Why Emerging Market Debt?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAfter a challenging 2022, it is time for investors to look forward to opportunities. Emerging Markets (EM) debt stands out as one place where investors can potentially take advantage of an underutilized asset class that offers attractive yields and diversification.

- With a few exceptions, EM sovereigns and corporates have been resilient in the face of rising rates and tighter financial conditions. A more mature policy framework, particularly on monetary policy, has supported this resilience. Since EM central banks have been “ahead of the curve” in terms of hiking, we believe this has set up local debt for a period of strong performance moving forward as tightening cycles peak and inflation prints roll over.

- Select countries and corporates have been under macro and market pressure amid the global volatility, including the commodity shocks of 2022. Idiosyncratic situations, like China property, have also been in focus. This is why, as active managers, issuer differentiation is a key part of the investment approach. The Russia-Ukraine conflict provided a valuable case study in this respect.

- One of the benefits of Emerging Markets Debt (EMD) in the current environment, is that it offers compelling valuations and an attractive long-run income opportunity. Investment consultant studies highlight that there is no clear “winning strategy” for investing in EMD. Payden & Rygel offers consistency and longevity in its EMD approach, while partnering with clients to create customized solutions that maximize their unique investment objectives.

Why Emerging Markets Debt (vs. EM Equity)

It is important to start out with what EMs are not—EMs are not a backwater in terms of economic activity. In 2021, EM GDP accounted for 58% of global GDP (in PPP terms), with EM ex-China equivalent to almost 40% of global GDP. To take this one step further, at the end of 2021, of the twenty largest economies (in 2021 dollars), half are from the Emerging World. This includes China, which is the globe’s second largest economy behind the United States, but it also includes the likes of India, Indonesia, Mexico, and Brazil.

A second misperception is that EMD, as an asset class, is underdeveloped and therefore risky. However, when we break down EMD, we see just how much of the universe is comprised of investment grade issuers. Within the sovereign dollar-pay index (JP Morgan’s EMBI Global), nearly 59% of the index is investment grade. The percentage is higher within EM corporates and EM local at over 65% and 76%, respectively.[1] This is part of the secular case for EMD—the investable universe of countries has matured with time.

Though EM economies continue to grow, there is an under- allocation to the asset class. Indeed, EMD in institutional portfolios is limited—in our experience across institutional clients, we generally see about 4-6% allocated to EMD. This coincides well with JP Morgan’s research which suggests that, across US/European investors, the average EMD allocation is 4-5%. However, we observe that many institutions maintain a smaller (2-3%) EMD allocation, and also that many institutions have no exposure to the asset class. These allocations are modest given that sovereign and corporate dollar-denominated debt in their respective JP Morgan indices totals approximately $2.0 trillion. If one factors in EM local-denominated sovereign debt, that total grows to nearly $6.0 trillion. This gives a sense of the EM investable universe and compares favorably to peer asset classes like US High Yield. The entire EM debt stock, which also includes less accessible securities, has been estimated by JP Morgan to be $27 trillion.[2]

There is a more qualitative consideration that falls beneath the diversification umbrella. When an investor buys an EMD portfolio, there is the possibility of gaining exposure to almost 90 countries (including those in both the corporate and sovereign universe). This is a sizeable increase from the 10 countries that were part of JP Morgan’s investable universe in the early 1990s.[3]This is significant particularly versus the other large EM asset class, equities. In the case of the main EM equity index, only 24 countries are represented. Beyond that, concentration in EM equity is much higher. Within the MSCI EM equity index, the top five countries comprise 75% of the market cap; China and Taiwan alone represent over 40%. In contrast, within the JP Morgan EMBI Global (sovereign dollar-pay index), the top five country exposures are only 41%. Various blends of EM sovereign, corporate, and local currency debt are similarly less concentrated compared to EM equities.

EM debt also offers better return per unit of risk versus EM equities. Over the past 20 years, the main EM equity index has approximately 2.5 times the volatility of the main hard currency EM debt indices (sovereigns or corporates). While EM equities have generated higher absolute returns over this time, when adjusted for the volatility, EM debt returns are about 40% higher than EM equities.

Fundamentals Matter

Monetary Policy, Fiscal Dynamics, and External Accounts

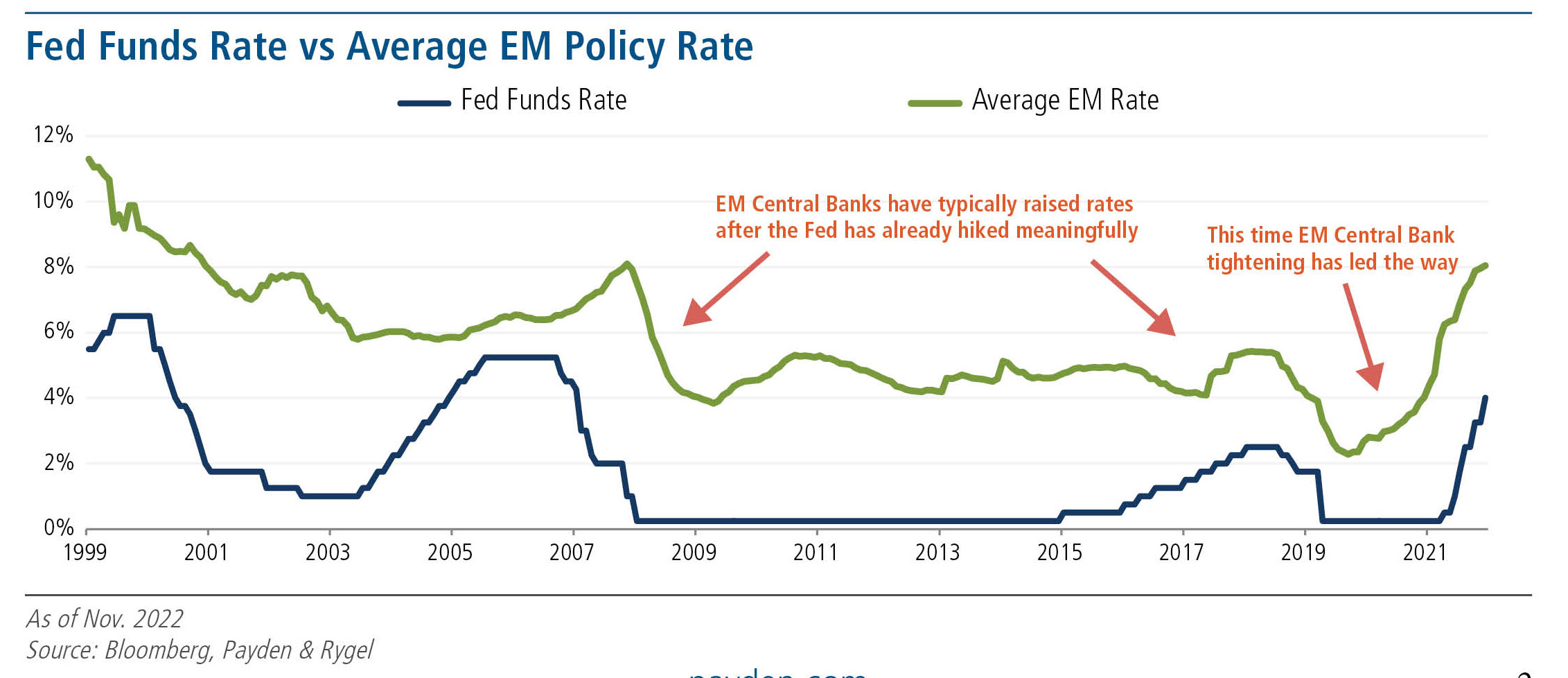

The growth of EM economies over the last four decades has been facilitated by the maturation of EM macro policy. In a nod to this point, in July 2022, the IMF’s Chief Economist noted that a number of EM economies have, “improved their policy frameworks, the way they implement monetary policy…to guarantee the stability of the financial sector.”[4] The recent period of elevated global inflation is no exception to the rule. Although the surge in EM inflation has not been home grown in most cases, the response to it was more front- loaded than it was in the advanced economies. During the recent cycle, one advantage for EMs has been that many of the largest EM central banks started hiking well before the US Federal Reserve (Fed) and other advanced economies. This has not always been the rule; in the previous two Fed hiking cycles, on aggregate, EMs have either been behind the Fed (2005 period) or moved in lock step with the Fed (Fed Funds Rate vs Average EM Policy Rate chart).

Proactive central banking has benefitted EMs. First, economists have been quick to flag financial stability concerns and the impact of the strong dollar on EM. Taking a closer look at 2022 points to some interesting takeaways. Not all EM currencies have weakened significantly against the dollar this year. In fact, while the euro, yen, and the pound have depreciated sharply, EM currency performance has been more balanced, especially when we look at total currency returns (which include carry). On the negative side, Central and Eastern European EM currencies are down over -5.7% year to date, reflecting in large part the moves in the euro and a negative terms of trade shock. However, the non-European EM currencies have posted positive returns of 1.6%. Some of this has been driven by currencies in Latin America such as the Brazilian real, Mexican peso, and Peruvian sol.

This is not to say that EM currencies have been stable in recent years. One of the advantages of the current EM policy framework is that the largest EM central banks have let their exchange rates act as a shock absorber. In other words, central banks do not fight the trend when it comes to currency depreciation, but rather, they look to smooth volatility. Taking a step back, over the last ten years, there has been consistent depreciation in EM real effective exchange rates; this “hands off” approach by central banks has allowed EM external accounts to adjust when imbalances are created.

Fiscal Considerations

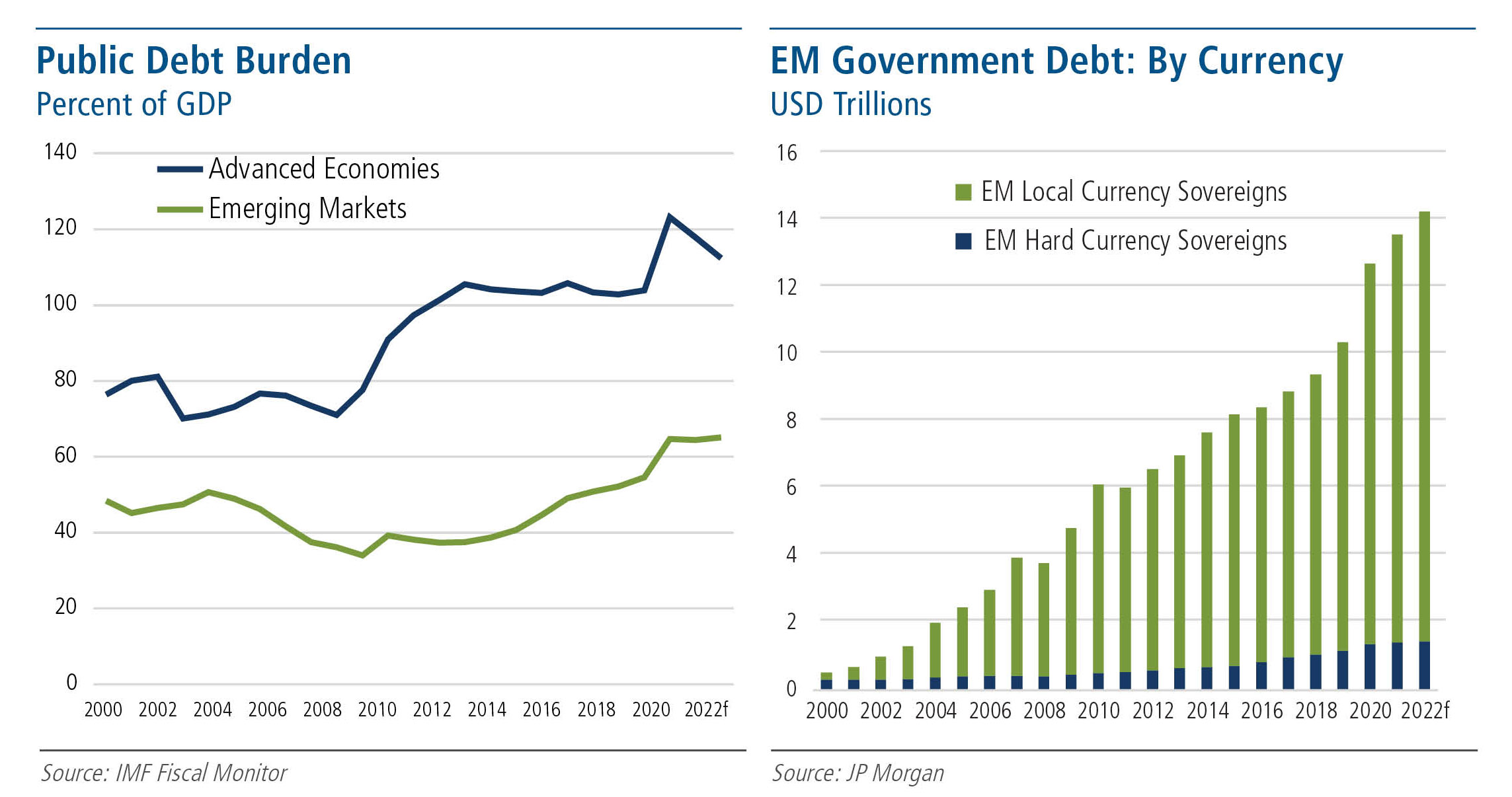

In the post-pandemic era, there has been significant attention paid to the increase in government spending. While advanced economy public debt has increased more than EM public debt (in most cases), there are questions about whether EMs are capable of “handling” higher debt burdens (Public Debt Burden chart). We highlight two points here— the “good news” and the “bad news” associated with the EM fiscal outlook. Starting with the “good news,” while EM indebtedness has risen, most of that has been denominated in each country’s local currency. In other words, the largest EMs have not fallen prey to the “original sin” phenomenon that plagued EMs in the 1990s and early 2000s—namely that EM countries borrowed in US dollars and were subsequently unable to generate sufficient foreign exchange to pay for their debts. JP Morgan puts some numbers to the phenomenon. They project that in 2022, EM (ex-China) debt denominated in local currency will be 76% of the total debt stock (GDP weighted).[5] This number rises to 85% when China is included (see chart above).

The “bad news" is that there are a few smaller economies that have entered distressed territory this year amidst a backdrop of tighter global financial conditions. These are countries that borrowed too much in foreign currency relative to the size of their economies. Of the ones that have investable debt (not all do), the resolution of the cases of Sri Lanka, and likely, Ghana will be watchpoints for the asset class moving forward. An important point to keep in mind, however, is the size of these economies relative to the size of the universe. For example, the GDP of both Ghana and Sri Lanka were each less than $100 billion in 2021. For context, total EM GDP was $44 trillion in current dollars in 2021 ($26.5 trillion ex China). This is all to say that while there are cases of sovereign distress/restructuring within EM, they are not systemic.

The Case for Differentiation

In a world of about 90 investable EM countries, there is space to differentiate among the opportunity set regardless of the global macroeconomic backdrop. EM aggregates hide plenty of variation and, in the current context, it is worth understanding the relative strength of EM sovereigns. An example of this differentiation is instructive. When the Russia- Ukraine conflict initially erupted, one of our first exercises was to determine which countries would be most vulnerable to this shock. Two factors stood out:

- a) proximity—countries near the conflict zone would perform poorly even if not directly involved; and b) the commodity supply shock. In so far as the conflict created a terms of trade shock, countries that benefited from selling commodities would be well positioned, where those that were large importers would suffer. The implications for the EM world were nuanced. For example, Latin America, on a regional level was a “winner,” with many of the economies in South America being large commodity exporters (oil and agriculture, in particular). Another point that stood out to us is that many of the largest commodity importers were the smaller, lower-rated economies.

Why Now? Why Active?

After an eventful year, investors are considering the outlook for 2023. The question that often arises is how EMs will fare in the context of slowing advanced economies. Historically, slowing US growth has been seen as negative for the EM complex. That narrative, however, has been challenged in recent years. Statistically, JP Morgan has done work that concludes that EM sensitivity to advanced economy growth has declined meaningfully in the last several years. In its place, China’s growth dynamics have become more linked to EM growth outcomes.[6] EM growth has been fairly resilient even amid the China headwinds posed in 2022, and turning to 2023, China growth could be a modest tailwind as the reopening from ‘COVID-zero’ gains credibility, and the property sector begins to recover. This may also be positive for oil and other commodities, where we see a rebound in Chinese demand after a subdued period since 2020. Oil in particular may be supported by strained supply factors, that could outweigh the potential for modestly lower demand in a global growth slowdown.

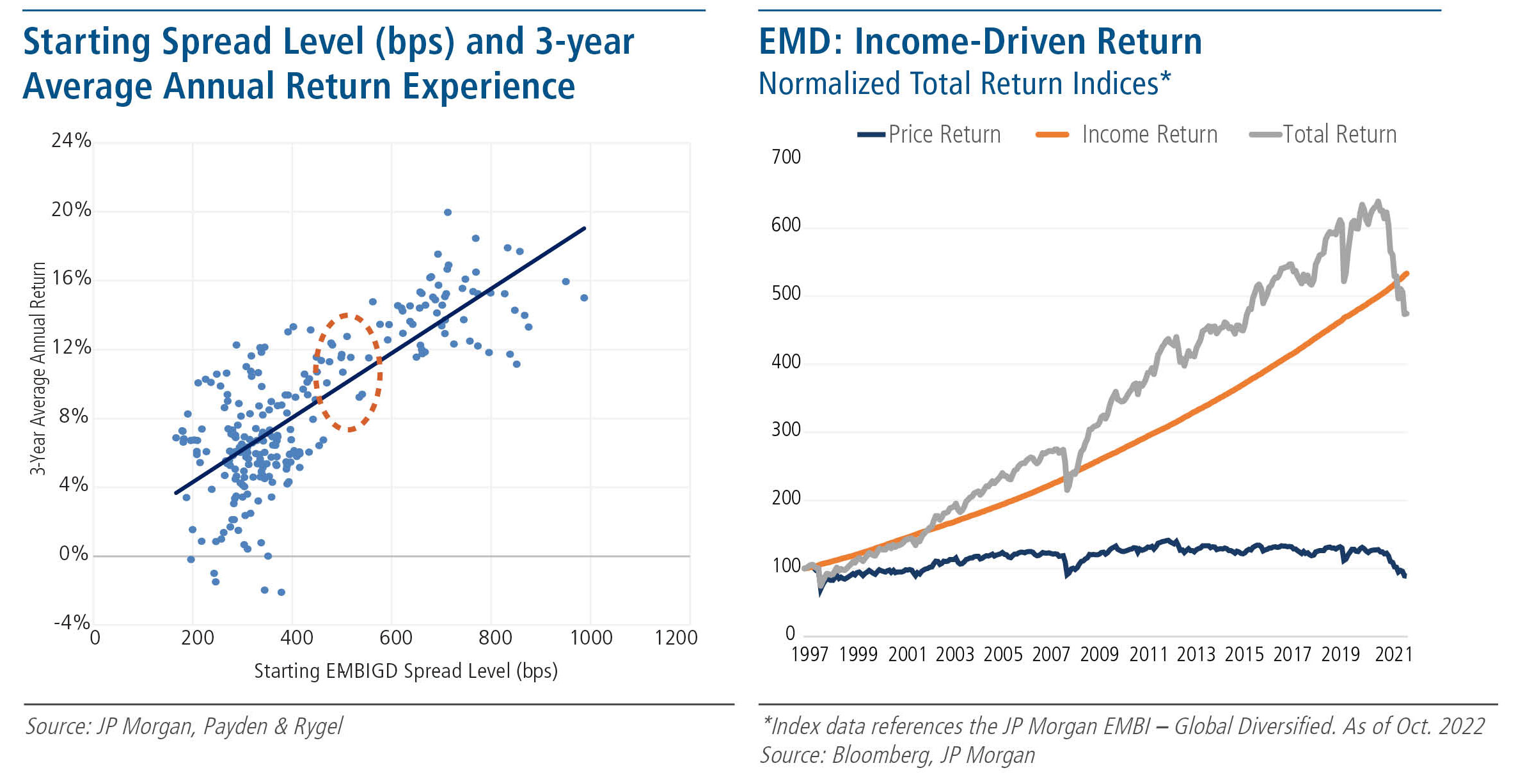

Timing the entry into EMD in the context of market volatility presents an opportunity and a challenge. While it is not possible to time the peak of US rates and/or EM spreads, there is a historical argument to be made in favor of the asset class broadly. In particular, when EM sovereign spreads reach over 500 basis points (bps) over Treasuries, the median three-year average annualized return has been 8.9% (Starting Spread Level (bps) and 3-year Average Annual Return Experience chart). Putting timing aside, there is also a more structural argument to be made for EMD. At an asset class level, using the dollar-pay indices for expositional purposes, the long-run return has been a function of the income. In other words, investors who have been patient in EMD, have been rewarded.

As EMD is a spread product, it is also worth considering how the sector fairs in a US recession. Here, it is worth noting that EM spread widening has already occurred in response to tighter US monetary policy. Since the end of 2021, EMBI Global Diversified spreads have widened by 30% (111 bps from the starting spread).[7] In order to gauge what a US recession might look like, we can look to 2001. During this period, EMBI Global Diversified spreads widened by about 23% (158 bps) from the beginning of the US recession until the official end in November 2001. It is worth mentioning that for this period, annualized returns were 3.3%.

It is worth considering other US economic outcomes. In an extreme US recession (Global Financial Crisis, GFC), spread widening was much more acute from trough to peak (240%, or 640 bps). That said, such widening is not our base case, for two reasons. First, EM spreads going into the GFC were much lower (265 bps), than they are today (465 bps). Second, Payden’s economics team does not see an acute US recession, given the healthy position of the US private sector. The other end of the spectrum would be a Fed hiking cycle that does not result in an immediate recession (2018/early 2019). Here, spreads widened 48% (137 bps) trough to peak. While spreads have partially retraced in late 2022, from end- 2021 to the peak in early July 2022, spreads had widened by over 60% (225 bps).

In this connection, it is worth considering the US Treasury market and the adjustment that we have already seen in US rates. While it is possible that spreads may be more volatile around a US recession, we see the Treasury market as a likely tailwind. In the US, five-year real rates have moved from -1.5% at the end of 2021 to +1.4% currently. After an almost 300 bps move in real Treasury rates, the house view is that much of the Fed tightening is now priced in. This is in a context in which EM USD sovereign and corporate yields are over 8.5% and 7.5%, respectively.

Beyond these factors, market technicals have turned from a headwind to at least more balanced, with the possibility of becoming a tailwind. Prior to the October-November rally, EMD managers were holding historically elevated cash positions, and sentiment had become almost universally bearish. Outflows from EMD had been large and persistent for eight consecutive months. Just as technicals exacerbated the sell-off through most of 2022, they may now be helpful in a recovery.

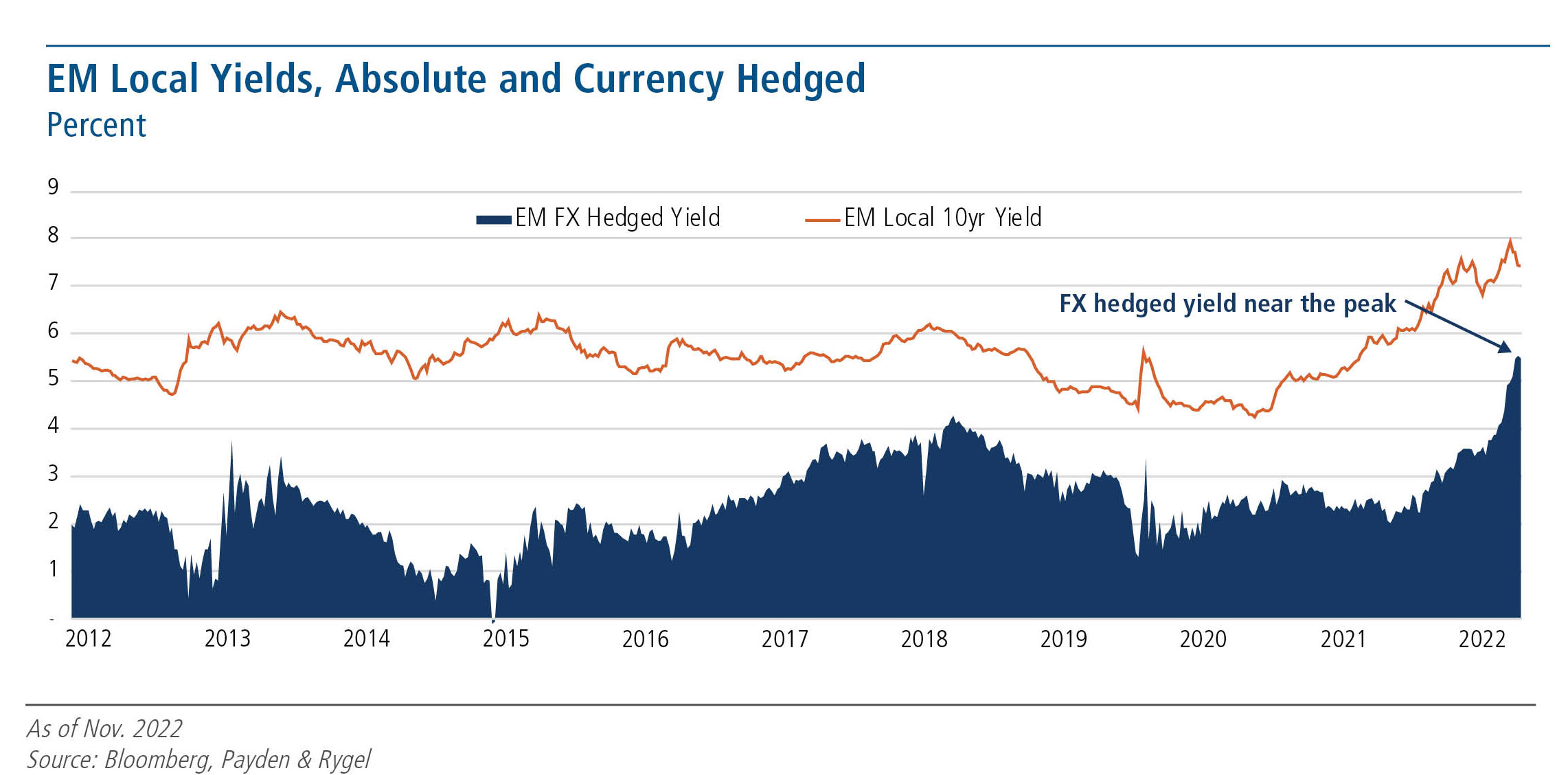

From an EM local market perspective, the opportunities looking ahead are bright. Inflation momentum appears to be decelerating, central banks have hiked aggressively, and EM currencies have exhibited resilience. Valuations in the US dollar are stretched, and the Fed’s aggressive tightening stance is likely to let up at some point in 2023. With this in mind, investors can earn attractive carry in local markets, with a distinct potential for yield compression as central banks turn to easier policy, particularly should downward growth pressures become more pronounced. While the currency component of local markets is subject to volatility, solid income can be had in many local markets even if currency risks are hedged (EM Local Yields, Absolute and Currency Hedged chart).

If the case for returns is based on income, a question that follows is why investors should prefer active management over passive? While more efficient markets, like US equities, may make a compelling case for passive investing, the less efficient world of EM debt argues for more agile and liquidity-conscious management. Replicating EMD indices poses challenges, and investors’ decisions to move in and out of passive EMD funds at inopportune times can exacerbate downside, especially in drawdown periods. One example was during peak concerns around the COVID-19 pandemic, where at one point in March 2020 the key passive EMD ETF (iShares JP Morgan USD Emerging Markets Bond ETF) was underperforming its benchmark by more than 600 basis points. From a longer-term perspective, this ETF has underperformed its benchmark by 67 basis points per annum since inception (December 2007), meaning that even when adjusting for its stated expense ratio of 39 basis points, it has underperformed.

At Payden, we continue to be nimble with credit and currency selection, as the fundamental impact of the global environment varies considerably by issuer. Overall, however, we see risks as better priced and better understood, and we expect key headwinds like higher real rates and tighter financial conditions to ease as we move through 2023.

In the current landscape, there are many EMD investment managers to choose from, each with distinctive investment processes and features. Interestingly, a recent consultant study of EMD managers found that: “... on testing some of the core ‘differentiators’ or styles highlighted by managers we find a distinct lack of statistically significant evidence to support the idea that a certain approach to EMD consistently outperforms over different time periods.”[8] In light of the idea that there is not “one way” to approach EMD investing, Payden's philosophy is to work hand-in-hand with clients, using a full toolkit approach to meet their stated needs. We emphasize thorough risk management to ensure proper diversification. Our core principles apply whether EMD mandates are single sector or blended, highly constrained or fully discretionary. We incorporate Environmental, Social, and Governance (ESG) considerations into the investment process, where appropriate, and manage customized portfolios for those clients who want to emphasize particular ESG goals. In partnership with our clients, Payden has built a comprehensive track record across sovereign, corporate, local currency, and blended currency EMD, backed up by almost twenty-five years of competitive performance.

This material is intended solely for institutional investors and is not intended for retail investors or general distribution. This material may not be reproduced or distributed without Payden & Rygel’s written permission. This presentation is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Sources for the material contained herein are deemed reliable but cannot be guaranteed. The statements and opinions herein are current as of the date of this document and are subject to change without notice. Past performance is no guarantee of future results.

[1] Corporates refer to the JP Morgan CEMBI Broad and Local markets refer to the GBI-EM Broad Diversified.

[2] Jonny Goulden. EM Local Markets Guide 13th edition. JP Morgan, Sept. 2022.

[3] Oganes, L., et al. EM as an Asset Class in the Post-pandemic World. JP Morgan, Sept. 2020

[4] Gourinchas, Pierre Olivier. “WEO Update July 2022 Press Briefing Transcript.” IMF, 26 July 2022, https://www.imf.org/en/News/Articles/2022/07/27/tr072622-weo-uptate-july-22-press-briefing-transcript.

[5] Goulden, J., et al. EM's Debt Vulnerabilities in a World of Higher Rates. JP Morgan, Nov. 2022

[6] Aziz, J.,et al. EM Outlook: The Resilient and the Vulnerable. JP Morgan, Nov. 2022

[7] Data as of Nov. 28th 2022. We use the EMBI Global Diversified Index here as this is the benchmark for most of our accounts.

[8] Cooney, Nick. “Building a Ship to Withstand the Storms.” LCP Vista Autumn 2022, LCP, 2022, https://lcpuk.foleon.com/vista/lcp-vista-autumn-2022/ building-a-ship-to-withstand-the-storms.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits