Payden & Rygel 2023 Macro Outlook: Macro Memes & Mind Viruses

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe call them narratives, memes, or mind viruses. They are the stories that infect investors’ minds, encouraged by market action. Sometimes the narratives are correct, other times wrong, and often sudden narrative shifts move markets the most. So what are the main macro narratives impacting markets as we head into 2023?

In his new book, Nineteen Ways Of Looking At Consciousness, Patrick House explores the various theories that attempt to explain the mystery of human consciousness.1 He tells the story of Anna, a patient with epileptic seizures who undergoes brain surgery to alleviate suffering. Doctors numb her scalp and, because the brain does not have pain receptors, keep her awake to talk to her while “using electricity and micro-thin blades” to explore her brain.

At one point, the doctors find a spot in her brain that, once stimulated, causes Anna to laugh out loud. When doctors ask her why she’s laughing, instead of saying, “I don’t know,” Anna’s story changes each time she’s asked the question. “You guys are just so funny...standing around,” was one response, “the horse is funny,” another.

House’s takeaway: “because the brain abhors a story vacuum and because the mammalian brain is a pattern-recognizing monster,” Anna made up a story to make sense of her laughter. She confabulated. “Even a wrong pattern, a guess, is at least a pattern to learn against,” House says.

A brain is a narrative-generating machine. Humans latch onto stories to explain the data and events we encounter. We struggle to admit “I don’t know” or “It’s more complicated.” Instead, the emotions generated by the ups and downs of financial markets further fuel our desire to make sense of things. We find or create a story that fits. But in telling stories, we often fool ourselves into believing we know what’s happening and, worse, what the future holds.

As a result, some famous investors have thrown out macroeconomic forecasting. Why pretend to know the future? Our macro stories about the present may be wrong, and nobody knows the future. None other than Howard Marks once quipped, “agnosticism is probably wiser than self-delusion.”2

We agree and have long advocated a different approach to macro. The heart of our process is identifying the popular narratives driving markets and where they could be wrong.

Call it “poking holes,” “criticizing views,” “myth-busting,” or “misconception-correcting.” We use criticism and skepticism, not prophecy, to drive our process.

Below we identify ten key macro narratives, criticize them, give our tentative take, and then handcuff ourselves by identifying specific metrics that will force us to change our view.

Remember Anna, and let’s begin.

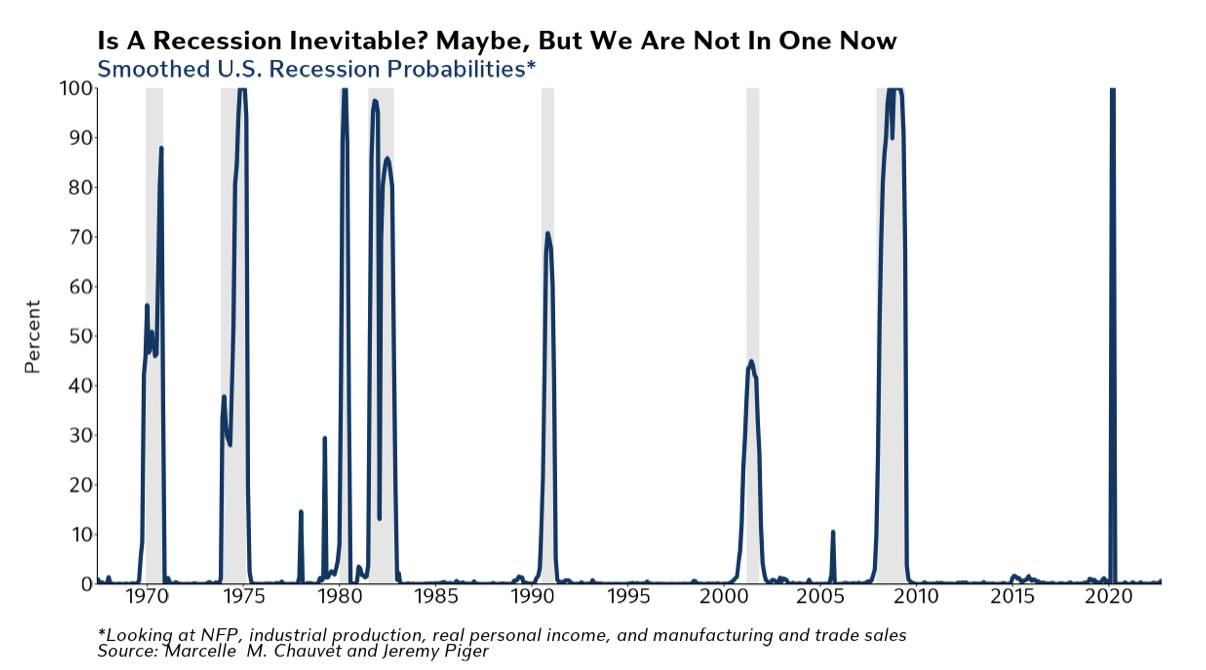

Narrative #1 | “A recession in the next twelve months is inevitable.”

The Bloomberg Consensus survey shows a 62.5% probability of a recession in the next year. If a recession occurs in 2023, it will be the most anticipated downturn on record.

And, yes, the “four horsemen” of recessions all point to a downturn. The Leading Economic Index (LEI) peaked in February 2022 and has declined for nine consecutive months. Never have the LEIs posted such a decline without a recession following.

The 3-month/10-year yield curve, one of our favorite business cycle indicators, is deeply inverted. The 3-month/10-year yield curve is also a reliable sign of an economic downturn, having inverted before every recession since 1960 (with one false positive in 1967).

Third, the housing market has slumped. Since the housing cycle (sales, building/investment) is the business cycle, a recession is likely to follow.

And, of course, the Federal Reserve’s

monetary policy stance is nearing restrictive territory. Rapid rate rises often precede downturns.

However, since the recession narrative is so widely held, it’s worth considering why it might not pan out as advertised. First, the above indicators do little to nail down the precise timing of a downturn. A good guess is sometime in the next 12 months, but the lag could be longer. A recession may not begin until the latter half of 2023 or later.

Why?

First, while the Fed has tightened financial conditions sharply in 2022, monetary policy is not yet restrictive by historical standards. The “real” (inflation-adjusted) federal funds rate is still negative as of this writing. Talk of the Fed “plunging the economy into a recession” might still be premature.

Second, the labor market is extremely tight, cushioning consumer spending. And, if job openings fall from extremely high levels without a rise in the unemployment rate, a “soft landing” could occur. While not our base case because it would be highly unusual, investors should consider the possibility of a soft landing scenario, at least in the short run.

What we’re watching that will force us to change our view:

A slowdown in aggregate income growth, which accounts for the total increase in employment and wages. Right now, aggregate income is growing ~7% year-over-year. Weakness in the labor market, signaled first by a continued pick-up in initial and continuing claims for unemployment insurance (both very low still), will also attract our attention.

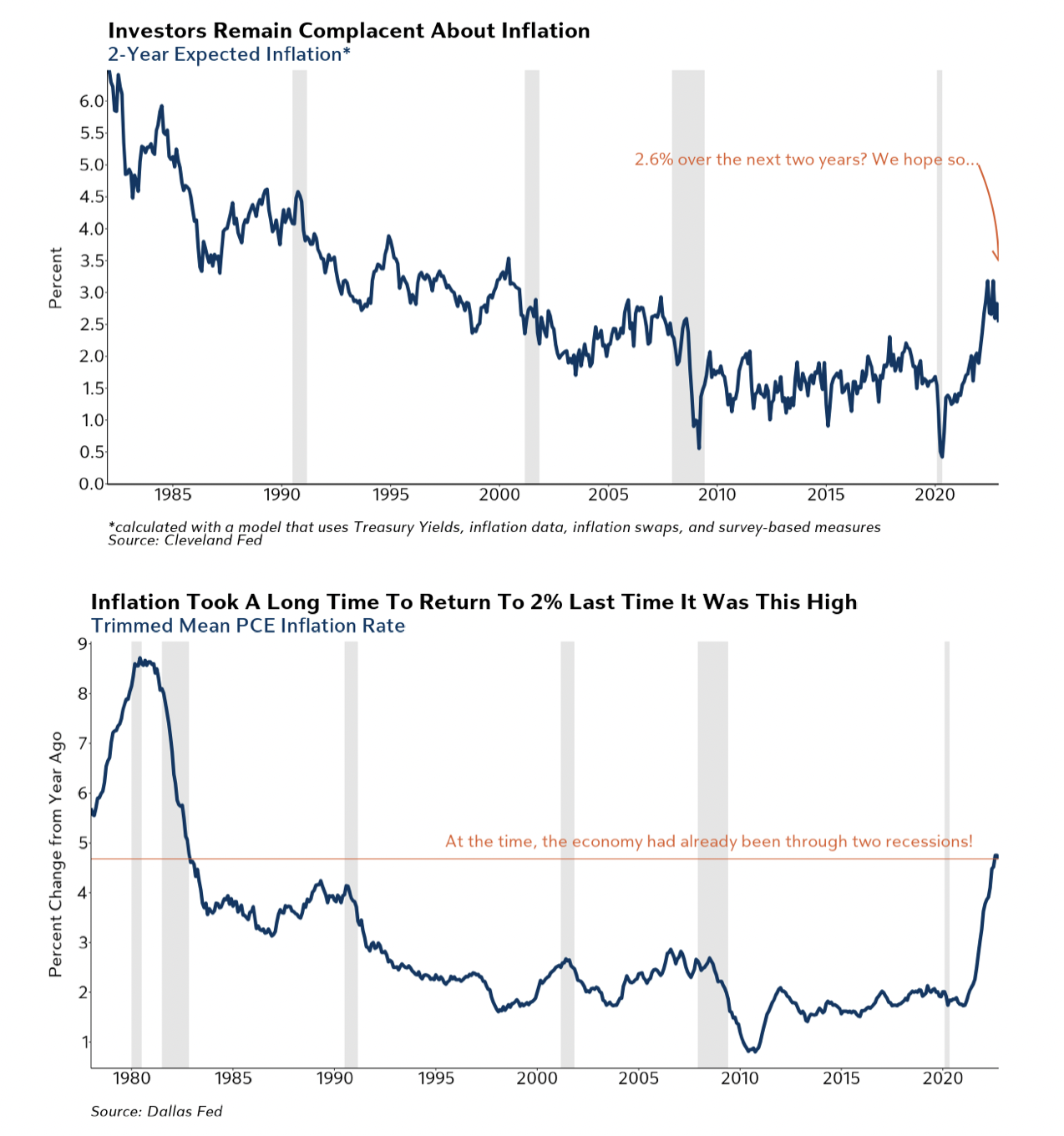

Narrative #2 | “Inflation Will Slow Quickly Next Year.”

The slowdown in inflation is widely expected and appears to be priced in. Case in point: the 1-year U.S. CPI swap is 2.4%, and two-year breakeven inflation derived from the TIPS market is already back to 2.1%. Since core inflation is currently in the 5%-6% range, the fact that the market expects a rapid deceleration in inflation is not a straw man narrative.

However, history does not provide much evidence for sharp slowdowns in inflation. For example, the last time the Dallas Fed’s trimmed mean PCE index was up 5% year-over-year, it took around 15 years to slow to the 2% range (see figure 3).

Even during the 2008 recession, which disproportionately impacted housing, core services CPI decelerated from 3.3% year-over-year at the start of the recession to 2.7% year-over-year a full year into the downturn.

What we're watching that will force us to change our view: Here’s our framework for 2023 inflation: dividing core PCE into three of its key components. First, we expect core goods deflation. Second, we expect housing services costs (e.g., rents) to peak in Q2 2023 and gradually decelerate toward their historical norm. And third, we expect non-housing services to remain robust until the labor market deteriorates (Q4 2023). As a result, core PCE will still be ~4% by the year-end of 2023. A more rapid deceleration in core goods, a sharper decline in housing services prices and/or a sustained decline in non-housing services prices would change our view.

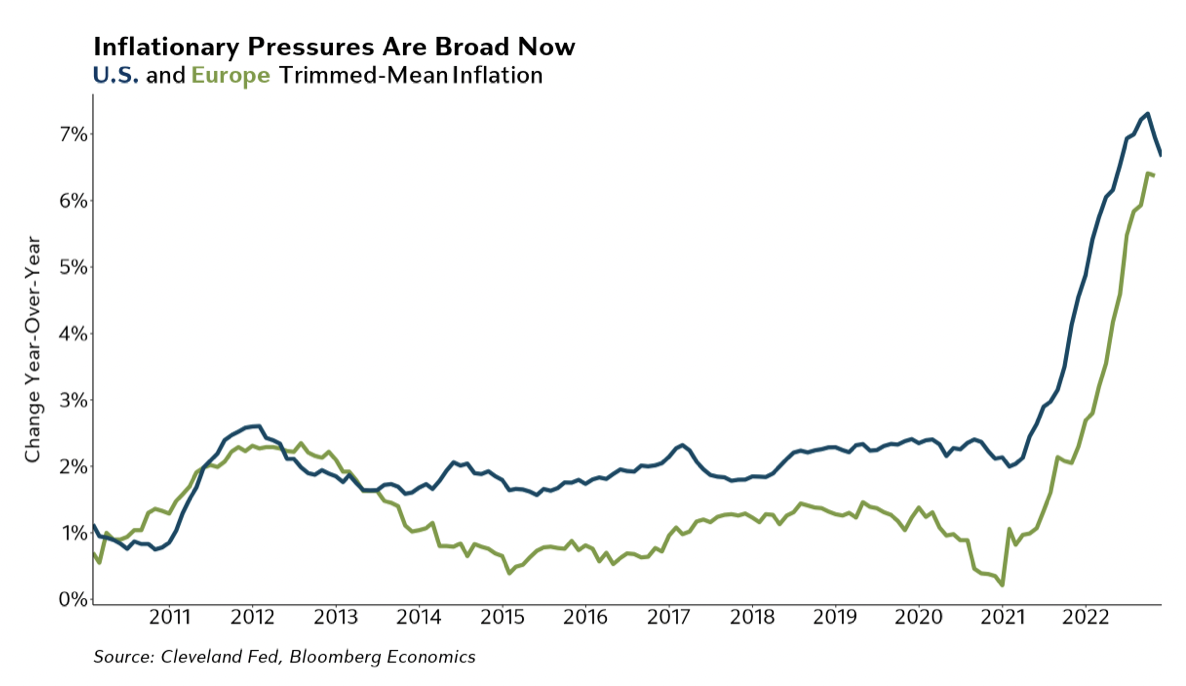

Narrative #3 | “Well, inflation in Europe is more supply-side, food and energy driven, meaning global inflation should dissipate quicker.”

Not so fast. We’re fond of using trimmed mean measures of inflation as “alternative core” measures because they exclude outliers to better gauge the underlying inflation trend. As shown in the chart below, the picture looks worrisome even (or especially) for Europe, which has been plagued by food and energy costs. Inflation pressures have spread broadly.

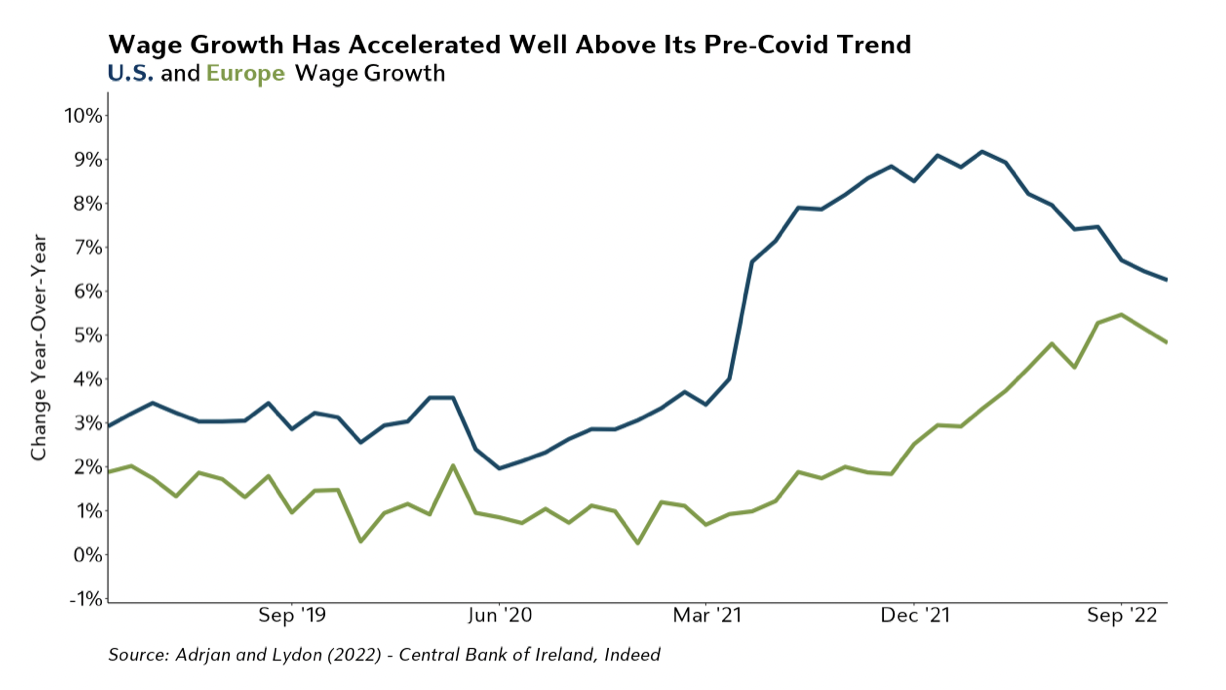

Second, inflation skeptics in Europe have cited low wage growth as a reason to remain sanguine about inflation. While not quite matching the increases seen in the U.S., European wage growth has accelerated well above its pre-Covid trend.

What we’re watching to make us change our view: A slowdown in trimmed mean inflation measures and fading wage growth would make us less concerned.

Narrative #4 | “The Fed will raise its inflation target since it can’t get actual inflation back to 2%.”

Olivier Blanchard, former IMF Chief Economist, and Jason Furman, former Chair of the Council of Economic Advisors, have floated the idea that there is nothing special about 2% and the Fed should raise its inflation target.3 The narrative has also become increasingly popular among traders over the last year as a retort to our “inflation will be slow to fade” view. But outside of academic circles, we see little support for the idea among policymakers.

Chair Powell was asked if he was open to a change in the target after the December 2022 Fed meeting. According to Chair Powell, “changing our inflation goal is something we’re not thinking about.” He emphasized that the Committee is “not considering that [raising the target] and not going to consider that under any circumstances.”

The most recent change to the Fed’s policy framework, the Flexible Average Inflation Targeting (FAIT) framework, resulted from a multi-year public review process. The next policy review is scheduled for 2025. Like it or not, we’re stuck with a 2% target.

What we're watching that will force us to change our view: If Fed policymakers, including Chair Powell, start commenting that they might discuss it in their policy review or if the longer-run forecast of inflation in the Summary of Economic Projections is changed from 2.0%.

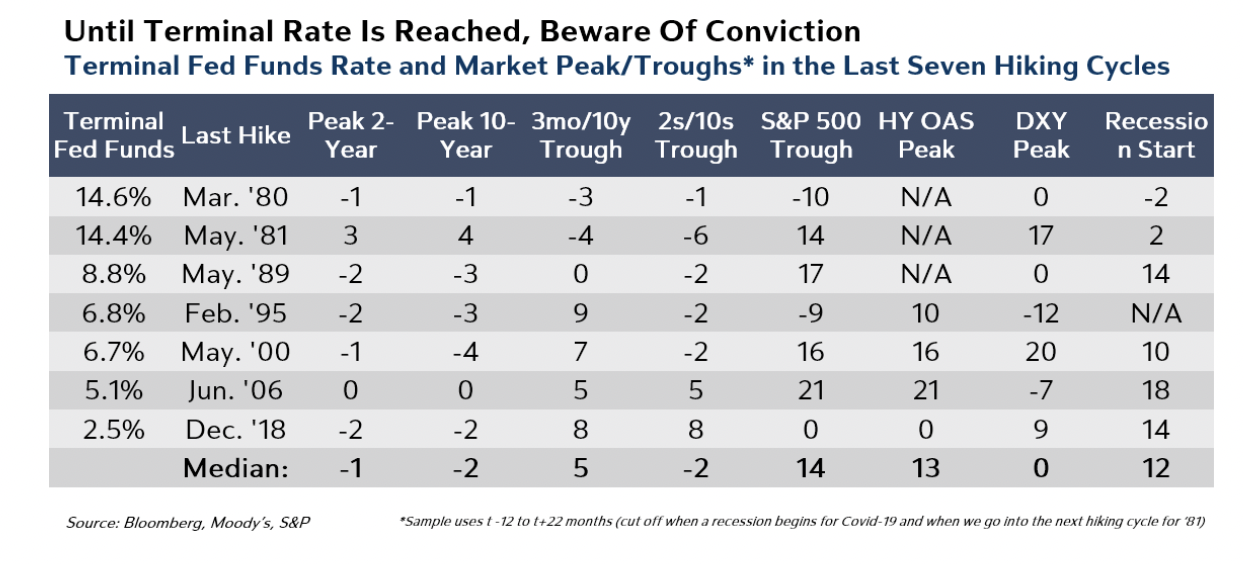

Narrative #5 | “Interest Rates Have Peaked.”

Global interest rates have rallied in recent weeks, but a peak rate call may once again prove premature.

Historically, interest rates, whether we are talking 3-month Treasury bills, 2-year Treasuries, or 10-year Treasuries, peak around the time the Fed reaches its terminal rate (see figure 6). Our view is that due to sticky inflation, the Fed will keep raising the federal funds rate until Q2 2023, bringing the federal funds rate to 5.50%. As such, peak rates may occur closer to Q2 2023.

What we're watching that will force us to change our view: Hints from Fed policymakers that a pause to their rate hiking cycle is closer than we currently anticipate.

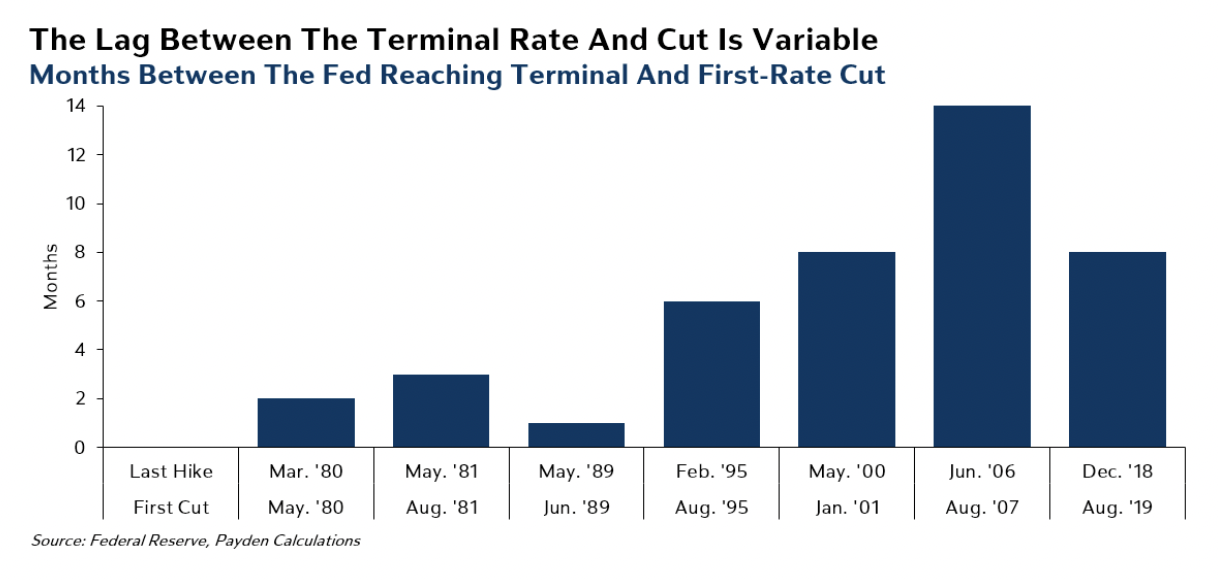

Narrative #6 | “OK, But Rate Cuts Arrive Soon After the Terminal Rate Is Reached!”

It’s a popular narrative that the federal funds rate doesn’t tend to hang around for long at its cycle peak. But is it true?

Reality: the Fed only started publishing its target rate in 1994. In the four hiking cycles since then, the Fed has waited for an average of 9 months between reaching the terminal rate and its first rate cut. However, during the mid-2000s cycle, the Fed paused for 14 months.

More importantly, the earlier cycles, which drive down the average and provide fodder for the narrative, represent the scenarios the Fed is expressly trying to avoid this time around. The Fed declared victory over inflation too quickly in 1980, cutting rates, only to resume rate hikes in 1981 once inflation picked back up. Also, none of the post-1994 cycles have been plagued by inflation, which may delay the Fed from cutting rates.

We wouldn’t bet on the “rate cuts will soon follow peak Fed” narrative unless inflation slumps soon. What we’re watching that will force us to change our view: Fed policymakers’ comments on what it would take to necessitate a rate cut and/or inflation decelerating much more quickly than we expect.

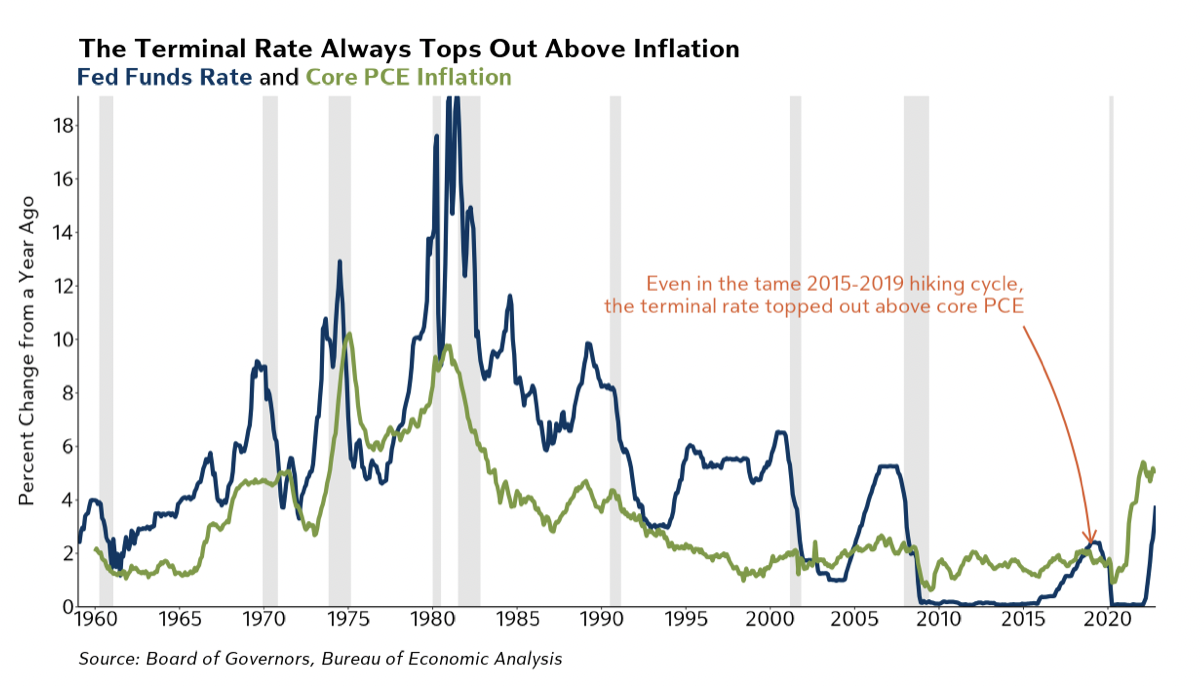

Narrative #7 | “The Fed won’t cut until inflation is below the federal funds rate.”

The idea underlying this narrative is that inflation won’t fall unless the Fed squeezes the economy even harder.

History agrees! In no cycle on record (not even the tame 2015-2019 one!) did the terminal federal funds rate top out below the year-over-year rate of core inflation. (see figure 8)

Will the Fed cease hiking when the real (inflation-adjusted) federal funds rate is still in negative territory? We wouldn’t bet on it at this point. The Fed Chair said in early December that the goal is to get the real federal funds rate “into positive territory” and keep it there “for some time.”

What we’re watching to change our view: Fed-speak about real federal funds rate, neutral rate estimates, and terminal rate compared to the actual path of inflation.

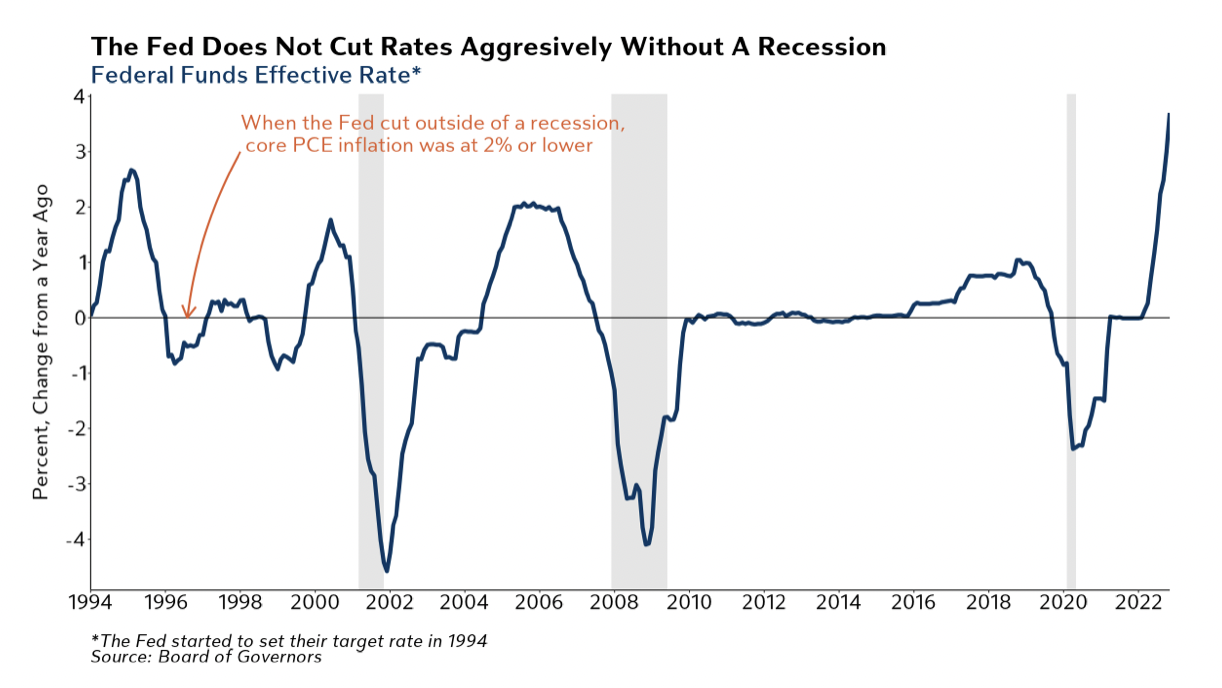

Narrative #8 | “When the Fed cuts rates, they do so quickly.”

The “Fed cuts fast” narrative seems to be adopted in service of the Fed pivot narrative. After all, investors remember that as recently as March 2020, the Fed cut rates by 150 basis points in a few weeks!

Apart from the obvious—that we aren’t forecasting a coordinated shutdown of global economic activity due to another pandemic—could the Fed cut rates quickly? History suggests that they can, with the Fed cutting rates in excess of 300 basis points within 12 months.

The key caveat to this narrative is that these periods involved a recession. Even then, the Fed did not cut rates until the economy was already in a recession.

Lastly, inflation has not been as much of a problem since the 80s. In past cycles, the Fed could cut rapidly since core PCE was around 2%. With core PCE inflation more than three times the Fed’s target, the risk is that rate cuts are slower even in a recession if they happen at all.

What we’re watching to change our view: The Fed would have to achieve its inflation target faster than expected, with or without a recession. If core PCE returned to 2% quickly, then the Fed could ease monetary policy.

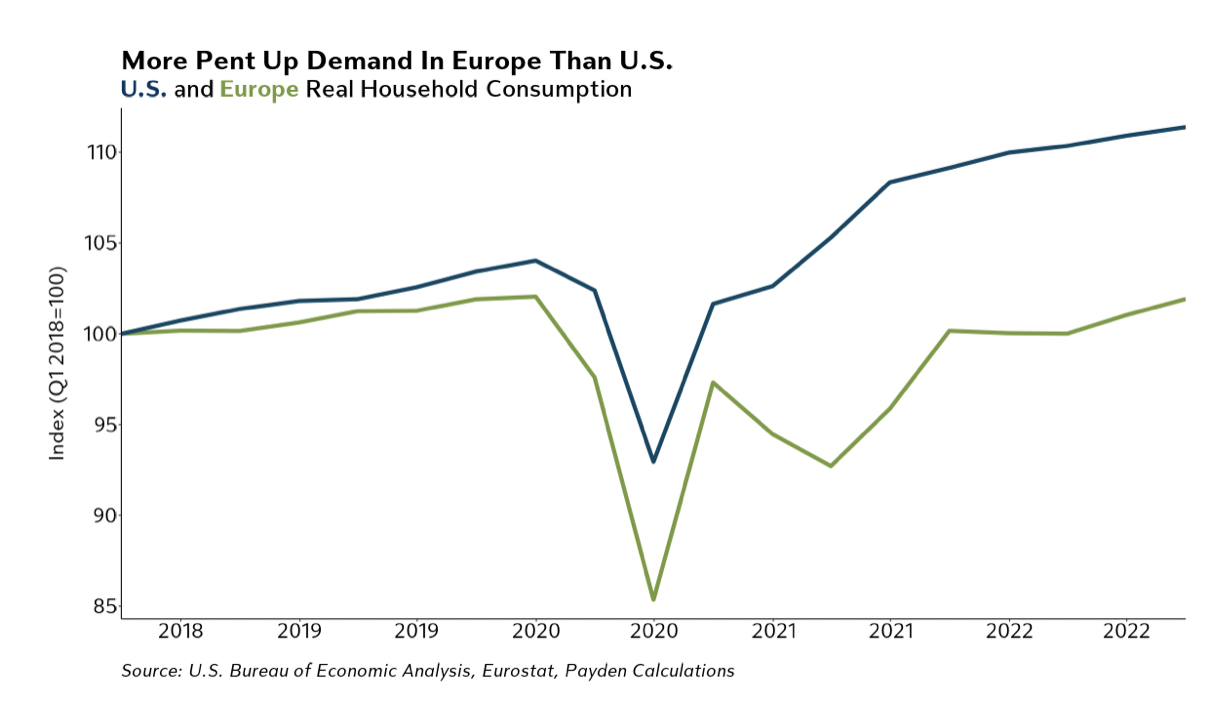

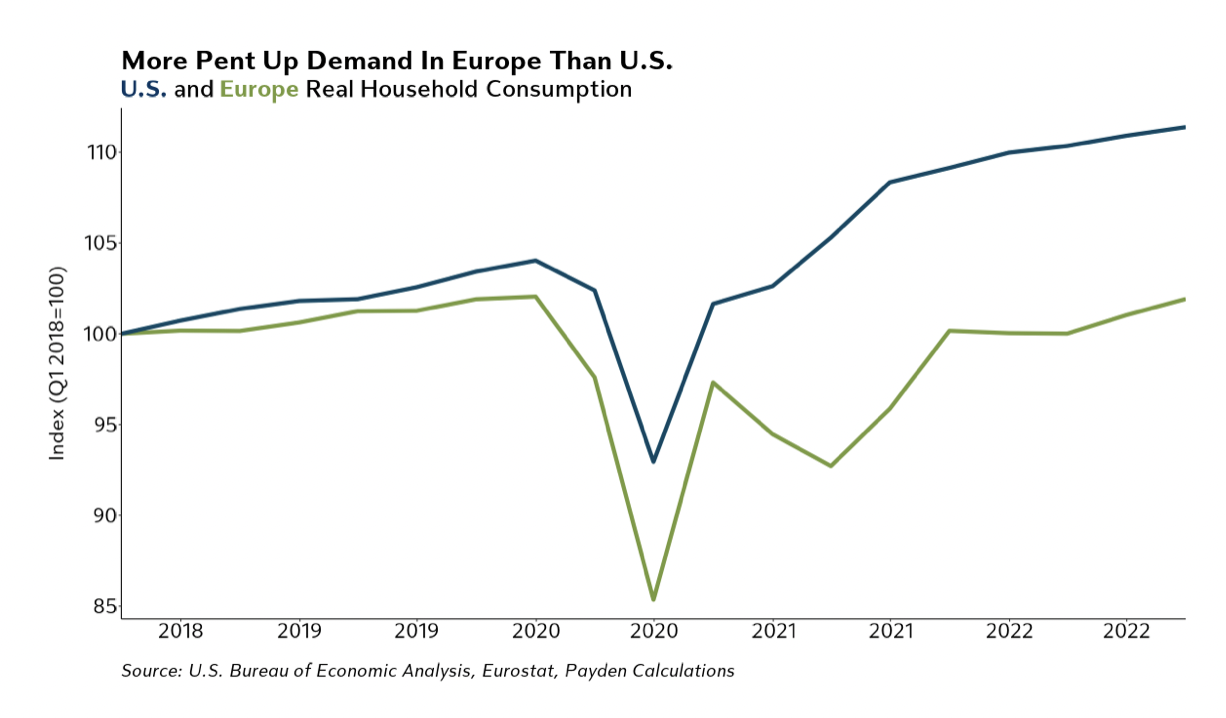

Narrative #9 | “The U.K. & Europe face worse recessions.”

Europe and the U.K. have had their host of issues, specifically after the Russian invasion of Ukraine. Europe’s energy reliance on Russia also led to a surge in energy prices and snarled supply chains that led to continued inflationary pressures.

During that time, the European Central Bank and the Bank of England raised rates by 200 and 300 basis points, respectively. Unsurprisingly, consumer and business expectations and economic activity indicators have soured and the narrative is that the U.K. and Europe face “hard landings” or worse recessions than the U.S.

While our baseline case assumes the same, the recovery in the U.S. was a lot more robust than in Europe, particularly household consumption. Even in a recession, there is more pent-up demand within Europe if the labor market and incomes don’t suffer as much.

Where we could be wrong: If the labor market in the euro area weakens and wage growth slows we would stick with our baseline view. Another reason would be if financial conditions tighten rapidly as the ECB rate hikes cause sovereign debt issues a la the 2011-2013 double-dip recession.

Narrative #10 | “If the U.S. economy struggles, the global economy will suffer.”

The adage goes, “When the U.S. sneezes, the global economy catches a cold.” It’s common for U.S. investors to settle on their U.S. outlook and then derive global views. But the saying may be outdated.

China likely matters more for the global economy in 2023. In a recently published paper, four Fed Board economists opined that “what happens in China doesn’t stay in China.”

Consider: China accounted for about 40% of global vehicle sales in 2021, almost double the size of U.S. sales, 25% of global smartphone sales, 50% of global steel and coal demand, and 14% of global oil demand!

Fed researchers found “similar effects from U.S. monetary policy easing and credit stimulus policies in China.” With the dollar depreciating, and global financial conditions easing, one percent of Chinese GDP stimulus would be equivalent to about half the size of a 25 basis point federal funds rate cut.

Investment Implications

Another virtue of our macro approach is that different strategists may glean different conclusions from our process and perspective. We aim to disconfirm narratives, not dictate views.

However, we do think there are many investment implications to consider. For example, if your view is that “a recession is imminent and inflation will quickly fade,” or “inflation is rolling over and the Fed will soon cut rates,” we have presented our doubts above.

As we see the macro picture today, it’s likely that continued U.S. growth over the first half of 2023, sticky core inflation, and potential upside surprises to growth in the U.S., Europe, and China, all lead to additional central bank rate hikes in 2023.

In short, perhaps the things everyone views as “inevitable” will just take more time to play out. We’ll update our views and address new narratives as the year progresses.

End notes

1. House, Patrick. Nineteen Ways of Looking at Consciousness. New York: St. Marten’s Press, 2022.

2. Howard Marks. Thinking About Macro. Memo To OakTree Clients. 29 July 2021.

3. Dudley, Bill. “The Fed Shouldn’t Raise Its Inflation Target.” Bloomberg. November 28, 2022.

4. Barcelona, William L., Danilo Cascaldi-Garcia, Jasper J. Hoek and Eva Van Leemput (2022). “What Happens in China Does Not Stay in China,” International Finance Discussion Papers 1360. Washington: Board of Governors of the Federal Reserve System.

2023 Payden & Rygel All rights reserved

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All