Gold Nearing Strongest Buy Signal In Four Months

Membership required

Membership is now required to use this feature. To learn more:

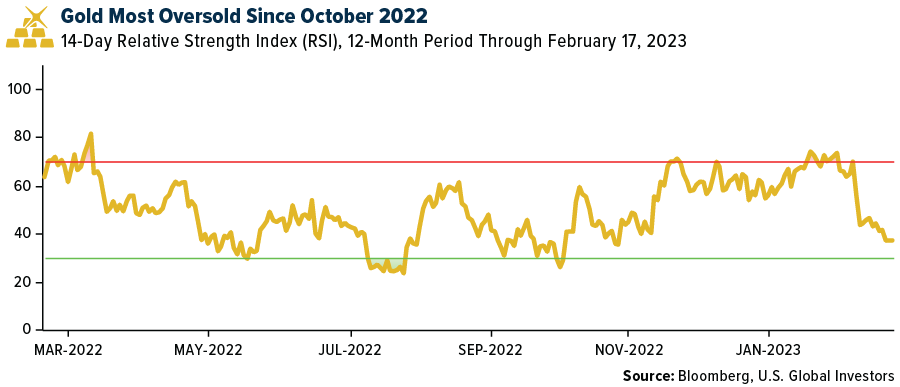

View Membership BenefitsGold is nearing its strongest buy signal in four months as the U.S. dollar eases off a rally that’s carried the greenback to its highest point since early January. According to the 14-day relative strength index (RSI), gold was at its most oversold level since October 2022 this week, indicating it may be time to consider buying in anticipation of mean reversion.

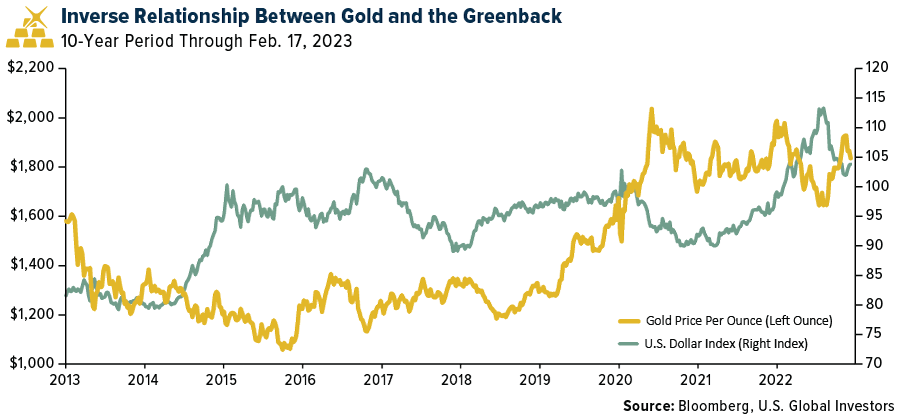

As I’ve shown you many times in the past, gold and the dollar share an inverse relationship, since the precious metal is priced internationally in the greenback. When the dollar is strong, it may be time to accumulate gold. Conversely, when the dollar begins to cool, it may be time to take some profits.

The Economics Of Underwear

Gold is currently about 6% off its 2023 high of just under $1,960 an ounce, under pressure from the dollar, which has made gains against a basket of world currencies in recent days on economic data that all but guarantees additional rate hikes. Unemployment sits at 3.4%, the lowest reading in more than half a century, giving the Federal Reserve the go-ahead to continue its fight against inflation.

This week, the consumer price index (CPI) showed that inflation is still running hotter than expected.

Consumer prices rose 0.5% between December and January, up from an increase of 0.1% in the November-to-December period. Some of the items and services that jumped the most in price in January were utility gas services, eggs, breakfast sausage and ham, instant coffee and—just in time for tax season—tax return preparation fees.

The price of men’s underwear rose 5.5% month-over-month, which is notable since this was former Fed Chair Alan Greenspan’s favorite economic indicator. According to Greenspan, a jump in underwear demand could mean that the economy is on solid footing, the reason being that no one’s aware if you’re wearing a pair of old skivvies or the latest brand-name undergarments. That underwear prices jumped so much from December to January implies that consumers are confident enough in the economy to splurge on something that’s generally out of public view.

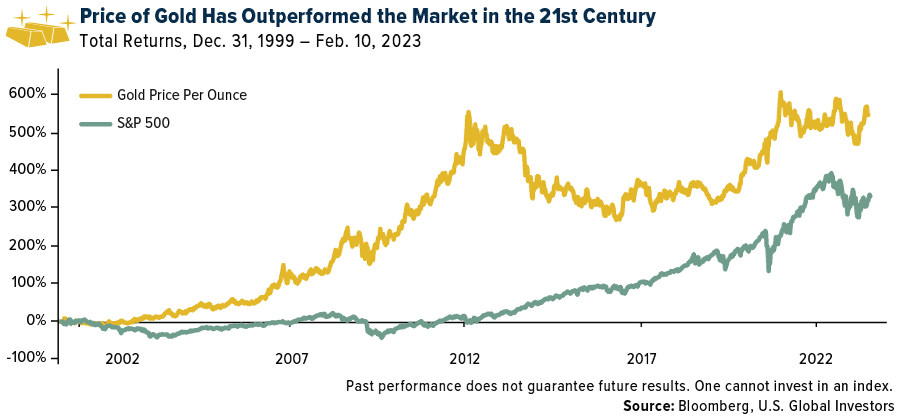

Gold Still Beating The Market Over The Long Term

Gold’s technicals may be telling us it’s time to buy, and its long-term fundamentals remain healthy and attractive. In the chart below, I’ve updated the performance comparison between gold and the S&P 500 since the start of the century. The metal is still beating the market as of the end of last week, by a factor of approximately 1.6.

In 2022, gold’s price was mostly supported by strong bullion demand in the U.S. and Western Europe and record purchases by central banks. We may see a repeat of the voracious buying this year, if one forecast turns out to be right.

Goldman Sachs analysts believe that global central banks are on track to add an unprecedented amount of gold by the end of 2023 as they seek to diversify away from the U.S. dollar. That’s especially the case following U.S.-led sanctions against Russia for its invasion of Ukraine.

Central banks purchased a record 1,136 tons of gold in 2022, the equivalent of 40 million ounces, according to the World Gold Council (WGC). Turkey was the biggest official buyer at roughly 147 tons, followed by China at 62 tons and Egypt at more than 44 tons.

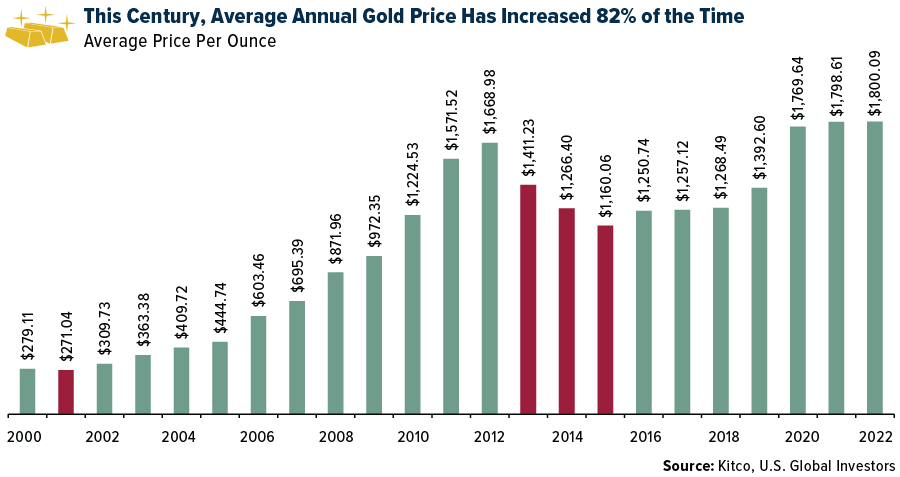

But banks could top that amount this year, with imports potentially exceeding 1,200 tons, Goldman says. Combined with improving economic conditions in China and India, the world’s two largest consumers of gold, the precious metal’s price could average $1,950 an ounce in 2023.

Although not a record total amount, $1,950 would represent a record average amount, as you can see below.

In 19 of the past 23 years, or around 82% of the time, the average price of gold has risen year-over-year. If the metal were to average $1,950 this year, it would mark the eighth consecutive year of average-price increases.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.13%. The S&P 500 Stock Index fell 0.29%, while the Nasdaq Composite climbed 0.59%. The Russell 2000 small capitalization index gained 1.46% this week.

- The Hang Seng Composite lost 2.22% this week; while Taiwan was down 0.69% and the KOSPI fell 0.75%.

- The 10-year Treasury bond yield rose 7 basis points to 3.812%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Air France, up 14.5%. Bombardier adjusted earnings per share (EOS) came in at $2.09. Adjusted EPS came in above the Bloomberg mean of $0.50. The beat was primarily driven by income tax recovery of $121 million, which added approximately $1.24 to EPS. Total revenues were up 49.9% year-over-year, mainly driven by increased deliveries, favorable aircraft mix, and aftermarket services growth of 14.6% year-over-year.

- After pulling back earlier this year on softer tanker pricing, the Evercore ISI Shipping Index moved up 5.5 points from 60.8 to 66.3. Contacts report the market is rebounding and remains strong as Russian crude absorbs a lot of ton-miles.

- Air India placed a record-breaking order for 470 new aircraft from Boeing and Airbus. The order contains 220 Boeing aircraft valued at $34 billion. Additionally, the order includes options for an additional 50 737 MAXs and 20 787s, bringing the total number of Boeing aircraft to 290 and the total value to $45.9 billion. This is Boeing’s third largest sale of all time in terms of dollar value and its second largest in terms of quantity.

Weaknesses

- The worst performing airline stock for the week was Azul, down 11.5%. Per press reports, the Department of Justice is likely to sue to block the pending $3.8 billion JetBlue-Spirit merger, which is an expected step in the ongoing process with most courts siding in favor of mergers.

- LNG shipping rates have been falling every week since mid-November and while not at trough levels, they are not far from it. At the same time, U.S. natural gas prices have fallen to levels last realized since the heart of the pandemic.

- European airline bookings, as a portion of 2019 levels, declined to -1% in the week, mainly driven by lower intra-Europe net sales. Total net sales were down 5% this week. Intra-Europe net sales declined by 14 points to -16% versus 2019 and were down 17% this week.

Opportunities

- On average, first quarter 2023 airline revenue guidance came in 0.8% better than Street estimates. Pricing guidance came in down 0.4%, worse than Street estimates. The only airlines which guided to a deceleration in the first quarter on revenue growth were American Airlines and Hawaiian, which is impacted by spoilage, a slow Japan re-opening, and inter-island competition.

- Nippon Express announced flat fourth quarter sales year-over-year, operating profit down 16% and a net loss of ¥7.8billion due to booking impairment losses. Operating profit of ¥27.3bn was 6% shy of consensus. While air and marine forwarding prices look set to normalize over the year, the company expects volume recovery in the second half and the achievement of its medium-term plan targets by strengthening its core businesses and improving cost control.

- Goldman’s domestic, close-in pricing airfare study is up 35% versus 2019 this week, the strongest print in 2023 to-date and helping to drive a positive 14% versus 2019 year-to-date average in 2023. Based on its proprietary pricing study, December and early January experienced a slightly softer pricing environment versus October/November before fares accelerated in mid-January.

Threats

- While fuel has come down in recent weeks, the average jet fuel price is up 4.7% year-to-date (primarily driven by New York Jet up 40.4% year-to-date). The most exposed airlines to New York jet fuel are United Airlines and JetBlue. Looking at various scenarios, the current fuel curve for 2023 is on average 6% higher.

- On the West Coast, port labor talks, which began in May 2022, remain in limbo with no signs of progress. The talks cover 22,000+ dockworkers at 29 ports along the west coast who have been working without a contract since the last agreement expired on July 1, 2022. On the West Coast, many regional issues have delayed discussions of major contract provisions such as wages and automation, so there is likely a long road ahead.

- Despite a dramatically improved demand environment since a year ago, along with fuel prices and a BRL back close to where they were, shares of Azul Airlines and GOL have declined markedly. This reflects the loss of confidence by capital markets (bond/equity) following the deterioration of balance sheets given the one-two punch of the Covid pandemic followed shortly by the knock-on effects on jet fuel prices from the Russian invasion of Ukraine.

Luxury Goods And International Markets

Strengths

- According to the Tourism Board, total visitation to Hong Kong during the month of December was 160,578 people (versus 113,763 in November of last year), (of which 67,244 were from the mainland). New numbers of visitors are still low compared to pre-pandemic levels, but they are improving. In 2022, visitors to Hong Kong grew 561% year-over-year.

- following a much weaker December in which sales fell 1.1%. Bloomberg economists were expecting the sales to rise only 1.9%. Stronger sales data is a sign of robust consumer spending despite elevated inflation.

- Beneteau SA, a French company that designs, assembles, and sells sailboats and motorboats, was the best performing S&P Global Luxury stock for the week, gaining 10.48%. The company reported record revenue for the full year of EU1.51 billion, an increase of 23%, beating estimates. Shares increased to 16.4 euros this week, the highest close since 2018.

Weaknesses

- Chanel’s sales have been decreasing in Hong Kong due to continuous price hikes, said an article from The Korea Times on Bloomberg. There are no longer long lines to enter Chanel’s stores, where in previous years customers would wait up to six hours to enter. Chanel has been raising its prices, especially in its handbags category, several times a year. A bag that costs around $7 million won ($5,400), now costs around $13 million won ($10,000). Channel’s handbag prices on secondhand online markets are declining however, because demand has been drying up.

- Kering reported results this week. Revenue decreased because of weaker results from Gucci and Balenciaga, two of its leading brands. The company said that Gucci’s revenue declined 14% in the fourth quarter because of disruptions out of China. In the case of Balenciaga, revenue fell 4% because of its controversial campaign in November. In the past year, Kering underperformed both its rivals LVHM and Richemont.

- Start Entertainment Group, an Australian company that owns and operates casinos, hotels, nightclubs and restaurants, was the worst performing S&P Global Luxury stock for the week, losing 20.53%. The company this week reported that revenue from one of its main casinos in Sydney decreased by 13.5% in December. Additionally, due to a regulatory inquiry, the company’s casino license was suspended, and they received an impairment charge of up to $1.6 billion.

Opportunities

- Benedetto Vigna, Ferrari’s CEO, one of the leading luxury carmakers worldwide, announced the company will launch its first 100% electric car in 2025. Ferrari wants to offer consumers a unique and exclusive experience while still guaranteeing the thrill of driving one of its exclusive vehicles.

- According to Bloomberg, the United Kingdom Services PMI is expected to be reported next week at 49.3 versus a previous month reading of 48.7. This is a key leading indicator that could represent an improvement in the state of the economy in one of the major economies in Europe. The Eurozone’s Service PMI will be released next week as well, and will likely jump further, moving higher above the 50 level that separates growth from contraction.

- LVHM, one of the most valuable luxury brands worldwide, announced that it has hired a new creative director of menswear, Pharrell Williams. His first collection will be presented during Fashion Week that will take place in Paris later this year. Williams has collaborated with the brand previously in 2004 and 2008. Williams is well-known in the industry and will offer brand new exposure through his social media community of more than 14.3 million followers.

Threats

- Year-over-year inflation in the United States decreased in January, but not as much as expected. The CPI was reported at 6.4% versus the previous month reading of 6.5% and a consensus call for 6.2%. Elevated inflation could give the Federal Reserve the green light for implementation of further

- Bloomberg reported that Tesla needs to fix its so-called Full Self-Driving Beta system in hundreds of thousands of cars after United States authorities said the company’s automated-driving technology could increase the risk of a crash. Tesla is expected to fix the issue through an over-the-air software update by April 15. It will impact 362,758 vehicles including certain Model 3, Model X, Model Y and Model S units manufactured between 2016 and 2023.

- Home loan applications fell 7.7% week-over-week as the 30-year mortgage rate increased 21 basis points to 6.39%, according to data from MBA’s Market Composite Index. This represents a deceleration in American economic activity and could be a sign of an upcoming recession that has been predicted by a handful of economists.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was coffee, rising 6.36%, likely on the news that the Arabic coffee growing regions of Brazil are contending with poor weather conditions that are delaying fertilization and pesticide applications. JPMorgan’s Global E&P Capex survey is now in its 20th year. In line with its previously published initial outlook, the bank sees global upstream capex up 12% year-over-year in 2023. This means the third consecutive year of low double-digit spending growth, and although capex is still 5% below 2019 levels, it is up $80 billion from the lows.

- Kinder Morgan Inc.’s El Paso Line 2000 natural gas pipeline to California has finally completed repairs and passed inspections; it came back online in the past week after being out of service over the past 18 months. This is good news for Texas natural gas producers as they will be able to sell into this more lucrative market.

- The Freeport liquefied natural gas (LNG) plant in Texas took an incremental step toward resuming full operations, exporting a shipment of fuel from storage for the first time since a June explosion. BP Plc’s Kmarin Diamond vessel departed the facility and is heading to the Suez Canal, according to ship-tracking data compiled by Bloomberg.

Weaknesses

- The worst performing commodity for the week was natural gas, dropping 9.55% to a 28-month low, as reported by Bloomberg. U.S. natural gas consumption was down 7% year-over-year this past week, driven by lower residential/commercial demand and slightly offset by higher industrial demand. Total demand was down 11% this week on the back of lower residential/commercial demand, power demand, and industrial demand.

- Copper and most other industrial metals wavered this week on little pickup in demand from China, reported Bloomberg. Copper still held a small gain for the week, but aluminum, lead, molybdenum, and nickel were all down for the week. Copper is being supported by the potential for supply disruptions in Panama while Freeport-McMoRan’s operations at their Grasberg have been curtailed due to recent heavy rains that have flooded infrastructure near their milling complex.

- The U.S. refining sector faces one of the heaviest turnaround seasons of the last five years in the first half of 2023. Ahead of what may be the first normal U.S. driving season since the Covid outbreak, and since the loss of the largest refinery on the U.S. East Coast (Philadelphia Energy Solutions, 2019) underlining a U.S. marketincrementally more dependent on imports so prices are likely to stay high.

Opportunities

- Goldman still sees the China comeback as the most persistent driver of the oil outlook. The 1.1 million barrels per day rise in China demand this year (Q4/Q4) should push oil markets back into deficit in June, expose structural underinvestment, boost prices, and lead OPEC to reverse its November 2022 production cut in the second half of 2023.

- According to Goldman, if China’s growth accelerates meaningfully into the second quarter, as its economists expect, then the resultant micro signals – tightening arbs, drawing inventories, downstream demand – would form the basis for the next leg higher in industrial metals. Set against already-low inventories and associated full-year metal deficits, this environment should provide strong price support, particularly for aluminum, copper, and iron ore.

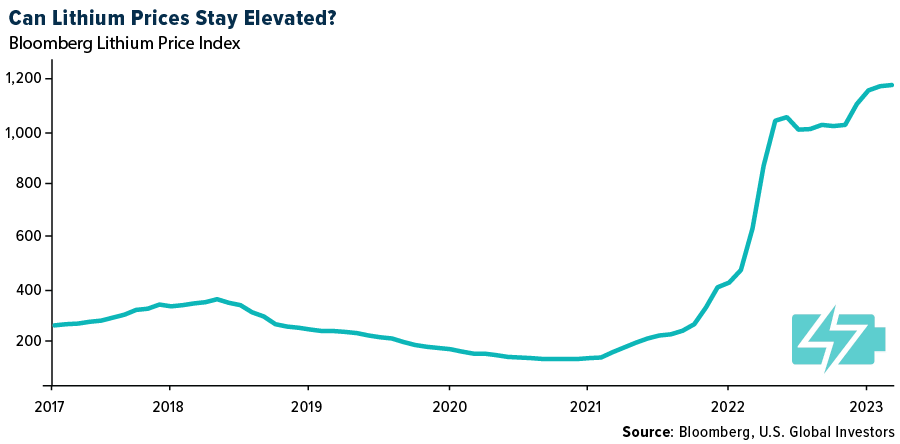

- In the U.S., January 2023 saw lithium demand could have a 20% CAGR while supply could have a 16% CAGR. By 2030, there could be a 603,000-ton deficit. This week LG Chem agreed to invest $75 million in the common shares of Piedmont Lithium to secure 200,000 metric tons of spodumene concentrate over four years.

Threats

- The International Energy Agency (IEA) calculated that spending by governments in 2022 reached $1 trillion last year to subsidize oil, natural gas, electricity, and coal as prices soared last year with the disruption of supply chains in the energy sector. The subsidies helped shield consumers from soaring energy prices, particularly in Europe.

- Glencore Plc said it is willing to hold back its cobalt supplies to try and support the price of the battery input which has fallen more than 50% since its peak in May, as reported by Bloomberg. Glencore, the largest supplier of cobalt to the market, noted automotive demand is still rising but that the Chinese electronics sector has shown a sharp drop-off in demand. Cobalt prices may still face further pressure to drop with a more expanded footprint in North America with the announcement by Ford this week to build a lithium-iron-phosphate (LFP) battery plant in Michigan. LFP batteries are cheaper to manufacture and don’t require the more expensive metals, such as nickel and cobalt, as input components.

- The IEA noted that Russian oil exports approached an all-time high last month with shipments reaching 8.2 million barrels per day in January. However, revenues from exports for January fell by more than a third to $13 billion from a year ago, due to international price caps imposed on the sales of Russian crude due to their invasion of Ukraine.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Filecoin, rising 57.38%.

- Bitcoin rallied to $25,000 for the first time since August on Thursday, rising to as much as 4.4% after falling 64% in 2022.

- MetaMask developer ConsenSys has teamed up with the global payments platform Mercuryo to streamline the process of purchasing cryptocurrencies directly from the web3 wallet, writes Bloomberg, using bank cards, Apple pay and Google Pay.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Pax Gold, down 1.23%.

- Crypto exchange Binance had secret access to a bank account belonging to (what it has said is) an independent U.S. digital-asset marketplace Binance.US. and transferred large sums of money to a trading firm managed by Binance CEO CZ. Over the first three months of 2021, more than $400 million flowed from a Binance.US account at Silvergate Bank to CZ’s trading firm Merti Peak, writes Bloomberg.

- Hedge funds, private equity firms, and pension funds could have a tougher time working with many crypto firms under a draft proposal from a top U.S. regulator, reports Bloomberg. Rule changes that the SEC plans to propose on Wednesday would effectively make it harder for crypto firms to be “qualified custodians,” the article explains.

Opportunities

- Taurus SA, a Swiss firm developing market infrastructure for digital assets, has raised $65 million in an equity round led by Credit Suisse Group AG, as bigger financial institutions push on with projects despite the prolonged crypto winter. Deutsche Bank AG, Pictet Group, Arab Bank Switzerland and Investis Holding also took part in the funding, according to Bloomberg.

- As the crypto industry spiraled from the fallout of FTX and regulators began closing in, one corner of the sprawling market saw an influx of demand from institutional investors, writes Bloomberg. The CME Group’s average daily trading volume in its crypto futures products rose a record 13% in 2022 to 53,600 contracts.

- Sony Network Communication has teamed up with multichain smart contract network Astar Network to launch a web3 incubation program for projects that focus on the utility of NFTs and decentralized autonomous organizations, according to an article published by Bloomberg.

Threats

- The native token of Binance, the largest crypto exchange, extended declines on Monday amid uncertainty over the platform’s outlook. Binance Coin dropped as much as 8.9%, the lowest level since mid-January, writes Bloomberg.

- The U.S. SEC is preparing to sue the company behind TerraUSD, a crypto stablecoin whose collapse last year kicked off an industry-wide crisis and cascade of high-profile bankruptcies. The SEC has been investigating whether Terraform Labs misled investors about the coin’s ability to maintain a 1-to-1 peg to the U.S. dollar, writes Bloomberg.

- The regulatory crackdown on cryptocurrencies is proving a boon for a token that’s located outside the U.S. and being scrutinized over the transparency of its reserves, writes Bloomberg. USDT increased its market share by about $1 billion in the past 24 hours alone, as some traders move their holdings out of rivals following a series of enforcement drives by financial watchdogs in the U.S.

Gold Market

This week gold futures closed at $1,851.80, down $22.70 per ounce, or 1.21%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.47%. The S&P/TSX Venture Index came in up 0.23%. The U.S. Trade-Weighted Dollar rose 0.23%.

Strengths

- The best performing precious metal for the week was gold, but still off 1.21%. Barrick Gold’s overall attributable gold reserves increased 10% to 76 million ounces. Operating reserves (excluding the 12 million ounces relating to the Norte Abierto project) increased 12% to 64 million ounces from 57 million ounces at year end.

- B2Gold announced the acquisition of Sabina Gold & Silver Corp (SBB) in an all-stock transaction. B2Gold expects to issue 0.3867 of a common share of B2Gold for each Sabina common share, representing consideration of C$1.87 (18% premium) for a total value of approximately C$1.1 billion.

- Superior Gold has begun releasing monthly operational reports with today’s announcement highlighting strong improvement at Plutonic in January. Compared to the fourth quarter 2022 monthly average, Superior achieved a 47% increase in underground production and a 12% reduction in underground costs per ton in the month of January.

Weaknesses

- The worst performing precious metal for the week was platinum, down 3.32%. Gold erased losses as the dollar weakened after U.S. data highlighted persistent inflation that could push the Federal Reserve to pursue further interest-rate increases in the months ahead, writes Bloomberg. U.S. producer prices rebounded in January more than expected, the article continues, with the index for final demand jumping 0.7% last month.

- Pan African Resources indicated that the headline earnings per share (EPS) for the period is expected to be between $1.40-1.64 per share versus consensus of $1.71 per share. The lower earnings seem to be primarily driven by lower gold sales and a marginally lower realized gold price. The company has not disclosed costs, which could be potentially higher than consensus.

- Burkina Faso exercised an option in their mining code to directly purchase 200 kilograms of gold from a mine owned by Endeavour Mining Plc. Endeavour’s share price initially dropped on the news confirming it had sold the gold under contract at current market prices which would equate to about $11.8 million of value in the transaction. Almost the entire western half of Burkina Faso is under militant control, and the government may have had an urgent need for liquidity.

Opportunities

- Goldman Sachs Group Inc. expects central banks to buy an unprecedented amount of gold in 2023 as some look to diversify their reserves away from the dollar, reports Bloomberg. Jeff Currie noted their target is 1,200 tons for central bank buying, surpassing last year’s purchases. Last year’s purchasers were largely unidentified, but China recently started reporting monthly purchases after a three-year window of silence.

- JPMorgan is marking its price forecasts to market and embedded the latest JPMorgan base case for falling U.S. real yields and a largely neutral U.S. dollar. The bank has upgraded its 2023 gold and silver price forecasts by around 10%. JPMorgan reaffirms its bullish bias on both metals and now forecasts gold prices will continue to rise over the course of the year to an average $2,045 per ounce in the fourth quarter of 2023, with silver prices rising to an average of $26.6 per ounce.

- According to Canaccord, despite the recent pullback following the strong January payrolls data, gold is up 2% year-to-date, and the S&P/TSX Gold Index is up 3%. Under the surface, however, Canaccord sees more robust performance led by the junior producers (+9.7% median) and intermediates (+6.1%) versus the senior producers (+1.5%). The group notes that approximately a third of its coverage universe has posted double-digit gains for the year so far.

Threats

- The government watchdog for the Democratic Republic of the Congo has called for a major overhaul of the country’s $6.2 billion minerals-for-infrastructure deal with China upon finding significant breaches of the 2008 agreement, as reported by Bloomberg. The General Inspectorate of Finance called for the value of the investment in infrastructure to be raised to at least $20 billion, considering the value of the mineral deposits transferred to Chinese ownership. China’s embassy in Congo released a statement saying the claims cannot be considered creditable and have no constructive value.

- Mark Bristow, CEO of Barrick Gold, opined that inflation is going to be sticking around to hobble the industry for a while longer, as reported by Bloomberg. Rising costs impacted almost every miner that was reported over the past weeks. Bristow did not view the Fed’s actions as sufficient to stop the rise in inflation under current conditions.

- Newmont Mining’s growth options could get a lot more expensive. The Newcrest Mining Board announced that it has unanimously rejected the Newmont offer (announced on February 6), as it does not represent sufficient value for Newcrest shareholders. The Board has indicated to Newmont that it is prepared to provide access to limited, non-public information on a non-exclusive basis subject to certain conditions, including the signing of an appropriate non-disclosure agreement.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

Barrick Gold

Newmont

Superior Gold

Victoria Gold

Bombardier

Azul SA

Boeing Co/The

Airbus SE

United Airlines

JetBlue Airways Corp.

American Airlines

Hawaiian Holdings

LVMH Moet Hennessy

Cie Financiere Richemont

Kering SA

Tesla Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P/TSX Global Gold Index is designed to provide an investable index of global gold securities.

The Relative Strength Index (RSI) is a momentum indicator that measures the magnitude of recent price changes to analyze overbought or oversold conditions.

The U.S. Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All