Thanksgiving Air Travel Demand Supported By Remote And Hybrid Work

Membership required

Membership is now required to use this feature. To learn more:

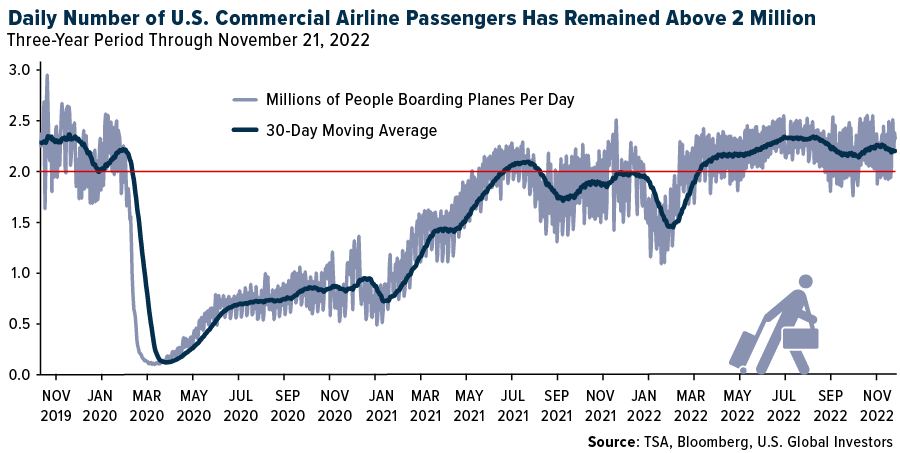

View Membership BenefitsCommercial air travel in the U.S. was incredibly robust this week, with passenger volumes close to 2.3 million per day. Thanksgiving was a major driver of demand, of course, but there may be another reason why travelers were able to board planes consistently throughout the week: remote and hybrid work.

Even though most offices and businesses have fully reopened following the pandemic, remote and hybrid work remains the norm for millions of American workers, allowing them to save both time and money they would have otherwise spent on commuting.

Working off-site has been a huge benefit to not just customers but also airlines, according to Helena Becker, an airlines analyst at Cowen. This type of work “enables [airlines] to be less ‘peaky’” and enables customers “to get better pricing,” Becker says.

Robert Isom shares the same idea. Speaking at last week’s Skift Aviation Forum in Dallas, the American Airlines CEO said that “demand is more spread out” due to the rise in remote work, adding that consumers, airlines and airports are no longer “beholden to the structure of the past.”

This helps explain why air travel demand was strong throughout the week instead of it being concentrated on the days immediately preceding and following Thanksgiving Day, as has historically been the case. On Sunday and Monday, more people boarded commercial jets than they did on the equivalent days in 2019, according to Transportation Security Administration (TSA) data.

What Americans Have Gained By Working Remotely

Remote work isn’t the perfect fit for every company or employee, but the potential benefits are easy to see.

According to Global Workplace Analytics, people who work remotely, either full-time or part-time, can save between $2,000 and $7,000 annually in transportation and work-related costs. They can also gain back the equivalent of two to three weeks per year in commuting time. An estimated $20 billion could collectively be saved at the pump.

With offices now fully open, you might think that remote and hybrid work is disappearing, but the opposite appears to be true. Gallup, the analytics and advisory firm, found that work away from home actually increased in 2022, accounting for 49% of the U.S. labor force in June, up from 42% in February. “Fully on-site work is expected to remain a relic of the past,” the firm says, though you’re welcome to disagree.

Will “Workcations” And “Bleisure” Replace Corporate Travel?

This week I was in Dubai, attending and speaking at the Alternative Investment Management, or AIM, Summit, and I also had the opportunity to take in the World Cup in Qatar.

I suspect there were hundreds more World Cup spectators who were also combining work and vacation (workcation), business and leisure (bleisure).

For the past year and a half, analysts and the media have questioned whether corporate business travel will ever return to pre-pandemic levels, as leisure travel has. An October survey of corporate travel managers in the U.S. found that domestic business travel volume has returned to 63% of 2019 levels, while international business travel is still only at 50%. Based on current trends, it may take until 2024 or 2025 before corporate spending on travel has fully recovered to pre-pandemic levels.

Thanks to the widespread acceptance of remote work, however, bleisure travel appears to be replacing traditional corporate travel, if not on a revenue basis (business class can cost three to four times as much as economy class) then certainly by volume. Domestic and international load factors, which measure the seat utilization rate on a scheduled flight, have returned to pre-pandemic levels.

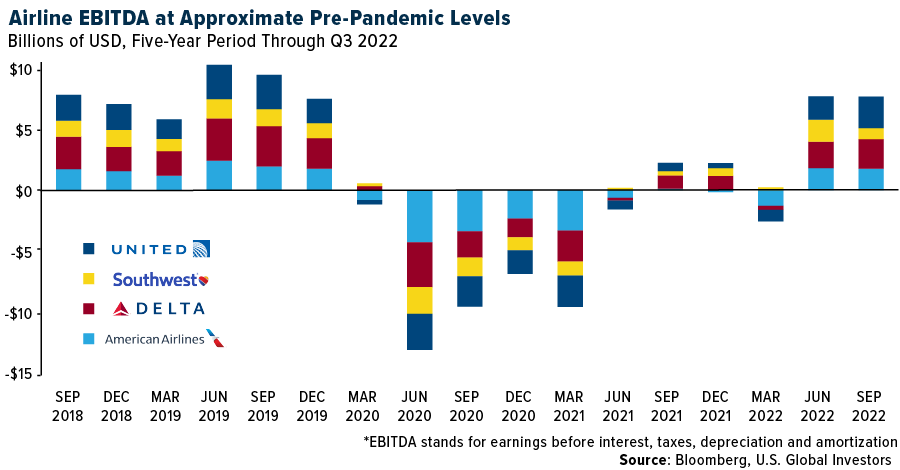

The same can somewhat be said about airlines’ profitability. As most of you know, EBITDA stands for earnings before interest, taxes, depreciation and amortization. It tells you how much profit a company made before debt and taxes were paid and before non-cash items like depreciation and amortization were factored in.

Looking at EBITDA for the Big Four U.S. carriers, we see that profitability is nearing pre-pandemic levels, even as American, United and Delta reported record revenues in the third quarter of 2022.

Lower Fuel Costs Would Be A Windfall

As you may have noticed, airfares have risen due to inflation, but they haven’t risen enough to compensate for higher fuel expenses.

The Organization of Petroleum Exporting Countries (OPEC), along with Russia, agreed to oil production cuts in early October, making it even more challenging for crude prices to fall and give consumers, including airlines, a break.

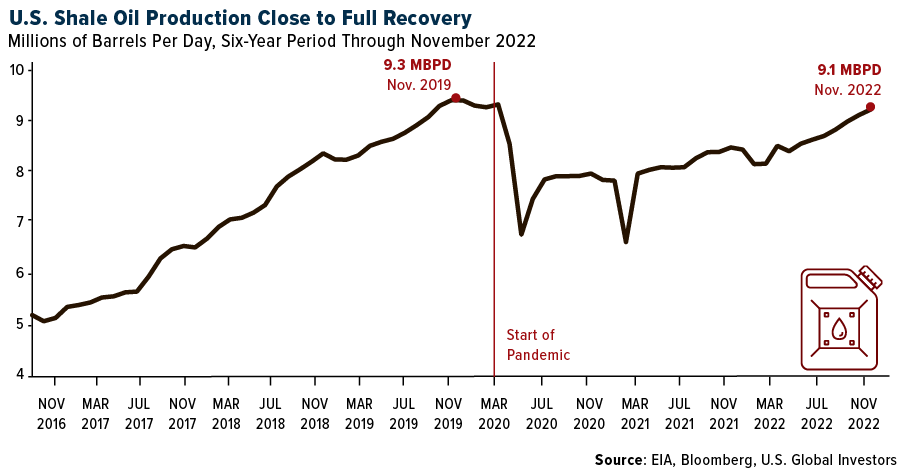

Here in the U.S., however, oil production continues to rise from pandemic lows and is nearing 2019 levels. Looking just at production from U.S. shale projects, which ordinarily require fracking to obtain oil, output has increased for seven straight months through November. This month, some 9.1 million barrels per day (MBPD) are expected to have been recovered from the ground. That’s only 200,000 BPD less than the all-time monthly high of 9.3 MBPD, set in November 2019, soon before the pandemic.

Jet fuel accounts for 25% to 35% of an airline’s total expenses, so lower fuel costs would be a nice windfall. According to Bloomberg, a new plane pays for itself in 12 years when jet fuel prices are lower than $4 per gallon, and as of last Friday, a gallon was $3.18.

On behalf of our team at U.S. Global Investors, Happy Thanksgiving! Have a safe and relaxing weekend surrounded by family, friends and loved ones!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.78%. The S&P 500 Stock Index rose 1.52%, while the Nasdaq Composite climbed 0.72%. The Russell 2000 small capitalization index gained 1.10% this week.

- The Hang Seng Composite lost 2.33% this week; while Taiwan was up 1.89% and the KOSPI fell 0.27%.

- The 10-year Treasury bond yield fell 13 basis points to 3.69%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Jet 2, up 11.9%. China Eastern Airlines announced it would raise ceiling prices, namely no-discount airfare for economy-class for seven domestic routes, together with its wholly-owned subsidiary Shanghai Airlines. This followed the new regulation issued by the Civil Aviation Administration of China (CAAC) in December 2017, which allows Chinese airlines to raise the ceiling price for domestic routes by 10% in each flight season (twice a year), but cannot raise the ceiling price for the same route for three consecutive times.

- ZTO Express reported adjusted net income attributable to shareholders of 1.9 billion renminbi (+64% year-over-year) in the third quarter, beating the Bloomberg consensus by 24%. Revenue came in 8.9 billion renminbi, up 21% yoy, driven by 12% yoy growth in parcel volume and a 10% yoy increase in prices.

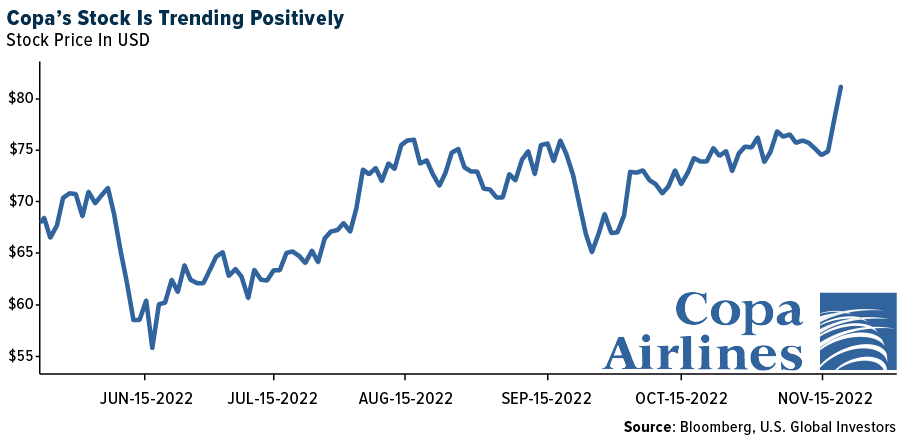

- Copa Airlines’ third-quarter earnings per share (EPS) of $2.91 exceeded consensus’ $2.74, and its earnings before interest and taxes (EBIT) margin of 17.8% also came in ahead of consensus’ 17.5%. The Panamanian carrier’s beat was driven by stronger non-fuel cost performance.

Weaknesses

- The worst performing airline stock for the week was Finnair, down 9.4%. Star Bulk Carriers reported a third-quarter adjusted EPS of $1.33, slightly below consensus of $1.41. The results were driven by 3Q rates of $24,365 per day, which were in line with consensus of $24,494 per day. Fourth-quarter bookings came in at 66% at $22,772 per day per vessel, which is lower than consensus.

- Due to the further deterioration of Chinese volume in Guangzhou, domestic passenger volume per seat capacity slightly declined to between 28% and 35% of 2019 levels, according to per Flight Master. Domestic passenger load factor (PLF) edged down to 64% from 66% in the prior week. Daily aircraft utilization for narrow-body aircraft slipped to 2.5 hours from 2.6 hours in the prior week.

- The air cargo market is oversupplied, possibly by as much as 9.7% as demand has fallen 5.5% when compared with the prior year (January-August). Capacity growth through dedicated freighters and passenger-to-freighter conversions continues with no moderation of supply anticipated in the near term. Air cargo spot rates have tumbled by two thirds since December 2021.

Opportunities

- In its annual survey, the Airports Council International (ACI) found that 86% of respondents are planning to travel by air in the year to come, the highest such score since the start of the pandemic. Further, the most recent Global Business Travel Association (GBTA) survey noted strong expectations of growth in business travel in 2023. Close to 80% of travel managers expect more business trips in 2023 compared to 2022. Among travel suppliers, 85% of respondents expect bookings by corporate clients to be higher or much higher in 2023. More than 65% of travel managers are optimistic that their company will conduct more internal and external travel.

- The huge need for European natural gas in the wake of the invasion of Ukraine and a severe shortage of ship capacity has sent spot rates on liquid natural gas (LNG) tankers to record highs. Over the course of 2022, rates have increased to between $200,000 and $500,000 a day, and that may last for a few years, participants in a panel debate at the Marine Money conference in New York said on Thursday.

- Copa’s revenue strength is coming mostly from leisure, but management said that there has been a recent uptick in corporate demand, currently at 75% of 2019 levels, with business now representing 25% of total revenues. On the fleet side, the company expects to receive 13 aircraft next year and has already secured financing for seven of them. Copa will discuss the restoration of dividend payments in the next board meeting, and it highlighted that it has been active on buybacks, with an active repurchase program of $200 million.

Threats

- Capacity in the first fiscal quarter of 2023 has been noticeably reduced for Spirit Airlines (-4.0%) and Allegiant Air (-1.7%). Spirit is adjusting its early 2023 network out of Florida by reducing frequencies to Fort Lauderdale, Tampa and Fort Meyers, as well as Philadelphia and Hartford. This is partially offset by additions to Las Vegas, Atlanta and Detroit. Allegiant’s reductions include Las Vegas, Asheville / Hendersonville, Phoenix and Punta Gorda, with a large addition to Nashville.

- According to Bank of America, Zim Integrated Shipping Services lowered its 2022 EBITDA (earnings before interest, taxes, depreciation and amortization) guidance by 6%, to between $7.4 billion and $7.7 billion. This decision is driven by a steeper-than-expected decline in freight rates, contract rates being renegotiated lower and weak demand. Zim notes that its contract rates were set above other liners as they were negotiated later in the season, when spot rates were higher.

- According to J.P Morgan, the environment for aviation in Latin America remains challenging. Oil price increases, high inflation, elevated interest rates and devaluing domestic currencies have been pressuring Latin American carriers, despite record top line trends during the third quarter. Airlines are facing cost increases especially on the fuel consumption side, though demand outlook remains solid for the near term.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 7.7%. The best performing country in Asia was the Philippines, gaining 2.8%.

- The Romanian leu was the best performing currency in emerging Europe this week, gaining 1.2%. The Malaysian ringgit was the best performing currency in Asia, gaining 1.6%.

- Turkish equities continue to outperform, supported by domestic buying and the government’s measures to support the economy before next year’s elections. The central bank of Turkey once again cut its one-week repo rate, despite inflation reaching 85.5% on a year-over-year basis in October. The Istanbul Stock Exchange is the best performing year-to-date, gaining 134% in dollar terms.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 1.0%. The worst performing country in Asia was Hong Kong, losing 2.2%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 0.2%. The Chinese yuan was the worst performing currency in Asia, losing 0.6%.

- Nomura analysts cited by Bloomberg calculated nearly 20% of China’s total economy is now affected by movement restrictions due to a growing number of covid cases. For now, China is avoiding widespread city lockdowns; however, if Covid cases continue to grow rapidly, the government may impose stricter measures.

Opportunities

- Reuters reported China is leading global initial public offering (IPO) activity this year, supported by easy monetary policy and a lack of clarity on access to offshore capital markets. Refinitiv data showed China IPOs raised $71.2 billion. Although lower than the $98.5 billion raised a year earlier, the amount is much higher than the U.S. ($17.3 billion) and Europe ($16.4 billion). Chinese offerings have been largely confined to the domestic market as deals in Western markets tumbled.

- People’s Bank of China (PBOC) adviser Wang Yiming said China’s economy next year could grow above 5%, but only if Covid’s impact ends. He also noted China has limited room to lower rates, but slower Federal Reserve hikes in the U.S. next year will give China more policy room. The recovery in China will depend on the government’s rollout of support measures needed to lift the economy.

- Preliminary Eurozone PMIs for November were reported stronger than expected. The Manufacturing PMI rose to 47.3 while a reading of 46.0 was expected by Bloomberg Economists. The Service PMI was reported at 48.6, unchanged from the prior month, but above an expected 48.0.

Threat

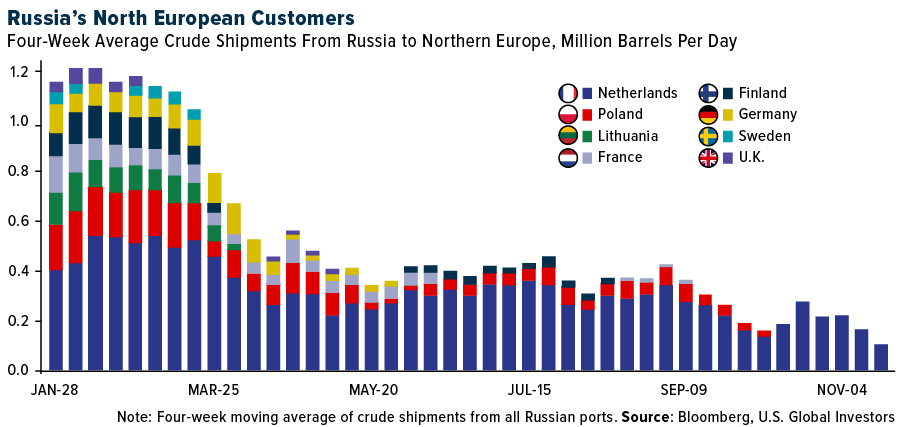

- The European Union (EU) plans to ban Russian seaborne crude imports starting December 5 and purchase the country’s oil products starting February 5. However, Europe has already cut imports from Russia, losing 90% of its market in the EU’s northern countries. The Netherlands is the only remaining European destination for seaborne deliveries outside of the Mediterranean/Black Sea basin. States like Lithuania, France, Finland, the United Kingdom and Germany halted such imports month ago, while Poland followed suit in September, Blomberg reported.

- Germany will send Patriot missiles and fighter jests to Poland as part of an air-defense deal following events from last week when two missiles landed in Poland near the border with Ukraine, killing two. Germany’s support for Poland may further escalate tensions between NATO members and Russia.

- China will release Manufacturing and Service PMIs next week. These economic indicators already fell into contractionary territory, below the 50-mark, but more weakness is expected due to ongoing covid lockdowns in China.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was natural gas, up 11.69%. Refining earnings in the third quarter exceeded expectations and showed continued execution to repair balance sheets to better than pre-COVID levels. Management teams indicated that overall fourth-quarter demand remains robust so far. Quarter-to-date, they believe margin capture will be flat to slightly down. Overall, refining continues to work well into 2023 on lower U.S. refining capacity, high international natural gas costs and steady demand, all while several potential catalysts are on the horizon. Refining stocks have continued to attract both generalists and energy-dedicated investors as shareholder returns continue to ramp.

- According to Trafigura CEO Jeremy Weir, Europe and the U.S. are bigger drivers of metal demand, as opposed to China, as the energy transition boosts usage of materials like copper. It’s a big shift, Weir noted, as there is much more consumption emerging from Europe and the U.S. for electrification.

- Countries around the world are scrambling to secure shipments of the power plant and heating fuel from major exporters like Qatar and the U.S., but there is little new supply coming online before 2026. Meanwhile, Europe is racing to replace Russian pipeline gas with liquified natural gas (LNG), further exacerbating the global shortage of fuel. This means importers will be forced to depend more on the volatile and expensive spot market, which is currently trading nearly three times higher than long-term contracts. Roughly 30% of all LNG deliveries were via the spot market last year, according to the International Group of Liquefied Natural Gas Importers (GIIGNL).

Weaknesses

- The worst performing commodity for the week was palladium, down 6.21%. The U.S. oil futures curve flipped to contango, a bearish market structure, for the second time this month, spoking traders to exit bullish positions on potential weaker demand going forward.

- Global urea benchmarks were lower, with Egypt down $55 to $580 per ton and NOLA down $20 to $510 per ton as sellers cut prices to secure sales. Second, phosphate prices were lower with Brazil MAP down $5 to $615 per ton but NOLA DAP down $35 to $645 per ton on average. Third, global potash prices were lower with Brazil down $15 to $570 per ton and SE Asia $50 lower to $700 per ton on average.

- According to J.P. Morgan, the key takeaways from the October World Steel data are: 1) China’s crude steel output dropped 11% month-over-month to a 939 (million tonnes per annum) Mtpa rate, but is up 11% year-over-year due to the soft 2021 base (YTD is down 2.2%), 2) Rest of World steel output remains down 10% YoY at five-year lows, with the EU and U.S. production decelerating further, and 3) Global steel production is down 4% year-to-date.

Opportunities

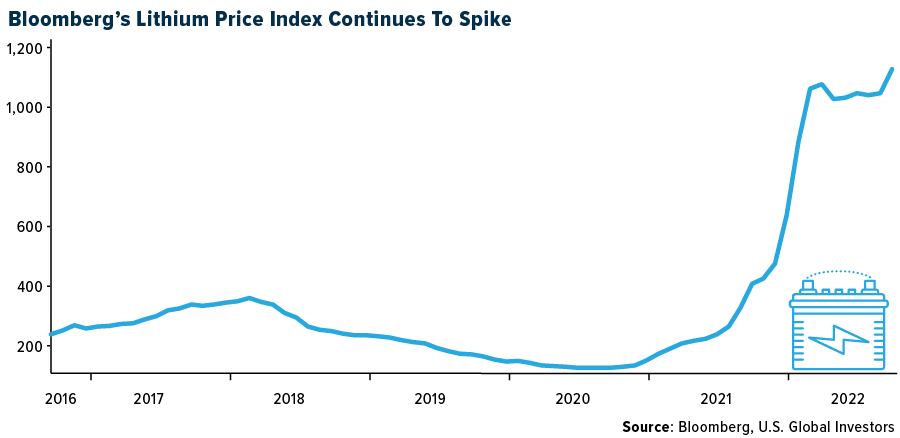

- Lithium prices continued to edge higher week-over-week by 1% in the range of $76,000 and $80,000 per ton. According to Benchmark, market participants reported cell manufacturers were limiting their production in November, which weighed on lithium demand sentiment, though this speculation has yet to be confirmed. The market participants noted the limited production could have been driven by the expectation of marginally lower demand in the first fiscal quarter of 2023 due to the cessation of the Chinese electric vehicle (EV) subsidies and Chinese New Year. With that said, demand in 2023 may remain robust on consumer preference and other government-provided EV incentive programs.

- According to S&P Global in its detailed report “The Future of Copper,” global copper demand is expected to grow from 25 million tons today to 50 million tons in 2035 and 53 million tons by 2050, should the world stay true to its 2050 net-zero targets. While China is forecast to drive this demand and is currently the largest user of copper, growth is closely followed by Europe, the United States and India, which together are expected to represent 70% of the global demand by 2035. S&P Global estimates a $4.18-per-pound copper price as the minimum price required to incentivize new supply.

- Infrastructure spending is starting to show up in the domestic economy. Deere’s share price surged 4.4% intraday toward a seven-month high on Wednesday, after the agriculture, construction and forestry equipment maker reported fiscal fourth-quarter sales that were well above expectations, and provided an upbeat full-year outlook, citing positive farm fundamentals and fleet dynamics and increased investment in infrastructure. The Inflation Reduction Act of 2022 should continue to drive domestic mining and spending to support an electric energy future.

Threats

- No fuel is more essential to the global economy than diesel, as highlighted by Bloomberg this week. It is essential to move trucks, ships and trains, and for heating homes during the winter. Expectations are that almost every region on the planet will face the danger of a diesel shortage within the next few months. Stockpiles are at their lowest point in four decades in the U.S., and residents in the Northeast can expect to pay 45% higher prices vs. last winter. In Europe, diesel futures are $40 above Brent vs. a five-year seasonal norm of $12. This could lead to a spike in inflation over the winter.

- At the Group of 20 Summit in Bali this week, Indonesian Investment Minister Bahlil Lahadalia floated the idea of an alliance that he said would help to unite government policies on the in-demand battery metal (lithium) and psush the development of the downstream industry. The plan has been discussed with both Canada and Australia. The idea also fits with Indonesian President Joko Widodo’s strategy of the nation becoming a hub for more refining of metals and even production of electric vehicles.

- According to Goldman, capping gas prices at the exchange level, as has been proposed this week by the E.C., likely has added detrimental effects, such as (1) further reducing liquidity in an already liquidity-poor market, (2) increasing the risk of a reduction in gas supply, and (3) disrupting commercial risk management.

Luxury Goods

Strengths

- One after another, luxury goods companies have reported bumper sales and profits despite inflation, as the world’s wealthy enjoy a “roaring 20s” age of decadence similar to the boom in the postwar period a century ago, writes The Guardian. This week, the company behind Veuve Clicquot and Moet & Chandon said it was “running out of stock on our best champagnes,” as it struggles to meet pent-up demand as parties take off following the full easing of Covid restrictions. In addition, companies like Burberry reported an 11% increase in sales in the three months ended September, and Kering reported a 14% increase in its latest third-quarter sales.

- Rolex, the biggest Swiss luxury watchmaker, is planning a major new production facility in Bulle, Switzerland, reports public broadcaster RTS (Radio Television of Serbia) and Bloomberg. Rolex could invest 1 billion Swiss francs in the manufacturing operation, creating about 2,000 new jobs. The facility would aim to begin operations in 2029.

- Ralph Lauren, was the best-performing S&P Global Luxury stock, gaining 6.4%. Over the weekend, Naomi Biden, the eldest granddaughter of President Joe Biden, wed her husband Peter Neal on the South Lawn of the White House. For the big day, she wore a Grace Kelly-inspired lace dress by Ralph Lauren.

Weaknesses

- Due to recent Covid outbreaks in China, luxury car brands are offering up to 20% price discounts. One of them is Mercedes-Benz, which is offering a price cut of up to 130,000 yuan ($18,172) on its high-end models, and at the same time, Audi and BMW have cut the prices by 110,000 ($15,376) and 80,000 yuan ($11,182), respectively. The decline in sales in the third quarter resulted from lower consumer demand; last year, it was because of the auto chip shortage and the high market prices.

- The Service PMI Index, one of the most important leading indicators of the U.S., decreased in November, coming in at 46.1 vs. 47.8 expected. It represents a stronger-than-expected contraction in North American services activity, pointing to economic slowdown.

- Chow Tai Fook Jewellery Group was the worst-performing S&P Global Luxury stock, losing 20.3%. Shares dropped on expectations that the latest Covid outbreak in China will weigh on the company’s profits.

Opportunities

- According to an article from Vogue Business, fashion had a limited impact on negotiations at this year’s UN Climate Change Conference (COP27). This makes sense, however, as higher priority items such as the War in Ukraine, protests in Iran and ongoing supply chain delays took precedence. LVMH kicked off the conference, though, by unveiling plans to work with King Charles III’s Circular Bioeconomy Alliance to build a regenerative agroforestry system. This comes with hopes of coupling cotton production with biodiversity restoration in Africa. The company’s environmental director said this builds on the group’s work implementing regenerative agriculture in its Turkish supply chain.

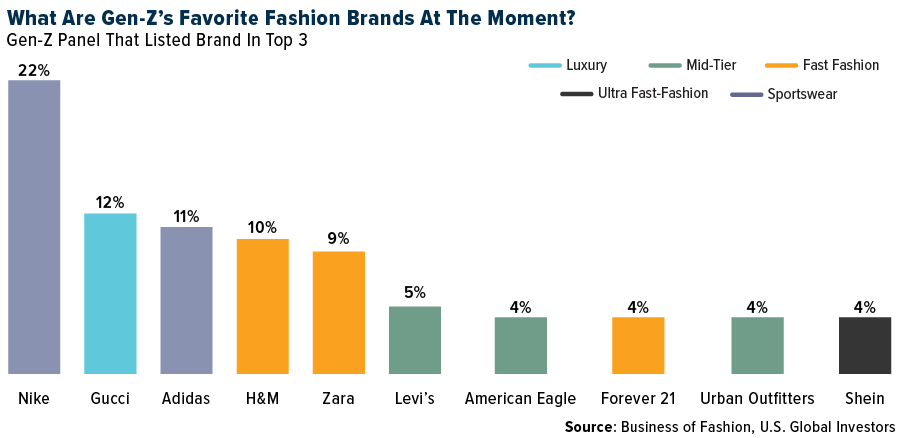

- According to a Business of Fashion (BoF) report, Gucci is the favorite luxury brand, while Nike is the number one sportswear brand for Gen Z consumers (those born between 1997 and 2010). This particular group of consumers represents 25% of the world´s population and has a purchasing power of about $360 billion, according to Bof. Despite being an important target market for luxury brands, Hen Z presents significant marketing challenges since they are digital natives. Gucci is the only luxury brand in the top 10 for this group of buyers because it has offered different experiences, such as providing NFTs and virtual spaces on Roblox (a leading gaming platform).

- Luxury brands are looking for different ways and scenarios to reach a new audience and expand their client base, reaching into sports events and targeting sport teams as new clients. One good example of this strategy is the presence of Louis Vuitton and Hublot at the FIFA World Cup, the world´s largest sporting event that is taking place in Qatar. Louis Vuitton launched the campaign “Victory is a State of Mine,” featuring Lionel Messi and Cristiano Ronaldo. Hublot is the official timekeeper for the tournament, reports Jing Daily from China.

Threats

- Based on a new report developed in partnership with Business of Fashion and eBay, which analyzes luxury customer behavior, shoppers now see luxury brands as a currency because they believe their luxury purchases will increase in value over time. According to the report, 62% of luxury shoppers have sold luxury accessories for a profit. E-commerce pioneers like eBay take an essential role in this secondary market, affecting the sales in the physical stores which the luxury brands target to offer customers a memorable experience.

- Leading luxury brands such as LVMH, Hermès, Swatch Groups, Richemont, Burberry, Gucci and Salvatore Ferragamo, have expressed concerns related to the potential contraction of the luxury Chinese market due to growing number of Covid cases. The latest Covid outbreak in China could result in the government imposing more restrictive measures to bring the outbreak under control.

- According to Bloomberg, the ISM Manufacturing PMI for the U.S. is expected to decrease from 50.2 in the previous month to 49.8 in November. It could represent a contraction in the general state of the economy, including in the luxury goods industry. The United States is one of the leading luxury goods markets worldwide.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Litecoin, rising 35.76%.

- Binance CEO Changpeng Zhao, or “CZ,” and several deputies met with investors in Abu Dhabi last week to raise cash for a crypto industry recovery fund. CZ and his team held meetings with potential backers, including entities affiliated with UAE National Security Adviser Sheikh Tahnoon bin Zayed, who oversees a large financial empire, according to an article published by Bloomberg.

- Crypto markets have steadied as Bitcoin climbed for a second day, trading back above $16,000. Ark Invest’s Cathie Wood is sticking to her bullish forecast of $1 million Bitcoin by 2030, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Chiiliz, down 20.57%.

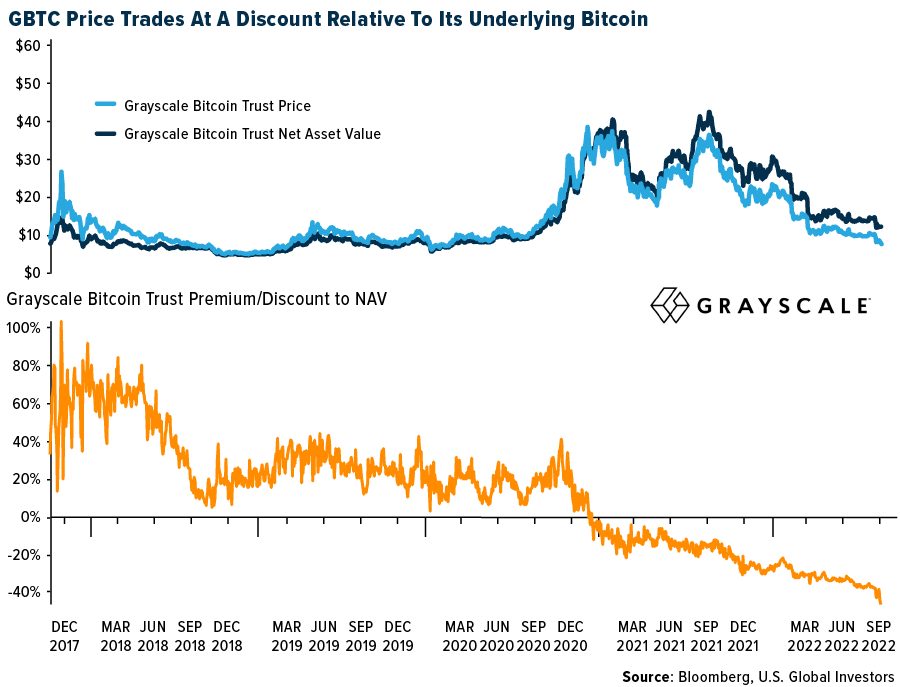

- Cascading crypto blowups have only exacerbated problems for Grayscale’s $10.5 billion Bitcoin Fund. The Grayscale Bitcoin Trust closed a record 45% below the value of its underlying coins on Friday, according to Bloomberg data, and shares fell another 5% on Monday. The dislocation has widened dramatically in recent weeks as GBTC, which can’t redeem shares unlike traditional ETFs, has fallen to a greater degree than Bitcoin itself.

- New York Governor Kathy Hochul has signed one of the most restrictive laws in the U.S. on regulating cryptocurrency mining, becoming the first state to impose such a ban. The bill triggers a two-year moratorium on new permits for crypto mining companies that are powered by fossil fuels.

Opportunities

- Wall Street’s waning conviction in Coinbase Global has done little to deter Cathie Wood. Instead, she’s been scooping up shares of the struggling cryptocurrency exchange in the wake of the collapse of Sam Bankman-Fried’s FTX. Wood’s Ark Investment Management funds have bought more than 1.3 million shares of Coinbase since the start of November, worth about $56 million.

- The Wild West days of crypto are back as the large trading houses that once thrived on arbitraging price gaps pull back in the wake of FTX’s collapse. That’s opening up profitable opportunities for anyone who still dares to trade. The gap between the funding rates of identical Bitcoin futures on Binance and OKX, for instance, has been as wide as an annualized 101 percentage points, writes Bloomberg.

- Crypto billionaire Mike Novogratz said the “crisis of confidence” in the digital asset world will drive more cryptocurrency users to seek out institutional players like Fidelity Investments. “The big winners in this are going to be people like Fidelity who have just come out with their crypto product,” Novogratz commented.

Threats

- Bitcoin dipped firmly below $16,000 as crypto markets dealt with the FTX shockwaves. The bearish price action also comes in the wake of risk-off trading in the stock market. The global crypto market, which was as high as $3 trillion in November 2021, stood at only $790.3 billion, according to CoinMarketCap data. With increased downward pressure in cryptos, liquidity on centralized exchanges appeared to have also taken a nosedive.

- Exchange-issued crypto tokens such as bankrupt FTX Group’s FTT can pose “extreme” risk when accepted by their issuers as collateral, Bank of England Deputy Governor Sir Jon Cunliffe said. Cunliffe said the volatility of unbacked crypto assets like exchange tokens makes them vulnerable to runs, exacerbating their price swings, according to an article published by Bloomberg.

- In a conference call on Tuesday, top partners at the powerful venture capital firm Sequoia Capital apologized to investors by backing FTX, a pair of bankrupt cryptocurrency exchanged that had allegedly been mismanaged by Sam Bankman-Fried.

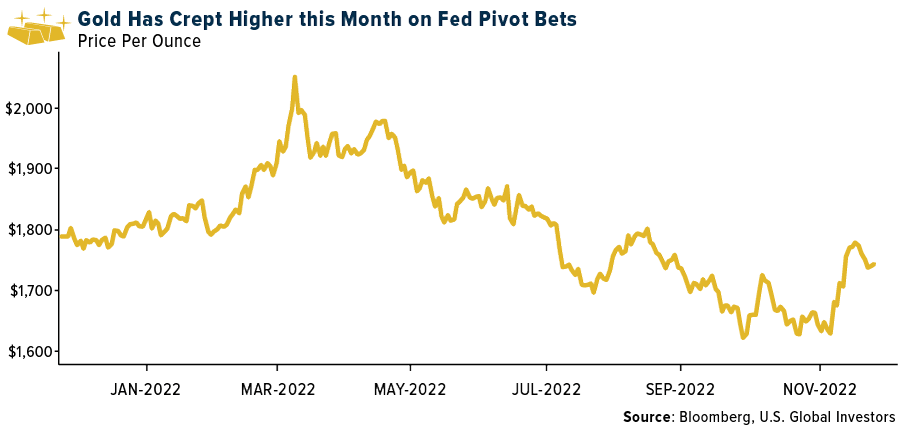

Gold Market

This week gold futures closed the week at $1,768.50, down $0.50 per ounce, or -0.03%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.97%. The S&P/TSX Venture Index came in flat at -0.02%. The U.S. Trade-Weighted Dollar fell 0.83%.

| DATE | EVENT | SURVEY | ACTUAL– | PRIOR |

|---|---|---|---|---|

| Nov-23 | Durable Goods Orders | 0.4% | 1.0% | 0.4% |

| Nov-23 | Initial Jobless Claims | 225k | 240k | 223k |

| Nov-23 | New Home Sales | 570k | 632k | 588k |

| Nov-28 | Hong Kong Exports YoY | — | — | -9.1% |

| Nov-29 | Germany CPI YoY | 10.4% | — | 10.4% |

| Nov-29 | Conf. Board Consumer Confidence | 100.0 | — | 102.5 |

| Nov-30 | Eurozone CPI Core YoY | 5.0% | — | 5.0% |

| Nov-30 | ADP Employment Change | 200k | — | 239k |

| Nov-30 | GDP Annualized QoQ | 2.8% | — | 2.6% |

| Nov-30 | Caixin China PMI Mfg | 48.9 | — | 49.2 |

| Dec-1 | Initial Jobless Claims | 233k | — | 240k |

| Dec-1 | ISM Manufacturing | 49.8 | — | 50.2 |

| Dec-2 | Change in Nonfarm Payrolls | 200k | — | 261k |

Strengths

- The best performing precious metal for the week was silver, up 2.02% largely on improved sentiment across the precious metals space, except for palladium, with the Fed Minutes indicating a more moderate interest rate path ahead.

- This week, UBS identified three structural reasons in favor of gold:

1) Long-term investors and the official sector are gradually building gold allocations. Central banks have been net buyers of gold for more than a decade now, amid a broader trend of diversifying dollar-denominated reserves. This year, the Russia-Ukraine war and corresponding sanctions reinforced this theme. Net official sector buying to 3Q22 is already higher than previous full-year highs.

2) The proportion of gold holdings relative to overall assets held by institutional investors remains light, in their view, and they think it is likely held more for diversification and portfolio protection rather than expectations of outright material price appreciation. This implies more resilient core positions and scope for allocations to grow.

3) Strong physical demand has also been a key factor affecting the relationship between gold and real rates, in their view. Key physical gold markets India and China have continued to buy large volumes of gold this year, helped by cheaper prices as gold came under pressure from macro forces.

Weaknesses

- The worst performing precious metal for the week was palladium, down 6.47% on little specific news. Harmony Gold’s first fiscal quarter gold produced is down 1%, but gold sold is up 4% and mining revenue is up 5%. Following the restructure of Tshepong, Harmony comments that Tshepong North & South have performed well, due to better recovered grades. Load curtailment has had a negative impact on first-quarter production, resulting in 3,200 ounces lost production. All-in sustaining costs (AISC) of $1,657 per ounce are 2% down year-over-year and 4% down quarter-over-quarter, but 8% up above consensus.

- The Australian Broadcasting Commission (ABC) reported that Cadia gold mine’s expansion approval was revoked after it failed an air quality audit. Newcrest’s proposed Cadia expansion to 35 million tons per annum (mtpa) from 32 mtpa was approved in December 2021 subject to conditions. ABC reports the independent audit returned findings in October that included one vent shaft was emitting 18 times what is legislated as safe amounts of carcinogen respirable crystalline silica. A second vent also exceeded limits.

- The government of Ghana let creditors know they should expect a 30% haircut on its outstanding bonds as it attempts to negotiate a new rescue package with the International Monetary Fund (IMF). Consequently, all gold miners, such as Newmont, AngloGold Ashanti and Gold Fields, must sell 20% of their gold production to the nation’s central bank which will use the gold to purchase oil for the country.

Opportunities

- Lucara Diamond announced that it’s extended its sales agreement with Belgium-based HB Trading BV (HB) for another 10 years, for the sale of its gem quality rough diamonds from the Karowe mine. This integrated approach de-risks any cash flow uncertainty from the sale of high-value diamonds and allows for potential revenue upside through polished price participation. The HB agreement has accounted for 60-70% of Lucara’s total revenue since first partnering in 2020.

- Bloomberg recently interviewed Nouriel Roubini with a view to where investors should park some money for the next decade. Roubini noted the current problems of inflation, geopolitical and environmental risk suggest one, very short adjustable-rate Treasuries, secondly own some Treasury Inflation-Protected Security (TIPS) because inflation expectations have not yet de-anchored and third, go back into gold and precious metals. He pointed out China has trillions of dollars in reserves in dollars that it is likely to move to other assets that can’t be sanctioned or seized by the U.S. or Europe.

- UBS has updated its near-term gold price forecast in line with the more bullish view from its Strategy team, which is now looking for the Federal Reserve to cut from 5% to 3.25% by the end of 2023, pushing gold to $1,900 per ounce.

Threats

- At its investor day, Barrick Gold highlighted in detail its strategy of creating a long-term, sustainable business with growth and exploration optionality. It provided an updated five-year outlook indicating gold production growth through 2027. Forecast gold cash costs have increased in 2023 given current global inflationary pressures, but then fall over time given higher production and the assumption of easing inflationary pressures

- There have been guidance revisions and cautious commentary from peers through 2022, and the market response suggested a belief that Barrick was immune from many of the inflationary pressures and production challenges affecting the rest of the market. Barrick provided rough revised five- and ten-year guidance at its investor day which showed some of the same impacts to Barrick in 2023 and going forward.

- Barrick’s plans indicated 2023 attributable capex of around $2.6 billion, up from $2.3 billion in 2022 and above consensus of $2 billion. Part of the increase is from the Pueblo Viejo (60% Barrick, 40% Newmont) expansion and new tailings facility that is now expected to cost $2.1 billion (100% basis), up from $1.4 billion previously.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

American Airlines Group Inc.

Delta Air Lines Inc.

United Airlines Holdings Inc.

Southwest Airlines Co.

Copa Holdings SA

Star Bulk Carriers Corp.

Allegiant Travel Co.

Zim Integrated Shipping Services Ltd.

LVMH Moet Hennessy Louis Vuitton SA

Burberry Group PLC

Kering SA

Mercedes-Benz Group AG

Bayerische Motoren Werke AG

Hermes International

Cie Financiere Richemont SA

Ralph Lauren Corp.

Harmony Gold Mining Co. Ltd.

AngloGold Ashanti Ltd.

Lucara Diamond Corp.

Barrick Gold Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits