A major reason for the Federal Reserve’s (Fed) relentless pace of rate hikes is the tight labor market that has been remarkably resilient in the face of weak economic activity and stressed financial markets. But that resiliency is about to turn. Expectations surveys across the economy have become quite pessimistic, with businesses expecting lower sales and consumers seeing bleaker personal finances. Last week’s Beige Book from the Fed, with reports of hiring freezes and more cautious consumer spending patterns, confirmed preparation for a downturn. Historically, such a broad and deep deterioration in economic expectations has been a leading indicator for a decline in employment.

Negative Expectations Across the Economy Bode Poorly for Job Growth

Surveys Include: Consumer, Forecaster, Small Biz, CEO, Manufacturing, Housing

Source: Guggenheim Investments, Haver Analytics. Data as of 9.30.2022 for payrolls, 10.31.2022 for surveys. Survey average is average Z-score.

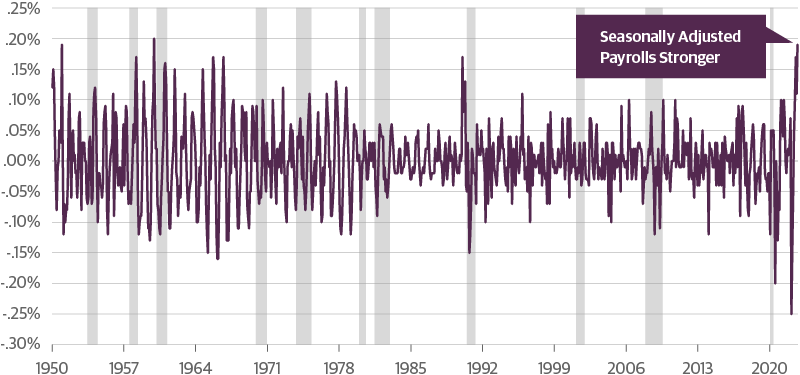

A more technical issue is also signaling an imminent change to weaker job growth. We’re seeing the largest gap since the 1950s between the year-over-year change in seasonally adjusted nonfarm payrolls and non-adjusted payrolls, when conceptually these measures should be equal. This gap is strongly mean reverting, adding additional downside risk to seasonally adjusted payrolls starting as soon as next month.

Seasonal Adjustment Boost to Payrolls Could Reverse in Coming Months

Nonfarm Payrolls: Gap Between Seasonally Adjusted YoY Change and Non-Seasonally Adjusted

Source: Guggenheim Investments, Haver Analytics. Data as of 9.30.2022.

With inflation still way too hot, and the Fed aiming for an unemployment rate around 4.4 percent, it will take some time before a weakening labor market causes the Fed to end rate hikes. But the correlation between our expectations survey aggregate and the labor market suggests that over the next six months the unemployment rate should rise to 4.2 percent with a cumulative decline in payrolls of over 800,000. As the jobs picture worsens, the Fed should gain confidence that tightening is having its intended effect.

That confidence should open up the door to a downshift in the pace of rate hikes at the December meeting. This downshift in rate hikes would be initially welcomed by markets, where there is huge pent-up demand for a Fed pivot. But as a recession continues to play out next year, risk assets would likely see renewed weakness, while interest rates would head lower.

From the Office of the Global Chief Investment Officer of Guggenheim Partners, Scott Minerd

By the Macroeconomic and Investment Research Group

- Matt Bush, CFA, CBE, U.S. Economist, Macroeconomic and Investment Research

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. Past performance is not indicative of future results.

Guggenheim Investments represents the following affiliated investment management businesses: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management. Securities distributed by Guggenheim Funds Distributors, LLC.

© 2022 Guggenheim Partners, LLC. All rights reserved.

54743

© Guggenheim Investments

Read more commentaries by Guggenheim Investments