Midterm Outcome And FTX's Demise: An Unexpected Turn Of Events

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat a week it’s been.

First, the midterm elections failed to produce the “red wave” that most pollsters and pundits predicted, and as I write this, it’s still unclear which party will have control of the House and Senate next year.

And second, the crypto industry may have experienced its very own Lehman Brothers moment.

FTX, until recently the world’s second-largest crypto exchange, filed for bankruptcy as its embattled founder, Sam Bankman-Fried, stepped down as CEO following a liquidity crunch that exposed the firm’s improper use of customer assets. FTX’s shocking demise comes within months of the collapse of Terra’s Luna coin, which triggered the bankruptcies of crypto firms Celsius Network, Voyager Digital and Three Arrows Capital.

The question on many investors’ minds is: How far and for how long will the contagion spread?

Biggest Midterm Upset In Decades?

It’s common knowledge that midterm results have not always been kind to the incumbent president. President Barack Obama’s agenda was famously sidelined by a Tea Party “shellacking” in 2010, and Republicans lost control of Congress midway through President Donald Trump’s term.

It’s also a given that past performance does not guarantee future results. As former Secretary of the Treasury Larry Summers tweeted on Wednesday, the last Democratic president to have such a favorable midterm outcome as Joe Biden did was John F. Kennedy, in 1962.

To be clear, the GOP may end up winning back a (very narrow) majority in one or both chambers of Congress once every vote is counted, but the victory, if we can call it that, is a Pyrrhic victory. In many contests across the U.S., voters rejected the most extreme forms of Trumpism, putting the former president’s 2024 ambitions into question.

Wall Street Loves Washington Gridlock

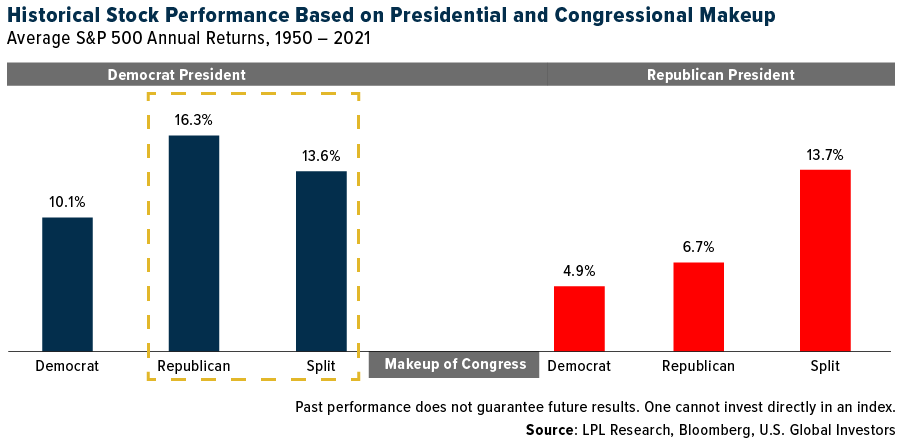

The big winner of the election was Wall Street. As I’ve pointed out before, legislative gridlock has historically been constructive for stocks, since sweeping policy changes become unlikely and there’s less risk to individual sectors.

Newly-installed Twitter boss Elon Musk was criticized earlier in the week for recommending that people vote for a Republican Congress, writing that “shared power curbs the worst excesses of both parties.” Like him or not, the billionaire entrepreneur is right. Since 1950, the S&P 500 has delivered the highest average returns when the White House was held by a Democrat and Congress by Republicans, according to LPL Research. Returns have also been higher-than-average when Congress was split, regardless of which party occupied the Oval Office.

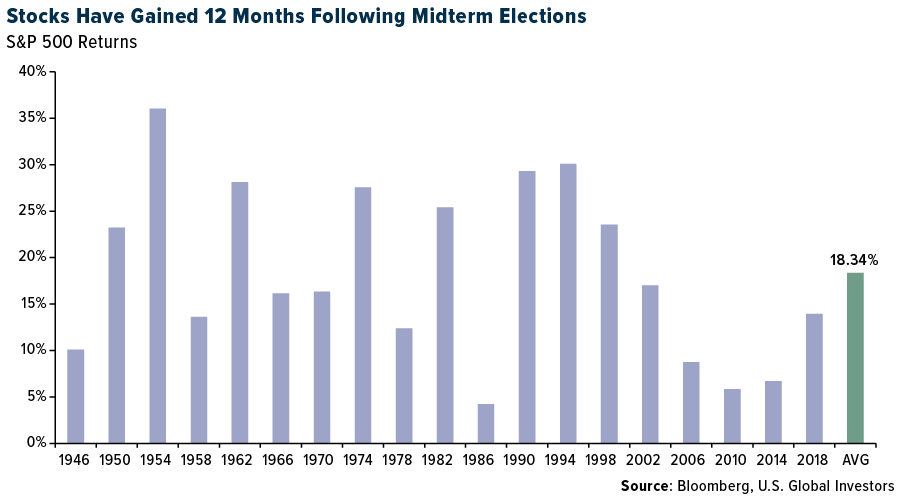

If 2022 ended today, it would be the worst year for stocks since 2008. But looking ahead, conditions appear brighter, if history is any indication. The S&P 500 was positive 12 months after all 19 midterm elections between 1946 and 2018, with an average return of over 18%.

Money Supply Growth Has Slowed To A Trickle

Of course, investors have other concerns besides politics—namely, inflation. Stocks rallied 5.5% on Thursday after the consumer price index (CPI) report showed that annual inflation cooled for the fourth straight month in October, falling to 7.7%.

Although inflation remains stubbornly high, the lower reading gave the market hope that the Federal Reserve may take its foot off the brake a little. I happen not to think this will be the case—we still have a way to go before inflation returns to a “normal” 2%—but the trend is headed in the right direction.

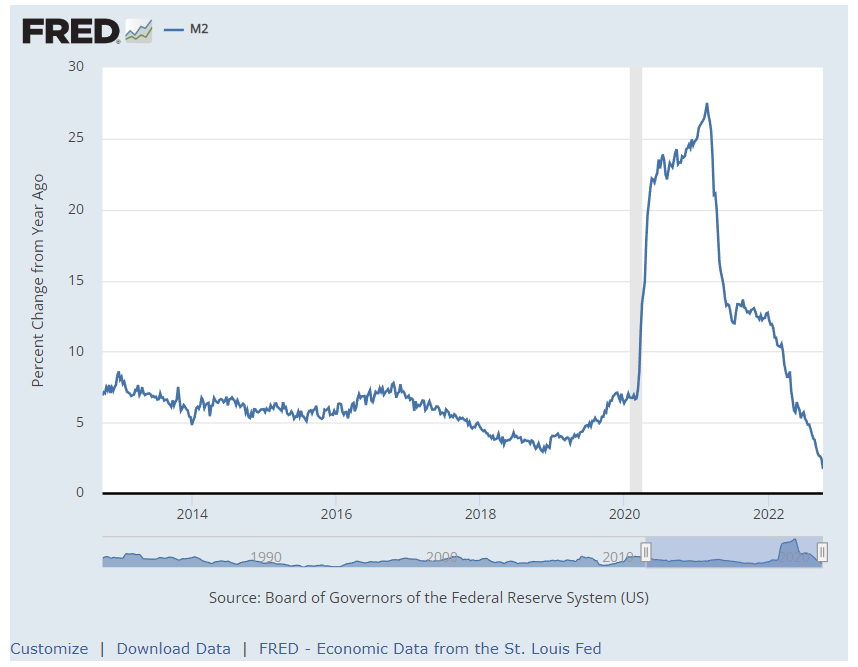

Driving much of the inflation of the past two years has been runaway money-printing by global central banks in an effort to pump liquidity into a pandemic-impacted economy. The good news is that the rate of this money-printing has slowed dramatically to a trickle since the frenetic days of 2020 and 2021. At a 1.7% annual growth rate currently, M2 money supply is well below its 10-year average of around 5%.

Crypto Industry Needs Reasonable Regulation

Returning to the issue of FTX, I think it’s important for people to understand that Sam Bankman-Fried, or SBF, was until recently seen as a smart, trustworthy wunderkind. Fortune magazine called him the “next Warren Buffett.” Last year, SBF said that FTX could one day buy Goldman Sachs and the Chicago Mercantile Exchange (CME).

But as it did with Theranos’ Elizabeth Holmes (who just this week asked to be sentenced with an 18-month at-home confinement), life has come at SBF fast. The 30-year-old entrepreneur’s net worth evaporated from an estimated $16 billion to less than $1 billion—all within an unprecedented 24-hour period.

FTX and SBF’s unethical decisions will inevitably contribute to many people’s lack of trust in Bitcoin and provide fuel to its biggest critics, Senator Elizabeth Warren chief among them. I believe that for crypto (and Bitcoin specifically) to gain widespread adoption, levelheaded lawmakers need to pass reasonable, rational guardrails protecting users and investors from bad actors in the still nascent crypto industry.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 4.15%. The S&P 500 Stock Index rose 5.90%, while the Nasdaq Composite climbed 8.10%. The Russell 2000 small capitalization index gained 4.60% this week.

- The Hang Seng Composite gained 7.00% this week; while Taiwan was up 7.53% and the KOSPI rose 5.74%.

- The 10-year Treasury bond yield fell 34 basis points to 3.814%.

Airlines & Shipping

Strengths

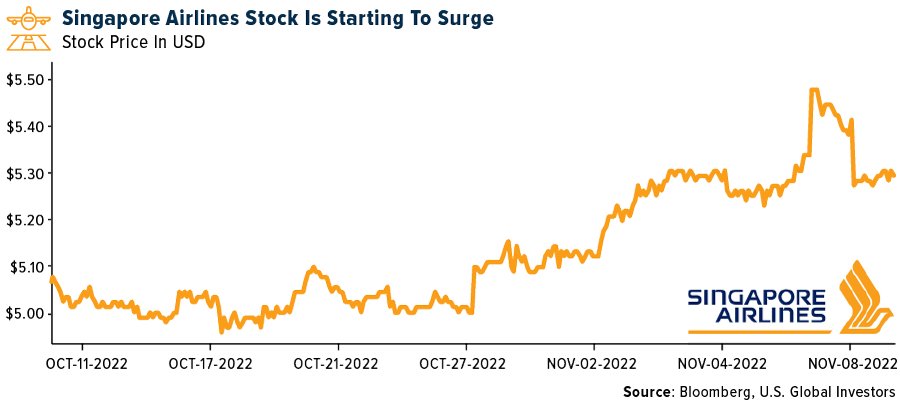

- The best performing airline stock for the week was Wizz Air Holdings, up 29.77%. Singapore Airlines reported second quarter 2023 net profit of S$557 million, up 50% quarter-over-quarter, well ahead of consensus estimates. Total revenue was S$4.5 billion, up 14% quarter-over-quarter thanks to continuous improvement in passenger revenue, offsetting the sequential decline in cargo revenue. Notably, passenger revenue was up 24% quarter-over-quarter thanks to improved travel demand, while passenger yield remains elevated.

- Maersk’s third quarter results came in strong, at 7% above consensus. The difference versus consensus was mainly in Ocean, where freight rates were 1% ahead of consensus. While volume was down 7.5% year-over-year, this was evenly split between spot and contracted volume, indicating there was not a mass exodus from contracts. Costs continue to rise, supporting the view that the mid-term breakeven rate will be above 2019 levels.

- According to Morgan Stanley, perhaps the biggest takeaway from this earnings season was Sun Country’s board of directors’ authorization to repurchase up to $50 million worth of SNCY shares. This announcement marks an important inflection point for SNCY (and for the industry) in terms of attracting investors back to the space as well as signs of normalization.

Weaknesses

- The worst performing airline stock for the week was Azul SA, down 21.18%. Air China, China Southern Airlines and China Eastern Airlines all suffered wider net losses year-over-year in the third quarter, due to dimmed demand recovery, oil price hikes along with the weaker CNY. Domestic travel may see gradual improvement month-by-month in the fourth quarter, but the “Big Three” carriers could continue to post widened losses year-over-year.

- International Seaways reported an adjusted third quarter EPS of $2.28, below the street consensus of $2.32. Rates came in lower than consensus virtually across the board except for the LR1 vessels. Although third quarter numbers were short of expectations, fourth quarter bookings are universally quite a bit higher than the current consensus.

- China’s domestic air traffic fell to just 26% of 2019 levels in the second half of October, down from 35% in the first half of that month, the worst level since the lockdowns in Wuhan (Feb. 2020) and Shanghai (Apr. 2022). Unsurprisingly, Beijing’s domestic traffic was most disrupted at only 10% of 2019 levels in the second half of October due to the political meetings, but other major cities like Shanghai and Guangzhou were just at 30% of normal traffic.

Opportunities

- According to Morgan Stanley, for Boeing, the group was positively surprised that the company provided more details regarding its 2022, 2023, and 2025/2026 free cash flow outlook. The unexpected supporting details provide a visible and credible path to $10 billion of free cash flow in 2025/2026. Even though sell-side consensus estimates are already at $10 billion in 2025, skepticism from the buy-side means that management’s outlook was received positively by the market.

- AD Ports announced signing an agreement to acquire an 80% stake in Dubai-based container shipping company Global Feeder Shipping for AED 2.9 billion. The transaction is expected to be closed in in the first quarter of the new year and will then make the group the largest single provider of feeder shipping services in the region (with a fleet of 35 vessels) and the third largest globally by volumes carried (with a total container capacity of 100,000 tons).

- China is planning to scrap penalties for airlines when deplaned passengers test positive for Covid after entering the country. Currently, China bans airlines from operating a route for one to two weeks depending on the number of positive tests. In addition, there is speculation that China may ease Covid rules in March.

Threats

- Spirit Airlines noted pilot attrition remains elevated, which contrasts with commentary from Frontier Airlines. One would expect relatively greater hiring/attrition issues at Spirit versus Frontier due to seniority list integration uncertainties related to the pending merger. While most forecasts assume new pilot contracts by 2023, the exceptions are Frontier (2025) and JetBlue (2024).

- The widely watched U.S.-West Coast International Longshore Warehouse Union negotiations remain unresolved, despite no major disruptions posed so far after its contract expiration on July 1. More recently, longshoremen at the Port of Oakland in California walked off the job as they seek to get back to the bargaining table. The negotiations are approaching a tipping point with port labor disputes and worker slowdowns potentially materializing after the U.S. November mid-term elections.

- JetBlue and Alaska Air guidance implies a 3-5% point revenue slowdown relative to 2019. JetBlue has some unique headwinds (loyalty comp and Caribbean hurricane impacts) while Alaska has higher technology exposure and guided earlier than other leisure carriers. Both carriers may have been conservative in their guidance and there could be revenue upside if the leisure strength persists.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 5.7%. The best performing country in Asia this week was Taiwan, gaining 7.3%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 4.3%. The South Korean won was the best performing currency in Asia this week, gaining 6.7%.

- Semiconductor and technology stocks in Taiwan and South Korea outperformed this week. Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest contract chipmaker, posted a 56% increase in sales in October. TSMC said this week it was preparing for another U.S. plant, in addition to the $12 billion complex already building in Arizona, which is a sign of confidence during the correction among technology names. Year-to-date, shares of TSMC declined 41%.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Hungary, gaining 2.5%. The worst relative performing country in Asia this week was China, as the Shanghai Stock Exchange gained 0.5%.

- The Turkish lira was the worst relative performing currency in emerging Europe this week, gaining 0.1%. The Hong Kong dollar was the worst relative performing currency in Asia this week, gaining 0.2%.

- China exports shrank unexpectedly in October, falling 0.7% year-over-year in dollar terms from up 5.7% in September. Imports also contracted by 0.7% versus forecasts of 0.1% growth. Trade balance dropped to $85.15 billion from $95.95 billion in the prior month.

Opportunities

- There is a growing enthusiasm about Chinese equites following rumors that China leaders are considering steps toward reopening its economy but are proceeding slowly and don’t have a timeline. The zero-Covid policy will likely not be relaxed this year, but China could approve its domestically developed Covid-19 vaccine based on mRNA technology, which is believed to be the most effective protection against sickness.

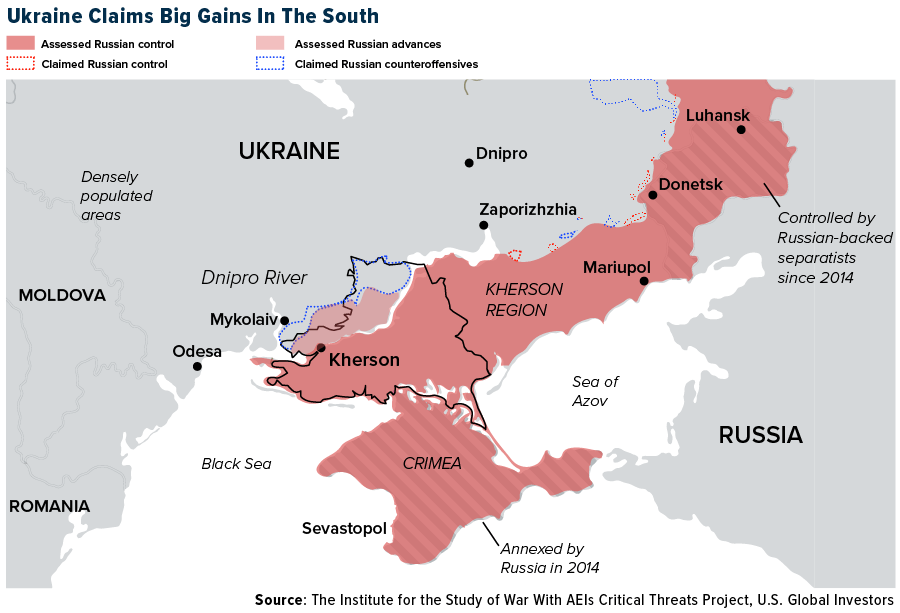

- Russia announced its withdrawal from the occupied Ukraine city of Kherson, which is one of the biggest military setbacks for Russia since its invasion began in February. Russia would still retain control of 60% of the Kherson region, including the coastline along the Sea of Azov. The President of Ukraine reiterated that his country would continue to retake territory from Russia. There is a possibility that world leaders during next week’s G-20 meeting in Indonesia may discuss options on initiating peace talks between Russia and Ukraine.

- Bloomberg reported onshore Chinese investors have been net buyers of Hong Kong-listed stocks for 24 consecutive trading sessions through Tuesday, spending around HKD118 billion ($15 billion). Tencent alone accounted for around a quarter of all flow, followed by Meituan and Wuxi Biologics.

Threats

- China continues to report higher Covid cases. Its nationwide Covid count increased to more than 9,000 on Wednesday; several major cities sent several districts under lockdowns. Beijing is emerging as a hotspot with the city finding 95 new cases on Wednesday, a five-month high. A handful of cases were found in Shanghai and Shenzhen as well.

- The President of Ukraine, Zelensky, extended the duration of martial law and general mobilization in anticipation that there will not be a quick solution to the conflict in the region. The last extension was implemented on August 15 for 90 days (until November 23). The war in Europe, which erupted February 24 and caused loss of life on both ends, has displaced millions and disrupted global markets.

- Investors may see an increase in volatility in trading as the dollar continues to correct. This week, inflation data in the United States came out weaker than expected, pushing emerging market equites and currencies higher. This week’s outperformance in emerging markets supported by a weaker dollar may be short lived as more consistent economic data is needed to conclude that CPI is on a down trend, toward the 2% desired by the Federal Reserve. Still, a 50-basis points hike is expected in December.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was nickel, rising 8.99%, as it and other metals surged with the easing of Covid restrictions in China. The new Vogtle reactors in Georgia are the first new reactors to receive construction approval in more than 30 years, according to the EIA. The Vogtle Units 3 and 4 project units are set to come online in the first quarter of 2023. The Department of Energy had offered conditional commitments totaling $8.3 billion in loan guarantees for the construction of the two 1.1K MW nuclear reactors, but the construction was delayed due to the lack of a proper domestic nuclear supply chain and skilled workforce.

- The third quarter of 2022 reporting season for European Union Big Oils marks the seventh consecutive strong quarter for the sector (10% beat on company-compiled consensus earnings in aggregate) and supports the view of ongoing positive earnings revisions, the re-ignition of the cash flow generation engine, double-digit cash returns to shareholders on the back of buybacks, and growing dividends.

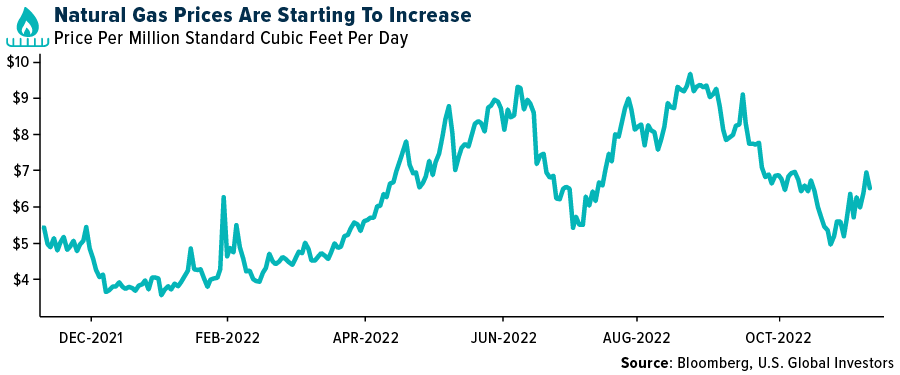

- U.S. natural gas futures soared as much as 10% to start the week as a winter storm hits the Pacific Northwest and frigid weather is expected across most of the country next week. In the first major cold snap of the season, air filtering across the West is pushing temperatures 15 to 25 degrees Fahrenheit under normal levels and will likely deposit two to four feet of snow through Tuesday in the Sierra Nevada mountains, according to the National Weather Service. However, there are rummers Freeport LNG will be delayed on reopening. The curtailed export capcity has resulted in stranded gas and lower domestic prices.

Weaknesses

- The worst performing commodity for the week was natural gas, losing 7.31%, over worries of stranded gas resurfacing. Urea prices were down this week as international producers cut prices, which sparked demand and lifted prices before India announced a surprise tender. Potash prices were down across all global benchmarks as competition remains high and demand still relatively slow.

- At the industry level, U.S. shale growth has generally fallen short of market expectations through the post-Covid recovery. Since the start of 2022, U.S. oil production has only grown 200 million barrels per day, roughly one-tenth of the peak growth seen in 2018. Capital discipline and the more transitory impacts of inflation and tight supply chains are certainly important drivers of this trend.

- The benchmark iron ore price briefly dipped below $80 per ton last week before rebounding to $88 per ton by the end of last week and into this week. Some Chinese domestic iron ore producers have been cutting output, with utilization rates of 53% last week down from 65% in mid-August.

Opportunities

- According to UBS, the long-term fundamentals for copper look compelling and arguably better now than six to nine months ago due to accelerated spending on energy transition and potential delays to new projects. However, there is an inconsistency between expectations of easing physical tightness and consensus, suggesting prices will not fall in 2023. Despite being more cautious than consensus near term, the risk versus reward for copper/copper stocks is improving.

- Following the U.K. and France, Japan established an ambitious plan to restart up to 17 nuclear power plants beginning in the summer of 2023 and construct nuclear plants to start commercial operations in the 2030s. Poland plans to spend $40 billion to build two nuclear power plants and has chosen the U.S. government and Westinghouse as partners. The U.S. and Canada are also planning to ride the wave of nuclear renaissance momentum.

- In the Middle East, there is an ambition to grow production capacity. Projects that were discussed in 2019 are now reaching decisioning, but a whole new wave of projects is stacking up behind this one, creating a quite ambitious project list. In Qatar, in addition to four trains at the North Field Expansion, Qatar Gas seems very likely to decision two incremental trains from the North Field South project in 2023 but could quite possibly raise this number to four. The UAE is looking to raise its production capacity by 1MMbpd through increased activity in a variety of fields and is also likely to develop its Hail & Ghasha sour gas project as well as its own potential LNG export facility.

Threats

- More U.S. SPR releases will be needed given the implementation risks around the forthcoming price cap on Russian oil exports. There are an additional 26 million barrels of congressionally mandated sales required in fiscal year 2023 that runs from October 2022 through September 2023 and will be delivered in the first quarter of the new year. In this scenario, crude oil stocks in SPR will exit the first quarter of 2023 quietly at 348 million barrels, the lowest since July 1983, and almost half of the stocks a year ago.

- Asian LNG imports fell 9% year-over-year in the first 10 months of 2022 on high pricing pressure and China’s Covid policy. High prices may still weigh on Asia’s imports next year, but this could be offset by a demand rebound especially in China following re-opening.

- The North American Electric Reliability Corporation warned this week that much of North America will face potential supply shortfalls this winter if weather becomes severe enough. Americans are already paying record high electricity rates amid tight natural gas and coal supplies and competing for these fuels in the international markets.

Luxury Goods

Strengths

- According to Bloomberg, year-over-year inflation (CPI) in the U.S. decreased in October to 7.7% from 8.2% in September, versus the expected 7.9%. This represents a slight growth in purchasing power for consumers in the U.S., one of the leading luxury goods markets worldwide.

- Ralph Lauren reported a 30% rise in sales in China despite pandemic closures due to the country’s zero-Covid policy and a third of its stores being closed across the country. The brand attributes the positive results to its popularity among younger and wealthier consumers in the Asian nation, according to Patrice Louvet, Ralph Lauren’s CEO, reports Bloomberg.

- Aston Martin Lagonda Global, a company that designs and manufactures automobiles, was the best performing S&P Global Luxury stock for the week, gaining 41.76%. The company launched new products, including the 2023/24 sports/GT line-up renewal. The company’s stock is higher for the seventh straight day (the longest winning streak since the company went public in 2018), and it is up more than 60% from the November 2 low.

Weaknesses

- European shares of both luxury and mining stocks fell at the start of the week, reports Reuters, after hopes of an easing in China’s strict Covid measures were quashed over the weekend. LVMH, Kering, and Pernod Ricard all dropped between 0.7% and 1.6%. Health officials in China reiterated their commitment to strict Covid curbs this weekend, the article explains, disappointing investors hopeful for relief. China is one of the primary markets for global luxury goods purchases, so this is a negative for the region.

- The head of the luxury research team from Morgan Stanley said the widening gap between a stronger dollar and other global currencies is impacting the luxury goods market, affecting leading luxury brands like Burberry, Louis Vuitton, and Kering. Companies from these industries have around a 35% price gap in Europe versus China and around a 25% price gap in Europe versus. the U.S. on average, however, now this is about 40% due to foreign currency movements. This is generating a gray market because consumers travel to countries with highly devaluated local currencies compared to the U.S. dollar to buy the same products but at lower prices. Louis Vuitton and Kering said, for now, they wouldn’t raise the prices in markets where the local currency has significantly depreciated.

- Brilliant Earth Group, a company that designs and manufactures jewelry products, was the worst performing S&P Global Luxury stock for the week, losing 20.05%. The company cut its year-end sales outlook, and the stock fell as much as 33%, (the most intraday since May 13). JPMorgan lowered its price target for the company from $11 to $10.

Opportunities

- As reported by Vogue Business, Kering is in advanced talks to acquire Tom Ford, the Wall Street journal noted at the end of last week (with rumors still highlighted into this week). The French luxury group, which owns brands including Gucci, Balenciaga, and Saint Laurent, could reach a deal soon, the article continues, which cited unnamed sources. News that Goldman Sachs was exploring a potential buyer for Tom Ford was first reported this summer. Kering is interested in Tom Ford’s beauty business which already holds the license. In June, Estée Lauder announced its plans to grow this license into a billion-dollar business.

- According to Bloomberg, Farfetch, one of the leading luxury goods e-commerce brands, will acquire a 47.5% stake in Yoox-Net-a-Porter Group, a move that is expected to finalize in 2023. This acquisition represents a significant opportunity for Farfetch to access China’s top retail sites, joint-venture cash injections from Alibaba and Richemont, and ventures in the U.S. and online beauty retailers.

- Over the weekend, Chanel built a cabana-lined, boardwalk-style runway – to stage a fashion show in early November, reports Fashionista.com. However, there was technically no new collection to showcase. So, what’s the deal? According to the article, this is an example of a growing trend among luxury brands, where they essentially re-do a runway closer to when the collection arrives in retail. It’s not quite see-now, buy-now, but it’s close.

Threats

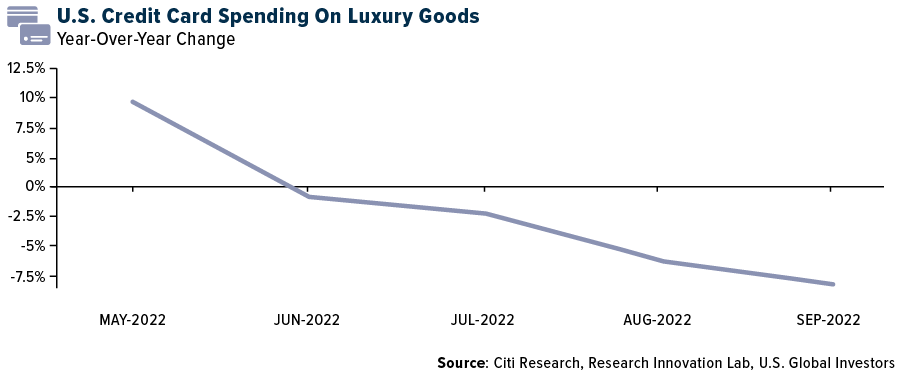

- Based on a survey of 2,200 U.S. adults by Morning Consult, credit-card data shows that spending on luxury goods slowed in the U.S. in recent months. In addition, 72% of consumers are planning to look for cheaper alternatives this holiday season because of the high inflation levels. They expect fewer holiday sales over the next two months, predicting an increase of around 6% and 8% from a year ago, after a 13.5% jump last year.

- Bloomberg economists predict that China’s year-over-year retail sales will decrease from 2.5% in September to 0.7% in October due to Covid restrictions. China continues to report a spike in Covid cases, and more lockdowns are expected. The sales data will be released next week on November 14.

- China’s government reiterated its zero-Covid policy and has asked for more precise Covid control measures. This could mean more lockdowns and the close of different industries across the country, impacting the production chain of many international companies whose manufacturing base is located in China.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was PAX Gold, rising 5.66%. Oil and gas giant Shell announced Thursday that it signed a two-year conference sponsorship with Bitcoin Magazine, a leading crypto publication, reports the media outlet. Representatives from Shell will speak on the mining stage about improving the energy costs of Bitcoin mining, using the company’s own lubricant and cooling solutions.

- BingX, the leading crypto social trading exchange, introduced a new bug bounty program on HackenProof. HackenProof is a web3 bug bounty platform trusted by the crypto market that connects its customers with the global hacker community to uncover security issues in their products. This program rewards both users and security researchers to find and report bugs in its ecosystem with cash.

- U.S. Senators John Boozman and Debbie Stabenow put out separate statements on Thursday highlighting their arguments in the wake of the turmoil at Sam Bankman-Fried’s FTX exchange and sister trading house Alameda Research. Lead sponsors of the legislation would give the Commodity Futures Trading Commission sweeping powers to regulate crypto assets directly while the FTX crisis underscores the need for greater oversight of the industry.

Weaknesses

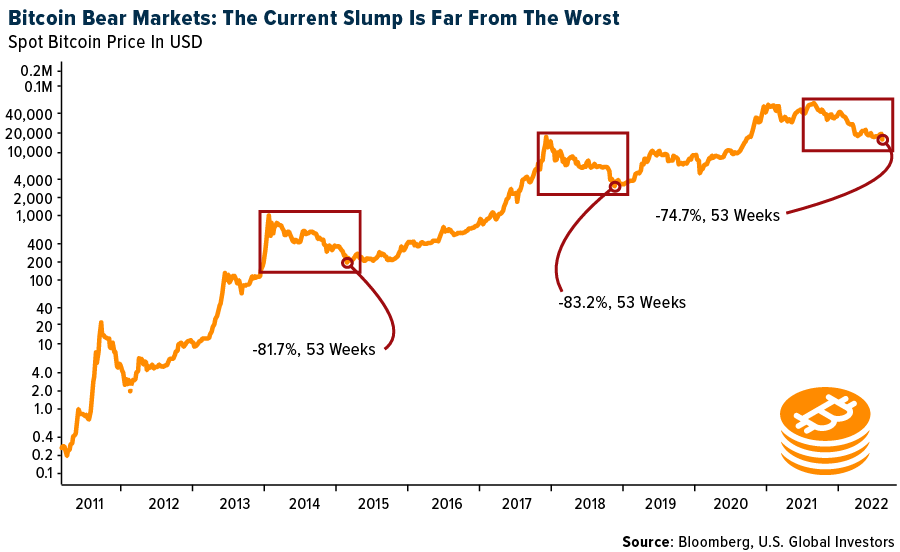

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was FTX Token, losing 89.33%. Bloomberg reports that this week’s rout in cryptocurrencies deepened, with Bitcoin tumbling to the lowest levels in two years, with the collapse of FTX.com. Bitcoin, the largest token by market value, fell as much as 16% to $15,731.30 on Wednesday, the lowest since November 2020. That brings this week’s decline to about 20%. It reached a record high of almost $69,000 a year ago. Nearly every digital coin was struggling; Ether, Solana, Polkadot, and Avalanche all dropped. FTT, the utility token of the FTX Exchange, collapsed by more than 40%, following a more-than-70% tumble on Tuesday.

- Core Scientific Inc., the Bitcoin miner that warned last month that it might seek bankruptcy protection, said its reserve of the digital token has dwindled to 62 coins as of October, from more than 8,000 earlier this year. Low Bitcoin prices, soaring energy costs, and fierce competition among miners have battered Bitcoin miners who took out billions of dollars of loans to fund their expansions during the bull run starting last November. Other miners, such as Argo Blockchain PLC and Iris Energy, are also struggling to repay debt.

- Decentralized finance is feeling the pain of Binance’s proposed, but dropped, takeover of FTX.com, with investors yanking cash from projects as uncertainty lingers about the future of one of the largest crypto exchanges. The total value of cash locked in DeFi dropped by more than 12% in a single day, after hovering around $50 billion to $60 billion since June, according to data tracker DeFi Llama. That number stood at more than $180 billion last December.

Opportunities

- Singapore’s desire to be a hub for the so-called web3 industry conflicts with the city-state’s proposed curbs on retail crypto trading, Coinbase Global Inc.’s Chief Executive Officer Brian Armstrong said. The nebulous term “web3” refers to a vision of a decentralized internet built around blockchains, crypto’s underlying technology. Asian economies including Singapore, Hong Kong and Japan are jostling to be at the forefront of the technology, anticipating it can aid economic expansion. Singapore is seeking to clamp down on retail-investor access to crypto trading to shield consumers from a volatile market that endured a $2 trillion rout over the past year.

- Bitcoin baseball team Perth Heat is now allowing fans to send micropayments to players with Bitcoin through Lightning, reports Bitcoin Magazine. Last year, the team became the first sports club to operate on a Bitcoin Standard. The feature was developed in collaboration with IBEX, the team’s official Bitcoin Lightning processor, and will be available starting on Perth Heat’s next game on November 11, 2022, the article explains.

- Cameron Crise, Bloomberg macro strategist, writes this week that the crypto crash reminded him of when Robert Heinlein popularized the phrase “there ain’t no such thing as a free lunch,” in the 1960s, but for much of the past several years the crypto industry has tried to dispute it. The bill, it seems, is now coming due. Generally speaking, if something seems too good to be true, it usually is. And when actors, supermodels, and sports stadiums are all telling at you to get excited about a financial innovation that entails heavy ownership of illiquid assets…perhaps consider walking the other way.

Threats

- Crypto markets face weeks of deleveraging in the fallout from the crisis at digital-asset exchange FTX.com, a period of upheaval that could push Bitcoin down to $13,000, according to JPMorgan Chase & Co. strategists. A “cascade of margin calls” is likely underway given the interplay between the exchange, its sister trading house Alameda Research, and the rest of the crypto ecosystem, a team led by Nikolaos Panigirtzoglou wrote in a note. “What makes this new phase of crypto deleveraging induced by the apparent collapse of Alameda Research and FTX more problematic is that the number of entities with stronger balance sheets able to rescue those with low capital and high leverage is shrinking” in the crypto sphere, the team said Wednesday.

- Crypto exchange FTX lent billions of dollars’ worth of customer assets to fund risky bets by its affiliated trading firm, Alameda Research, setting the stage for the exchange’s implosion, a person familiar with the matter said. FTX Chief Executive Sam Bankman-Fried (who stepped down Friday) told an investor this week that Alameda owes FTX about $10 billion, the person said. FTX extended loans to Alameda using money that customers had deposited on the exchange for trading purposes, a decision that Mr. Bankman-Fried described as a poor judgment call, according to the person. The FTX.com fiasco has ensnared some of the biggest names in finance.

- Bitcoin is currently trading around its lows of the year, which is feeding through into broader risk sentiment. It’s been said that the crypto industry has tried to compress all the mistakes of the past few centuries of traditional finance into the span of a few years– FTX and associated companies allegedly encapsulate a lot of those errors themselves. It turns out that the lack of a credible lender of last resort in decentralized finance might be a bug, rather than a feature.

Gold Market

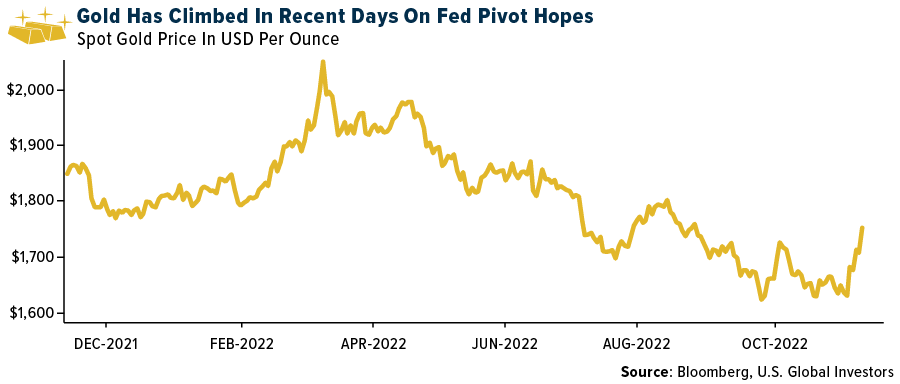

This week gold futures closed at $1,770.90, up $94.30 per ounce, or 5.62%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 14.88%. The S&P/TSX Venture Index only gained 1.03%. The U.S. Trade-Weighted Dollar sunk 4.06%.

| DATE | EVENT | SURVEY | ACTUAL | PRIOR |

|---|---|---|---|---|

| Nov-10 | CPI YoY | 7.9% | 7.7% | 8.2% |

| Nov-10 | Initial Jobless Claims | 220k | 225k | 218k |

| Nov-11 | Germany CPI YoY | 10.4% | 10.4% | 10.4% |

| Nov-14 | China Retail Sales YoY | 0.7% | — | 2.5% |

| Nov-15 | Germany ZEW Survey Expectations | -50.0 | — | -59.2 |

| Nov-15 | Germany ZEW Survey Current Situation | -67.8 | — | -72.2 |

| Nov-15 | PPI Final Demand YoY | 8.3% | — | 8.5% |

| Nov-17 | Eurozone CPI Core YoY | 5.0% | — | 5.0% |

| Nov-17 | Housing Starts | 1,415k | — | 1,439k |

| Nov-17 | Initial Jobless Claims | 220k | — | 225k |

Strengths

- The best performing precious metal for the week was palladium, up 10.46%. Allied Market Research published a report outlining 5.8% compounded growth for global palladium markets through 2031. Barrick Gold reported third quarter 2022 adjusted earnings per share (EPS) of $0.13 versus consensus of $0.11. The beat versus consensus was on lower depreciation, corporate costs, exploration, interest as well as slightly lower copper costs. Cash costs of $891 per ounce were largely in line with consensus of $892 per ounce, while all-in sustaining costs (AISC) of $1,269 per ounce was slightly below consensus of $1,271 per ounce on lower corporate allocated overheads.

- AngloGold Ashanti’s third quarter 2022 results were better than forecast due to an improved production and unit cost performance, which resulted in a 10% beat on EBITDA (earnings before interest, taxes, depreciation and amortization). Cash generation for the period was $203 million better than forecast, with management highlighting that it continues to generate strong cash flows from the Kibali JV, while the outstanding value-added tax (VAT) balance in Tanzania was further reduced through corporate tax offsets.

- Central banks bought almost 400 tons of gold in the third quarter, the largest quarterly increase on record. Year-to-date purchases are already at the highest level since 1967, and there have been eight consecutive quarters of net buying. In particular, the World Gold Council (WGC) noted a big increase in unreported buying, while reported purchases were predominantly at emerging market banks.

Weaknesses

- The worst performing precious metal for the week was silver, but still up 4.65% and is the strongest performer so far this quarter. Sibanye-Stillwater’s third quarter 2022 operating results disappointed, with production missing consensus by 6% at the SA PGM operations, 11% at the SA gold operations and 23% at the Stillwater mine. Group adjusted EBITDA for the period declined 51% year-over-year to $496 million and missed consensus by 46%.

- Equinox Gold reported third quarter adjusted EPS loss of $0.09 against consensus of a gain of $0.01, and the Street estimate of a loss of $0.02. The disappointing quarter was punctuated by lowered production guidance and increased cost guidance for the full year 2022.

- Franco Nevada reported adjusted EPS of $0.83 versus consensus of $0.85; EPS was lower than consensus on lower revenue performance from precious metals offset by stronger performance from the energy division (Marcellus and Haynesville) versus consensus.

Opportunities

- Pan American Silver and Agnico Eagle delivered a definitive binding offer to acquire Yamana, topping the bid from Gold Fields. This consolidates 100% ownership of the Canadian Malartic mine, one of the world’s largest gold mines. The transaction would also create the leading precious metals producer in Latin America. The consideration consists of 153,539,579 common shares in the capital of Pan American; $1 billion in cash contributed by Agnico Eagle; and 36,089,907 common shares in the capital of Agnico Eagle. Under the offer, each Yamana share would be exchanged for approximately US$1.04 in cash, 0.1598 Pan American shares and 0.0376 Agnico Eagle shares, for an aggregate value of $5.02 per Yamana share.

- On Sunday evening, SolGold announced that it had entered into an agreement with Osisko Gold Royalties for a $50 million royalty financing on SolGold’s Cascabel copper-gold project located in northern Ecuador. Osisko has a 5% net smelter return (NSR) royalty on the Canadian Malartic mine and 3-5% NSR royalties across the Odyssey underground project. In addition, Triple Flag Precious Metals agreed to buy Maverix Metals for $606 million, elevating its profile and increasing the liquidity of their shares with the purchase.

- With another jumbo rate hike last week, gold and the markets rebuked Powell’s hawkish tone last Friday and continued their narrative of defiance throughout the past week with further price gains fueled by China reopening steps. The adage that the Fed will raise rates until something breaks may have seen the first shoe to drop with trillions eviscerated from crypto since the Fed changed policy. Less than a week after the most recent hike, FTX collapsed in a matter of days, wiping out customer accounts and another $5 billion in essentially vapor assets from companies associated with crypto. This may be part of why gold is now getting a firmer bid as investors ask… “Where is my money safer?”

Threats

- Argonaut Gold reported roughly in line adjusted EPS of $0.00 but achieved lower-than-expected production (45,900 ounces gold) and higher-than-expected costs in the third quarter of 2022. Weaker results at La Colorada and Florida Canyon were largely what led to the consolidated production miss. For the second quarter in a row, the company has raised its cash costs and AISC guidance by approximately $100 per ounce.

- Gold Fields has rescinded its offer for Yamana Gold after two Canadian rivals teamed up with an unsolicited $4.8 billion bid to break up an earlier merger agreement with the South African miner. Gold Fields CEO Chris Griffith noted that the company is still interested in assets in Canada and is not deterred by its experience in trying to acquire Yamana. Companies like Wesdome Gold Mines or Fortuna Silver Mines might be more palatable to acquire.

- Petra announced that the eastern wall of the tailings storage facility at its Williamson mine in Tanzania was breached. No fatalities or injuries have been confirmed. All mine production has been suspended pending further investigation into the breach. While Williamson only represents 3% of Petra’s total asset valuation, this is unfortunate news from an environmental perspective and in terms of potential impact to nearby communities.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All