Strategies for Volatile Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits1. Volatility is back

We’ve entered a new regime where volatility from inflation and policy tightening is reverberating through financial markets.

2. Portfolios are under pressure

The traditional balanced portfolio comprised of stocks and bonds is under pressure; 2022 has been one of the worst performing years for the 60/40 portfolio in decades.1

3. Evolving for a new regime

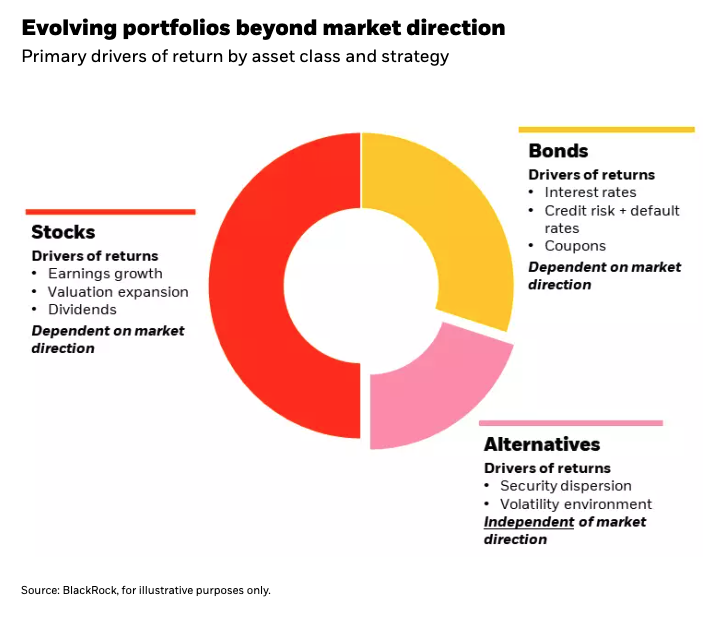

Investors may consider incorporating alternative strategies that can seek to provide differentiated, uncorrelated returns and portfolio diversification.

For years leading up to the pandemic, low inflation and stable growth created a favorable environment for investors that supported sustained periods of robust stock and bond returns. With inflation virtually non-existent, economic downturns were met with monetary and fiscal stimulus that provided a backstop for financial markets. Figure 1 highlights the volatility of U.S. inflation-adjusted gross domestic product (“Real GDP”) and inflation since 1965. During the period of the Great Moderation from the mid-1980s to the late-2000s, real GDP growth was relatively stable and inflation uncertainty remained benign.

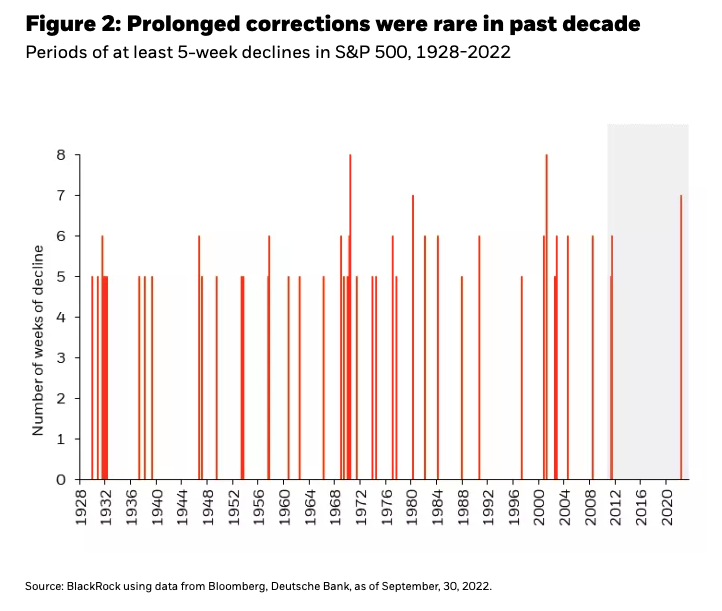

This structural “Goldilocks” scenario supported by ultra-accommodative policy made prolonged market corrections more of a rare occurrence. Today, that’s started to change with the re-emergence of macro volatility and distinct policy trade-offs between growth and inflation. Earlier this year, the S&P 500 fell for five or more successive weeks for the first time since June 2011, marking an end to the longest streak without a similar correction since the data began in 1928 (Figure 2).

Broken bonds in the “balanced” portfolio

In the previous economic cycle, low inflation risk and inexhaustible central bank liquidity generally supported 60/40 portfolio returns. Periods of slowing growth were met with easing financial conditions that provided relief during equity market downturns. Central banks would typically cut interest rates to support economic growth. When interest rates are cut, bond yields drop but bond prices go up. This provided a cushion in the traditional 60/40 portfolio with stocks under pressure.

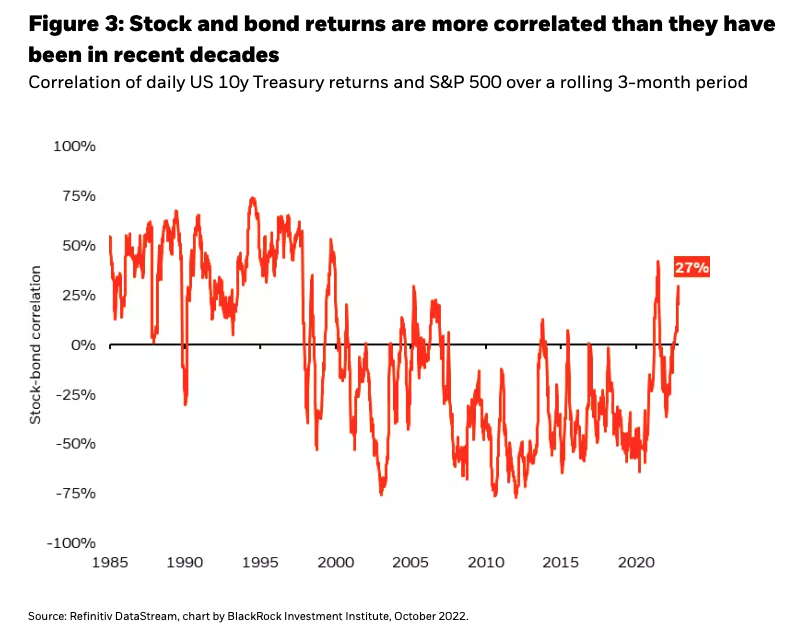

Today, inflation has virtually erased the uncorrelated, diversifying nature of that relationship. The 60/40 portfolio is down more than 20% so far in 2022.2 This marks one of the deepest drawdowns for the traditional balanced allocation in decades. Central banks are rapidly increasing interest rates to restore price stability, driving bond prices lower as stocks simultaneously fall on recession concerns. While higher yields have created a more attractive entry point for bond investors, inflation and policy tightening continue to weigh on bond returns and diminish their role as a portfolio buffer. Figure 3 shows the rolling three-month correlation of daily stock and bond returns. Stock-bond correlations have risen to 27% after averaging roughly -30% from 2000 through the start of the COVID-19 pandemic. This reflects several periods throughout 2022 where both sides of the 60/40 were falling at the same time, and while inflation uncertainty and upside surprises persist, it’s a trend that’s likely to continue.

The economic and policy dynamics that supported portfolios in the past regime have shifted. Now may be the time to rethink the traditional asset allocation playbook with alternative investments that provide new sources of diversification and returns.

An alternative source of diversification and returns

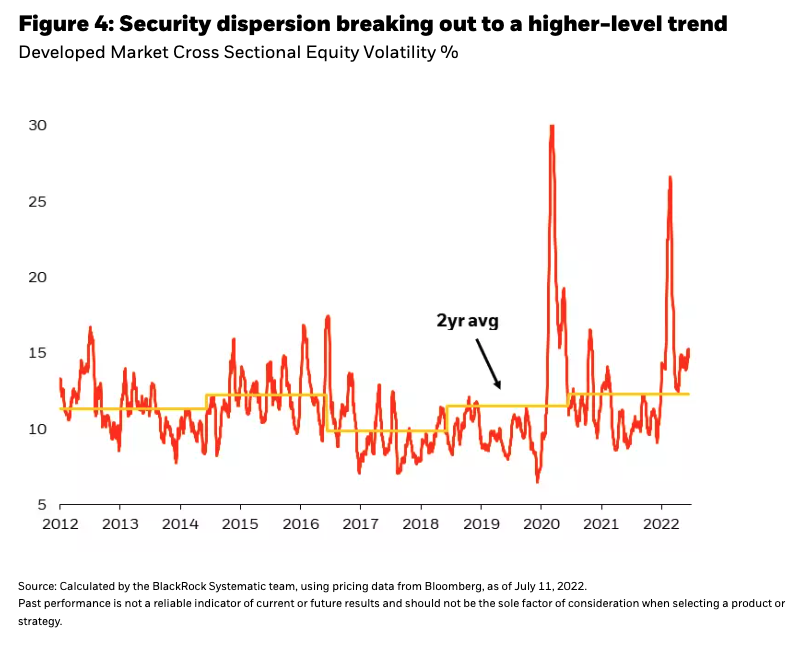

With market beta becoming a less reliable return source, alternative strategies have the potential to access new and differentiated opportunities that are surfacing in the current environment. Volatile macro conditions can increase security dispersion—or the divergence between the best and worst performing assets. Volatility in inflation and interest rates, for example, can increase dispersion by exposing vulnerabilities in companies with inelastic products or higher short-term debt levels while leaving other businesses less impacted. Figure 4 shows how the current macro backdrop has translated into a trend towards greater underlying security dispersion.

Expanding the toolkit for return generation

Building and maintaining an information advantage in security selection is key to remaining nimble and identifying opportunities that arise from higher dispersion and macro volatility. But how can these insights be implemented to generate returns?

In the previous cycle, the 60/40 portfolio worked well because of its dependence on market direction. Long-only strategies comprised of the “best-in-class” securities were better positioned to outperform as supportive economic conditions pushed markets higher and negative stock-bond correlations worked well to dampen overall portfolio risk. Looking ahead, with greater uncertainty in the directionality of beta exposures in an environment of rising recession risk, as well as heightened inflation uncertainty undermining negative stock-bond correlations, investors may consider diversifying portfolio exposures to include alternative strategies that can implement long AND short exposures. These strategies seek to exploit cross-sectional dispersion and generate returns by taking long positions in assets expected to outperform and short positions in assets that are expected to underperform. This long/short framework provides an expanded opportunity set to dynamically target returns on both sides of the market.

Building resiliency through diversification

Providing true portfolio diversification requires a durable return stream that’s disconnected from the ups and downs of the overall market. Alternative strategies with a low correlation to broad asset classes can act as a buffer when other assets in the portfolio are under pressure—the missing component in 60/40 portfolios today.

There are different ways that alternatives can be designed to deliver diversification. One way is by structuring the strategy to be “market neutral” so that long and short positions in the portfolio are relatively matched. This aims to capture the unique differences in security performance across the market and generate returns that are independent of market direction. Another example is a “multi-strategy” alternative which encompasses multiple uncorrelated underlying strategies in a single solution. This can help target consistent returns across a range of different market environments. When choosing an alternative, investors can consider incorporating a combination of complementary strategies with a low correlation to one another as an added layer of portfolio resiliency.

Evolving portfolios for market volatility

The Great Moderation in macroeconomic data reflects the collapse in the volatility of growth and inflation over the past two decades. The substantial increase in inflation and the potential for a more persistent contribution to macro uncertainty from inflation in a post-COVID world of structural change suggests we are entering a new regime of greater volatility. Inflation and policy dynamics are putting pressure on stocks and bonds—undermining the diversifying nature of the traditional “balanced” portfolio that investors have relied on for decades.

With macro volatility likely to persist and inflation remaining a key risk to global economies, now may be the time to augment the 60/40 portfolio with alternative strategies designed to generate returns that dampen overall portfolio volatility. Using an information edge and differentiated investment approach, alternatives can harvest new sources of return including security dispersion implemented in a market neutral or multi-strategy framework. These strategies can help build the resiliency that’s needed in the 60/40 portfolio today—providing durable, uncorrelated returns for navigating volatile markets.

Rich Mathieson

Senior Global Portfolio Manager, Systematic Active Equity

Jeff Rosenberg

Senior Portfolio Manager, Systematic Fixed Income

Christopher DiPrimio, CAIA

Head of Americas Strategy, Systematic Active Equity

James Dembinski

Product Strategy, Systematic Fixed Income

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All