Crude Tanker Rates Could Reach a Jaw-Dropping $200,000 a Day Next Year

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOver the past 12 months, global container shipping rates have steadily declined to their long-term averages as supply chain snarls have receded and backups at ports have disappeared.

Now, another segment of the cargo shipping industry is seeing day rates explode to record highs.

So-called dirty tankers, those that carry crude oil, are charging over $100,000 a day for their services as international sanctions against Russia force ships—including Suezmaxes, Aframaxes and very large crude carriers (VLCCs)—to take longer, more circuitous routes. Carriers that once made deliveries to the North Sea port of Rotterdam via the Baltic Sea are now having to sail to China, India and Turkey, which are twice or three times the distance.

All three countries have said they will continue to buy Russian oil.

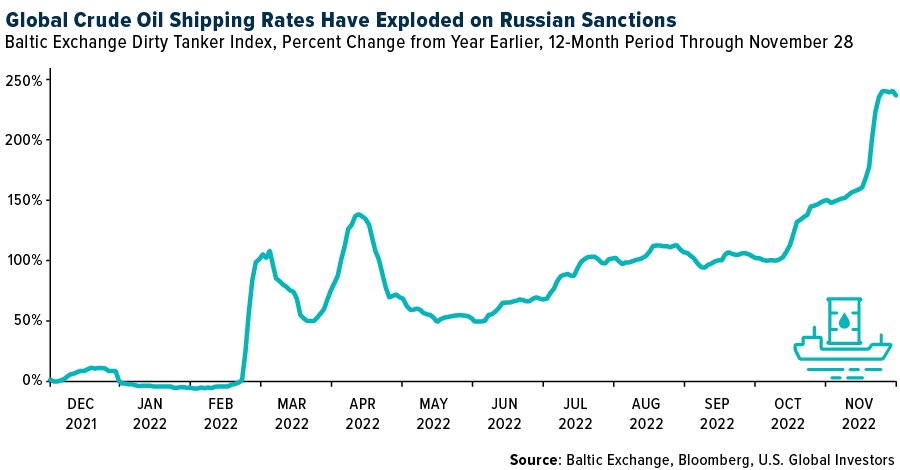

The Baltic Exchange Dirty Tanker Index, which measures shipping rates on 12 international routes, rose as much as 243% for the 12-month period through the end of November.

So how high could rates go? According to Omar Nokta, a shipping analyst at Jefferies, they could potentially climb to between $150,000 and $200,000 a day.

We’re almost there now. The Aframax day rate to ship oil from the Black Sea to the Mediterranean hit an astronomical $145,000 a day during the week ended November 18, according to Compass Maritime.

Russia Oil Turmoil To Drive Tanker Market Higher

The 27 countries of the European Union (EU) are scheduled to ban crude imports from Russia, the world’s number two producer, this coming Monday, December 5, and all Russian oil products by February 5, 2023. This will have the effect of disrupting global trade routes further, driving up rates even more.

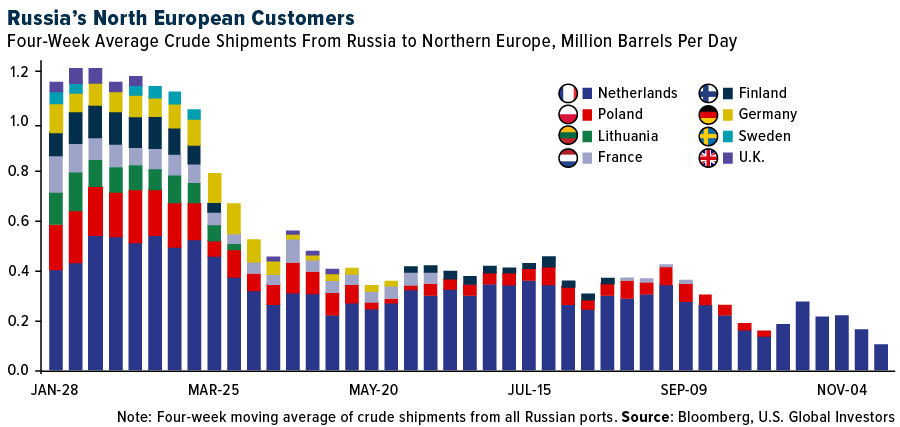

As you can see below, Europe’s imports of Russian oil are already down dramatically from the beginning of 2022, when the country invaded Ukraine. The Netherlands was the only remaining European destination for deliveries outside of the Mediterranean and Black Sea basin. To help offset the loss of Russian supply, Norway will ship a record volume of North Sea oil in January, Bloomberg reports.

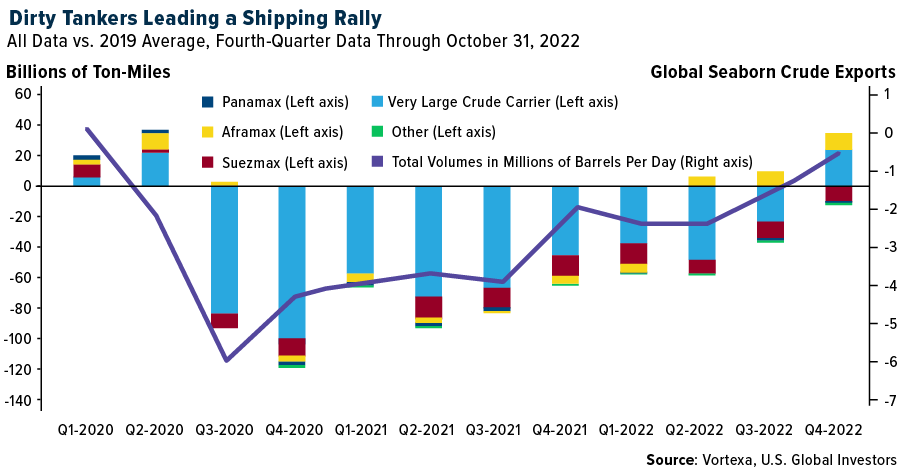

Due to changes in shipping routes, demand for oil tankers is expected to surge to levels not seen in three decades, according to Clarkson Research. The U.K.-based group is forecasting that the number of ton-miles, defined as one ton of freight shipped one mile, could increase 9.5% next year. That would mark the largest annual increase since 1993.

Volumes are already at pre-pandemic levels, with VLCCs and Aframaxes having exceeded 2019 volumes for the first time since the second quarter of 2020.

Oil Tankers Generating Record Revenues, Stocks Hitting New Highs

Also supporting rates is the fact that oil carriers are replacing vessels at a historically low pace.

In July, Clarksons reported that new shipbuilding orders for container vessels had surpassed those for tankers for the first time ever. Whereas the global orderbook for containerships stood at 72.5 million deadweight tonnage (dwt)—a measure for how much weight a ship can carrier—the orderbook for crude oil and oil product tankers was 34 million dwt, a new record low.

This has contributed to massive revenues and net income, which should keep carriers in a strong position even as container rates have dried up. This week, Mitsui O.S.K. Lines president Takeshi Hashimoto told JPMorgan analysts that he believes profits will remain strong due to the company’s liquified natural gas (LNG) business as well as dry bulkers and tankers.

Frontline, the fourth largest oil tanker company, just reported net income of $154.4 million in the third quarter, compared to $108.5 million estimated.

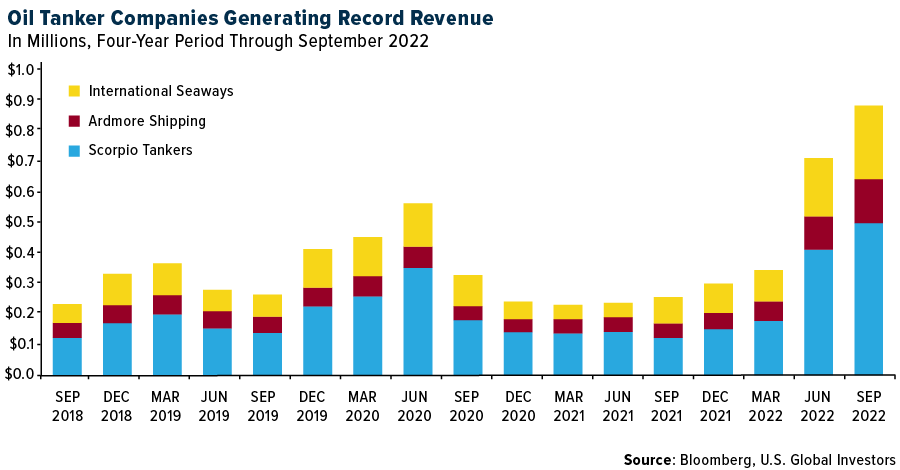

Below you can see how revenues have surged for companies such as International Seaways, Ardmore Shipping and Scorpio Tankers.

With the S&P 500 still down more than 13% for the year, shares of a number of oil tankers have hit new all-time highs recently. Among those are Ardmore, International Seaways and Euronav. Teekay Tankers is up 219% year-to-date, while Scorpio is up 321% over the same period.

Will these returns continue? I can’t say, of course, but the structural support doesn’t appear to go away anytime soon.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.24%. The S&P 500 Stock Index rose 1.06%, while the Nasdaq Composite climbed 2.09%. The Russell 2000 small capitalization index gained 1.17% this week.

- The Hang Seng Composite gained 6.07% this week; while Taiwan was up 1.30% and the KOSPI fell 0.14%.

- The 10-year Treasury bond yield fell 20 basis points to 3.481%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Bombardier, up 14.4%. According to CLSA, it appears upgrades also come in clusters, with Qantas lifting its first half 2023 guidance to A$1.35-A$1.45 billion, roughly one month after releasing previous record guidance. Improved net debt guidance of A$2.3-A$2.5bn was also a key positive. Given the company’s strong balance sheet position and expectations, its current buyback will be completed in the first half of the year. Qantas forecast an A$400 million buyback to be announced in February.

- A.P. Moller-Maersk A/S, the Danish transport giant, said it’s seeing signs that a sharp decline in demand for shipping containers is starting to moderate. “Following a sharp decline, the demand for ocean transportation is now stabilizing, and we are adjusting our network to match the new reality,” Morten Juul, head of Maersk’s Asia Pacific Ocean business, said in a market update for November. “This will limit the weekly ad hoc adjustments and enable customers to plan their supply chain better.”

- Net sales through the leisure channel improved this week to -7.9% versus 2019, driven primarily by better volumes. Domestic and international leisure volumes were -15.7% versus 2019 and -3.2% versus 2019, respectively. The strong step in international volumes was offset by weaker pricing, which is now -5.1% versus 2019. Domestic pricing was up 9.5% versus 2019 (versus +11.6% prior).

Weaknesses

- The worst performing airline stock for the week was Sun Country, down 8.4%. After failing to reach a new agreement with unions representing its cabin crew, TAP Air Portugal was forced to cancel 360 flights on December 8-9 because of a strike. Chief Executive Officer Christine Ourmieres-Widener said that the canceled flights would result in about $8.3 million in losses. The strike affects almost 50% of TAP’s schedules and nearly 50,000 passengers in two days.

- Spot rates on the container market are continuing to plummet and fell by 18% this week on the Shanghai-Rotterdam route – the largest drop over the past two months. According to the WCI Index, the drop in spot rates has accelerated on Asia-Northern Europe routes this week, and has now almost reached pre-pandemic levels, falling by 84% compared to levels seen before the Chinese New Year in January 2022. Compared to the pre-pandemic level, the rate this week is now just 32% higher than the level seen in the same week in 2019 going into North Europe.

- European airline bookings as a proportion of 2019 levels declined by 5 points to -20% in the week, mainly driven by lower intra-Europe as well as international volumes. Total net sales were down 8% on a week-over-week basis. Intra-Europe net sales declined by 5 points to -27% versus 2019 and were down 6% week-over-week. International net sales fell by 4 points to -17% versus 2019.

Opportunities

- U.K. leisure carrier Jet2 Plc said full-year earnings are set to exceed analyst consensus as demand for its flights and package holidays endures through an economic slump. While margins will come under pressure from wage increases and the stronger dollar, winter bookings are encouraging and air fares remain robust, Jet2 said in a recent statement. The company has backed up its growth bid with a spate of orders for Airbus SE A320neo jetliners after switching last year from Boeing Co.

- Global container congestion declined to 8.8% of the fleet, while U.S. inland congestion has also improved as weaker import demand has improved system fluidity. While the threat of U.S. rail strikes lurks, Congress is likely to step in and order mandatory arbitration if no agreement can be reached. The system is much better positioned to absorb a disruption given easing congestion and weaker demand.

- According to JPMorgan, Indian airlines are at peak yield. The bank is optimistic on yield in the second half of 2023 as supply constraints and route optimization aid expansion. For IndiGo the holding cost can be offset by yield/compensation, but smaller airlines may see a more adverse impact.

Threats

- According to Abracorp, the corporate travel segment in Latin America registered R$1.0 billion billing in October 2022, down 4% versus October 2019, showing a deterioration versus September – which had R$1.2 billion billing, up 20% versus 2019 levels. This is negative for Azul and Gol, as corporate demand has been showing a recovery in the past months, which had been supporting yields.

- So far in 2022, the container shipping fleet has grown by 0.87 million TEU or 3.5%. Next year the orderbook is 2.5 million TEU or 9.8% gross growth. The following two years are 4.6 million TEU, or collectively the orderbook to fleet ratio is 29.6%. Of course, attrition will increase, but with only 21.6% of the fleet at 20-years of age in the scrapping zone, the offset to deliveries is likely to be brutally slow. This year, however, clearly the softening has not been caused by fleet growth, but a combination of softening demand and a reduction of port congestion have quickly swung the balance of supply/demand.

- Airlines continue to scale back presence at regional airports. Since the pandemic began and airlines have balanced route economics and hiring challenges, flight schedules have dropped at regional airports. According to the Regional Airline Association, 76% of the 430 airports in the continental U.S. and Hawaii had fewer flights scheduled in 2022 compared to 2019. Small airports have lost an average of 34% of flight traffic while larger airports saw an average schedule shrinkage of 16%.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 3.1%. The best performing country in Asia this week was Hong Kong, gaining 6.1%.

- The Polish zloty was the best performing currency in emerging Europe this week, gaining 1.5%. The Thailand baht was the best performing currency in Asia this week, gaining 2.9%.

- The Hong Kong Stock Exchange, which is heavily weighted with Chinese technology/internet stocks, noted strong gains over the past five days. There is growing optimism among investors that the Chinese Communist Party have started taking necessary steps for the economy to fully reopen next year.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 3.6%. The worst performing country in Asia this week was the Philippines, losing 1.7%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 3.2%. The Indian rupee was the worst relative performing currency in Asia this week, gaining 0.3%.

- JPMorgan Global Manufacturing PMI was reported at 48.8 versus 49.4 in October, pointing to a deeper slowdown in economic activity. China’s Manufacturing PMI dropped to 48.0 from 49.2. The U.S. Manufacturing PMI dropped from 50.4 in October to 47.7 in November. Manufacturing PMIs in the Eurozone ticked higher (to 47.1 from 46.4), but it remains in contractionary territory (below the 50 mark).

Opportunities

- Due to recent protests against Covid lockdowns in China, the government eased some anti-virus rules, but affirmed sticking with its zero-Covid policy for now. China will no longer set up gates to block access to apartment compounds where infections are found. Beijing will start to allow low-risk Covid positive individuals to isolate at home rather than at the government-run quarantine camps.

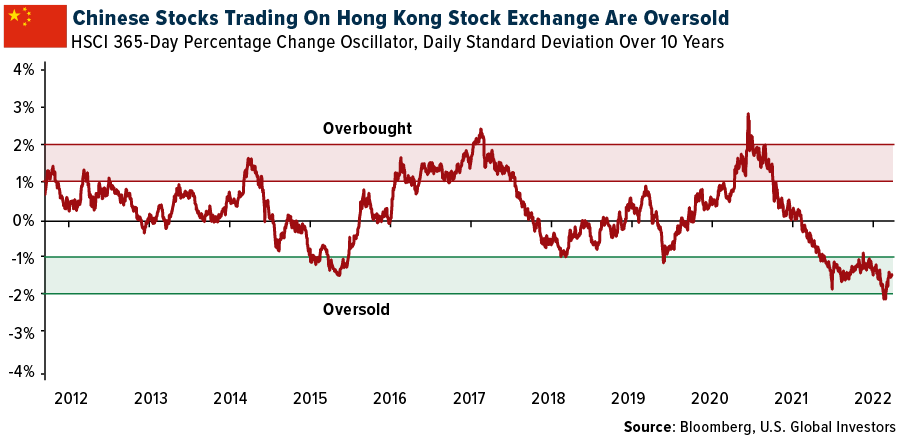

- Bloomberg economists are expecting China to fully reopen by the middle of next year. Further saying that China will gradually be relaxing measures over the next seven months leading to full economic reopening by the end of first half of 2023. Chinese stocks are oversold, and equites could continue to gain on expectations of market reopening.

- China announced five measures to support equity financing for real estate. Restrictions covering mergers and acquisitions (M&As), restructuring, replenishing working capital and refinancing will be lifted. Listed companies may also raise money through private placements to fund acquisitions of unfinished home projects.

Threats

- The recent protests that erupted in China due to the government’s zero-Covid policy could turn into wider protests showing peoples’ growing disapproval for the Chinese Communist Party. Many protestors are demanding the basic right of freedom, and some are asking for President Xi Jinping to resign.

- Russian forces keep attacking infrastructure and civilian complexes across Ukraine. Ukrainian President Volodymyr Zelensky says Russia’s military has destroyed some 30% of Ukraine’s power stations and people experience constant backouts with temperatures already below zero. It seems that Putin wants to break the people of Ukraine by leaving them without heat and electricity during winter. Many may wish for the war to end, but that wish may not come true this Christmas.

- The dollar has been weakening since its peak at the end of September and a price reversal could send emerging market currencies lower. The dollar oscillator, using a 60-day percentage change over the past five years, shows the dollar is in oversold territory. This suggests a reversal is approaching.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was nickel, rising 8.66%, perhaps on speculation over the announced EV growth plans of the major auto manufacturers to ramp up production dramatically in the coming years. Base metals advanced as investors bet Chinese protests may accelerate a shift away from zero-Covid policies, boosting the outlook for demand. Gold also gained. Copper rose as much as 2% after protests in China dissipated as authorities responded with a heavy police presence and a quiet loosening of some measures.

- Citing a company spokesperson, Reuters reports that some processes have resumed at BP’s 400,000 barrels per day Rotterdam refinery. The refinery operations have been suspended for a week due to a dispute with workers over wages. A BP spokesperson said that even though operations have resumed at the refinery, “We are still in dialogue with the unions to reach an agreement.”

- The latest $60 billion+ LNG supply deal between Qatar and China takes relations between the two countries to new heights. By securing a greater foothold in Qatar’s North Field East, China will gain an unparalleled hold over the biggest gas reservoir anywhere in the world.

Weaknesses

- The worst performing commodity for the week was natural gas, losing 14.60%, largely on a shift to milder weather forecasts and the Freeport LNG export hub likely to remain closed through year-end. With limited export capacity, prices tend to weaken, which has led to stranded gas with below-market prices. Oil did the opposite of natural gas, stringing together a four-day rally for its longest winning streak in two months, as reported by Bloomberg.

- According to Goldman, the paper industry has had significant cost inflation since 2020. Reported numbers from the third quarter show some signs of stabilization at high levels. Inflation was mainly driven by fuels and chemicals, and to a lesser extent, equipment, and labor. North America appears to have been hit the hardest, which Goldman thinks is explained by a combination of rising wood costs and more expensive in land transportation (mostly in Canada). Europe has been the region posting the lowest cost inflation.

- According to Random Lengths (“RL”), the Framing Lumber Composite decreased by $10 to $453, and the OSB Composite decreased by $44 to $360. For next week, RBC Elements forecasts that the RL Framing Lumber Composite will decrease $6 to $447, and the RL OSB Composite will decrease $37 to $323.

Opportunities

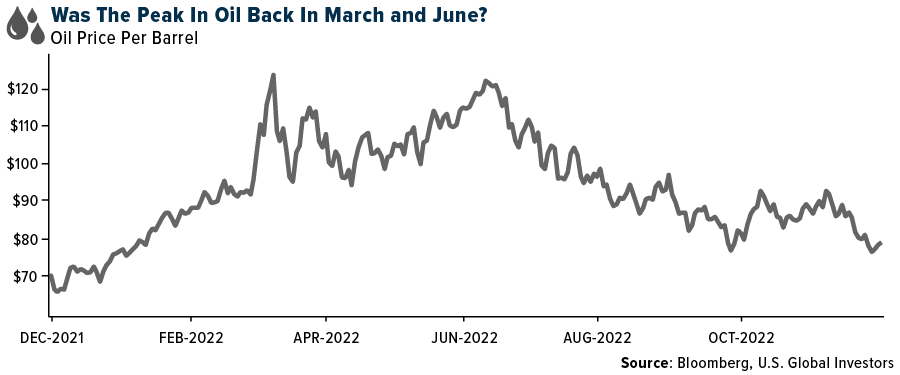

- Goldman continues to believe that the long-term commodity curve is undervalued, and that normalized Brent should be closer to $90 per barrel versus December 2024 at $75 per barrel, the near-term path has gotten more uncertain with front month having rapidly descended to $80-$85 per barrel. First, China consumption is surprising to the downside given Covid cases. Secondly, Russian oil supply has been resilient, and likely to track above consensus expectations.

- For the first time ever, green hydrogen is starting to compete on pure economics; in fact, it’s become a lower-cost alternative. This is still a nascent market, but green hydrogen is making headway around the world, and Europe is where the adoption curve is seeing the most potent boost.

- High natural-gas prices in Europe are likely to speed up the global energy transition, leading to strong copper demand, and good times ahead for miners.

European consumers have already shown a propensity to change behavior because of higher energy prices. Governments and utility companies will do the same, switching to renewable sources faster than they otherwise would. This transition will be heavily reliant on copper, the global conductor of choice, as more and more energy needs depend on the delivery of electricity.

Threats

- EU energy ministers failed to come to an agreement on the proposed gas price cap at EUR275/Mwh. The failure to reach an agreement on the price cap also led to a delay in approval of measures like joint gas purchases and quicker renewables permits. According to the press release from the European Council, the agreement on substance of other measures includes joint gas purchases, which will exclude Russian gas, and a new benchmark for gas prices.

- JPMorgan ultimately sees base metals prices once again retesting the lows approached earlier this year around mid-year 2023. With deeper cracks beginning to appear in the U.S. labor market over the second quarter of 2023, the macro focus will likely begin to swiftly shift from relief that the Fed hiking cycle is over to building concerns around the potential further fallout from U.S. rates rapidly rebasing to 5%. Adding in China’s reopening likely hitting a stumbling block and likely still-anemic levels of demand growth in some major regions outside of China, the group thinks base metals prices could hit an air pocket in in the second quarter.

- BHP Group Ltd., the world’s biggest miner, is warning that a shortage of skilled workers from mining engineers to mathematicians will hamper efforts to meet the soaring demand for metals crucial to the energy transition, as reported by Bloomberg. Laura Tyler, BHP’s chief technology officer, noted that to meet the demand for green metals, copper, lithium and nickel by 2040, the world will need 21% more mining and geotech engineers and 29% more metallurgists, citing a PricewaterhouseCooper LLP research. Tyler added “We need to train them now.”

Luxury Goods

Strengths

- Based on Knight Frank’s ranking of luxury home price growth for 2023, Dubai, which aims to become a luxury and investment hub in the Middle East, is leading the list with an increased price forecast of 13.5%, thanks to booming interest from foreign buyers. In second place is Miami, where prices are expected to increase by 5%. According to the report, European cities such as Lisbon, Dublin, Madrid, and Paris have an increase in price forecast to be around 4% next year. One reason could be the current global recession; buyers are looking for more exposure to the U.S. dollar, which is getting stronger and is suitable for the luxury industry, including homes and goods.

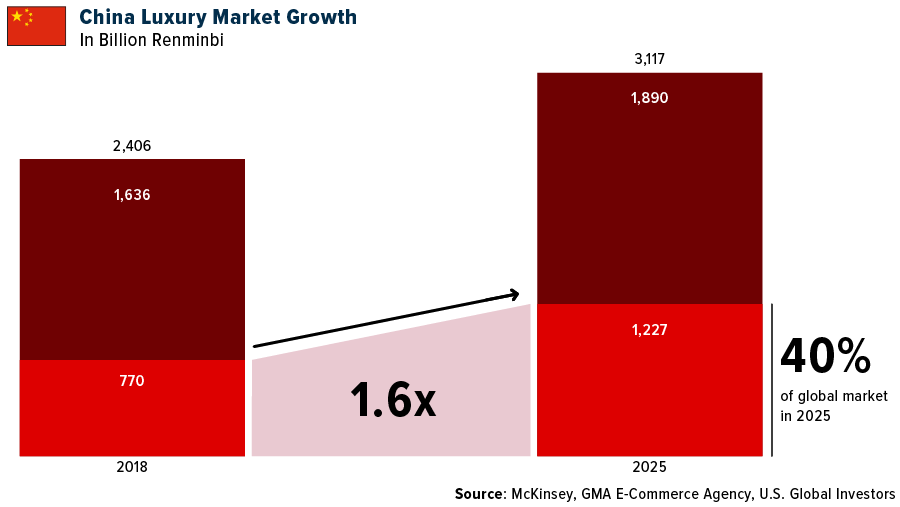

- China is one of the leading global luxury markets, representing around 35% of the market in 2020. In fact, 46% of luxury products in 2015 were bought by Chinese citizens and represented about $80 billion in 2021. China’s luxury market is expected to grow by around 4% by the year 2025. According to research by Bain & Co, Chinese customers will make 50% of their purchases in China (considering the prospect of China fully reopening after the Covid easing restriction by the government) which will benefit the luxury goods industry.

- Wynn Macau, a Chinese casino and hotel operator, was the best performing S&P Global Luxury stock for the week, gaining 56.7%. Undervalued Macau stocks gained in the past five days on expectations that the government will further ease Covid-related restrictions.

Weaknesses

- According to Bloomberg, the Manufacturing PMI Index, one of the most important leading economic indicators, especially in China (a leading luxury goods market worldwide), decreased in November. It was reported at 48 versus last month’s reading of 49.2.

- Shares at Mulberry Group PLC fell by more than 10% on Wednesday, reports Investing.com, after the luxury leather goods maker reported a first-half loss due in part to Britain’s cost-of-living crisis hitting demand in the country. In a statement, Mulberry said the decline stemmed from additional investment in marketing and technology, as well as acquisition costs in Sweden and Australia, which led to operating expenses ballooning by 42% to £48.6M.

- Farfetch Ltd., a Chinese online retailer, was the worst performing S&P Global Luxury stock for the week, losing 24.4%. Shares fell sharply on Thursday (down 35%) after the company reported a loss in the third quarter and provided a disappointing 2023 outlook.

Opportunities

- Based on an article from CNN, gaming and fashion may appear to be unlikely bedfellows, but what our avatars wear (characters in games like The Sims or Fortnite) has been of interest since these characters could first change their clothes. More recently, luxury labels have been keen to enter the video game space. For example, Louis Vuitton, Marc Jacobs and Tommy Hilfiger have all dabbled over the past few years, hosting runway shows in games and collaborating on outfits, often called “skins.”

- According to Jumpstart, the demand for luxury brands worldwide remains strong, and the luxury fashion market is predicted to reach about $332.98 billion in 2029, with a compound annual growth rate of 4.0%. Based on this research, the luxury brand that consumers need to pay attention to in 2023 is Chanel, which is planning to hire around 3,500 sales associates. The second is Burberry which is planning to invest more in omnichannel experiences, focusing on in-person and virtual appointments. Also, Hermès is investing in its entry into web3, and Louis Vuitton is looking to expand into new markets with its upscale take on hotels.

- Harrods’ restaurants have become a critical part of its business future. According to Bloomberg, Harrods is betting on fine dining to save the future of its luxury brand. The company launched the store’s Studio Frantzen on November 28, which has received around 1,500 reservations from all over the world.

Threats

- According to Bloomberg, the University of Michigan Consumer Sentiment Index in the U.S. is expected to decrease from 56.8 in the previous month to 56 in December. This index determines changes in consumers´ willingness to buy and helps to predict their discretionary expenditures. The reading could represent a small contraction in consumption levels in the U.S. including in the luxury goods industry.

- According to Bloomberg, the China Imports & Exports Trade Balance Index is expected to decrease from $85.15 billion in the previous month to $78.10 billion in December. This could mean a slight contraction in the economic activity level in China, including the luxury goods industry. China is one of the leading luxury goods markets worldwide, so the drop would be significant.

- Tesla is losing traction in the Chinese market because of the entrance of new electric vehicle (EV) players there. Global automakers have crammed the market with more than 200 EV models versus 120 models at year-end 2019 when Tesla launched production in Shanghai. The company will need more than price cuts to keep its market share in China at 11% in 2022 versus 16% in 2020.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Fantom, rising 32.44%.

- The European Union (EU) should step up the monitoring of digital currencies to prevent a situation where crypto crises like the collapse of the FTX exchange can pose a systemic risk, an EU lawmaker said. The bloc has reached a preliminary agreement on its first major crypto regulation proposal, known as Markets in Crypto assets, which would address supervision of service providers, as well as consumer protection and environmental safeguards for crypto assets such as Bitcoin and Ether, writes Bloomberg.

- Bitcoin spiked higher on Wednesday in the countdown to a speech by Federal Reserve Chair Jerome Powell that may cement expectations for a slower pace of interest rate hikes in the U.S. The token added 3.7%; the highest level in two weeks, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was BinaryX, down 19.88%.

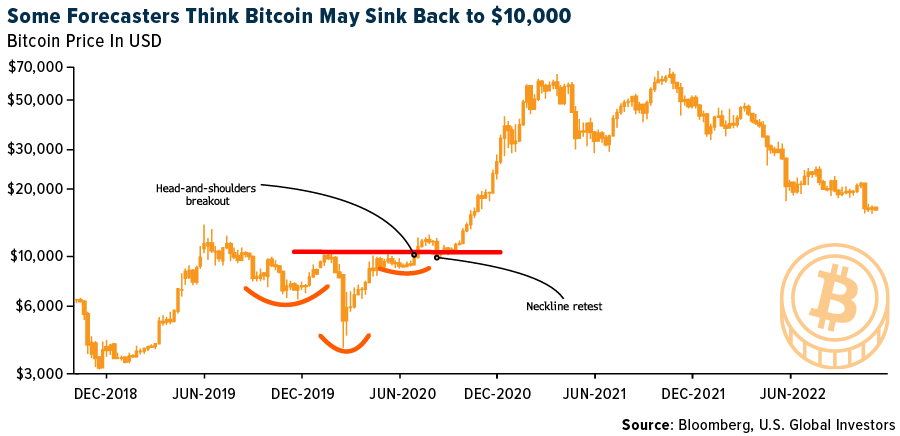

- The crypto route has room to run, according to veteran fund manager Mark Mobius who sees Bitcoin going down to $10,000. The co-founder of Mobius Capital Partners said in an interview Monday in Singapore that his next target for Bitcoin is $10,000 and he wouldn’t invest his own cash or client money in digital assets as it’s too dangerous, writes Bloomberg.

- The U.S. Securities and Exchange Commission is one of the largest creditors to BlockFi, which filed bankruptcy in the wake of a number of failures within the digital-assets space. The regulator has a $30 million unsecured claim against the crypto lender, which makes it BlockFi’s fourth-biggest creditor, writes Bloomberg.

Opportunities

- Binance bought a Japanese crypto exchange service provider to re-enter a market it said will play a “key role” in the future of cryptocurrency adoption. The firm acquired 100% of Sakura Exchange Bitcoin, paving the way for it to enter Japan as a regulated entity. The purchase will give Binance its first license in East Asia, writes Bloomberg.

- The Japanese subsidiary of Sam Bankman-Fried’s failed crypto empire FTX has put together a draft for clients to withdraw funds, in what would be one of the rare cases of investors getting money back from the collapsed exchange. FTX Japan customer balances would be transferred to a platform called Liquid after a verification process so that users can withdraw their money, according to Bloomberg.

- Creators selling NFTs on OpenSea collectively earned $1.1 billion this year, with 80% of that amount allocated to collections outside the top 10. These earnings do not include sponsorship revenue, engagement incentives or grants, writes Bloomberg.

Threats

- BlockFi Inc. filed for bankruptcy, the latest crypto firm to collapse in the wake of crypto exchange FTX’s rapid downfall. Blockfi said in a statement Monday that it will use the Chapter 11 process to “focus on recovering all obligations owed to BlockFi by its counterparties, including FTX and associated corporate entities,” writes Bloomberg.

- Bankrupt cryptocurrency lender BlockFi has sued two companies with ties to Sam Bankman-Fried’s Alameda Research to recover Robinhood stock used as collateral for loans. BlockFi claims it has secured interest in the collateral, but Alameda has declined to turn over the stock. Their tussle reflects the tangled cryptocurrency connections that have caused several large crypto firms to file for bankruptcy, writes Bloomberg.

- Crypto exchange Kraken is laying off 30% of its workforce, or about 1,100 people, the company said in a blog. The news follows similar moves by many rival exchanges, including Coinbase Global Inc. and Gemini. Many exchanges have seen trading activity fall off in recent months, as falling crypto prices led many traders to stay on the sidelines. The recent collapse of crypto exchange FTX added to market uncertainty, writes Bloomberg.

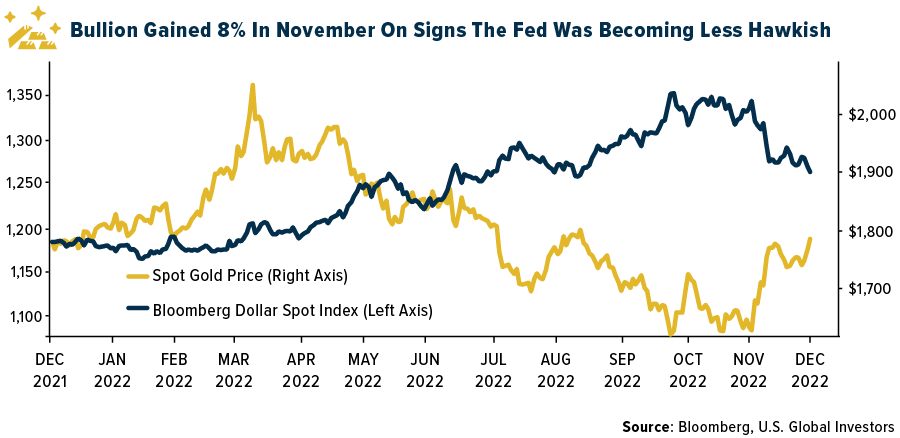

Gold Market

This week gold futures closed at $1,811.50, up $42.70 per ounce, or 2.41%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.71%. The S&P/TSX Venture Index came in up 4.09%. The U.S. Trade-Weighted Dollar fell 1.31%.

Strengths

- The best performing precious metal for the week was silver, up 8.15%. The global silver market is forecast to record a second consecutive deficit in 2022, with a multi-decade supply gap of 194 million ounces forecast, as demand is set to rise to a new high this year. Industrial demand is on course to grow to 539 million ounces, bolstered by developments such as ongoing vehicle electrification, growing adoption of 5G technologies and government commitments to green infrastructure.

- The price of gold advanced after Federal Reserve Chair Jerome Powell signaled the pace of tightening would slow at the next meeting, writes Bloomberg, ahead of economic data that could bear on the central bank’s future rate hikes.

- Endeavour Mining reported Tuesday a 17% increase in measured and indicated resources at its Ity gold mine in Cote d’Ivoire. Endeavour said it remains on track to achieving its goal of discovering 3.5 million to 4.5 million ounces of indicated resources over the 2021-2025 period, with nearly 2.0 million ounces already discovered.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 2.41%. Alamos Gold reported a fatality at their Young Davidson Mine killing an employee. No details were immediately released but the company is working with local authorities.

- The Environmental Protection Agency (EPA) issued a ban on moving mined waste rock into Bristal Bay, citing potential harm to the salmon industry in the region. The Pebble Project is owned by Northern Dynasty Minerals and has been trying to permit the project for several decades. The ban effectively stops the Pebble Project from going forward but the company is not walking away. John Shively, CEO of Pebble Limited Partnership, wrote in a press release that “Congress did not give the EPA broad authority to act as it has in the Pebble case.”

- The Royal Bank of Canada (RBC) expects Osisko to face significantly higher upfront capex and operating costs versus 2021, in line with sector-wide cost inflation. The financials outline a costlier (but likely more realistic) project than anticipated, even excluding the power line. That said, the base case economics of the project remain solid at $1,600 per ounce gold, with first quartile margins at an all-in sustaining cost (AISC) of $800 per ounce.

Opportunities

- The tone of the gold market is getting more positive as Jerome Powell signaled the pace of rate hikes would slow at the Fed’s next meeting. In some ways, the market has taken the lead from the Fed. In November, gold gained 8% with talk of Covid loosening in China, but the dollar lost 5% in conjunction with a rise in gold and some anticipation that the Fed can’t keep raising rates this fast. We had a major blow up with the crypto space, and now Blackstone’s $69 billion real estate fund for wealthy individuals announced it is limiting redemption requests on the fund as total requests to liquidate exceed the threshold withdrawal limits. Blackstone became a massive player snapping up apartments, suburban homes and dorms with low interest rates and their property values have likely fallen with the rise in interest rates. Gold is beginning to get interesting as other investment returns look less certain.

- Alamos Gold reported new drill results from surface and underground at the Island Mine in Ontario. High-grade mineralization at Island West was extended 225 meters west of existing resources. Mineralization also extended down from the large high-grade Inferred Mineral Resource block in the lower part of Island East. At Island Main, high-grade mineralization extends 160 meters below Inferred Mineral Resources. John McCluskey, president and CEO of Alamos, noted the significant exploration potential the Island Gold deposit has demonstrated and continues to deliver impressive results.

- MMC Norilsk Nickel PJSC, which controls 40% of global palladium output, said the global market will face a sharp deficit of the metal after the London Platinum and Palladium Market (LPPM) delisted Russian refineries from delivery lists earlier this year. The LPPM’s “arbitrary decision” has “created a major shortfall of supply of good delivery branded sponge and ingots,” the Russian miner known as Nornickel said in its metals outlook on Wednesday.

Threats

- According to Macquarie, the Australian gold sector has experienced inflationary pressures with costs rising in key areas including labor, energy fuel and explosives. Global shipping cost escalation/delays and other supply chain constraints have also impacted the sector more broadly, which has impacted the ability to execute capital projects. Rising costs have led to a general erosion of margins of large-cap gold miners over the last three years. If rising real rates cause gold to fall, balance-sheet strength may become increasingly vital.

- Newmont’s 2022 targets were reviewed as challenging to achieve given NEM’s December 2021 guidance occurred prior to the Ukraine crisis, Covid case surges in the first quarter, China-related uncertainties, and monetary policy changes that precipitated sizable U.S. dollar appreciation. In addition, details for NEM’s non-managed operations (i.e. Nevada Gold Mines and PV) that represent ~25% of production are not fully available until the first quarter.

- Newmont’s capital spending guidance annually was a discussed $2.5 billion through the cycle, supported by $1.0-$1.2 billion in sustaining capital, $0.8-$1.0 billion in development capital, and $0.4 billion in exploration spending. In the near term, spending is guided to be above this target, given tailings-related investment in sustaining capital and spending at key projects. According to RBC, Newmont targets paying 40-60% of free cash flow out as its dividend, now reviewed to be “through the cycle,” and payouts could be higher, near-term, given upcoming elevated spending.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

Superior Gold

Endeavour Mining

Osisko Gold Royalties

Newmont Corp

Qantas Airways Ltd

Azul SA

LVMH Moet Hennessy Louis Vuitton

Hermes International

Tesla Inc.

Mitsui OSK Lines Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The World Container Index (WCI) is the premium resource for frequent, independent container market data.

The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of consumer confidence levels in the United States conducted by the University of Michigan.

The Baltic Dirty Tanker Index is made up from 12 routes taken from the Baltic International Tanker Routes. Rate assessments are quoted in Worldscale rates.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All