The 2022 bear market has marked the end of the super-growth cycle.

The U.S. Superbubble, as Jeremy Grantham has termed it, featured the most dangerous mix of factors in modern times at the end of last year: all three major asset classes – housing, stocks, and bonds – were critically historically overvalued. And all have retracted in 2022. Perhaps the most pertinent question we sought to answer for our clients at GMO’s Fall Conference was: what actions should investors take during the deflating superbubble?

Explore our content below and Contact Us or your GMO representative for more information. Intended for accredited investors.

Featured Session:

VALUE’S ATTRACTIVENESS: HOW HAS IT EVOLVED AND HOW MUCH IS LEFT?

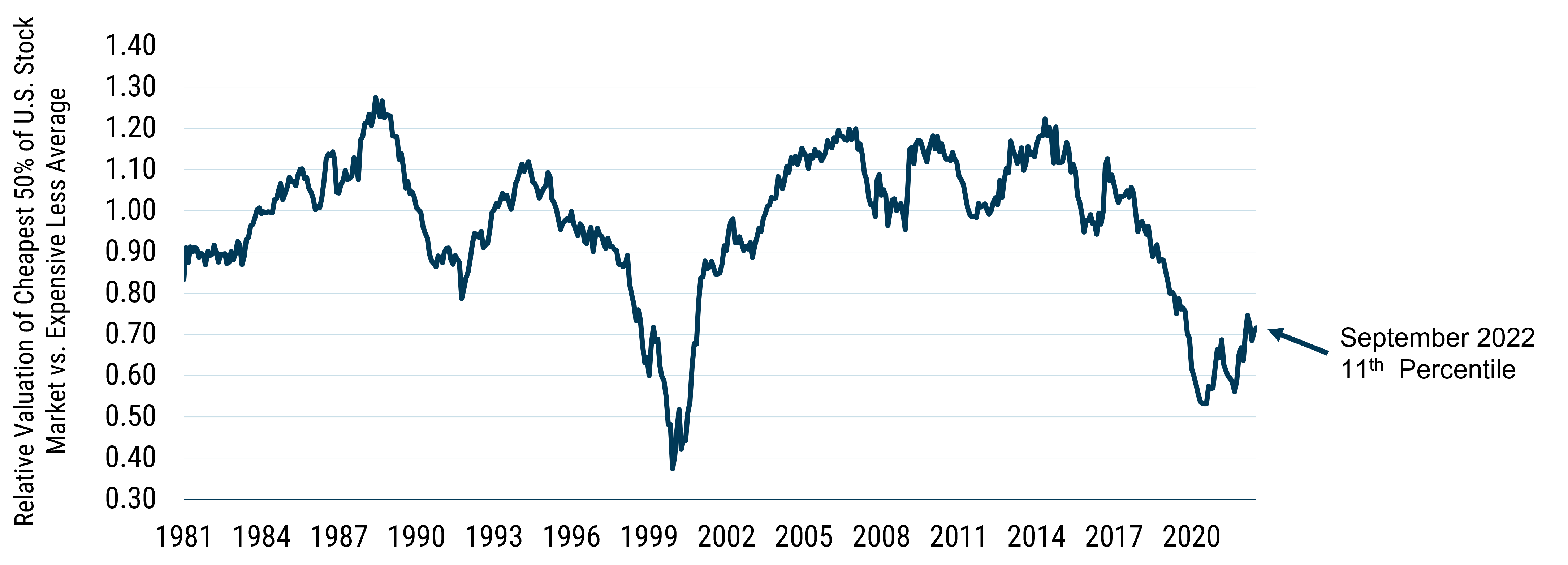

Two years ago at GMO’s 2020 Fall Conference, we first highlighted the extraordinary valuation spread between cheap Value and expensive Growth stocks and launched GMO’s Equity Dislocation Strategy to take advantage of this historic opportunity.

At this year’s Fall Conference, Equity Dislocation Portfolio Manager Ben Inker and Carl O’Rourke, a Systematic Equity team quantitative researcher, provided an update on the ongoing attractiveness of Value relative to Growth. Even after Value’s recent significant outperformance, it is nowhere near back to its average relative valuation compared to Growth, which means the opportunity remains quite strong. And even if Value/Growth spreads do not continue to come back to historical averages, the act of rebalancing provides an incredible opportunity at today’s valuations.

Ben and Carl discussed the evolution of Equity Dislocation, which is long the cheapest Value stocks and short the most expensive Growth stocks and still our highest conviction Asset Allocation trade.

WHERE ARE WE ON RELATIVE VALUATIONS?

Valuation ratios have recovered, but they are nowhere near back to averages.

As of 9/30/22 | Source: GMO

Composite Valuation Measure is composed of price/sales, prices/gross profit, price/book, and price/economic book.

GOODBYE GOLDILOCKS: THE GLOBAL ECONOMY ENTERS DIFFICULT TIMES

Jeremy Grantham sat down for a conversation with Andy Golden, President of PRINCO. The two investment experts shared a discussion ranging from the ongoing U.S. superbubble and the prospect of recession to climate change progress and continued risks and the long-term corrosive effects of inequality.

QUALITY INVESTING IN INTERESTING TIMES

There’s been no shortage of topics to keep things interesting for investors today – a looming recession, inflation, rising rates, geopolitical risks, and Covid (which is still a disrupting force, three years in). Tom Hancock, Lead Portfolio Manager of GMO Quality and Head of the Focused Equity team, and Kim Mayer, Quality Portfolio Strategist, discussed how each of these key issues impacted Quality in 2022 and the markets in general. They also explained what separated successful Quality strategies from the rest in this year’s bear market and why we believe Quality offers strong downside protection.

ALLOCATING AMIDST DISCOMFORT

As equity markets have declined over the course of 2022, GMO has seen interesting and attractive opportunities arise. John Thorndike, Co-Head of Asset Allocation, shared his thoughts on where to allocate capital in the current market environment. He sees improved valuations around the globe, particularly in certain equity markets, such as Value in Europe, EM, and Japan, as well as in Corporate, EM, and Structured credit.

© GMO

Read more commentaries by GMO