At KCR, we believe in the Quantamental Investment approach–a strategy that leverages the most useful aspects of both quantitative investing and fundamental investing.

Below, we detail our strong belief in the quantamental investment strategy and show why KCR’s models– which we have been meticulously building and improving since 2010– are relied upon by some of the world’s leading institutional investors and asset allocation firms.

What is Quantamental Investing?

First, we have to define quantitative investing and fundamental investing.

Quantitative management involves using large portfolios of stocks that are rebalanced at predetermined intervals with the goal of exploiting alpha, or excess return, using various factors or alternative data. Building on work done by Joseph Lakonishok, the legendary professor of behavioral finance and a founder of LSV, our white paper The Persistence of Profits offers compelling evidence based research on the power of mean reversion in factor-based investing.

This is a clear departure from Fundamental Investing, the more traditional approach, which involves evaluating the quality of a company based on projected future cash flows and various qualitative factors. Note that KCR understands the importance of the fundamental approach – see our recent post on speculative trading for a transcribed presentation from Peter Lynch, who champions the fundamental approach.

The term "Quantamental" refers to a hybrid approach that combines quantitative and fundamental analysis to make investment decisions. This approach seeks to exploit returns by using both quantitative methods and more traditional fundamental methods.

Quantamental Investment has become an umbrella term for a wide variety of methods, including the use of big data and machine learning for high-speed trading and the use of simple factor-based tools. While Quantamental Investing removes the potential complication of human bias, fundamental analysis allows for the human capacity to recognize factors that machine learning will not be able to account for. Combining the two approaches provides the most advanced, actionable portrait of a potential investment, in our view.

Quantamental Investing Strategies: The KCR Approach

KCR’s team believes in the Quantamental approach as the best method for creating systematic alpha. This belief is based on 60+ combined years of experience, and a set of models that we have been building and improving by hand since the company’s founding in 2010. This process is arduous, but it yields results: in the 12 years since our firm’s founding, our model portfolios have generated significant alpha across a number of diverse US equity products.

Our published research has applied our quantamental approach to identify and capitalize on bubbles in a variety of areas, including dividend stocks and speculative excess similar to that observed in 1999. We have also identified instances of undue pessimism in the market, enabling us to purchase blue-chip companies at discounts to intrinsic value.

This 90-second video tutorial provides a brief overview of how our model functions.

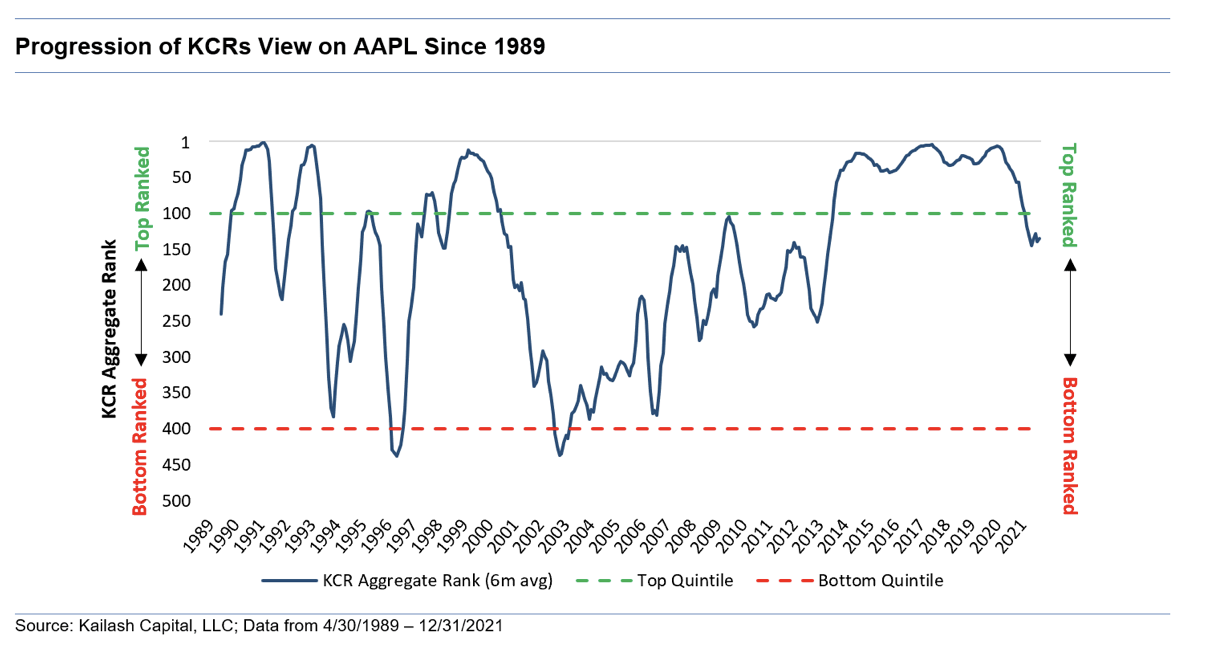

The chart below shows how KCR classifies our bullish, neutral, and bearish zones.

- When a stock ranks in the top 100 ranked stocks, our model identifies the stocks that Kailash Concepts believes represent mispriced quality.

- When a stock is in the middle of the model, between rank 200 – 400, the model effectively has no actionable opinion.

-

When a stock falls into the bottom 100 stocks, the model warns that the firm is either grossly overvalued, has balance sheet problems, accounting irregularities, or some combination of those issues

Dr. Sanjeev Bhojraj is a portfolio manager and co-founder of L2 Asset Management. He is widely published in journals in finance and accounting and specializes in behavioral finance. Dr. Bhojraj is a Chaired Professor in Asset Management and the co-director of the Parker Center for Investment Research at Cornell University’s Business School. He has a Ph.D., ACA, ACMA, and B.Com.

Matt Malgari is a portfolio manager, Managing Member, and co-founder of L2 Asset Management. Matt spent 14 years at Fidelity Investments as an Assistant Portfolio Manager on its $70 billion Diversified International Fund, sector analyst, diversified analyst, and trader. In 2010, Matt became the Managing director of Equity Research for Knight Capital Group. He received his MBA from Cornell University and a BA from Middlebury College.

© Kailash Concepts Research, LLC

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research