Anxious equity investors seeking comfort in market history might be reassured by the fact that large stock market declines tend to be followed by large gains.

After the brutal selloff of 2000-2002, for example, during which the S&P 500 nearly fell by a cumulative 37.6%, stocks recovered vigorously—rising 28.7% in 2003. Similarly, following 2008’s 37% drop, stocks roared back, gaining 26.5% in 2009.

We’ve been conditioned to expect dramatic reversals of fortune. And renowned academic Jeremy Siegel recently declared that stocks are “undervalued greatly.”[1]

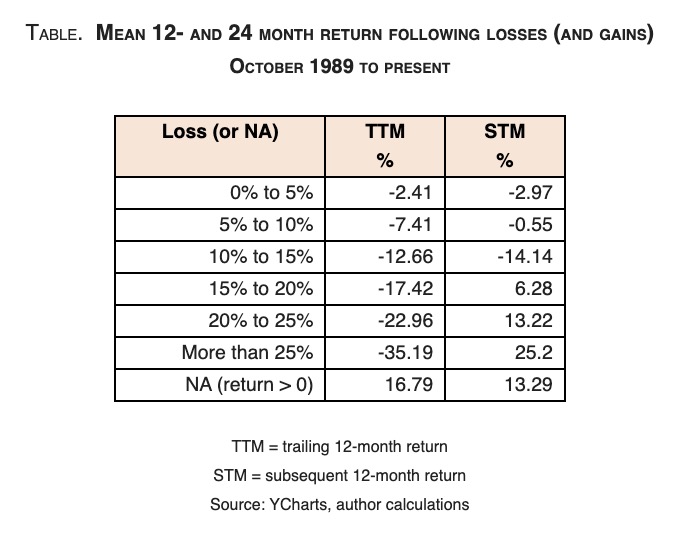

In fact, large losses do precede large gains, on average (table). Trailing 12-month (TTM) declines in the S&P 500 index in the 20% to 25% range, for instance, are followed by 12-month periods (subsequent 12-month return, or STM) during which stocks go up by more than 13%, on average. Typical recoveries from larger falls are even bigger.

Using averages of rolling before and after 12-month periods, an investor might conclude that the odds are in favor of a stock market bounce soon—perhaps in 2023 as hinted at by Professor Siegel last week.[2]

But a slightly more rigorous look at the data suggests a strong caveat. I test the relationship between TTM and STM returns using simple linear regression, first with no “controls” (i.e., holding nothing else constant). The estimated effect (“coefficient”) of TTM return on STM return is small—a 1 percentage point change in TTM return associated with a 0.01% change in STM return—and it isn’t significant statistically. To control for the stance of monetary policy, a widely recognized driver of equity market returns, I add a dummy variable for Fed tightening. I assign this variable a “yes” if the Federal funds rate (Fed funds) gradually goes up in each STM period, and a “no” if Fed funds if flat or falling. But the estimated effect of TTM return on STM return changes hardly at all (the estimated “coefficient” is about the same). And in both specifications, the R2 is tiny (about 0.01), meaning TTM return captures almost none of the variation in STM return.

Trailing-12-month return should probably not be used to forecast subsequent 12-month performance.

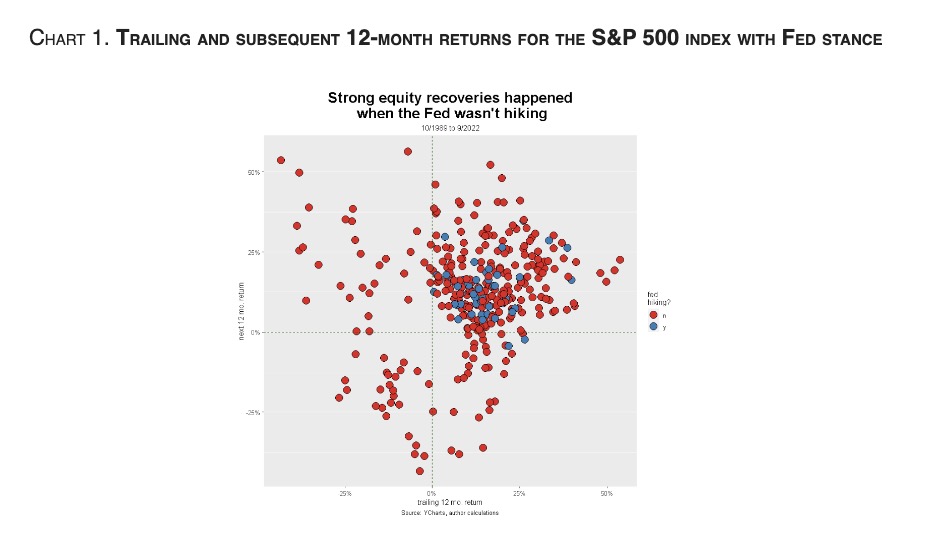

Visual inspection of the relationship between TTM and STM returns does, however, reveal two potentially interesting—and potentially discouraging—patterns.

The scatterplot in Chart 1 shows pairs of TTM and STM returns, each represented by a dot. The color of the dot denotes monetary policy stance. Using the same monetary policy stance definition as earlier, I color the dots blue for periods during which STM returns coincide with Fed tightening. Those pairs that don’t coincide with tightening are colored red.

What’s striking is that all instances of positive STM following negative TTM returns (those in the upper left-hand region bordered by the vertical axis above zero and the dashed lines) are red. Negative TTM returns have never been followed positive STM returns—using my definition of tightening and in the period from October 1989 to present, anyway. Thus, strength and speed of equity market recoveries may depend on whether the Fed is tightening.

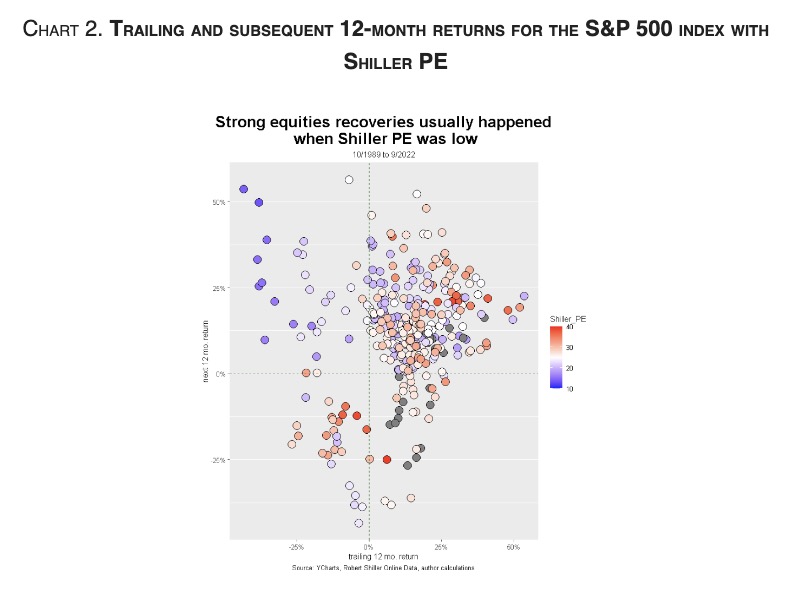

Another pattern emerges when I add equity valuations. The scatterplot in Chart 2 shows the same pairs of TTM and STM as Chart 1, but this time coded for starting equity valuations as measured by Robert Shiller’s cyclically adjusted price-to-earnings ratio (Shiller PE).[3] Lower valuations are denoted by blue, and higher by red. Strong equity market rebounds—again, the upper left-hand region—are almost always associated with low Shiller PEs in my sample.

Reasons for these patterns probably aren’t hard to figure out. Equites perform better following big drawdowns which result in lower, more attractive long-term, smoothed valuation measures and when the Fed’s either done tightening or trying to revive the economy (and markets) by lowering rates.

So, while investors can take some heart from past recoveries, they may have to wait until the Fed’s done tightening for equity-market fortunes to change. The next bull market may not start until both inflation and valuations are again low.

The author is an applied economist and portfolio strategist at Armstrong Advisory Group in Needham Massachusetts

ARMSTRONG ADVISORY GROUP – SEC REGISTERED INVESTMENT ADVISOR

The information contained herein including any expression of opinion, has been obtained from or is based upon, sources believed to be reliable, but is not guaranteed as to accuracy or completeness. This is not intended to be an offer to buy, sell or hold or a solicitation of an offer to buy, sell or hold the securities, if any referred to herein.

© Armstrong Advisory Group

Read more commentaries by Armstrong Advisory Group