Ignition! Fusion Energy Comes Closer To Being A Reality, With Exciting Investment Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIf all of your attention was consumed by Sam Bankman-Fried’s arrest this week, you may have missed news of a major, highly disruptive scientific breakthrough, with exciting investment opportunities.

Scientists at the Energy Department’s Lawrence Livermore National Laboratory (LLNL) in California announced the first-ever demonstration of fusion “ignition.” This means that more energy was generated from fusion than was needed to operate the high-powered lasers that triggered the reaction. More than 2 megajoules (MJ) of laser light were directed onto a tiny gold-plated capsule, resulting in the production of a little over 3 MJ of energy, the equivalent of three sticks of dynamite.

This important milestone is the culmination of decades’ worth of research and lots of trial and error, and it makes good on the hope that humanity will one day enjoy 100% clean and plentiful energy.

Unlike conventional nuclear fission, which produces highly radioactive waste and carries the risk of nuclear proliferation, nuclear fusion has no emissions or risk of cataclysmic disaster. That should please activists who support renewable, non-carbon-emitting energy sources such as wind and solar and yet oppose nuclear power.

75th Anniversary Of Another Great American Invention, The Transistor

I think it’s only fitting that this breakthrough occurred not just in the U.S., the most innovative country on earth, but also on the 75th anniversary of the invention of the transistor.

Like fusion energy, the transistor’s importance can’t be overstated. Invented this week in 1947 in New Jersey’s storied Bell Labs—also the birthplace of the photovoltaic cell, fiber optic cable, communications satellite, UNIX operating system and C programming language—the transistor made the 20th century possible. Everything we use and enjoy today, from our iPhones to our Teslas, wouldn’t exist without the seminal American invention.

In 2021, the electric vehicle maker unveiled its proprietary application-specific integrated circuit (ASIC) for artificial intelligence (AI) training. The ASIC chip, believe it or not, boasts an unbelievable 50 billion transistors.

Getting your electricity from a commercial fusion reactor is still years if not decades away, but that hasn’t stopped money from flowing into the sector. This year, private investment is estimated to top $1 billion, following the record $2.6 billion that went into fusion research in 2021, according to BloombergNEF.

At the moment, there aren’t any publicly traded fusion companies. However, Bloomberg has a Global Nuclear Theme Peers index that tracks listed companies with exposure to the industry, estimated by Bloomberg to one day achieve a jaw-dropping $40 trillion valuation. Some of the more recognizable names include Rolls-Royce, Toshiba, Hitachi and General Electric.

For the five-year period, the index of 64 “nuclear” stocks has advanced approximately 100%, compared to the MSCI World Index, up 38% over the same period.

The number of private firms involved in R&D continues to grow, raising the possibility that some will tap public markets in the coming years.

Among the largest is Commonwealth Fusion Systems, or CFS, which spun out of MIT’s Plasma Science and Fusion Center in 2018. The company raised $1.8 billion in December 2021, on top of the $250 million it had raised previously. Its investors include Bill Gates and Google, along with oil companies, venture capital firms and sovereign wealth funds. CFS claims to have the fastest, lowest cost solution to commercial fusion energy and is in the process of building a prototype that is set to demonstrate net energy gain by 2025.

Another major player is TAE Technologies. Located in California, the company has raised a total of $1.2 billion as of December 2022, from investors such as the late Paul Allen, Goldman Sachs, Google and the family office of Charles Schwab. TAE says it is developing a fusion reactor, scheduled to be unveiled in the early 2030s, that will generate electricity from a proton-boron reaction at an incredible temperature of 1 billion degrees.

Other contenders in the field include Washington State-based Helion Energy, Canada’s General Fusion and the United Kingdom’s Tokamak Energy. In February 2022, Tokamak broke a longstanding record by generating 59 MJ of energy, the highest sustained energy pulse ever.

As an investor, I would keep an eye on this space!

Solar Accounted For 45% Of All New Energy Capacity Growth In The U.S.

In the meantime, energy investors with an eye on the future still have renewable energy stocks to consider.

2022 has been a challenging year for the industry, with much of it facing supply constraints. According to Wood Mackenzie, total new solar installations in the U.S. were 18.6 gigawatts (GW), a 23% decrease from 2021.

Even so, solar accounted for 45% of all new electricity-generation capacity added this year through the end of the third quarter. That’s greater than any other energy source. Wind was in second place, representing a quarter of all new energy power, followed by natural gas at 21% and coal at 10%, its best year since 2013.

WoodMac expresses optimism in the next two years. Solar projects that were delayed this year due to supply issues may finally come online in 2023, and by 2024, the real effects of President Biden’s Inflation Reduction Act (IRA) should be felt. The U.K.-based research firm forecasts 21% average annual growth from 2023 through 2027, so now may be an opportune time to start participating.

One of our favorite plays right now is Canadian Solar, up more than 11% for the year. On Thursday of this week, the Ontario-based company announced that it would begin mass-producing high efficiency solar modules in the first quarter of 2023. Canadian Solar shares were up more than 1% for the week, despite experiencing two down days on this week’s news of continued rate hikes into 2023.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.66%. The S&P 500 Stock Index fell 2.09%, while the Nasdaq Composite fell 2.72%. The Russell 2000 small capitalization index lost 1.90% this week.

- The Hang Seng Composite fell 2.24% this week; while Taiwan was down 1.20% and the KOSPI fell 1.21%.

- The 10-year Treasury bond yield fell 9 basis points to 3.488%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was China Southern, up 4.1%. Ryanair Group’s CEO Michael O’Leary has had his contract extended from July 2024 to July 2028. The contract’s new terms will see the final vesting date for share options granted in 2019 extended to 2028 from 2024, subject to new performance targets. The share option scheme is estimated to be worth roughly EUR100 million. Ryanair’s guidance is for profit of EUR1-1.2 billion in fiscal year 2023.

- Dynagas LNG Partners reported an adjusted earnings per share (EPS) of $0.04, although after adding back the realized gain on interest rate derivatives, the EPS was $0.11, (above consensus of $0.08). The quarter was lower than normal, due to the scheduled dry dockings of the Amur River and Ob River, which contributed to roughly $9.4 million in operating expenses. With all six vessels on time charter, adjusting for the dry docking, fleet utilization was 100% for the quarter.

- With some investors anticipating a 2023 earnings per share guide for Delta Air Lines, the guide of $5.00-6.00 came in better than investor expectations. Additionally, reiterating the 2024 EPS guide of $7.00 is ahead of consensus of $6.38. Importantly, Delta is guiding to strong free cash flow of $2.0 billion in 2023 and $4.0 billion in 2024.

Weaknesses

- The worst performing airline stock for the week was Mesa Air, down 20.6%. The International Air Transport Association (IATA) warned that the amount of airline funds for repatriation being blocked by governments has risen by more than 25% in the last six months. Total funds blocked now tally close to $2.0 billion. The IATA calls on governments to remove all barriers to airlines repatriating their revenues from ticket sales and other activities, in line with international agreements and treaty obligations.

- According to Morgan Stanley, Nippon Express released parent sales growth data by business for November, showing an overall year-over-year increase of 0.8%. Its first impression is neutral. The company’s fiscal year 2022 fourth quarter parent sales growth assumption is up 3.4% year-over-year, but the unweighted average for October-November is short of this level, at up 3.0%. In addition to shortfalls in domestic business, air forwarding, which had been driving an overshoot, saw sales turn down 7.9% year-over-year. In addition, Morgan Stanley believes that a steep slowing of the growth rate for air freight rates, as well as a negative trend for handling volumes, forms the background to the year-over-year sales decline for air forwarding.

- JetBlue now expects to be at the lower end of its fourth quarter revenue guidance of up 15-19% versus 2019 driven by: 1) a negative impact from Hurricane Nicole (50 basis points), 2) weaker close-in demand for December (50 basis points), and 3) a greater adverse impact from holiday timing (200 basis points versus 100 basis points prior). The company’s fourth quarter capacity, CASM-ex and fuel are all tracking in line with guidance.

Opportunities

- United Airlines and Boeing announced an order for 100 787 and 100 MAX aircraft, marking the largest 787 order in Boeing’s history. The order brings the 787 backlog to 500-plus units, compared to Boeing’s stated production rate target of 10 per month in 2025/2026. It continues a robust order cycle for narrowbody aircraft and reflects growing demand for widebody aircraft as international travel recovers.

- Energy shipping rates are indeed down 48.5% from the peak in early November, but rates are still up 18 times from the start of 2022 (and were running negative for many weeks in 2022). Taking Europe’s challenges with Russian fossil fuels out of the picture for a moment, the orderbook of new tonnage is still at 30-year lows, inventories are still below five-year averages, and even amid widespread recession fears, consensus forecasts call for oil demand growth over the coming year. As it relates to the stocks, the group is down 5-17% from year-to-date highs.

- In 2023, travel demand in Asia may rebound strongly. With passenger air traffic in October 2022 at only 46% of pre-Covid levels, there is substantial room for demand to recover. The key bottleneck of travelling—namely mobility restrictions—are receding with increasing numbers of unrestricted travel routes in APAC, according to UBS Evidence Lab’s Global Travel Restriction Monitor.

Threats

- Airbus lowered its 2022 delivery target from the 700 previously (565 through November) and lowered the A320-family monthly delivery target from 75 to 65 over 2023-2024, (but remains confident of reaching 75 by 2025). Additionally, a bill to extend the FAA certification deadline (currently December 2022) for the MAX 7/10 using existing flight crew alert systems, has been omitted from the annual defense bill.

- JPMorgan’s second quarter 2023 forecast for FedEx remains $2.65 as the group still sees risk of Express market conditions deteriorating faster than FedEx expected, while most expected cost savings are variable and will take time to implement. Freight should be able to carry most of the load again but the tailwinds from fuel surcharges will be hard to ignore even if FedEx doesn’t disclose them again. The bank sees risk to third quarter 2023 consensus given estimates reflect a contra-seasonal margin trend that seems too aggressive in its view, since cost reductions will be difficult to accomplish during peak season while still providing good service levels.

- Mesa Air Group is postponing the company’s fourth quarter/full-year 2022 release from today to a date in the future. Management filed an 8K indicating it will seek to delay filing its 10K until the second half of the month, but no later than December 29. Cowen views this development as concerning and remains cautious on the shares.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 4.2%. The best performing country in Asia this week was Indonesia, gaining 1.5%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 3.8%. The Hong Kong dollar was the best performing currency in Asia this week, gaining 0.1%.

- Consumer confidence in the Eurozone improved in November, beating expectations, despite concerns over increased costs of living and a slowdown of the economy. The European Commission said Tuesday that its measure of consumer confidence in the region rose to -23.9 in November from a revised reading of -27.5 in October.

Weaknesses

- The worst performing country in Asia this week was Hong Kong, losing 2.2%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 3.4%. The Thailand baht was the worst performing currency in Asia this week, losing 0.5%.

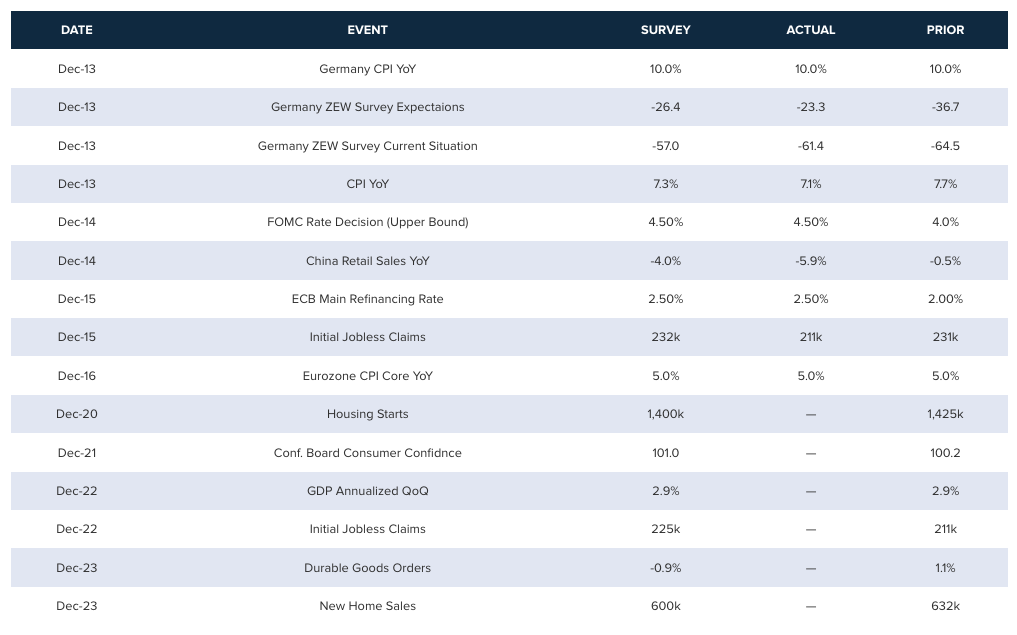

- China’s economic activity was worse-than-expected across the board in November. Retail sales fell 5.9% year-on-year, industrial output growth slowed to 2.2%, and fixed-asset investment growth weakened. The jobless rate climbed to 5.7%. More disruption is seen in the months ahead as Covid cases surge.

Opportunities

- The European Commission approved all of Poland’s plans to spend €76 billion from the bloc’s Cohesion funds. The money will flow to Poland from the EU’s budget for the years 2021-2027 and are separate from the €36bn in grants and loans Poland should receive from the bloc’s pandemic recovery fund, but which are currently frozen. Also, another central emerging Europe country, Hungary, is expected to sign an EU funding agreement within days that will bring it closer to accessing billions in suspended European Union funding. The EU’s 2021-2027 budget includes €34.5 billion for Hungary and additional funds from the coronavirus recovery plan.

- Goldman Sachs predicts that emerging market Asian currencies will continue to rally, following a recent rebound as the Federal Reserve looks to slow its pace of tightening and China continues to push for further removal of Covid restrictions. The Federal Reserve this week hiked its main policy rates by 50 basis points, as expected.

- The South China Morning Post (SCMP) reported that the border between Hong Kong and China is expected to fully reopen next month. Hong Kong Chief Executive John Lee took a more cautious stance publicly, saying it is “highly possible” to reopen the border with mainland China in 2023. China continues to push forward with the removal of additional Covid restrictions despite more people getting sick.

Threats

- Jimmy Lai, a pro-democracy Hong Kong media tycoon, was sentenced to more than five years in prison for fraud over a sub-lease at the former headquarters of his media company. He was a critic of the China Communist Party and has remained in custody for almost two years (and is also facing trial under Hong Kong’s sweeping national security law). Since the security law was imposed by Beijing in 2020, protesters and journalists have been jailed.

- Political tensions in Turkey may rise as Turkey convinced Istanbul’s mayor, the most popular political figure who could challenge Erdogan in next year’s presidential elections, of insulting election officials back in 2019, sentencing him to almost three years in prison. If the verdict is upheld by the higher appeals court, he will be banned from running in presidential elections next year. This event, of course, is highly criticized by the opposition, calling for the resignation of the government. Most people in Turkey are dissatisfied with the current economic situation.

- Chinese President Xi Jinping has met with more than 25 heads of state — including U.S. President Joe Biden — since he was elected for another term as a President. Xi is stepping out into the world to try and strengthen his position in the global arena and challenge the United States.

Energy And Natural Resources

Strengths

- The best performing commodity for the week natural gas, rising 5.67%, on expectations of fridged temperatures moving across the U.S. next week. On Friday, the Department of Energy announced that it plans to purchase 3 million barrels of oil following the release of 180 million barrels to tap down gasoline prices. Global refining supply has been constrained by capacity reductions in the 2019-2022 time period, driven by: 1) unprofitable economics during Covid, 2) physical damage that would be costly to repair, and 3) conversions to renewable diesel. With demand beginning to return toward pre-Covid levels in early 2022, the refined product market tightened up quickly with less capacity to service this demand.

- Spot market prices for lithium continued an upward climb to reach record levels in November, with China lithium carbonate breaching the $80,000 per metric ton

mark for the first time. Similarly, lithium hydroxide prices for Asia seaborne and Europe and U.S. markets surged to a record price of $85,000 per metric ton. - Despite China’s reopening and sudden outbreaks of Covid, base metals did not pare back much of their recent gains. Peru, which is the world’s fourth-largest producer of zinc, may see some production delays getting its concentrates to market due to blocked roads by protestors, so prices could remain well bid.

Weaknesses

- The worst performing commodity for the week was lumber, losing 12.76%, as housing affordability continues to be a headwind to demand. Australia’s parliament passed legislation that caps domestic natural gas and coal prices to effectively shield voters from high international prices. Without intervention, consumers were expected to see retail gas prices rise a further 20% and electricity prices by 35%. The government has so far ignored calls for windfall profit taxes on the energy sector.

- According to Morgan Stanley, the decline in European gas demand is accelerating, even adjusted for weather. Gas consumption within Europe fell 25% in November relative to the average of the same month during 2017-2021. This followed on from October, when demand was down by a similar 26%. Last month, the majority of October’s decline could be attributed to weather. However, this is not the case for November. Even adjusted for weather, the underlying decline is at a large 19%.

- Protestors at Las Bambas, Peru’s No. 3 copper mine, which is owned by China Metals Corp, might force the mine to shut down as it is running out of storage space for concentrates on site with the blocked trucking roads, likely by year-end. Las Bambas supplies roughly 1.4% of world copper production, so any prolonged delay could boost copper prices.

Opportunities

- Investors have been concerned about both copper supply growth and demand weakness moving into 2023 before a structural deficit materializes into the end of the decade. But the Goldman global commodities team believes the combination of weaker-than-expected supply, resilient demand, and record low inventories is likely to result in a 178,000-ton deficit in 2023. In this context, Goldman now upgrades its average 2023 forecast to $9,750 per ton and its 2024 forecast to $12,000 per ton.

- Redwood Materials announced this week that it will invest $3.5 billion to develop a 600-acre site in Charleston, South Carolina, to manufacture battery components with enough capacity to supply more than 1 million electric vehicles per year. This announcement follows on the heels of LG Chem’s plans for a similar plant in Tennessee. Bloomberg reports that billion-dollar battery factories are popping up everywhere along the Battery Belt which stretches from Michigan to Georgia. Domestic lithium mines are in the pipeline in Nevada and the Carolinas.

- General Motors is signaling it will reach further down the value chain to ensure it has the minerals it needs to become a major player in electric vehicles. “We absolutely are convinced we need to have control of our own destiny when it comes to EV critical minerals,” Tanya Skilton, GM’s director of electric vehicle critical materials, said on an industry panel in Washington. “At times we have engaged, for example, with the steel industry, with steel mills in our history, but to go all the way down to mine sites is new and unique for us at this stage.”

Threats

- The performance of the oil sector has rolled lower, but incoming questions have focused on whether it has rolled low enough. Contango is in near dated oil prices and multiple sources of potential support headed into 2023 starting with the expected end of the SPR release. However, it appears that the deep value opportunity across U.S. oil is set up for a much more challenging year in 2022.

- Panama has rocked the copper market as well as investors exposed to the Cobre Panama copper mine owned by First Quantum Minerals Ltd, with its failure to conclude a new royalty agreement. Cobre Panama supplies 1.5% of world copper production and First Quantum has invested $10 billion into building the mine. The most contentious issue is, Panama is asking for a minimum $375 million per year in royalty payments, regardless of whether the copper price drops in the future.

- China is centralizing its iron ore trade by creating a new state-owned company called China Minerals Resources Group (CMRG) that will consolidate the purchasing power of about 20 of the largest steelmakers into a single trading house. It’s the latest move to consolidate buying power where China is almost the biggest buyer of every commodity already. The move should give China more bargaining power and influence over global markets. Bloomberg reports that confidential sources are citing discussions between CMRG and the likes of Rio Tinto Group, Vale SA, and BHP Group have already commenced.

Luxury Goods

Strengths

- As reported by Bloomberg, India’s luxury car market has registered its highest-ever growth this year. Sales increased by 50% in 2022. This market is dominated by Italian carmakers such as Lamborghini and other players such as Bentley, Ferrari, Rolls-Royce, Aston Martin, Maybach, and Porsche. The luxury car market expects to end the year selling 450 cars versus 300 sold last year.

- The consumer price index (CPI) decreased both month-over-month and year-over-year in November, reports Bloomberg. The CPI month-over-month reading was reported at 0.1% versus the previous month of 0.4%. The CPI year-over-year was reported at 7.1% versus 7.7% in the previous month.

- Faraday Future Intelligent, an application software company, was the best performing S&P Global Luxury stock for the week, gaining 21.5%. The company plans to start production of its long-awaited electric vehicle car, the FF 91 Futurist, at its manufacturing facility in California at the end of March 2023.

Weaknesses

- According to Bloomberg, retail sales in both the U.S. and in China, the luxury goods leaders worldwide, decreased in the month of November. For the U.S., retail sales was reported at -0.6% month-over-month versus 1.3% the previous month. In China, retail sales was reported at -5.9% year-over-year versus -0.5% the prior month.

- Based on a Fox Business article, luxury condo prices in San Francisco corrected sharply, primarily due to an increase in crimes and drug use activity that are battering the city. The condo sales price dropped from $1.47 million last December to $1.23 million this year. The prices downtown have fallen by 16.5% since 2021 and in areas outside of downtown, by 7%.

- Tesla was the worst performing S&P Global Luxury stock for the week, losing 15.82%. To top it off, Elon Musk is no longer the wealthiest person, according to Forbes, after a decline in Tesla’s share price. Chief Executive Officer of LVMH, Bernard Arnault, is now the richest person in the world now. Elon Musk sold about 22 million Tesla shares according to a financial filing out Wednesday night.

Opportunities

- Blockchain technology is here to stay and is something most global industries will have to adopt to remain relevant. This is one reason why leading luxury goods companies are using it to help beat counterfeiting. Some industries are working on a blockchain-based passport for tangible products. According to Bloomberg, luxury goods counterfeiting is expected to reach $1.5 trillion by 2025. Using blockchain technology, however, luxury companies aim to offer their clients the security and insurance that they are buying something original. This will also apply if they purchase the product in a secondary market such as luxury e-commerce.

- According to research led by McKinsey and Business of Fashion (BoF), the luxury goods industry has a good outlook for next year, even with inflation levels worldwide expected to continue increasing. The luxury sector in the U.S. is projected to grow by 5%-10% in 2023, and in Europe it is expected to grow by 3%-8%. In China, thanks to the reopening after strict Covid rules, it is expected to grow from 9%-14%.

- According to a Bloomberg article, Americans, taking advantage of the strong dollar, are traveling more to Europe to buy luxury goods. This is helping leading luxury brands such as Gucci and Louis Vuitton to cover the considerable decrease in big spending by Chinese tourists. The spending by American tourists in Europe rose more than 40% during the Black Friday weekend versus the same period in 2019. An analyst at Bank of America said that U.S. buyers are paying 38% more for luxury goods in the U.S. compared with prices in Europe. The price difference used to be around 20%.

Threats

- This month China decided to flex its strict zero-Covid policy, as a higher number of cases are being reported. Over the weekend, Beijing reported long lines at hospitals and a shortage of medicine to treat fevers associated with those infected. Beijing’s clinics reported more than 20,000 visits on Sunday, according to Bloomberg. After years of lockdowns, however, China’s easing Covid restrictions will benefit the economy in the long run.

- Many people expect the luxury sector to perform well next year, betting on China reopening its economy, but this week China reported disappointing economic data. Unfortunately, it may take a while for the Chinese economy to come back to normal operations after years of Covid restrictions.

- According to Bloomberg, personal spending in the U.S. is expected to decrease from 0.8% to 0.2% in November. This could mean a contraction in the United States economy, one of the leading luxury goods markets worldwide.

Blockchain And Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Toncoin, rising 31.18%.

- Binance Holdings’ founder “CZ” said outflows from the largest cryptocurrency exchange have stabilized, writes Bloomberg, while warning employees that the industry’s recovery from rival FTX’s collapse will be bumpy. He’d earlier said Binance saw about $1.14 billion of net withdrawals on Tuesday.

- Bitcoin spiked to $18,000 for the first time since the exchange FTX slid into a chaotic bankruptcy last month, with the world’s largest digital currency also getting a boost from bets on a Federal Reserve downshift. A second month of weaker-than-expected inflation data also boosted crypto, alongside risk assets on the premise that would pave the way for slower Fed hikes, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Neutrino, down 33.29%.

- Binance Holdings, the dominant cryptocurrency exchange, has been hit by large outflows as traders move to take custody of their tokens amid revelations that rival FTX may have misused customer funds before its November implosion. As reported by Bloomberg, net outflows of digital tokens from Binance amounted to about $3.7 billion in the past week including almost $2 billion in the last 24 hours.

- Mazars Group, the accounting firm used by crypto giant Binance Holdings and other big players in the industry to vouch for their assets held in reserve, has halted all such work for crypto clients, dealing a blow to an industry seeking to shore up confidence in the wake of FTX’s collapse. In an email sent by the French Firm, Mazars said it had suspended work from cryptocurrency firms because of indications that markets haven’t been reassured by the “proof-of-reserves” reports it had published so far, writes Bloomberg.

Opportunities

- Cathie Wood scooped up more shares of Tesla and Coinbase, underscoring her faith in electric vehicles and cryptocurrency as key trends for the future. Ark Investment Management bought nearly 75,000 shares of the EV maker and about 297,000 of the cryptocurrency exchange operator on Wednesday, continuing a dip-buying streak that started in October, writes Bloomberg.

- Customer outflows from Binance’s cryptocurrency trading platforms are slowing, reports Bloomberg, according to blockchain data from two digital-asset analytics firms. The net outflow, the difference between the value of crypto coming into and leaving the exchange, was around $239 million in the past 24 hours, which is down from the daily average of $272 million over the past week.

- Hong Kong crypto futures ETFs raised over $70 million ahead of their debut. The CSOP Bitcoin Futures ETF has raked in $53.8 million, while the CSOP Ether Futures ETF has collected $19.7 million in initial investments. According to Tim McCourt, an executive at CME group, the listing of the ETFs shows the “increasing client demand for exposure to Bitcoin and Ether,” writes CoinTelegraph.

Threats

- FTX co-founder Sam Bankman-Fried was accused by U.S. regulators of carrying out a multi-year scheme to defraud investors, reports Bloomberg. The SEC said on Tuesday that Bankman-Fried, who was arrested on Monday in the Bahamas and is facing criminal charges in the U.S., raised more than $1.8 billion from investors. The SEC also said he concealed risk and FTX’s relationship with his trading firm Alameda Research and used commingled customer funds.

- Sam Bankman-Fried’s trading house Alameda Research had a secret speed advantage when executing orders on his now-collapsed FTX crypto exchange. Alameda, which also tumbled into bankruptcy last month along with FTX, was able to skirt certain portions of the exchange’s trading architecture and sidestep some automated verification process, writes Bloomberg.

- One of the most closely watched indicators of trader sentiment on Binance’s market-leading derivatives exchange suggests that anxiety over additional fallout from this year’s crypto market meltdown has grown. The seven-day average of open interest for Bitcoin perpetual futures has dropped 40.3% from the start of November, as of Wednesday. The decline comes as investors pull cryptocurrencies from exchanges such as those run by Binance, writes Bloomberg.

Gold Market

This week gold futures closed at $1,802.50, down $8.20 per ounce, or 0.45%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.36%. The S&P/TSX Venture Index came in off 0.24%. The U.S. Trade-Weighted Dollar was flat.

Strengths

- The best performing precious metal for the week was gold, but still off 0.45%. GoGold Resources finished the week up over 20% with new holes released from the El Favor East deposit within the Los Ricos North Property. Hole LRGF-22-140 intersected 0.7 meters of 2,529 grams per ton silver equivalent with a 13.9-meter section grading 294 grams per ton.

- South African gold exports in October recovered 9% month-over-month, but were only 8% lower year-over-year, due to base effects. With Sibanye Stillwater recently highlighting that it only achieved normalized production levels in October 2022, the improving trend could continue.

- Gold has enjoyed an 11% recovery from its early November lows, benefitting from the broad-based relief rally that has followed expectations of an accelerated Chinese reopening and increasing signs of a peak in developed market inflation. Specifically, the knock-on impact from a weaker U.S. dollar and the move lower in U.S. Treasury yields, with the 10-year now back below 3.45%, have also helped as well.

Weaknesses

- The worst performing precious metal for the week was palladium, down 12.99%. At the start of the week, 1.61% of the total known ETF palladium holdings were liquidated, which is 4.5 standard deviations from normal trading days. Gold fell this week after Federal Reserve Chair Jerome Powell said the authority isn’t close to ending its campaign of rate hikes, with higher-than-expected borrowing costs signaled for next year. As reported by Bloomberg, Powell pushed back strongly against bets of rate cuts next year, even as data show inflation abating, and the dollar is weakening.

- Anglo American Platinum has released a statement ahead of its 2022 investor day providing updated medium-term production guidance, plus 2023 cost guidance. Medium-term production guidance (concentrate and refined production) has been downgraded, driven by the following: lower grade at Mogalakwena, lower volumes from Amandelbult (following infrastructure closures and challenging geological ground conditions), and anticipated lower purchase of concentrate volumes.

- Gold Fields has announced the resignation of CEO Chris Griffith, and has appointed an interim CEO (Martin Preece, EVP of Gold Fields South Africa), who has six years’ worth of experience at Gold Fields and 37 years of overall industry experience. Gold Fields has not provided details on the timeline to appoint a permanent CEO.

Opportunities

- Ascot Resources has entered a non-binding letter of intent for a total of C$200 million in project financing for construction of the Premier Gold Project, located on Nisga’a Nation Treaty Lands in the prolific Golden Triangle of northwestern British Columbia. The proposed finance package will consist of a $110 million, 8.76% gold and 100% silver streaming agreement with Sprott Resource Streaming and Royalty and its affiliates and a strategic equity investment by Ccori Apu S.A.C of C$45 million for 19.9% of the company.

- Gold miner St. Barbara has agreed to acquire rival Genesis Minerals for A$541.3 million, reports Mining-Technology.com, which will result in the consolidation of its gold assets in Leonora, Western Australia. The deal will result in the creation of a mid-tier gold producer named “Hoover House” that will exclusively focus on the Leonora District in Western Australia. Other assets, such as Atlantic and Simberi will be spun out to shareholders as a new company named Phoenician Metals to be listed on the Australian Stock Exchange. The Atlantic Gold acquisition by St Barbara, on the advisement of Deutsche Bank investment advisors, was a value-destroying transaction. Interesting that as opposed to one company taking over another, we have management refocusing core operations and reshuffling non-core assets into a new entity.

- Aya Gold & Silver closed its deal with the National Office of Hydrocarbons (ONHYM) and Mines to acquire 15% in the Zgounder project and fire adjacent permits to the Zgounder Silver Mine for approximately $6.5 million. ONHYM will maintain its 3% royalty on the Zgounder property and on the newly granted permits. Benoit La Salle, President and CEO of Aya Gold & Silver, noted they look forward to their continued partnership with ONHYM to generate value for all stakeholders on mining opportunities in the Kingdom of Morocco.

Threats

- In 2022, South African gold miners have faced similar challenges to those in Europe — supply disruptions, downward production revisions and cost inflation. There may be 5% refined gold production growth in 2023/2024 driven by a ramp-up at several miners and some recovery in Anglo Platinum’s refined production from a low 2022 base. However, upgrades of downstream processing facilities are ongoing and power outages are likely to continue in 2023, limiting refined supply growth.

- Many companies could suffer from high-cost inflation through 2023 as most continue to work through high-cost inventories and as labor rates are sticky. In addition, continued Russia-Ukraine conflict and/or increased travel associated with an eventual China reopening could maintain elevated fuel prices (and other consumables associated with oil or energy) through the new year.

- The Fed pressured the market hard; it is nowhere near raising interest rates simply because we had a few economic reports of tamer inflation. The S&P 500 and the Nasdaq both lost more than 2.5% on the jawboning, yet gold only pulled back slightly. Total known physical gold ETF holdings look to have climbed this week after falling in the prior two weeks. Investors have largely pulled money out of the gold ETF since the peak this year back in April.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

Argonaut Gold

Endeavour Mining

Barrick Gold Corp.

Sibanye Stillwater

Anglo American Platinum

Ascot Resources

Ryanair Holdings

Nippon Express Holdings

Delta Air Lines

JetBlue Airways Corp.

United Airlines

Boeing Co/The

Airbus SE

FedEx Corp

LVMH Moet Hennessy Louis Vuitton

Tesla Inc.

Canadian Solar Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Bloomberg Dollar Spot Index tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar.

Retail sales tracks consumer demand for finished goods by measuring the purchases of durable and non-durable goods over a defined period of time.

The BI Global Nuclear Theme Peers is an index not for use as a financial benchmark that tracks 64 companies exposed to nuclear energy research and production.

The MSCI World Index is a free-float weighted equity index which includes developed world markets and does not include emerging markets.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All