Doll's Deliberations - Weekly Investment Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY:

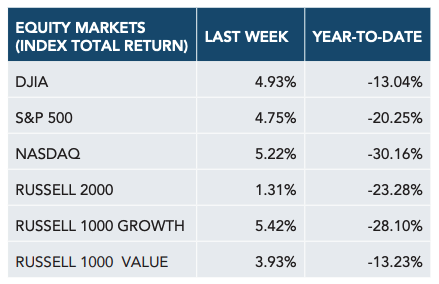

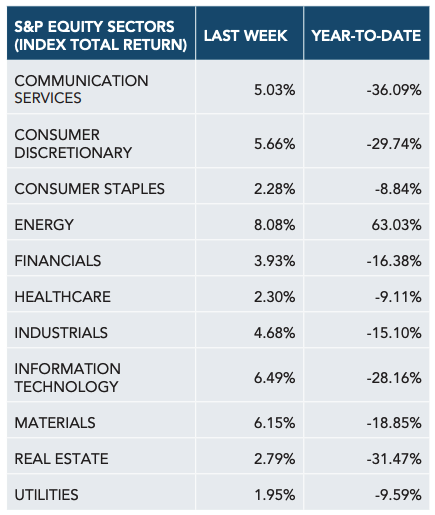

Stocks rose last week (S&P 500 +4.7%) after falling to a 2.5 year low the week before. The increase was attributable to technical and sentiment reasons, but also Q3 earnings reports coming in less bad than feared. Best sectors were energy (+8.1%), technology (+6.5%), and materials (+6.2%); worst sectors were utilities (+2.0%), consumer staples (+2.2%), and healthcare (+2.3%).

KEY TAKEAWAYS:

1. The Fed’s tone has shifted recently with several FOMC members acknowledging that the pace of tightening will need to moderate in the coming months. This could cause the Fed to reduce the pace of tightening in December and then pause rate hikes early next year.

2. A number of indicators have suggested that inflation pressures may be starting to ease (e.g., wage pressures.)

3. A further decline in the leading economic indicators (LEI) coupled with an increasingly inverted yield curve raises the probability of a recession in 2023.

4. 30-year fixed mortgage rates are up more than 400bps since the 2021 low, mortgage applications have fallen more than 50%, and the new and existing home sales have fallen more than 25%. So far, however, home prices are still rising.

5. S&P 500 2023 estimated earnings peaked in July at just above $250. Estimates have recently fallen to below $240. We think the number may come in closer to $200.

6. The soaring dollar is exporting inflation to the rest of the world and putting pressure on foreign central banks to raise their rates more aggressively. Credit crunches and hard landings are more likely overseas than in the U.S.

7. Undecided voters are breaking towards the Republicans. If this continues, U.S. voters will have removed the party in power in eight of the past nine elections. Increased political volatility increases policy uncertainty.

8. Many market breadth measures indicate that sentiment is depressed. From a contrarian perspective, this implies that U.S. stocks are meaningfully oversold and potentially ready for a rebound.

9. A bullish narrative could be 1) inflation has peaked and is now falling, 2) the Fed will cease interest rate increases post year-end, and 3) earnings continue to hold up better than expected. The probability of these actually occurring seems to be increasing.

10. Small stocks (Russell 2000) are selling at the lowest relative multiple since the bursting of the tech bubble in 2000-2001, and typically outperform once a recovery starts.

SUSTAINED RALLY IN STOCKS REQUIRES CALM BOND MARKET

Global equities attempted yet another rally and again have run into an uncooperative bond market. Weakness in bonds reflects ongoing concerns that inflation will prove sticky, which in turn increases equity investors’ concerns that the endpoint will be a recession. Although many leading inflation measures have rolled over, the impact has yet to show up in actual CPI. As we know, central banks belatedly and aggressively responded to the surge in global inflation. In addition, the war in Ukraine, Europe’s energy crisis and China’s Covid-zero policy have all added to inflation and economic strains.

One silver lining is that global equities and bonds are deeply oversold, while the U.S. dollar is extremely overbought. The bar for a solid positive rebound in financial asset prices is rather low, given the gloomy current outlook. We remain more upbeat than consensus on underlying economic resilience, although we are also more concerned than the consensus about the longer-term inflation outlook. Nevertheless, there are good prospects for a decent reprieve rally provided that this year’s bad news gives way to better news (or even just less bad news), starting with at least some easing in inflation from 40-year highs. Cyclically, however, we doubt that a new bull phase will emerge until it is clear that inflation will sustainably return to low levels. Here the odds are still low.

So far, corporate earnings have only been downgraded modestly, while equity valuations have declined considerably. Q3 corporate earning season so far has shown acceptable underlying profitability and better than headline economic numbers and sentiment suggest. The solid recent results from U.S. banks underscore that conditions are far from recessionary. The downside of relatively good corporate results, however, is that it also reflects the increase in pricing power (higher inflation).

To summarize, a more durable rally may develop due to an oversold condition, horrible sentiment, Q3 earnings not bad (especially banks), more reasonable valuations, short covering, and renewed thoughts that the Fed may finish raising rates by year-end. We continue to think stocks have moved from free-falling (January 3 – June 16) to volatile side-wise trading (stocks are up from the June 16 low four months ago) and that the bulls and bears will both continue to be frustrated. A sustained move to the upside probably requires the bond market to calm down.

CONCLUSION:

Periodic tactical opportunities to go long risk assets are expected to develop whenever inflation pressures ease and bond markets calm, especially since the global economy is more resilient than is widely believed. There are good odds of such a development in the coming months once the Fed turns less hawkish. However, the cyclical global outlook remains worrisome, since a return to low inflation is unlikely absent a recession. A potential for dislocation (credit or liquidity problems) is possible (most likely outside the U.S.) given the quick pace of central bank interest rate increases.

Data from Bloomberg, as of 10/21/2022.

Crossmark Global Investments, Inc. (Crossmark) is an investment adviser registered with the Securities and Exchange Commission that provides discretionary investment management services to mutual funds, institutions, and individual clients. Investment advice can be provided only after the delivery of Crossmark’s firm Brochure and Brochure Supplement Form ADV (Parts 2A and 2B) and Form CRS, and once a properly executed investment advisory agreement has been entered into by the client.

All Investments are subject to risks, including the possible loss of principal. Past performance does not guarantee future results.

Information and recommendations contained in market commentaries and writings are of a general nature and are not intended to be construed as investment, tax or legal advice. These materials reflect the opinion of Crossmark on the date of production and are subject to change at any time without notice. Where data is presented that was prepared by third parties, the source of the data will be cited, and we have determined these sources to be generally reliable. However, Crossmark does not warrant the accuracy of the information presented.

This content may not be reproduced, copied or made available to others without the express written consent of Crossmark.

DD-WKLY-COMM-2.42 10/22

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits