Is tax drag holding your clients back? More likely, how much is tax drag holding your clients back?

Investing can come with a hidden cost—and that cost is taxes. How much are taxes costing your clients? If you are a tax-smart advisor, you probably already know the answer to that question. But if you aren’t taking steps to reduce the impact of taxes on your client portfolios, then the cost is likely a lot more than you think. And that cost can have a long-term impact on something that is near and dear to your clients: their retirement savings and their ability to enjoy the years after they leave the workforce.

Run fast, or run slow?

How is it that taxes have that impact? It comes down to the drag on performance they represent. Think about an activity such as running. My friend Mark in the picture above is a runner. He prepares for a run by warming up, wears athletic clothes to prevent restriction of motion, uses specific running shoes to both protect his feet and legs and assist in the motion. But what if, after all of that, someone tied a rock to him?

You may well ask: “Why in the world would someone have a rock tied to them as they are about to embark on a run?” I will counter that by asking: “Why is someone investing for retirement intentionally trying to slow down the growth of their portfolio while increasing their risk?” When a portfolio is weighed down by tax drag, that is in essence what is happening.

Metaphorical reality = Capital gain distributions

There are a number of factors causing the tax drag so many investors experience in their portfolios. The primary one is capital gain distributions. Each calendar year, investment portfolios of all sorts need to pay taxes on their realized capital gains. Looking just at U.S. mutual funds, 81% paid a capital gain distribution in 2021, with the average distribution at 12% of net asset value (NAV). That was the highest level in 20 years! Those distributions are taxable and can result in a hefty tax bill.

It’s also important to note that these distributions can happen in both up and down markets. That’s a little like adding insult to injury. Some of your clients could see negative returns in their portfolios and even so receive a Form 1099-DIV with a big tax bill due in April. Markets have been challenging so far this year. But as the chart below shows, there have been capital gains distributions every year over the past decade, regardless of the market’s performance.

Source: Morningstar. U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category ‘US Equity’ which includes mutual funds and ETFs (and multiple share classes). Total Capital Gain Distribution % = calendar year cap gain distribution ÷ year-end NAV (For years 2012 through 2020), = total cap gain distribution ÷ respective pre-distribution NAV (For 2021). Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. As of 6/30/2022

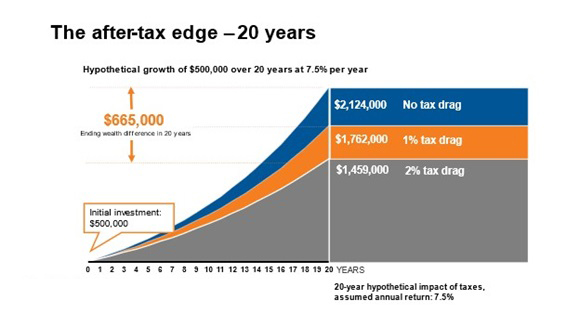

What’s an even bigger deal is the impact this has on long-term wealth. Your clients’ retirement goals are largely dependent on how their investment portfolio performs. What if their portfolio is weighed down by that “rock” in the form of tax drag? On a $500k initial investment over a 20-year investment horizon, the impact could be as high as $665k. That’s the difference between a portfolio that has the potential to grow to $2.124 million and a portfolio with average tax drag that only has the potential to grow to $1.459 million. That’s a lot of dollar bills left behind; and it could be worse when state and local taxes are added on.

This is a hypothetical illustration and not meant to represent an actual investment strategy. Taxes may be due at some point in the future and tax rates may be different when they are. Investing involves risk and you may incur a profit or loss regardless of strategy selected.

Scissor beats rock, saving you paper!

As an advisor, you can help your clients cut the rope to the metaphorical tax rock. How?

Consider helping your clients potentially improve their outcomes with tax-managed investing. Tax-managed investment products include strategies that help minimize taxable distributions and maximize after-tax returns.

You can start with our value of tax management tool (financial professional login required). This tool shows you how lowering investment-related tax costs can make a significant impact on your clients’ ability to meet their long-term goals. It allows you to quickly input specifics about an individual client's case to see their specific opportunities to manage investment-related taxes, including years to break-even, dollars of excess wealth and tax bill reduction.

Additionally, our tax impact comparison tool, which uses Morningstar data, is a great way to assess the impact taxes have on investment returns in taxable accounts. This tool shows the amount of return lost to taxes (tax-cost ratio), after-tax return and pre-tax return, and also shows their percentile rank within a peer universe.

Taxes on investments slow down a portfolio's potential growth like a rock slows down a runner. They represent a drag on the portfolio's returns. We believe this is something that should be managed to both minimize its impact and maximize the after-tax return for investors. Tax management should be a major consideration when constructing an investment portfolio for a taxable investor. As a tax-smart advisor, you can help cut the rope to the metaphorical tax rock holding your investors back. Because at the end of the day, it’s not what they make, it's what they get to keep.