West Coast crack spreads as inventories, particularly for gasoline, remain incredibly tight.

Weaknesses

- The worst performing commodity for the week was wheat, falling 4.15%, as global stockpiles edged up with no shortage in the cards. The Grain Industry Association of Western Australia announced it would have a near-record harvest as weather conditions have been optimal. Coal stockpiles at U.S. power plants have plunged to a record low as railroad logistics have slowed shipping and surging global demand is pushing up prices, reports Bloomberg. U.S. prices have leaped past $200 a ton while Europe is scrambling to buy everything it can, pushing prices to nearly $300 per ton.

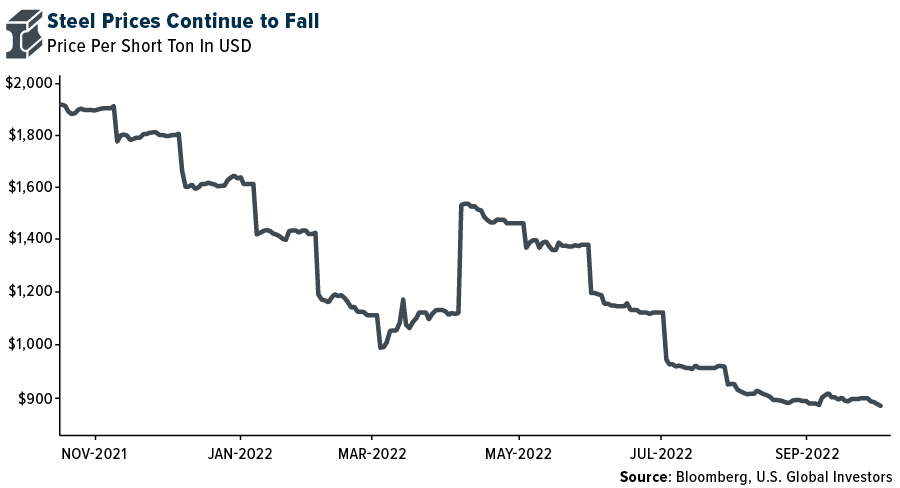

- According to BMO, U.S. spot steel prices resumed a downward trend, declining 2.5% to $780 per short ton. Among the key indicators, capacity utilization rates are at a 22-month low, while sheet product lead times remain low and are now declining, (both indicative of ample supplies and a soft demand environment).

- Copper production estimates were recently released by Chile’s statistics agency. The numbers suggest that August saw less than 5 million tons per year of copper output, down almost 10% year-over-year and the lowest August since 2006. These initial figures often differ from the more detailed Cochilco data, due for release later this month, however, there is no doubt that Chilean production is having a poor year.

Opportunities

- While electric vehicle (EV) batteries only account for 15% of global nickel demand, Chinese EV materials players are the most active investors in new nickel supply, globally. This is because nickel is by far the largest cost component, accounting for 80% of overall costs.

- While production was relatively range-bound through the first half of the year, the total U.S. gas rig count is currently 65% above the 2021 average, including a notable 54% increase in the Haynesville rig count to 71 rigs, (25 rigs above the 2021 average of 46 rigs). This lag in production is in some part due to normal supply chain constraints as well as localized constraints, including tightness on local gathering systems.

- The steel sector has not traded at such discounted valuations, and this could be an opportunity for investors. The low multiples are not a function of higher returns or peak earnings. The sector is trading at 2.1-2.8x EV/EBITDA for 2022-2023, already considering steel prices at $650 per ton. This compares to pre-pandemic multiples of 6-7x. Investors are already incorporating a de-carbonization charge—the capex needed to transform the old iron ore and coal route into green steel production.

Threats

- Goldman now expects a protracted period (>2 years) of lower production for European chemicals on the back of the region’s energy crisis. The group sees up to 40% of Europe’s chemical industry (petrochemicals and basic inorganics) at risk of permanent rationalization unless a sufficient economic assistance package is introduced, or natural gas prices fall to or below EUR70/MWh.

- The IEA released its inaugural World Energy Employment Report, highlighting a recovery in energy employment toward pre-pandemic levels, led by clean energy. That said, the report points out that market/policy uncertainty and labor shortages are contributing to disruptions and project delays in oil and gas. Labor Department data released Friday showed the unemployment rate in the oil & gas industry fell to 2.5% from 2.6% in the prior month. The industry has been reluctant to boost pay with rising costs. However, labor shortages in the oilfield have been one of the biggest challenges to boost production.

- Lithium prices have rallied 300% over the past year, reflecting the panic as consumers rush to secure supply. Consequently, the price has settled well above reinvestment economics. With the supply response improving, the lithium market could ease off this extreme short position into the middle of the decade.

Luxury Goods

Strengths

- According to Bloomberg, the S&P Global US Manufacturing PMI Index, which is one of the most important leading indicators and shows the expansion or contraction of the manufacturing sector, has increased. For September, it was reported at 52.0 vs. a consensus of 51.8 and a previous month of 51.8.

- India is set to become the world’s third-largest fashion market, reports Business of Fashion (BOF), and Bollywood’s most popular actress has become a global brand ambassador for the likes of Levi’s, Adidas, Louis Vuitton and now Cartier. Deepika Padukone is the new A-list ambassador for Louis Vuitton (as announced this summer), as well as the first ever Indian brand ambassador.

- Melco Resorts & Entertainment, an Asian company that operates casinos, restaurants, bars and resort facilities, was the best-performing S&P Global Luxury stock for the week, gaining 22.02%. Thanks to a relaxation of travel restrictions because of the Golden Week, shares jumped 9% and outperformed the Hang Seng Index.

Weaknesses

- According to Bloomberg, the University of Michigan Consumer Sentiment Index, which shows consumer behavior related to discretionary expenditures, has decreased. For September, it was reported at 58.6 vs. a consensus of 59.5 and a previous month of 59.5. It represents a decrease in consumer interest to expend money, including luxury goods. The United States is one of the leading luxury goods markets.

- Despite their reputation for being reliable performers during periods of turmoil, writes TheDrinksBusiness.com, the global wine and spirits giants have followed the markets down in response to the intensifying crisis in Ukraine, chaos in the energy markets and a sudden rise in interest rates. The world’s largest premium beverage alcohol producer, Diageo, has seen shares fall by a little over 6% since last holiday season, whereas European-based rivals have fared far worse. Across the Atlantic, however, both Constellation Brands and Brown Forman have weathered the storm much better than Wall Street overall, the article continues.

- Aston Martin Lagonda Global, a British company that design and manufactures automobiles, was the worst-performing S&P Global Luxury stock, losing 19.45%. Despite the investment of Greely Automobile Holdings, acquiring 7.6% of the British luxury car maker, the company continues with huge losses. In the first half of 2022, it has tripled to 285.4 million pounds from 90.7 million pounds a year ago.

Opportunities

- Hermes has opened a new impressive store in the heart of New York City, 706 Madison Avenue. The store has 20.250- square-foot. The store has 110 sales associates and five craftspeople to welcome their customers and at the same time be the ambassadors of their new strategy based on its sustainable and artisanal model.

- Based on an article from Vogue Business, luxury brands are investing in initiatives focused on teaching their customers about NFTs and crypto wallets because most do not know how to use them. For Example, Prada Crypted Discord group, the Gucci Vault, Rebecca Minkoff’s educational Zoom sessions, and others. It means luxury brands and the fashion industry, in general, are aware that the crypto world has arrived to stay. They must be part of it to keep relevant on the market and attract new generations of customers.

- When it comes to shopping, Gen Z knows how to balance discount purchases with luxury investments, reports GoBankingRates.com. This group of shoppers has a spending power of $143 billion. According to a recent survey, this generation of consumers listed 5 luxury item sub-groups they say are worth the price. These include electronic goods, technology, small business goods, wellness products and beauty products.

Threats

- According to Business of Fashion (BOF), today’s consumers might be trading their sneakers and hoodies for loafers and oxford shirts, underscoring a shift in the menswear fashion cycle and shifting away from the popular streetwear trend. While this could be seen a threat to brands who rely heavily on this theme of clothing, BOF explains that many younger brands like Daily Paper and Corteiz should not find any disruption in sales. In fact, these names are still finding success in the classic streetwear playbook, the article reads, selling logo-heavy clothing and merch to their loyal followings.

- One of the main challenges the luxury goods giant players face is the second-hand marketplaces. Because of its higher prices as a consequence of inflation, customers prefer to buy second hand products because of their lower price and environmental reasons related to consumption. According to a study from the consulting firm Bain & Co, the sales of second-hand luxury goods articles increased 65% compared with 2017, and they estimated an increase of this market by 15% in five years. According to WSJ, the new generation of customers has a new mindset. They buy a luxury good article, thinking about recovering between 70% and 80% of its value when they do not want to use it anymore and sell it through second-hand fashion e-commerce as The Real Real.

- China keeps doing lockdowns, scaring off the tourist and affecting essential industries such as luxury goods, considering that China is one of the leading markets worldwide. On the other hand, they have the gaming industry (including casinos), whose revenue fell 49.6% in September. It is because of China’s Zero-Covid policy to control the virus outbreaks. China’s new covid case climbed above one thousand for the first time in almost a month driven by people traveling during the week-long holiday, posting 1,138 new cases on Wednesday.

Blockchain & Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Casper, rising 21.84%.

- In Mastercard’s latest step into crypto, the credit card behemoth is leaning on a recently acquired blockchain analytics company to do due diligence on digital assets merchants, reports Bloomberg. The company is leveraging data from CipherTrace, acquired in 2021, to launch a solution that ought to keep Mastercard compliant with crypto regulation, the article explains.

- The European Union (EU) is looking to exchange views on the development of crypto legislation with U.S. officials during next week’s IMF-World Bank annual meetings. The EU is moving ahead with key legislation to regulate the crypto sector with common rules across all 27 member states, reports Bloomberg, marking the first time globally that lawmakers have attempted to supervise the industry on such a scale.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Unus Sed Leo, down 11.19%.

- The growth in Texas crypto-mining capacity will be stunted as Russia’s war on Ukraine drives up global energy prices and Bitcoin prices languish. Mining capacity in the Lone Star State will increase by 2 gigawatts to 3.5 GW by the first quarter of 2024, rather than the former forecast of up to 5 GW, writes Bloomberg.

- Executives at bankrupt crypto lender Celsius withdrew more than $56 million of cryptocurrencies before suspending customer withdrawals from the platform. Celsius CEO Alex Mahinsky, co-founder Daniel Leon, and CTO Nuke Goldstein withdrew the money largely from custody accounts, denominated in Bitcoin, Ether, USD and Celsius’ own CEL token between May and June, according to documents filed for the Southern District of New York, Bloomberg writes.

Opportunities

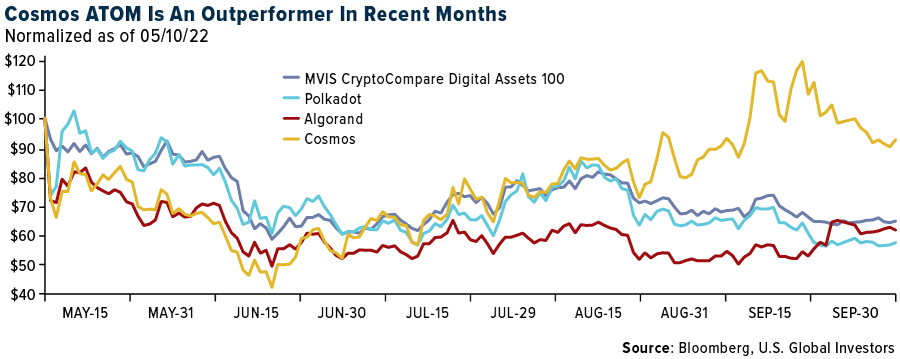

- Modular Asset Management’s crypto hedge fund has been buying tokens like Algorand and Polkadot in a bet that coins with stronger sustainability characteristics will outperform after a $2 trillion shakeout in digital assets, writes Bloomberg. The Modular Blockchain Fund has also stepped-up purchases of Cosmos in recent weeks. CIO Daniel Liebau said he is seeking to gain edge in choppy markets by picking coins he believes will better withstand rising scrutiny of the ESG characteristics of crypto, the article continues.

- Cboe Global Markets is making some real-time market data freely available over blockchain, as the exchange operator makes its entry into decentralized finance. The Chicago-based firm is joining the Pyth Network, the Jump Trading Group-backed decentralized publisher of crypto and other market data, as a contributor. It will provide data on 10 equities starting in the fourth quarter, reports Bloomberg.

- Grayscale Investments, the largest crypto asset manager, is shifting strategy during the midst of the market downturn by setting up an entity seeking to buy Bitcoin mining equipment at distressed prices. The Grayscale Digital Infrastructure Opportunities LLC will purchase the computer rigs used in mining and hopes to profit by selling the Bitcoin earned in the process, writes Bloomberg.

Threats

- Kim Kardashian will pay $1.26 million to settle SEC allegations that she broke U.S. rules by touting a crypto token without disclosing she was paid for the promotion. The SEC said Kardashian was paid $250,000 to post on her Instagram account about EMAX tokens, a crypto asset offered by EthereumMax, writes Bloomberg.

- A crackdown by the Taliban has led to a collapse in cryptocurrency use in Afghanistan following a surge last year when the nation was cut off from global banking and international aid. The value of crypto received by the country has fallen to an average of less than $80,000 a month since November, down from a peak of more than $150 million in September last year just after the Taliban swept back to power, according to a report by blockchain research firm Chainalysis.

- Top Bitcoin mining firm Marathon Digital Holdings disclosed it has over $80 million of exposure in the bankrupt data center firm Compute North Holdings. The total includes investments comprised of $10 million in convertible preferred stock of Compute North and $21.3 million related to an unsecured senior promissory note with the firm as well as $50 million in operating deposits to Compute North entities for its hosting services, writes Bloomberg.

Gold Market

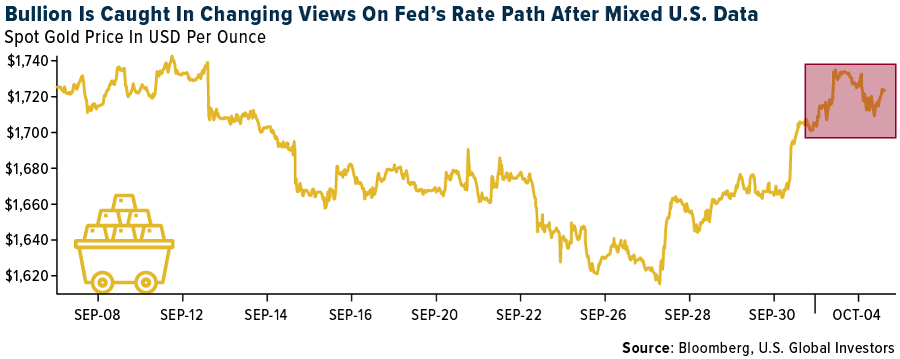

This week gold futures closed at $ 1,702.70, up $30.70 per ounce, or 1.84%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.36%. The S&P/TSX Venture Index came in up 2.34%. The U.S. Trade-Weighted Dollar rose 0.60%.

| Date | Event | Survey | Actual– | Prior |

|---|---|---|---|---|

| Oct-3 | ISM Manufacturing | 52.0 | 50.9 | 52.8 |

| Oct-4 | Durable Goods Orders | -0.2% | -0.2% | -0.2% |

| Oct-5 | ADP Employment Change | 200k | 208k | 185k |

| Oct-6 | Initial Jobless Claims | 204k | 219k | 190k |

| Oct-7 | Change in Nonfarm Payrolls | 255k | 263k | 315k |

| Oct-12 | PPI Final Demand YoY | 8.4% | — | 8.7% |

| Oct-13 | Germany CPI YoY | 10.0% | — | 10.0% |

| Oct-13 | CPI YoY | 8.1% | — | 8.3% |

| Oct-13 | Initial Jobless Claims | 225k | — | 219k |

Strengths

- The best performing precious metal for the week was platinum, up 6.48%. The increase may have been buoyed by a report by the Hydrogen Council in collaboration with McKinsey & Co. that notes that to reach the goals of the Inflation Reduction Act, there needs to be a tripling of current spending on green hydrogen production where platinum acts as a catalyst boost the production. Lundin Gold reported a strong third quarter 2022 production beat. Gold production was 122,000 ounces, 13% higher than the 108,000-ounces consensus, driven by better-than-expected head grade and improved recoveries.

- K92 Mining reported third quarter production of 32,995 gold equivalent ounces from its Papua New Guinea mine, up from 24,122 in the prior quarter. K92 noted the increased production came from processing 37% more ore through the mill at its Kainantu mine. The mine is currently outperforming the mill and the mill stockpile has reached its highest level since late 2020. Head grade to the mill averaged 8.67 g/t gold, 0.72% copper and 11.53 g/t silver with gold grades coming in 3% higher than budget.

- Gold soared the most since March at the start of the week, writes Bloomberg, helped by a continued decline in Treasury yields, as traders weighed concerns that central banks’ monetary tightening will lead to recession and the possibility that bond rates may have reached a peak. Although the yellow metal fell approaching week-end, bullion extended its first weekly gain in three as of October 2, as lower bond rates boosted the appeal of the non-interest bearing asset. However, gains were higher than expected in employment, initial jobless claims and nonfarm payrolls, which eroded about half of the gains gold made earlier in the week.

Weaknesses

- The worst performing precious metal for the week was palladium, but still up 0.70%. Exchange-traded funds (ETFs) cut 143,678 troy ounces of gold from their holdings in the last trading session, bringing this year’s net sales to 808,948 ounces, according to data compiled by Bloomberg. Gold fell near the end of the week, sliding toward $1,700 an ounce as traders assess whether the U.S. central bank may maintain its hawkish stance after a slew of mixed U.S. data, Bloomberg reports.

- Morgan Stanley expects Endeavour Mining to produce 318,000 ounces of gold during the third quarter, or 6% below its previous forecast, as the company provisions for a worse-than-expected rainy season in Senegal, impacting output at Sabodala-Massawa. The group also fine-tuned volume estimates at other mines, including Ity and Hounde, and lifted its all-in-sustaining cost (AISC) to $1,040 per ounce to reflect the lower production base. Therefore, its third-quarter EBITDA (earnings before interest, taxes, depreciation and amortization) now stands at $269 million versus the prior estimate of $296 million, compared to the consensus of $295 million.

- Gatos Silver released an updated mineral reserve estimate and plan for its Cerro Los Gatos mine, after the company announced in January 2022 that the 2020 technical report should not be relied upon, estimating 30%-50% of the metal content had been overstated. The updated estimate includes decreases of 32% silver, 37% zinc, 36% lead, and 35% gold after accounting for depletion. The revised plan has a mine life to 2028, with a 5% net present value (NPV) of $377 million on a 100% basis.

Opportunities

- Financing decisions are a key component to advancing a project in the mining sector, with the most common sources of financing being debt, equity, private equity, a royalty or stream on the asset, or a combination of these alternatives. Over the past decade, royalties and streams have become increasingly more mainstream, offering a competitive source of financing for mine operators. Further to the benefits to mine operators, these arrangements are beneficial to royalty and streaming companies, providing them exposure to the asset, usually for life of mine, and thus allowing them to share in future growth from project expansions, exploration potential and upside from commodity price increases, with more limited exposure to inflation.

- The World Platinum Investment Council (WPIC) estimates if China imports platinum at its current pace, the market will register a deficit of 800,000 ounces in 2023, increasing to 1 million ounces by 2025. That said, the WPIC has revised down automotive demand by 1.6% per year in its base case for the 2023-2026 period, albeit still up 8% per year. Mine supply growth has been moderated by 1% per year, and jewelry demand has lifted 4% per year, deepening annual deficits by 50,000 ounces per year.

- In a Bloomberg interview with Neal Froneman, CEO of Sibanye Stillwater, he noted that they expect the market to tighten further as some buyers seek to avoid Russian sourced palladium. MMC Norilsk Nickel PJSC currently supplies about 40% of world production from its Russian operations. Froneman said “We could see a real shortage of supply.” as platinum group metal producers in South Africa could lose 10% to 20% of their planned production if the current system of rolling power cuts are maintained by Eskom.

Threats

- Ibrahim Traore, a military officer in Burkina Faso, has formally announced a countercoup, removing the prior military leader, Paul-Henri Damiba, who took control of the government in January 2022. The new military leader has announced the government and constitution has been dissolved, and the country’s borders have been closed. Reportedly, the actions of the military are in response to increasing terrorist activity. IAMGOLD has not yet made a statement on its Essakane mine, which operates in Burkina Faso—the mine is unlikely to be directly affected by political instability, although logistics and productivity could be temporarily negatively affected. Essakane represents the overwhelming majority of IAMGOLD’s current cash flow, and potential operating disruptions could materially impact the company’s financial position.

- Victoria Gold (VGCX) production in the third quarter of 50,028 ounces met BMO’s expectations, but a conveyor failure at the end of the quarter will weigh on the fourth quarter with two to three weeks of expected ore stacking downtime. VGCX has retracted its annual guidance (previously 165,000 ounces) until the conveyor is back online; the company lowered its fourth quarter production estimates and now forecasts full-year production of 150,000 ounces, down from 159,800 ounces.

- Upon reflection, investors expressed their disapproval of the $27.5 million Gold Royalty transaction with Nevada Gold Mines this past week by selling the stock down more than 14%. Gold Royalties paid the consideration by issuing 100% of the proceeds in newly registered stock to Nevada Gold Mines at a deemed price of $2.93.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All