$2.8 Billion Lithium Investment Expected To Jumpstart The “White Gold” Rush

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith this week’s announcement that the White House is deploying nearly $3 billion to boost domestic output of EV batteries and the minerals used to make them, it may be time for investors to take notice.

Is your portfolio positioned for a “white gold” rush?

In North America and the U.S. specifically, the hunt for lithium, a key component of batteries used in electric vehicles (EVs), has historically trailed a handful of other countries. That includes Australia, which mines more “white gold” than all other countries combined, and China, the leader in both lithium refining and lithium-ion battery production.

But with this week’s announcement that the White House is deploying nearly $3 billion to boost domestic output of EV batteries and the minerals used to make them, it may be time for investors to take notice.

In an October 19 press release, the Biden Administration said it was awarding $2.8 billion in grants to as many as 20 U.S.-based companies to “expand domestic manufacturing of batteries for electric vehicles and the electrical grid.” The lion’s share of the investment—part of the $1.2 trillion Bipartisan Infrastructure Law, signed in November 2021—will go to three companies involved in the production of critical minerals including lithium.

More than $114 million is set aside for Talon Metals, which will use the grant to support the construction of a battery minerals processing facility in North Dakota. In January of this year, the Minnesota-based company entered into an agreement with Tesla to supply 75,000 metric tonnes of nickel concentrate from its Tamarack Nickel Project in Minnesota.

Piedmont Lithium, one of our favorite industry plays, was selected to receive $141.7 million. The North Carolina-based company says the investment will go toward the construction of a new lithium project in Tennessee, which aims to supply up to 30,000 metric tonnes of lithium hydroxide per year.

Also based in North Carolina, Albemarle is the recipient of a $150 million grant. The company says this will help support the construction of a new lithium concentrator facility at its Kings Mountain location in North Carolina. Albemarle hopes to eventually have the capacity to produce up to “100,000 metric tonnes of battery-grade lithium per year to support domestic manufacturing of up to 1.6 million EVs per year,” the company said in a press release.

As context, the entire global lithium industry produced 100,000 tonnes in 2021, according to the U.S. Geological Survey (USGS).

Shares of all three companies traded sharply up on the news this week, with Talon Metals and Albemarle both gaining more than 13%, Piedmont Lithium more than 20%.

Weaning The U.S. Off Chinese Lithium Products

To impress upon you how much of a game-changer these investments are expected to be, the U.S. has been a virtual non-player in the global lithium game until now, with production limited to a single brine project in Nevada. Besides Australia and China, other big suppliers include Chile and Argentina, with Zimbabwe, Brazil and Portugal gaining ground.

This presents a national security issue, especially if the U.S. is to meet the Administration’s goal for EVs to make up half of all new passenger vehicle sales by 2030. Lithium is quite literally poised to become “the new gasoline.”

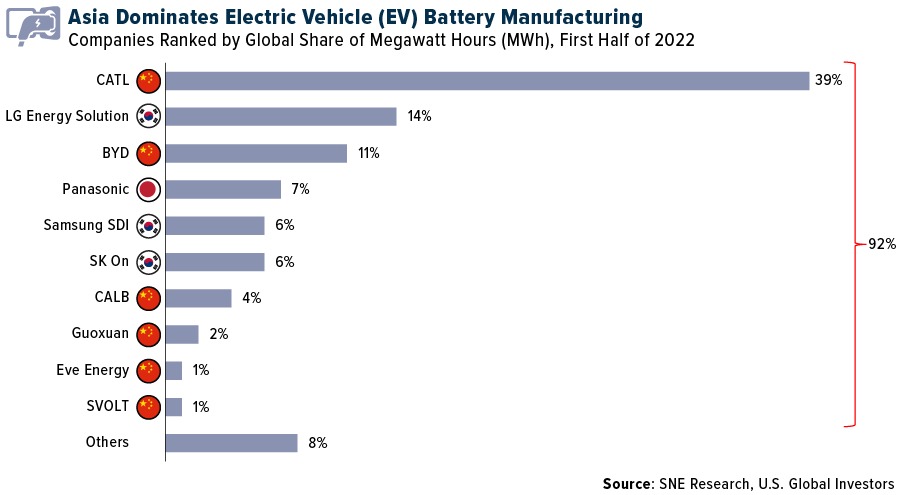

As for batteries, Asia is hands down the global leader in manufacturing, with only 10 companies accounting for 92% of the world’s supply. Close to two-fifths of all batteries are produced by a single Chinese company, Contemporary Amperex Technology Co. Limited, or CATL. Earlier this year, CATL introduced its EVOGO system, which allows Chinese EV drivers to swap out batteries at special stations in a fraction of the time it takes to charge them. The company now has plans to expand to international markets.

Driven by increasing global demand, lithium carbonate prices have exploded worldwide. But in China, where the renminbi has plunged to near-record lows against the dollar, a tonne of the stuff now trades at more than half a million yuan, or approximately $75,000. That’s up 13-fold in just two years.

What this means is that Chinese inflation is being exported alongside the physical batteries that CATL and its peers supply to Tesla, Ford and other U.S. carmakers. Bringing end-to-end production to the States would not only bolster national security but also stabilize prices. It might also give investors better investment options in more favorable jurisdictions.

Tesla Confirms Plans To Refine Its Own Lithium In Texas

During Tesla’s earnings call on Wednesday, CEO Elon Musk commented on lithium prices, calling them “crazy expensive.” He also confirmed that the company was moving forward with plans to build its own battery-grade lithium hydroxide refinery facility near Corpus Christi, Texas, just three hours south of Tesla’s headquarters in Austin.

I’ve often said that corporate investment and innovation should be the main driving force behind finding solutions to lower emissions, and I hope that Musk can deliver.

Although Tesla vehicle deliveries in the third quarter came in below expectations, largely due to logistics and shipping snarls, Musk expressed confidence in an “epic end of year.” He also shocked listeners by saying he believed that Tesla’s market cap would one day eclipse the combined market caps of Apple and Saudi Aramco, the world’s two most valuable companies. As I write this, Tesla’s valuation stands at around $661 billion, while Apple and Saudi Aramco’s is $4.5 trillion. No one’s ever accused Musk of lacking ambition.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 4.89%. The S&P 500 Stock Index rose 4.69%, while the Nasdaq Composite climbed 5.22%. The Russell 2000 small capitalization index gained 3.52% this week.

- The Hang Seng Composite lost 2.27% this week; while Taiwan was down 2.35% and the KOSPI rose 0.03%.

- The 10-year Treasury bond yield rose 20 basis points to 4.222%.

Airlines & Shipping

Strengths

- The best performing airline stock for the week was SAS, up 16.7%. According to UBS, in Latin America, October yields came in up 74% and November yields were higher by 57% year-over-year. December yields were up 39% year-over-year. Compared to 2019, October yields increased by 11%, while November yields grew 18%, and December yields increased 21%.

- Average crude tanker rates have increased 320% this year. Crude activity has not slowed in recent months as these vessel earnings are staying elevated from the positive tailwinds of shifted trade routes. Russian exports are moving much longer distances toward Asian countries while Europe is now importing most of its crude from the U.S. and the Middle East. This demand has led to considerable earnings premiums across vessel classes for the first half of the year.

- United Airlines reported third quarter 2022 adjusted net income of $927 million on revenue of $12.9 billion and guided fourth quarter unit revenue to an increase of 24%-25%. Adjusted earnings per share (EPS) is forecast to be $2.00-$2.25, ahead of consensus of $0.96. High load factors and unit revenue are driving strong demand that continues to grow versus 2019 levels.

Weaknesses

- The worst performing airline stock for the week was Wizz Air, down 4.7%. U.S. airlines’ trailing seven-day website visits decelerated year-over-year (but still up) to +13% for the week. Following Southwest Airlines’ winter fare sale last week, visitation stepped back to +18% year-over-year. The network carriers all saw visitation decelerate this week compared to last week (on a year-over-year basis).

- According to UBS, container import volumes were 6.4 million tons, which is below the four-week moving average of 6.7 million tons. On a four-week moving average basis, container imports in Week 40 were down 5.6% year-over-year. Imports have declined 14% from the June high and UBS believes a peak season bounce in the coming weeks is unlikely given the significant pre-shipping that took place earlier this year.

- Pilots of Lufthansa’s budget carrier Eurowings walked off the job for the second time in less than two weeks in Germany in the absence of a new workload offer from their employer, DPA reports, citing the pilots’ union Cockpit. Lufthansa still expects more than 230 of a scheduled 400 flights to take off.

Opportunities

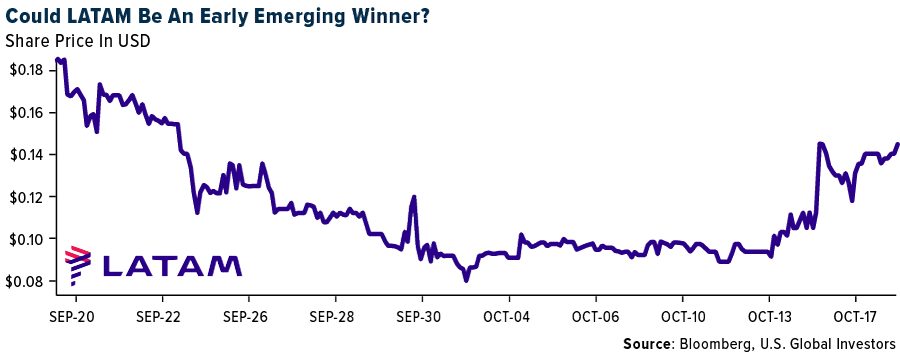

- Last Friday, LATAM Airlines announced that it plans to exit Chapter 11 on November 3 and it will have approximately 10.3 billion in equity and 6.9 billion in debt. On that date, the company will give shares and convertible bonds to shareholders and creditors and will pay certain obligations such as de Junior DIP and other fees as established in the Reorganization Plan.

- According to CIBC, Cargojet Inc. is not seeing any signs of volumes slowing down. CIBC expects the third quarter to be consistent with what was seen in the first half of the year, and the fourth quarter should be the strongest quarter in 2022. Customer conversations continue to point to a healthy volume environment.

- System net sales were 4.8% below 2019 for the week compared to 9.8% below 2019 last week as hurricane impacts ease. System volumes improved to -8.6% versus 2019 while system pricing improved by 4.2% versus 2019.

Threats

- According to JPMorgan, in the U.S. and Europe, the airline recovery appears to have stalled in volume terms (although very strong air fares mean that airlines on most sides of the Atlantic have printed much stronger revenue than many analysts expected). They cannot be sure why the volume recovery has slowed in the U.S. and Europe, but there are several possible reasons: a shortage of staff for airports and airlines, weaker economic growth, and less transit traffic from Asia into these markets.

- The Evercore ISI Shipping Companies Survey has declined slightly, as bulk shipping pulled back and tanker activity improved. The survey is modestly off the highest level since 2006.

- Bank of America’s high frequency travel tracker shows that the Chinese domestic air travel weakened to 35% of normal levels in the first half of October. The recently announced increase in Chinese international flights does not look significant with timetabled seat data suggesting capacity back to only 9% of normal in the fourth quarter.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 8.8%. The best performing country in Asia this week was Malaysia, gaining 4.5%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 2.8%. The South Korean won was the best performing currency in Asia this week, gaining 0.5%.

- European stocks recorded gains this week, supported by the political changes taking place in the U.K. Western Europe, as measured by the STOXX Europe 600 Index (SXXP) gained 2% over the past five days, while equites in eastern Europe, measured by the MSCI EM Europe Index (MXMU) surged 6% higher in the first four days of the week.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Poland, gaining 0.4%. The worst performing country in Asia this week was Hong Kong, losing 1.6%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 0.4%. The Indonesia rupiah was the worst performing currency in Asia this week, losing 1.0%.

- China’s Communist Party is holding its 20th party congress this week, during which a release of important economic data has been postponed with no explanation provided. Investors worry that the GDP data could be released weaker than expected due to ongoing Covid restrictions in the Asian nation.

Opportunities

- Hong Kong’s chief executive John Lee announced new measures to help retain talent in Hong Kong and stop the exodus that started a few years back when China attempted to bring Hong Kong closer to the mainland. The city will ease visa rules for job-hunting graduates and cut property taxes for people without Hong Kong residency. Currently, non-permanent residents pay 30% tax on new property purchases.

- The United Kingdom’s stock market is now expecting some stability after recent volatility due to the new Prime Minister, Liz Truss’, decision to drastically cut taxes. This week, the new Finance Minister reversed almost all tax cuts accounted three weeks ago by Truss. Later in the week the newly elected prime minister resigned after holding the PM position for only 45 days; equites gained, and the British pound appreciated against the dollar. The U.K.’s new prime minister could be announced on Monday.

- Turkish equities continue to outperform, supported by strong gains in banks. The Central Bank of Turkey cut its one-week repo rate to 10.5% from 12%, following President Erdogan’s call for a one-digit rate during times when inflation in the country is at 83% on a year-over-year basis. Turkish banks are likely to report strong quarterly results, supported by low funding costs and high lending rates.

Threats

- We question if the recent rally in Turkish equities can last much longer. As mentioned above, Turkey’s central bank once again cut its one-week repo rate to 10.5% from 12%. Most likely, wages will have to be increased significantly to compensate for the rising cost of living. Turkey has a large account deficit but has been able to balance its book supported by larger inflows to the central bank. The question now is whether the government will be able to support its economy and protect its currency from further depreciations, particularly during times of low rates and record high inflation.

- Russian President Vladimir Putin declared martial law in the four illegally annexed regions in Ukraine and is planning to impose new restrictions in order to have better control of the territory. Meanwhile, Ukraine is counterattacking, possibly preparing to retake Kershon, a city of 250,000, with key industries and a major port. Ukraine claims that a third of the country’s power stations have been destroyed in Russian strikes since October 10, causing blackouts and water shortages throughout the country.

- Shanghai announced a plan to build a 3,250-bed Covid facility near the city center, confirming that the country is unlikely to exit its zero-Covid policy any time soon. Shanghai is also recruiting almost 1,000 people on two-year contracts to staff testing stations and manage logistics.

Energy & Natural Resources

Strengths

- The best performing commodity this week was once again lumber, up another 9.31%. With mortgage rates soaring, lumber is going up along with, what might be, the start of some production cuts across the industry. This week, Vancouver-based Interfor, one of the biggest lumber producers in the world, announced it is cutting fourth quarter production by 17% due to deteriorating economic conditions.

- Schlumberger posted its best profit in seven years this week and noted fourth quarter sales look to be on pace for growth in the mid-20% range compared to last year. The company highlighted that, contrary to an OPEC+ output cut of 2 million barrels per day, it sees an acceleration of the pace of drilling and expects activity to increase in the Middle East.

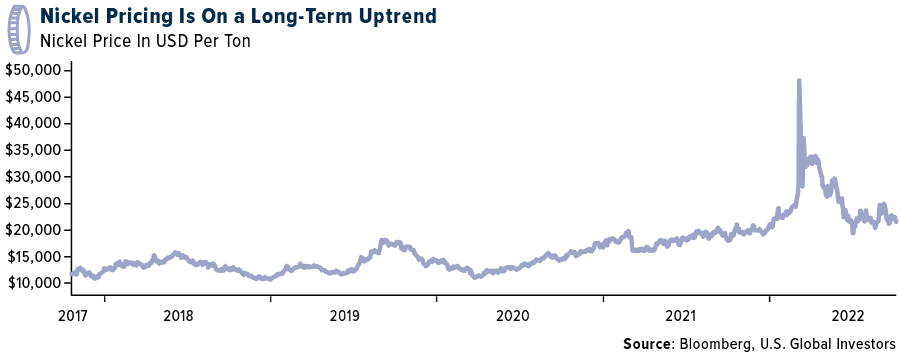

- This is the first year in nickel’s history that the surplus has not emerged in class 1 nickel metal. Surpluses have emerged in class 2 nickel pig iron and ferronickel as well as in stainless steel scrap and intermediates. The price for class 1 nickel has moved to an unprecedented premium to class 2, which is trading at $5,000-$6,000 per ton below the LME price.

Weaknesses

- The worst performing commodity this week was natural gas, down a whopping 22.45%, marking its ninth consecutive weekly loss as winter stockpiles expanded more than the five-year average last week. Recession fears may be impacting a robust diamond market up until now. De Beers notified its diamond buyers that they can purchase stones on sweetened terms at its next sale. Diamond prices had been rising but it appears stones from Russian diamond miner Alrosa started to make their way into the market while Chinese lockdowns have curtailed shopping.

- China told its state-owned gas importers to stop reselling LNG to energy-starved buyers in Europe and Asia in order to ensure its own supply for the winter heating season.

- Iron ore added to five weeks of declines after Chinese President Xi Jinping offered no immediate prospect of changes to policies that have ravaged steel demand over the past year. Demand remains weak, according to Chen Wenguang, research director at Lange Steel Information Research Center. That’s been reflected by last week’s dive in spot steel prices, while the recent spread of Covid in the nation has further dampened traders’ confidence, he said.

Opportunities

- This week, the U.S. Department of Energy awarded $2.8 billion in grants for 20 projects in 12 states to help wean the U.S. off Chinese and Russian minerals imports. This is the first round of a larger $7 billion package passed into law last year. The focus is on lithium, graphite and other minerals that are used in electric vehicles. Talon Metals and Piedmont Lithium both received grants for advancing their projects.

- Rio Tinto Group signaled a change in strategy to refocus on dealmaking amid concerns about missing out on future growth. Bloomberg reports that Rio Tinto has asked major investment banks to showcase lithium companies that might help the miner to expand into battery metals. Back in June, Rio Tinto purchased a 4.63% stake in Nano One, which has proprietary cathode manufacturing technology and an LFP fabrication plant acquired from Johnson Matthey. World lithium supplies need to grow fivefold by the end of the decade to meet the growing demand for electric vehicles.

- According to Bank of America, in the fertilizer industry, after a multi-month seasonal lull, the bank expects buying in the northern hemisphere to resume in the coming months, which should provoke higher prices. The bank believes the U.S. will have tight nitrogen supplies ahead of spring planting. Lofty grain futures reflect tight global supplies for the next several years, which is strongly supportive of fertilizer prices, owing to the impact on buying patterns, resulting in very high correlations.

Threats

- North American flat steel found a temporary price floor in the third quarter when mills raised prices, driven by the decline in the import arbitrage and underlying imports. Price support, however, has been short-lived. The outlook remains volatile given the risk of lower Chinese construction activity coupled with higher iron ore supply driving down iron ore prices and, in turn, steel prices into next year.

- Supplies of heating oil are in such short supply in the U.S. Northeast that fuel is already starting to be rationed to customers in Connecticut, reports Bloomberg. Fuel stockpiles in New England are a third of seasonal norms and New York is running tight, too. Adding to the pain, wholesale heating oil in New York Harbor is averaging about $4.09 a gallon compared to $2.46 a year ago.

- LNG imports in the EU and the U.K. are on track to reach record levels this year, but supply capacity for new seaborne LNG exports remain inelastic in the short run. This has led to a dynamic of Asian LNG buyers reexporting their contracted volumes from the U.S. to Europe. Asian buyers have collected a wide gas spread, which has helped supply European shortages.

Luxury Goods

Strengths

- Luxury watches continue to sell well. Swiss watch exports were up 19% in September versus 15% in August on a year-over-year basis. Wealthy consumers continue to buy luxury watches, some as means to hedge against inflation and preserve assets during times of economic uncertainty.

- The super-rich are buying properties in Dubai and most of these transactions are paid for in cash. Real estate prices in the UAE surged 70.3% over the past 12 months through September, making it the biggest gainer on Knight Frank’s Global Index, which focuses on a city’s most desirable and most expensive homes. For comparison, London prices increased only by 2.5%, Paris 8.9%, and New York 7.3%.

- Brilliant Earth Group, a jewelry retailer, was the best performing S&P Global Luxury stock for the week, gaining 27.68%. This week, the company announced the launch of its Cocktail Rind Collection made by natural and lab grown gemstones, ranging from $2,000 to $8,000 and available for purchase at the company’s showrooms.

Weaknesses

- Kering SA posted slower sales growth than its luxury rivals including Luis Vuitton and Hermes International during the third quarter. The company has higher exposure to China where sales were negatively impacted by ongoing Covid lockdowns.

- The Emles Luxury Goods ETF (LUXE) that invests in a portfolio of global, high-end products and services closed for trading as of October 19. The ETF’s inception date was November 24, 2020.

- Wynn Macau, a hotel and casino operator located in Macau, was the worst performing S&P Global Luxury stock for the week, losing 19.26%. Shares have been declining on speculation that gaming group tours from mainland China may not resume anytime soon.

Opportunities

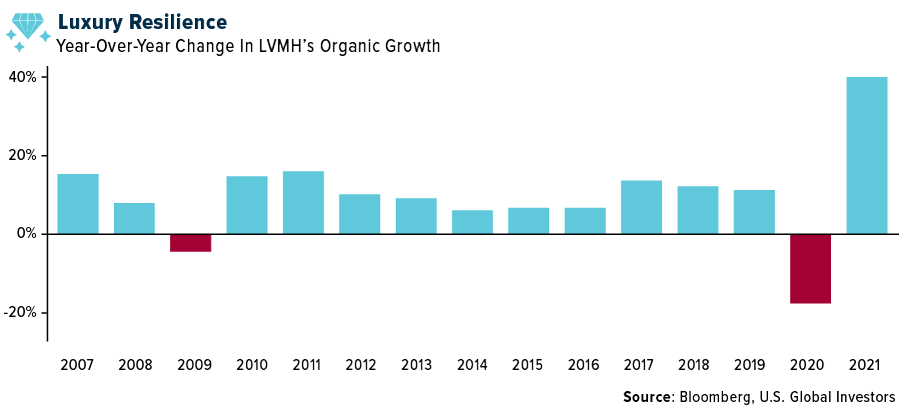

- Luxury brands are posting strong results. Last week, the world’s biggest luxury company, Louis Vuitton, posted strong sales. This week, Hermes International reported strong sales as well, posting a 24% sales increase in the third quarter, above expectations of a 15% increase, proving that luxury goods are in high demand despite talks about an upcoming global recession. Since 2007 Louis Vuitton has seen only two years where revenue fell (in 2009, right after the financial crisis, and in 2020, due to the Covid-19 outbreak). Both years were followed with strong sales recoveries.

- Two major festivals are coming up in India (Dhanteras and Diwali) which will present shopping opportunities for consumers. At the upscale DLF Emporio, one of the major luxury malls in New Delhi, the festival spirit is high, and business is good, Bloomberg reports. Consumers feel like life is back to normal and want to celebrate Diwali in good health and hope. India is one of the fastest growing luxury markets in the world.

- S&P Global’s U.S. Manufacturing PMI is expected to remain in expansionary territory. The data will be released next week on October 24. Bloomberg economists predict the number to fall to 51.0 in its preliminary reading for October, down from 52.0 in September, but remaining above the 50 level that separates growth from contraction.

Threats

- Luxury goods companies have been raising prices due to higher cost of production, and many may continue to do so. Hermes CFO warned that 5%-10% price hikes may come in January, compared to an increase of about 4% this year. A Birkin bag that currently costs EUR 7,400 ($7,424) in France today, next year may sell for EUR 8,140.

- Shares of companies that build houses may continue to decline in the United States. On Wednesday, economic data showed U.S. housing starts declined and mortgage applications fell with rates moving higher. The thirty-year mortgage rate is at 7.2%, up from 3.3% at the beginning of the year.

- China’s October ex-auto sales could rise less than 1% from a year ago for a second straight month. This year’s growth will only meet half of the consensus estimated at a 2.7% gain, Bloomberg reports. Sales have been negatively affected by renewed lockdowns in the country. Recent comments emerged that China may be willing to amend its zero-Covid policy no sooner than late next year.

Blockchain & Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Casper, rising 33.34%.

- JPMorgan Chase & Co. has hired a new head of digital assets regulatory policy, less than a month after CEO Jamie Dimon told lawmakers that cryptocurrencies are “decentralized Ponzi schemes.” Aaron Iovine joined the company this week as executive director for digital assets regulatory policy, reports Bloomberg, a newly created role. He was previously head of policy and regulatory for cryptocurrency lender Celsius Network writes Bloomberg.

- Crypto billionaire Sam Bankman-Fried has outlined a framework for limiting the impact of the hacks and exploits plaguing the industry, including capping the maximum bounty for attackers at $5 million. Bankman-Fried proposed in a blog post what he called a “5-5 standard,” where hackers keep either 5% of the amount they’ve taken from a protocol or $5 million, whichever is smaller, according to a Bloomberg article.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was TerraClassic, down 23.99%.

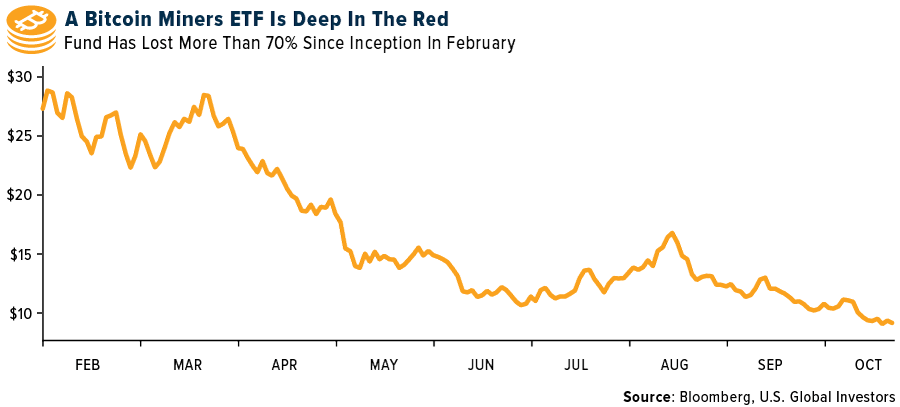

- Bitcoin miners have been pummeled by low Bitcoin prices, soaring energy costs, and steep competition in the industry. These firms had rushed to the equity market to raise money during crypto’s bull run, when investors expected Bitcoin prices to surge, and publicly traded miners were seen as an efficient way to invest in the sector, writes Bloomberg.

- German cryptocurrency exchange Nuri has closed its business after struggling to find investors, reports Bloomberg. The Berlin-based exchange with over 500,000 customers filed for insolvency in August after challenging market developments and subsequent effects of financial markets. Customers have been asked to withdraw funds by December 18 and trading will be possible before November 30, the article explains.

Opportunities

- Mastercard debuted a service that will let consumers buy and sell digital assets through their bank accounts, potentially paving the way for thousands of finance firms to offer crypto trading for the first time. The product, called Crypto Source, will start in the U.S., Israel, and Brazil early next year though a pilot program, Ajay Bhalla, Mastercard’s president of cyber and intelligence, said in an interview, writes Bloomberg.

- N26 will start offering cryptocurrency trading to its customers via a partnership with Bitpanda GmbH following similar moves by the digital bank’s peers, writes Bloomberg. The product will be offered in Bitpanda’s home market of Austria first and then rolled out more broadly over the next six months.

- Fidelity Investments is hiring an additional 100 people for its digital assets unit, stepping up an expansion that started in May and taking advantage of turmoil among crypto firms to lure talent. The new round of hiring will bring Fidelity Digitals Assets’ headcount to roughly 500 by the end of 2023’s first quarter, writes Bloomberg.

Threats

- FTX trading and its billionaire founder Sam Bankman-Fried are being probed by the Texas securities regulator over whether certain lending offerings violate state law, reports Bloomberg. Texas is investigating whether the company’s yield-bearing crypto accounts are illegal securities offerings being sold to U.S. residents. Until the state determines FTX is complying with the law, the agency said the company shouldn’t move forward with its $1.4 billion purchase of Voyager assets announced last month, the article explains.

- Crypto lender Voyager Digital is pursuing settlements with two top executives after an internal probe uncovered potential claims of gross negligence stemming from risky loans made to defunct hedge fund Three Arrows Capital. CEO Stephen Ehrlich, in consultation with then CFO Evan Psaropoulos, agreed to let Voyager lend nearly $1 billon of crypto to Three Arrows despite extremely limited financial disclosure from the hedge fund, writes Bloomberg.

- Silvergate Capital shares slumped as much as 10% in premarket trading after the crypto-focused bank reported third-quarter results that missed the average analyst estimate. Silvergate Exchange Network handled $112.6 billion of U.S. dollar transfers in the third quarter of 2022, a decrease of 30% compared to $162 billion in the second quarter, writes Bloomberg.

Gold Market

This week gold futures closed at $1,659.70, down $10.80 per ounce, or 0.65%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.94%. The S&P/TSX Venture Index came in off 2.07%. The U.S. Trade-Weighted Dollar rose 1.31%.

| DATE | EVENT | SURVEY | ACTUAL– | PRIOR |

|---|---|---|---|---|

| Oct-18 | Germany ZEW Survey Expectations | -66.5 | -59.2 | -61.9 |

| Oct-18 | Germany ZEW Survey Current Situation | -68.5 | -72.2 | -60.5 |

| Oct-19 | Eurozone CPI Core YoY | 4.8% | 4.8% | 4.8% |

| Oct-19 | Housing Starts | 1461k | 1439k | 1566k |

| Oct-20 | Initial Jobless Claims | 233k | 214k | 226k |

| Oct-17-31 | China Retail Sales YoY | 3.5% | — | 5.4% |

| Oct-25 | Hong Kong Exports YoY | — | — | -14.3 |

| Oct-25 | New Home Sales | 580k | — | 685k |

| Oct-26 | ECB Main Refinancing Rate | 2.000% | — | 1.250% |

| Oct-27 | GDP Annualized QoQ | 2.3% | — | -0.6% |

| Oct-27 | Durable Goods Orders | 0.6% | — | -0.2% |

| Oct-27 | Initial Jobless Claims | 225k | — | 214k |

| Oct-28 | Germany CPI YoY | 10.1% | — | 10.0% |

Strengths

- The best performing precious metal for the week was silver, up 6.58%. Silver ETFs saw inflows last week for the first time in almost six months as short interest retreated from 10-year highs. The outflow of physical silver from vaults also continued in September with levels reaching record lows and down 26% since the highs in June 2021. Global ETF holdings of 750 million ounces remain almost 30% off from 2020 highs, but well above pre-pandemic levels around 600 million ounces.

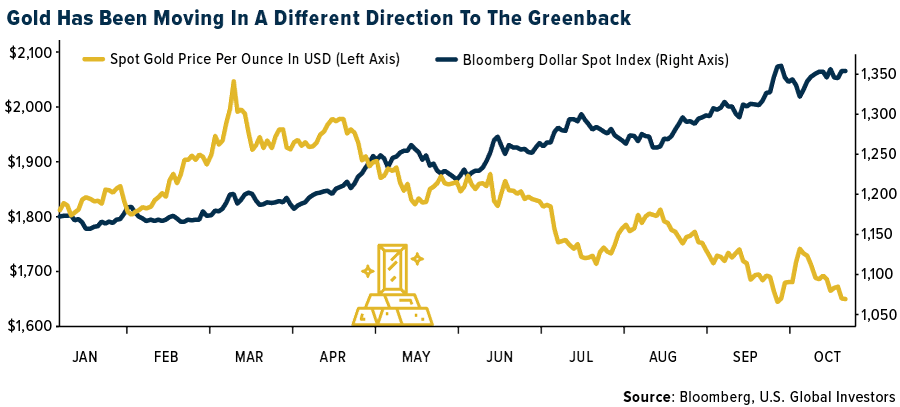

- Gold advanced on weakness in Treasuries and the dollar, as rising fears of a global economic slowdown boost the precious metal’s haven status. The gain comes after bullion last week traded near the lowest level since the end of September, dropping 3% amid expectations of more aggressive rate hikes by the Federal Reserve. On Friday, the BOJ defended its currency, which was off as much as 1%, to push the value of the yen higher by 2%. Consequently, gold rallied more than 1.5% on Friday.

- According to Stifel, IAMGOLD (IMG) announced entering into an agreement with Zijin Mining to sell IMG’s interest in Rosebel Gold Mines for $360 million cash and the transfer of $41 million in liabilities. Stifel believes IMG is getting a reasonable price for an asset that requires significant reinvestment, and it is negative net free cash flow for IMG now. Importantly, this is a material step toward reducing the funding gap to complete Côté.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 0.65%. Wesdome Gold Mines’ production of 22,883 ounces missed consensus of 29,400 ounces as maintenance work at Eagle River and Kiena impacted throughputs during the quarter. Wesdome is targeting the lower end of its 120,000-140,000-ounce guidance in 2022.

- At midweek, gold held a three-week low, reports Bloomberg, as speculation the Federal Reserve will keep aggressively tightening monetary policy and trigger a recession had investors again seeking shelter in the U.S. dollar. Renewed strength in the greenback has now seen bullion tumble more than 20% since a March peak, the article continues.

- Mandalay Resources reported third quarter production of 27,000-30,000 ounces gold which was below consensus of 33,000-37,000 ounces gold. The company has attributed the production miss to lower grades and Covid-related absenteeism. As a result, Mandalay has adjusted its annual production guidance down from 118,000-130,000 ounces gold to 106,000-115,000 ounces gold.

Opportunities

- The London Bullion Market Association gathered in Lisbon for its annual conference. Members from the world’s top bullion traders, refiners and miners always have an annual gold price forecast for one year forward. Despite gold being down about 20% since March, consensus forecast is for gold to trade around 10% higher in one year. The surprise standout was silver which is predicted to boom 50%, as reported by Bloomberg.

- Barrick Gold Corp. President and Chief Executive Mark Bristow says the process of completing the final agreements and legal steps that would enable the development of the Reko Diq project is making steady progress. Once the transaction is complete, Reko Diq, one of the largest undeveloped copper-gold deposits in the world, will be owned 50% by Barrick, 25% by Balochistan province, and 25% by major Pakistani state-owned enterprises.

- B2Gold reported consolidated gold production of 215,000 ounces, 39,000 ounces lower than the consensus of 254,000 ounces. Results were below forecasts at each operation, where Fekola was impacted by the rainy season, Otjikoto’s underground ramp-up was delayed, and Masbate processed greater sulfide material. Despite lower third quarter output, the company reiterated full-year corporate production guidance, implying output of 330,000 ounces in the fourth quarter, a considerable 53% improvement quarter-over-quarter.

Threats

- As a result of lower realized commodity prices and potential operational challenges experienced at the asset or a delay in access to higher grades, earrings may be at risk. As margins narrow, royalties/streamers and companies with less exposure to operating and capital cost escalation, such as AEM, could do well.

- St Barbara (SBM) had a weak first quarter, with Gwalia labor issues forcing an 8% gold downgrade to fiscal year 2023 guidance. First quarter gold of 63.7 missed consensus by 9% on Gwalia labor issues and a major storm event at Atlantic. AISC was 13% above consensus at an elevated A$2,490 per ounce. SBM has lowered its fiscal year 2023gh Gwalia mine tonnage expectations to 950,000 tons from 1.1 million tons, with site gold guidance falling 14%.

- Worldwide diesel fuel is in short supply and that is pushing up costs for miners across the globe. Open-pit miners with lots of ore and waste haulage will be impacted the most as few miners, outside of Alamos Gold, have hedged their fuel risks.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

Endeavour Mining

Barrick Gold Corp

B2Gold

Mandalay Resources

Wesdome Gold Mines

IAMGOLD Corp.

United Airlines

Southwest Airlines

Kering SA

Louis Vuitton

Hermes International

Schlumberger NV

Interfor Corp.

Talon Metals Corp.

Piedmont Lithium Inc.

Nano One Materials

Tesla Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Free cash flow (FCF) is the cash a company generates after taking into consideration cash outflows that support its operations and maintain its capital assets.

The Bloomberg Dollar Spot Index tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar.

The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All