With Tuesday's (Nov 15th) Producer Price Index (PPI) numbers bringing more relief on the inflation side, a new bearish narrative has been put forward by financial pundits over the last few days. The new story goes like this:

“While we now acknowledge that the Fed has put in place enough tightening to bring inflation under control [PS: they did not acknowledge this last week], we now gravely caution investors that the Fed will bring about a recession which will be accompanied by poor corporate earnings, and this will be the new catalyst to bring stocks down to levels at which buying them will be a great investment. So sit on the sidelines and wait it out.”

Fair enough, and certainly inventive. But let’s look at the data.

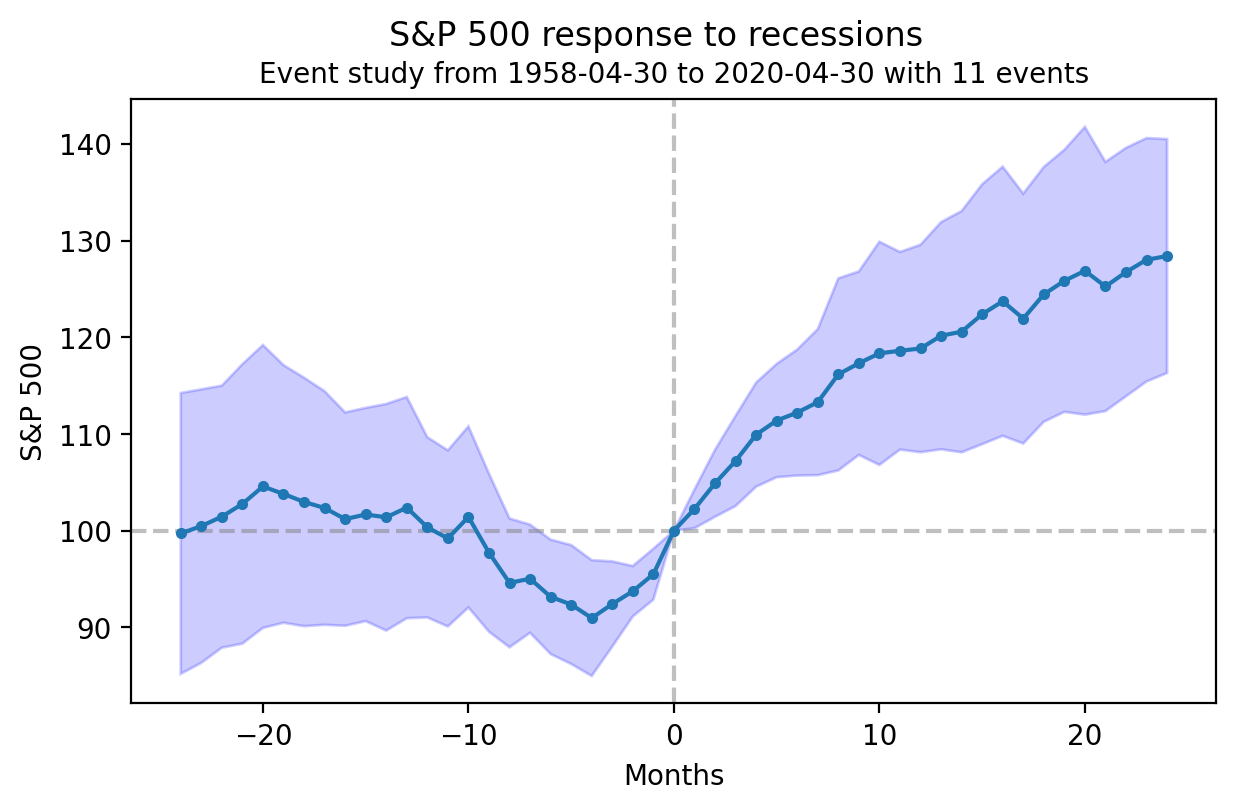

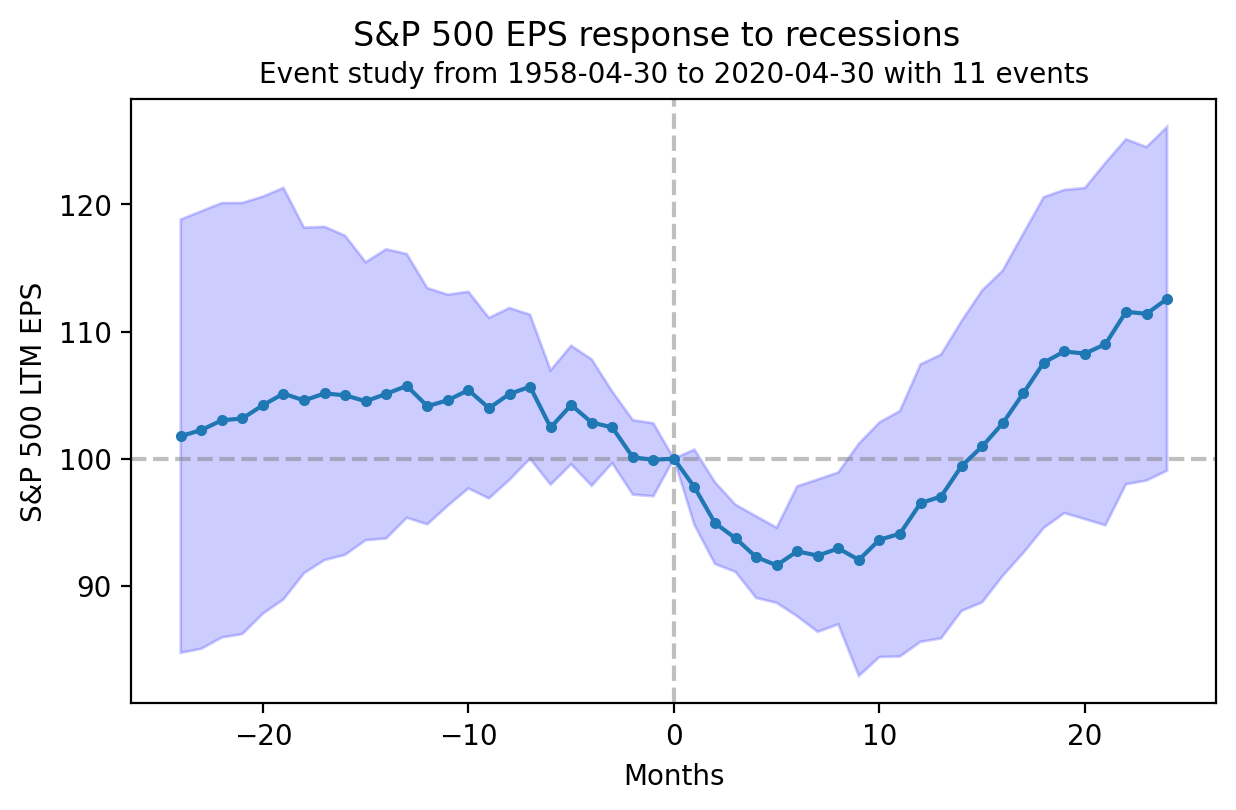

First, if we count as recessions episodes of trough year-over-year (YoY) growth in industrial production (IP), then there have been 11 such events since the start of our S&P 500 earnings data. In those 11 recessionary episodes, last 12-month S&P 500 earnings per share did indeed fall (by about 10%) after the onset of the recession. See Figure 1.

Figure 1: Event study of average S&P 500 earnings per share (EPS) around troughs in YoY IP growth. The EPS number has been normalized to 100 on the month of trough YoY IP. The blue region indicates 95% confidence bands around the event study. Source: QuantStreet Capital