2022 was one for the record books, with historic sky high inflation and aggressively hawkish central banks around the world creating significant headwinds to both equity and fixed income portfolios. As we head into 2023, we believe investors will face a new set of challenges, driven by some of the same macroeconomic concerns. In our 2023 outlook, we outline three key themes for the new year and highlight several implementation solutions advisors can use to navigate potential challenges and grow client portfolios in the new year.

1. Rent is coming due

2. Lower no longer

3. Earnings recession and range-bound valuations

THEME 1:

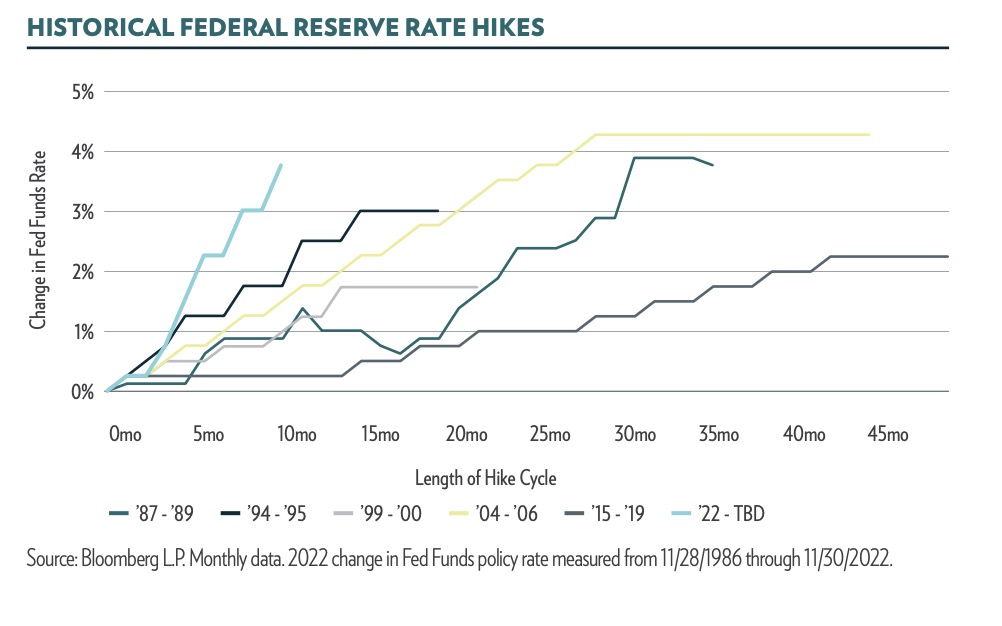

RENT IS COMING DUE The Federal Reserve increased interest rates at the most aggressive pace since 1970, but up until now, the US economy has been very resilient. Unemployment has remained extremely low, consumer spending has remained intact, and the Purchasing Managers Index, while well off the peak, remains near 50 (levels above 50 are viewed as expansionary).

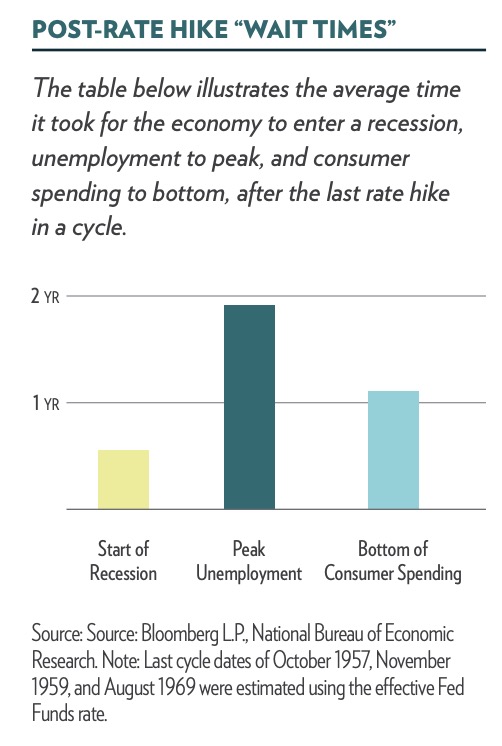

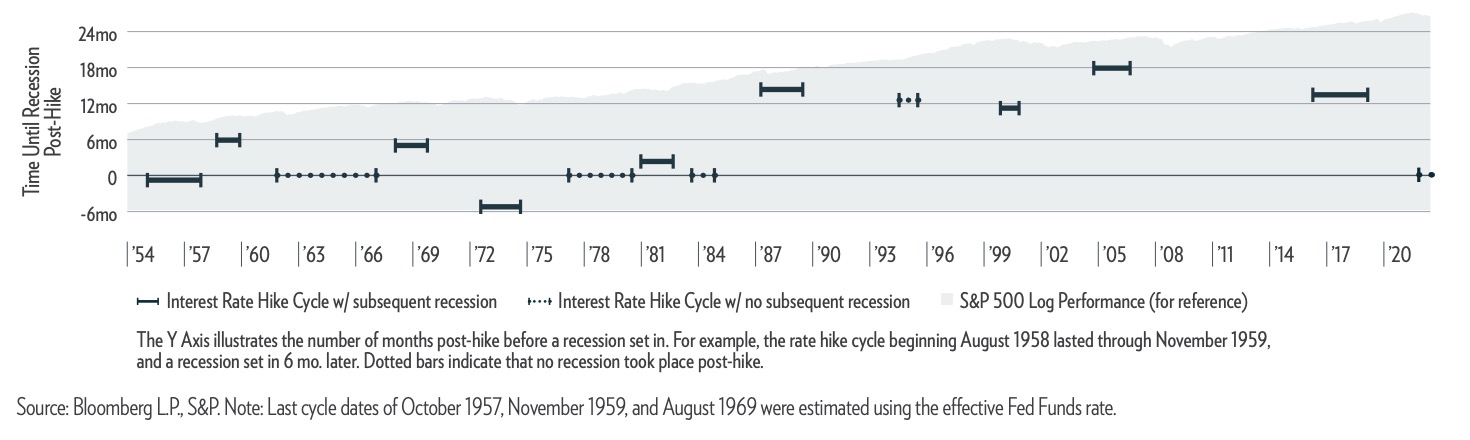

While this highlights the strength of the economy entering the rate hike cycle, the reality is, monetary policy does not immediately impact the economy. The bar chart to the left highlights this dynamic, examining the amount of time unemployment and consumer spending have taken to drop and bottom historically after a rate hike cycle ends. On average, unemployment started to rise approximately 2.5 years after the first Fed hike, and peaked around two years after the last hike. Additionally, on average, consumer spending bottomed approximately one year after the end of the rate hike cycle. This time around, the damage could be dealt quicker given how rapidly the Fed has increased rates, although the full impact has yet to be determined. We expect growth to slow substantially throughout 2023 and see the elevated probability of a recession near the end of the year. Historically, as shown in the bar chart to the left, when recessions occurred, they began an average of 6.8 months after the last Fed rate hike. The strong labor market and strong consumer could act as a double-edged sword; threatening to keep inflation higher for longer, and also dampening the economic blow from rate hikes and keeping investor hopes of a soft landing alive.

THEME 2:

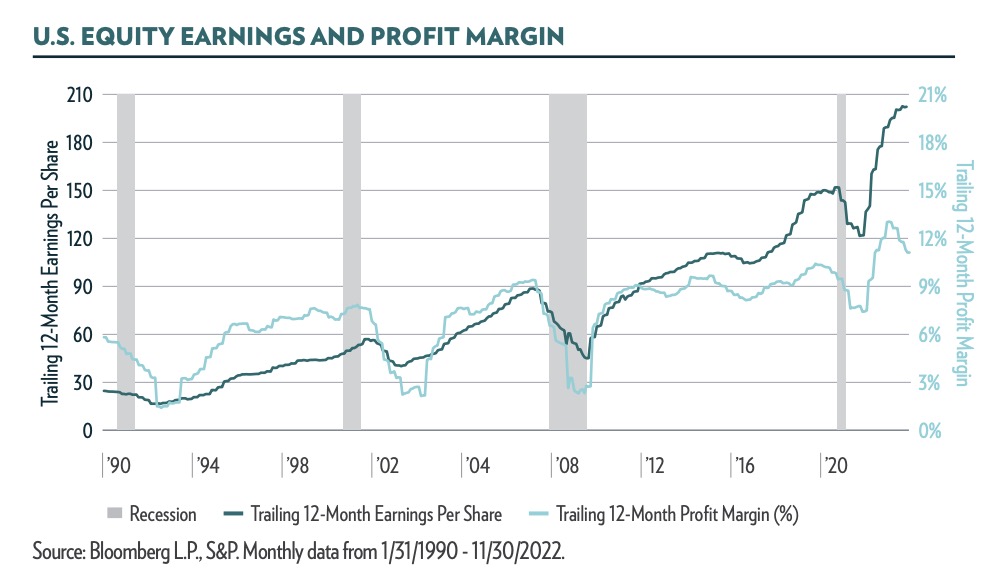

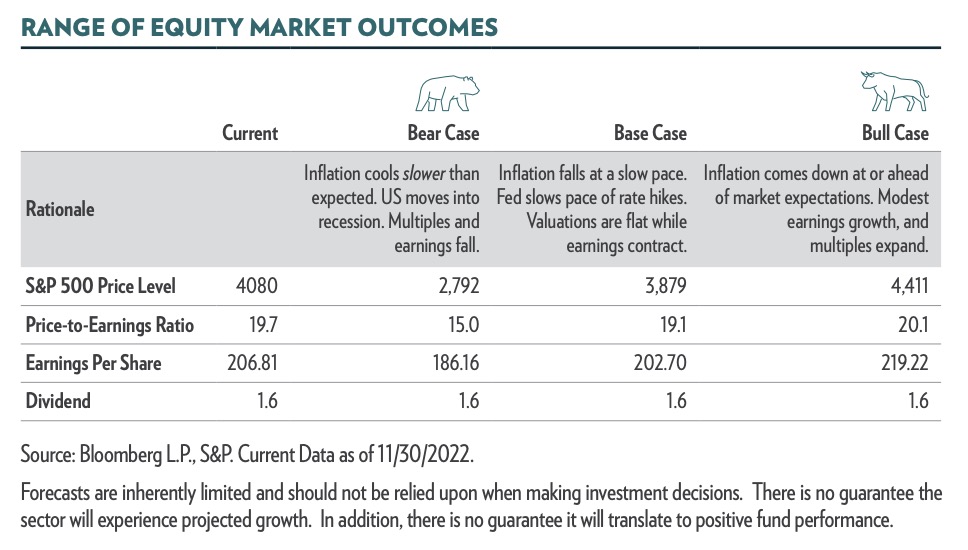

EARNINGS RECESSION & RANGE-BOUND VALUATIONS While macro headwinds were the key risk to portfolios in 2022, the headwinds to earnings growth are likely to dominate in 2023 (e.g., higher borrowing costs, driven by the spike in bond yields, and weaker consumer demand, driven by recent Fed action). We believe current consensus estimates calling for +5% earnings growth on the S&P 500 Index in 2023 are overly optimistic and instead expect an earnings recession as economic growth slows.

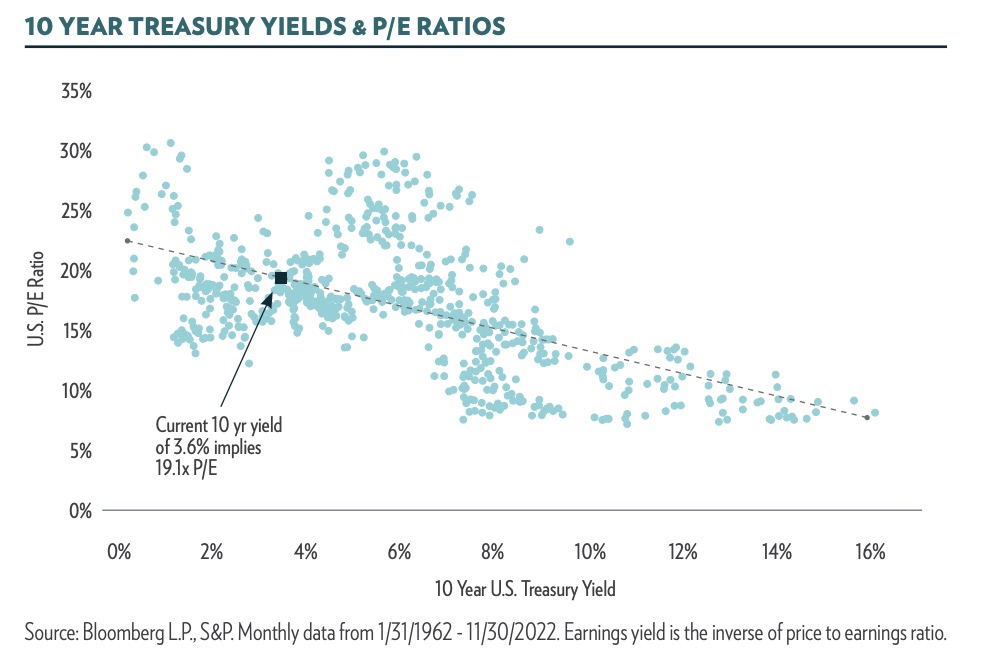

Valuations were the driving factor of the sell-off in 2022. We believe current levels are fair to slightly elevated given interest rates, but will have significantly further to fall should the US tip into a recession. Looking at the regression between interest rates and valuations, current interest rates imply a price to earnings ratio of 19x, very close to the 19.7x the S&P 500 Index is trading at today. It is also important to note that in the back half of 11 of the last 13 Fed hike cycles, valuations have fallen an average of 14%. As such, we do not anticipate equity returns receiving a boost from multiple expansion, but instead expect valuations to be range bound with the potential for a meaningful contraction in the event of a recession.

Overall, without a boost in valuations or earnings, US equity investors may need to tamper their total return expectations for 2023 and also understand the potential downside risks that may be lingering. Current market pricing leaves little room for disappointing news on the economic front.

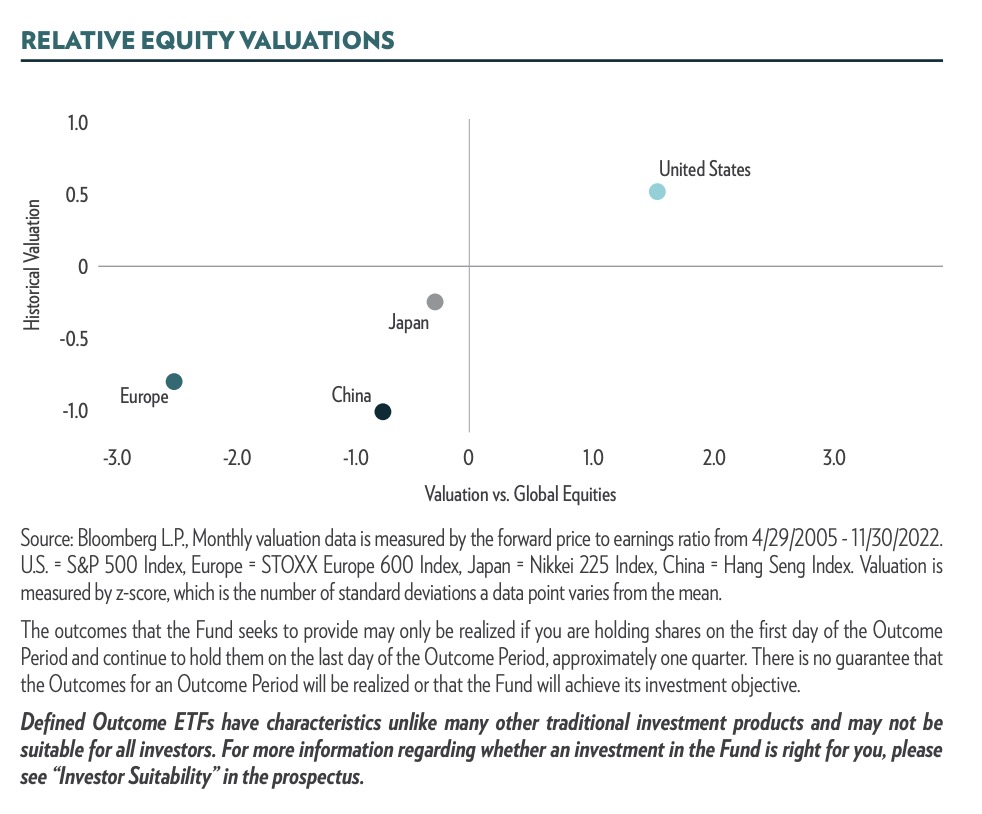

Investors that are looking for value may be well suited to look outside of the US. The Eurozone, UK, and China are all trading at a steep discount relative to the US and significantly below the typical spread as shown in the chart below. Although valuations outside the US are more attractive, they come with a unique set of risks.

THEME 3:

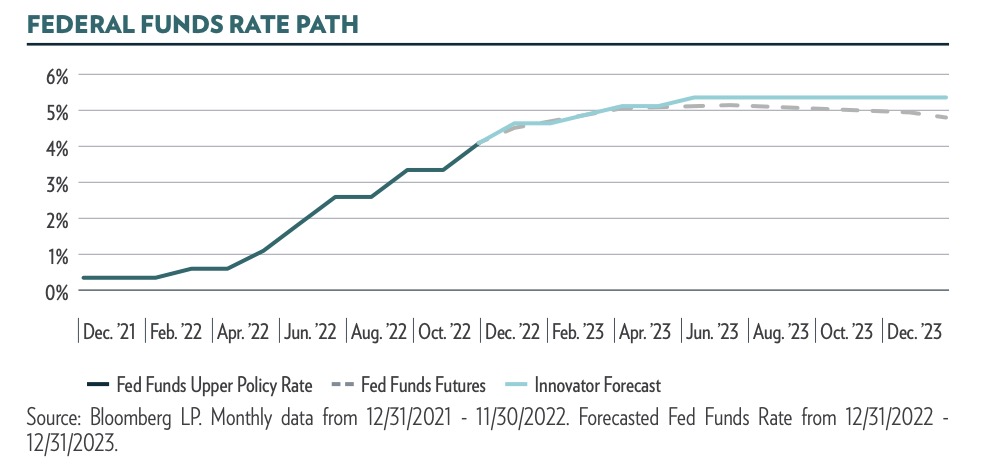

LOWER NO LONGER We believe the tightening cycle is coming to an end, and expect the pace of hikes to slow in the new year, with several smaller rate hikes coming through the end of June. At this time, we anticipate the Fed to pause, but not pivot, contrary to current market expectations. Inflation may have peaked, but it will likely take time to drop to the Fed’s 2% target. Until then, the Fed needs to keep financial conditions tight to keep growth in check, and any cuts or hints at rate cuts could work in opposition, potentially prolonging the issue.

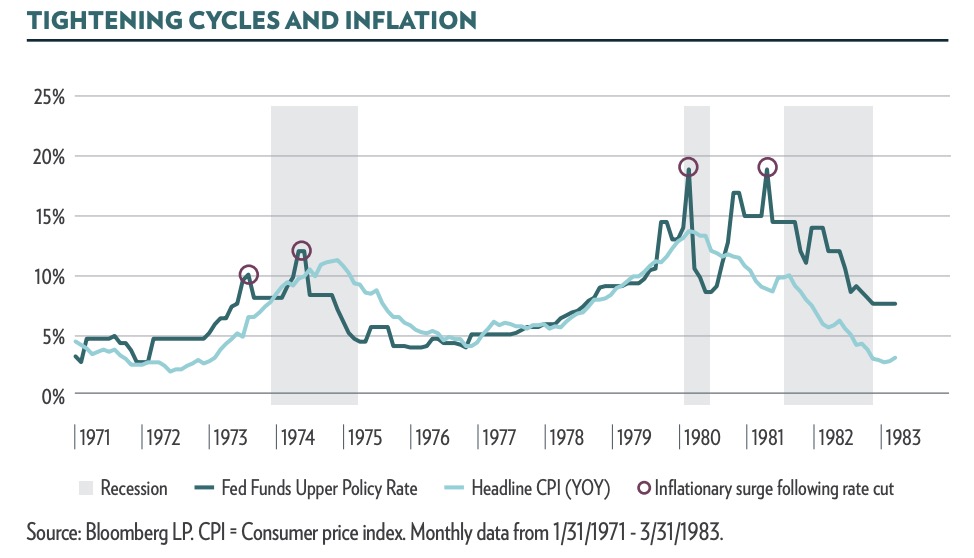

Even in the event of a mild recession, the transition to interest rate cuts could be slower than some anticipate, for fear a resurgence in inflation. As we saw in the 1970’s, inflation can be stubborn, and shifting to rate cuts too soon could end up extending the issue.

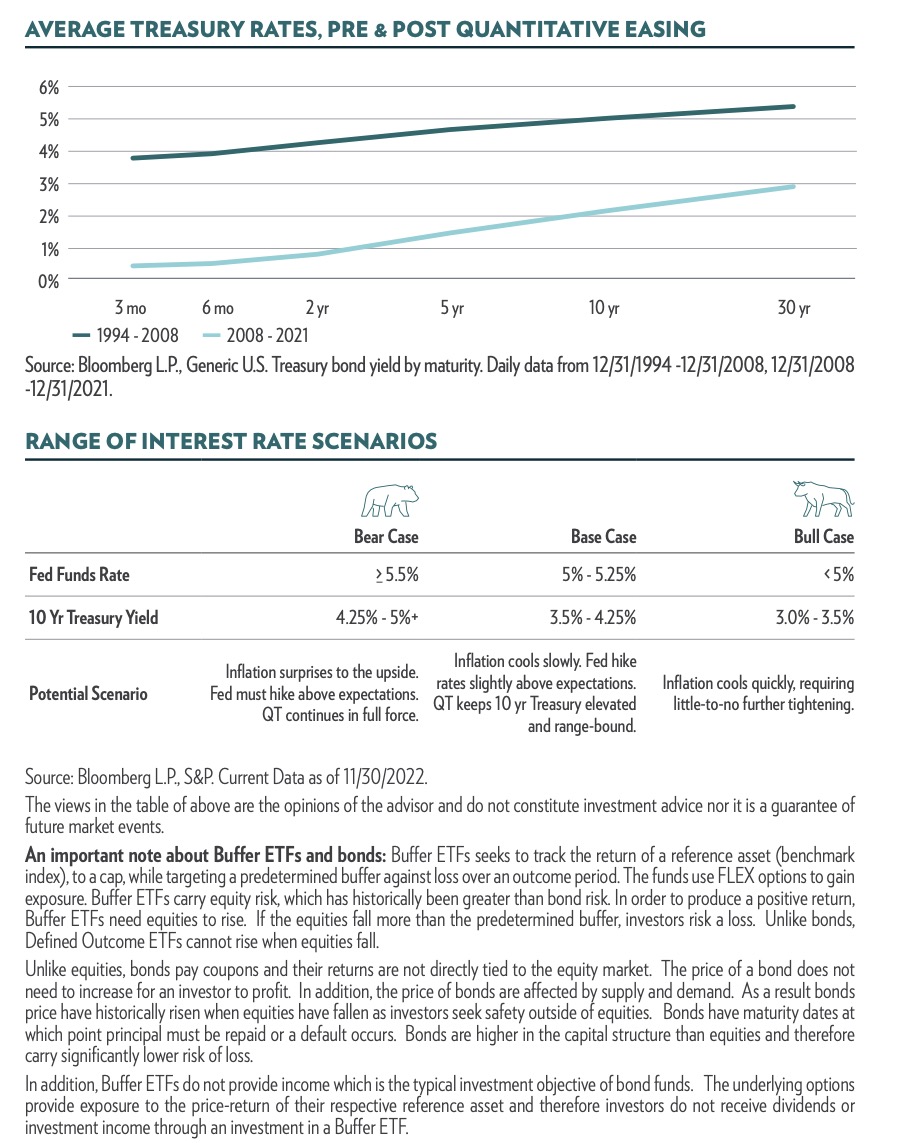

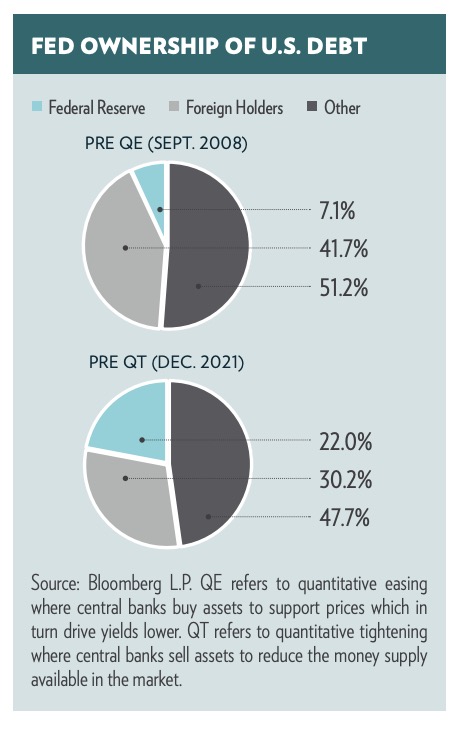

The strong labor market and accelerating wage growth both pose the threat that more rate hikes could be needed to tame inflation, pushing rates across the curve higher. Rates are also likely to face pressure from quantitative tightening (QT). In the last 14 years since quantitative easing (QE) began, the Fed has become the largest buyer of treasuries, artificially suppressing bond yields and bond volatility. To put the Fed’s treasury buying in perspective, in September of 2008, pre-QE, the Fed owned 7% of the $6t treasury market. At the end of 2021, prior to the start of QT, that jumped to 22% of the $25t treasury market. With QT ramping up, supply and demand dynamics are shifting with bonds once again requiring investor demand. Should the Fed allow the $60B of max runoff (ex mortgagebacked securities) to occur each month, that would represent about 9% of the entire treasury market by the end of 2025. The question is what yield will investors require to step in and fill the demand gap? The chart below displays the average yield by maturity in the 14 years pre-QE and post-QE. It highlights how different interest rates were when treasuries required a natural bid, irrespective of the Fed. All-in-all, we expect rates to remain rangebound, with elevated risks to the downside if inflation persists.

IMPORTANT DEFINITIONS AND DISCLOSURES

The S&P 500 Index is a broad measure of U.S. large cap stocks. The STOXX Europe 600 Index is a broad measure of the European Stock Market, representing large, mid and small cap companies across 17 European countries. The Nikkei 225 Index is a price-weighted equity index representative of blue-chip stocks across the Prime Market in Japan. The Hang Seng Index is a free-float market capitalization-weighted index of the sixty largest companies that trade on the Hong Kong Exchange. Purchasing Managers Index (PMI) is an index that measures the month-over-month change in economic activity with the manufacturing sector. Max runoff describes the decline of income-producing assets if proceeds from maturing securities are not reinvested. Price-to-earnings ratio is the ratio for valuing a company that measures its current share price relative to its per-share earnings. SFLR Risks: The Fund seeks to provide risk-managed investment exposure to the S&P 500 through its hedging strategy. There is no guarantee that the Fund will be successful in implementing its strategy to provide a hedge against overall market exposure. The fund seeks to achieve its investment objective by purchasing a series of four, one-year Flex Options packages with “laddered” expiration dates that are 3 months apart. The Fund will also systemically sell short-dated call option contracts, which have an expiration date of approximately two weeks, with an objective of generating incremental returns above and beyond the premium outlay of the protective put option contracts. The Fund does not provide principal protection or non-principal protection, and an investor may experience significant losses on its investment. In a market environment where the S&P 500 is generally appreciating, the Fund may underperform the S&P 500 and/or similarly situated funds. The Sub-Adviser will seek to “ladder” the Fund’s option contracts by entering into new purchased put option contracts packages every three-months. After such put option contracts expire, the Fund will enter into new put option contracts with one-year expiration dates that are staggered every three months. As a result of the Fund’s laddered investment approach, on an ongoing basis the Fund will experience investment floors that are expected to be greater or less than the 10% floor provided by an individual Options Portfolio. The Fund is actively managed and seeks to provide capital appreciation through participation in the large-capitalization U.S. equity securities of the S&P 500® Index (the “S&P 500”) while limiting the potential for maximum losses. Because the Fund ladders its option contracts and the Fund’s put option contracts will have different terms (including expiration dates), different tranches of put option contracts may produce different returns, the effect of which may be to reduce the Fund’s sought-after protection. Therefore, at any given moment the Fund may not receive the benefit of the sought-after protection on losses that could be available from Options Portfolio with a single expiration date. IGTR Risks: Non-U.S. securities and Emerging Markets are subject to higher volatility than securities of domestic issuers due to possible adverse political, social or economic developments, restrictions on foreign investment or exchange of securities, lack of liquidity, currency exchange rates, excessive taxation, government seizure of assets, different legal or accounting standards, and less government supervision and regulation of securities exchanges in foreign countries. Depositary Receipts Risk: The Fund invests in depositary receipts which are currently expected to be comprised of American Depositary Receipts (ADRs) and Global Depositary Receipts (GDRs). Depositary receipts, such as ADRs or GDRs, may be subject to certain of the risks associated with direct investments in the securities of foreign companies, such as currency, political, economic and market risks, because their values depend on the performance of the non-dollar denominated underlying foreign securities. The Fund expects to declare and distribute all of its net investment income and its net realized capital gains, if any, at least annually. The Fund may distribute such income dividends and capital gains more frequently, if necessary, in order to reduce or eliminate federal excise or income taxes on the Fund. The amount of any distribution will vary, and there is no guarantee the Fund will pay either an income dividend or a capital gains distribution. A momentum style of investing emphasizes investing in securities that have had stronger recent performance compared to other securities, on the basis that these securities will continue to increase in value. Securities that previously exhibited relatively high momentum characteristics may not experience positive momentum or may experience more volatility than the market as a whole. High momentum may also be a sign that the securities’ prices have peaked, and therefore the returns of such securities may be less than the returns of other styles of investing. The performance of the Fund and the Market Segment Indices that represent the global equity market segments the Fund invests in may vary for a variety of reasons. Buffer ETF Risks: The funds only seek to provide their investment objective, which is not guaranteed, over the course of an entire outcome period. Investors who purchase shares after or sell shares before the end of an outcome period will experience very different outcomes than the funds seek to provide. The Funds have characteristics unlike many other traditional investment products and may not be suitable for all investors. For more information regarding whether an investment in the Fund is right for you, please see Investor Suitability” in the prospectus. XBJA: Investors purchasing shares after an outcome period has begun may experience very different results than funds’ investment objective. Initial outcome periods are approximately 1-year beginning on the funds’ inception date. Following the initial outcome period, each subsequent outcome period will begin on the first day of the month the fund was incepted. After the conclusion of an outcome period, another will begin. Investors purchasing shares after an outcome period has begun will be exposed to enhanced downside risk. IJAN & EJAN: Non-U.S. securities and Emerging Markets are subject to higher volatility than securities of domestic issuers due to possible adverse political, social or economic developments, restrictions on foreign investment or exchange of securities, lack of liquidity, currency exchange rates, excessive taxation, government seizure of assets, different legal or accounting standards, and less government supervision and regulation of securities exchanges in foreign countries. Investing involves risks. Loss of principal is possible. The Funds face numerous market trading risks, including active markets risk, authorized participation concentration risk, buffered loss risk, cap change risk, capped upside return risk, correlation risk, liquidity risk, management risk, market maker risk, market risk, non-diversification risk, operation risk, options risk, trading issues risk, upside participation risk and valuation risk. For a detail list of fund risks see the prospectus. FLEX Options Risk: The Fund will utilize FLEX Options issued and guaranteed for settlement by the Options Clearing Corporation (OCC). In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses. Additionally, FLEX Options may be less liquid than standard options. In a less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. The values of FLEX Options do not increase or decrease at the same rate as the reference asset and may vary due to factors other than the price of reference asset. Defined Outcome ETF Risks The Funds are designed to provide point-to-point exposure to the price return of a reference asset via a basket of Flex Options. As a result, the ETFs are not expected to move directly in line with the reference asset during the interim period. Additionally, FLEX Options may be less liquid than standard options. In a less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. Fund shareholders are subject to an upside return cap (the Cap) that represents the maximum percentage return an investor can achieve from an investment in the funds’ for the Outcome Period, before fees and expenses. If the Outcome Period has begun and the Fund has increased in value to a level near to the Cap, an investor purchasing at that price has little or no ability to achieve gains but remains vulnerable to downside risks. Additionally, the Cap may rise or fall from one Outcome Period to the next. The Cap, and the Fund’s position relative to it, should be considered before investing in the Fund. The Funds’ website, www.innovatoretfs.com, provides important Fund information as well information relating to the potential outcomes of an investment in a Fund on a daily basis. The Funds only seek to provide shareholders that hold shares for the entire Outcome Period with their respective buffer level against reference asset losses during the Outcome Period. You will bear all reference asset losses exceeding the buffer. Depending upon market conditions at the time of purchase, a shareholder that purchases shares after the Outcome Period has begun may also lose their entire investment. For instance, if the Outcome Period has begun and the Fund has decreased in value beyond the pre-determined buffer, an investor purchasing shares at that price may not benefit from the buffer. Similarly, if the Outcome Period has begun and the Fund has increased in value, an investor purchasing shares at that price may not benefit from the buffer until the Fund’s value has decreased to its value at the commencement of the Outcome Period. The Fund’s investment objectives, risks, charges and expenses should be considered carefully before investing. The prospectus contains this and other important information, and it may be obtained at innovatoretfs.com. Read it carefully before investing. Innovator ETFs are distributed by Foreside Fund Services, LLC. Copyright © 2022 Innovator Capital Management, LLC | 800.208.5212