Your CBDC Survival Guide

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsNigeria may not be on a lot of people’s radars, but it should be. Africa’s largest economy is in the early stages of a monetary experiment that could be coming to the U.S. sooner than you think.

In October 2021, Nigeria’s central bank introduced the eNaira, a digital version of its currency, the naira, and so far, things aren’t going well. Nigerians aren’t using the currency, for one.

And two, the central bank has recently replaced old high-denomination banknotes with new, less counterfeitable ones. As you might expect, this has triggered a chaotic run on the banks. Cash withdrawals are reportedly limited to around $45 USD per day.

Some people believe the crisis has been engineered to push people into using the eNaira. True or not, the country isn’t giving up on the currency. Nigeria, which is holding a highly contested presidential election on Saturday, entered into talks this week with a New York-based technology firm to help it “keep full control” of the eNaira, according to reporting by Bloomberg.

I’ve written about the pros and cons of central bank digital currencies (CBDCs) before, and I think by now most people have developed their own opinion about them.

The thing is, CBDCs are not just for emerging and developing countries like Nigeria. Close to 90% of the world’s central banks are at some point in the process of creating their own digital currency. Sweden, already one of the most cashless societies (despite it being the first country in history to issue paper banknotes), may be close to rolling out the e-krona.

Not everyone favors the idea of a centralized digital currency, and a few nations are working on legislation limiting their scope. Switzerland, whose citizens hold the most physical cash per capita, wants to enshrine the availability of paper banknotes in its constitution. This week, a U.S. legislator introduced a bill, titled the “CBDC Anti-Surveillance State Act,” that would prohibit the Federal Reserve from issuing its own digital dollar.

It’s All About The Benjamins

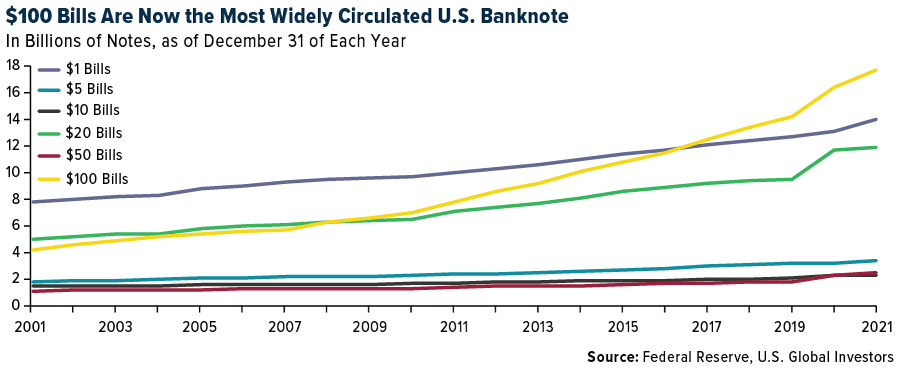

Even among those who may not support the creation of a CBDC, the calls to ban certain banknotes have been growing louder over the years. The U.S. has rightfully done away with bills ranging in denomination from $500 and $100,000, and the next on the chopping block could be the $100 bill.

Supporters of this idea say that discontinuing bills bearing Ben Franklin’s face would go a long way in combating corruption, terrorism and other illicit activities, particularly overseas. Believe it or not, a vast majority of $100 bills are held abroad—an estimated 80% of them, according to the Chicago Fed.

Demand rises in times of political and financial crisis.

With Benjamins now being the most printed U.S. currency, having overtaken both the $20 bill and $1 bill in recent years, the amount of money that exists outside the American financial system is substantial.

I don’t know what the solution to this is, but eliminating the $100 bill seems extreme to me. What would that do to the value of the U.S. dollar? How would that affect people’s faith in our monetary system? We see what’s happening in Nigeria.

Similarly, I don’t believe CBDCs are the solution. Unlike Bitcoin, CBDCs are by definition centralized. They’re also traceable and programmable, with potentially chilling consequences.

In Gold We Trust

This only improves the investment thesis for gold, silver, collectibles, real estate and other hard assets. Although not as liquid or portable as cash, hard assets are attractive stores of value because they’re private property, not issued by a central authority.

The same goes for Bitcoin, gold’s digital cousin. The only way to produce a new Bitcoin or new ounce of gold is through intensive work, a literal conversion of time and energy. No central banker or finance minister can unilaterally affect supply with a snap of their fingers.

It’s for this reason that central banks like gold. They collectively bought a near-record amount of the yellow metal last year, and some analysts forecast they’ll buy even more this year.

Could Bitcoin end up on banks’ balance sheets? It’s not as crazy as it sounds. In December 2022, the Bank of International Settlements (BIS), often called the “central bank of central banks,” released guidance on banks’ exposure to crypto assets. The standard, which goes into effect in 2025, limits that exposure to 2%.

American Exceptionalism

I want to leave you with something that was shared with me recently. Last month I attended Harvard Business School Case Studies, where I finally received my MBA after several years of attending. (I like to joke that I’m a slow learner.)

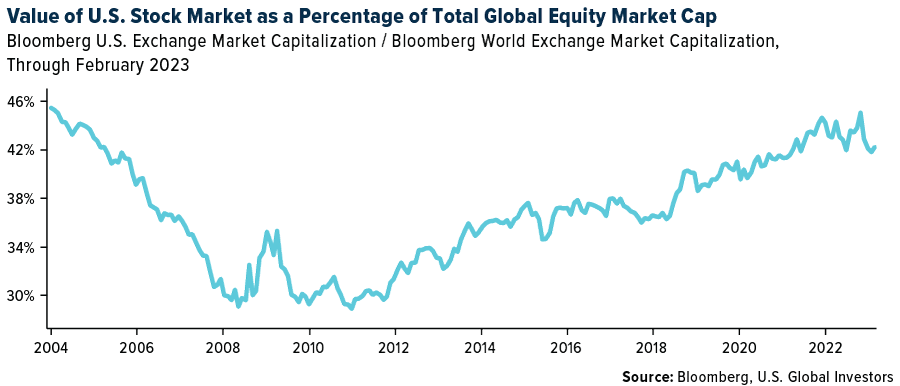

Larry Summers—former Treasury Secretary and current President Emeritus of Harvard—reminded us how remarkable it is that the total market cap of U.S. stocks represents over 40% of total world equities.

This is true despite the U.S. economy representing around 16% of global GDP and its population representing less than 5% of the world’s population.

Summers’ words reinforce my belief that it’s unwise to bet against the U.S., no matter who’s in charge or what else is going on in the world. American exceptionalism is much more than a pie-in-the-sky concept—it’s apparent in the strength of our institutions and capital markets.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.99%. The S&P 500 Stock Index fell 2.71%, while the Nasdaq Composite fell 3.33%. The Russell 2000 small capitalization index lost 2.92% this week.

- The Hang Seng Composite lost 3.14% this week; while Taiwan was up 0.16% and the KOSPI fell 1.13%.

- The 10-year Treasury bond yield rose 12 basis points to 3.948%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Bombardier, up 2.9%. Air France reported late last week its highest-ever fourth quarter 2022 revenue results, according to the company’s release, in addition to full-year guidance now standing at $28 billion. Full-year net profits now stand at $774 million, while operating profits came in at $1.2 billion. This makes it the most profitable year for the company since the pandemic.

- VLCC tanker rates have firmed in the past week with China returning from holiday driving robust Middle East loadings. Looking to the second quarter of this year, there may be more U.S. strategic reserve releases. This supports an increase in U.S. crude exports through the second quarter (helping to offset seasonal headwinds from refinery maintenance). The crude tanker orderbook remains extremely low at 4% which, combined with recovering crude tanker flows on China reopening, should support robust rates particularly into the second half of 2023.

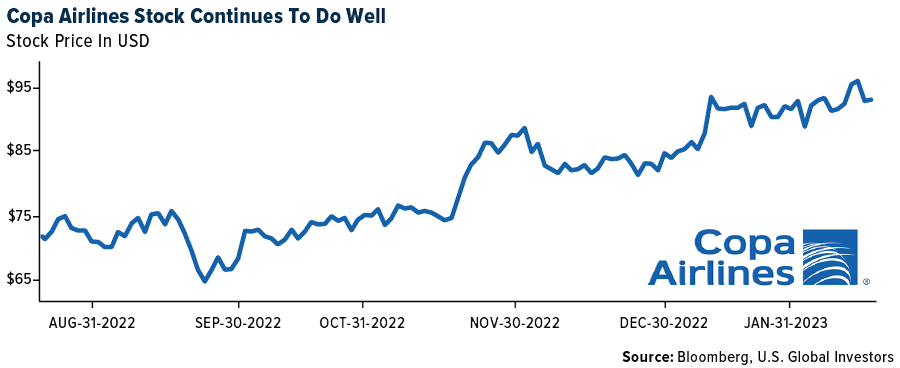

- Copa Holdings recently posted an impressive fourth-quarter beat with earnings per share (EPS) of $4.49, coming in above consensus of $4.03. The company’s preliminary 2023 guide implies $12.20 EPS at the mid-point, which is 13% above consensus.

Weaknesses

- The worst performing airline stock for the week was Wizz Air, down 9.3%. Air Canada’s fourth quarter 2022 EBITDA of $389 million was below consensus of $500 million, largely due to higher-than-expected ex-fuel CASM. While revenues and RASM were generally in line with consensus, ex-fuel CASM (unit cost) was 14.1% higher than consensus. The cost pressure seems broad-based with most cost items coming in higher than expected, particularly labor.

- Air volume was down 15.8% year-over-year, while Seafreight was down 6.7%. Compared to 2019, air volume was down 9.3%, whereas Sea was 0.2% lower. These compare to “normal” growth levels of 3-4% CAGR, indicating that demand is currently below trend, particularly in Air. Transpacific had generally been the strongest lane for both Air and Sea volume, though container imports into the U.S. are now down 20% year-over-year.

- United Airlines has delayed plans to add extra U.S.-China flights by at least six months, according to a person with knowledge of the matter, as the two nations remain deadlocked over lifting Covid flight caps. The increase in flights was originally slated to start late next month, but the move was postponed over the weekend, said the person, who isn’t authorized to speak because the matter is private. The airline has started to inform affected passengers, they added.

Opportunities

- Airline markets are continuing to tighten. Over the past month the highest downward capacity revisions for March/April have been for Ryanair (4-5%) while for European-listed airports the highest capacity decrease has been for Fraport (5%). Transatlantic passenger capacity is now 98% of pre-Covid levels. Passenger capacity for Asia shows China-Europe/U.S. capacity is 20-40% of 2019 levels.

- Today, rates are down from extraordinarily high levels but have not dipped into $500 per container price-war territory. Instead, rates fluctuate at $2,000 per container. With this background, Maersk doesn’t expect profitability in the Ocean division to collapse once the high contracted rates of the 2021/2022 contracting season roll off. Here, contract rates are expected to converge toward spot or a small premium in the 2022/2023 contracting season. Maersk stressed that there may be volatility in Ocean earnings on a quarterly basis but reiterated the “no-collapse” scenario several times.

- Air traffic continues to recover in other parts of Asia. Singapore Airlines’ traffic has increased to 90% of 2019 levels in January. Japan’s domestic traffic was at 80% of 2019 levels in December while timetabled seats data shows a rapid addition of inbound seats in the coming quarters, led by flights from Vietnam, Canada, and Australia. In addition, Taiwan’s traffic has already recovered to 70%+ of 2019 levels and Cathay Pacific at almost 40% of 2019 levels in January.

Threats

- Recent dramatic spikes in physical jet fuel prices to almost $250 per barrel reflect scarcity still present in refined product markets. This stands in stark contrast to crude markets, which have remained range-bound so far this year, as physical sponsorship confirming the large increase in China demand, and the corresponding deficits, need to be confirmed.

- For shipping, the supply side will also become more challenging in 2023-24, with the orderbook now at 28% of the fleet. On main trade lanes, capacity operated looks 12% lower than peak, due to capacity management by the carriers. There has been increasing usage of slow steaming across the industry in recent months.

- Daily website visits for European Union airlines decreased by 3 points to -6% versus 2019 levels on a seven-day trailing basis, in the week. Wizz Air cut 3 points of capacity from first quarter 2023 schedules, while Lufthansa and Wizz added 1 point each to second quarter 2023 schedules.

Luxury Goods And International Markets

Strengths

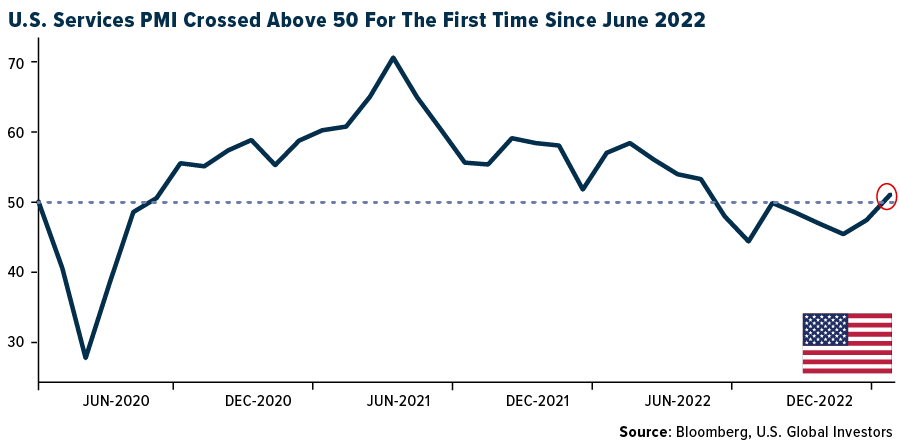

- S&P Global’s U.S. Services PMI increased in February. The PMI reading came in at 50.5 versus 46.8 in the previous month, and above consensus of 47.3. A reading above the 50 level indicates a positive development in the service sector, which also supports the luxury goods industry. The U.S. Services PMI crossed above this level for the first time in the last eight months.

- According to a report released by the Business of Fashion, “Fashion in the Middle East: Optimism and Transformation,” $89 billion of the fashion industry is represented in this region, where 50% of high earners spend more than $1,000 a month on high-end luxury goods. The industry in this region is changing in the upcoming year because of shifting consumer behaviors, especially among Gen-Z’ers. This is thanks to new government policies, including more females as part of the labor force, as well as the region starting to be considered a world-class tourist destination. The Middle East’s fashion industry is expected to grow 7% in the next five years, according to Euromonitor International.

- Sleep Number Corporation was the best performing S&P Global Luxury stock for the week, gaining 14%. Shares gained almost 13% on Thursday after the company reported fourth quarter results and said it is experiencing early signs of improvement in business. Wedbush analyst Seth Basham maintained a “neutral” rating for Sleep Number but upped the stock price target from $27 to $37 per share.

Weaknesses

- According to Bloomberg, the S&P Global Eurozone Manufacturing PMI was reported for February at 48.5 versus 48.8 in January, and below consensus of 50.7. The data represents a slight decrease in economic activity in the Eurozone (particularly because this leading indicator is under the 50 level – indicating contraction zone).

- Economic growth in the United States in the fourth quarter was weaker than previously estimated, primarily due to weaker consumer spending. Household expenditures increased an annualized rate of 1.4% in the fourth quarter of last year, not 2.1% as previously estimated. The U.S. economy grew by 2.7% in the last three months of 2022 versus the previously reported 2.9%.

- Lucid Group, an electric car maker and distributor, was the worst performing S&P Global Luxury stock for the week, losing 23.3%. Shares sold off after the company reported worse-than-expected results in the fourth quarter of last year and provided weaker guidance for 2023.

Opportunities

- Lidar maker Luminar said on Wednesday that Mercedes-Benz will incorporate its sensors and software in a “broad range” of vehicles starting mid-decade, reports CNBC. This is a significant expansion of an ongoing partnership between the two companies. Under the expanded deal, Mercedes-Benz will incorporate the next version of Luminar’s Iris lidar into an upcoming partially automated driving system that will be made available on many future Mercedes models, the article explains.

- According to an article from Business of Fashion, luxury brands have started to use augmented reality (AR) as a sales driver. Based on the article, Cartier launched a new campaign using AR on Snapchat, showing the history of its first watch designed by Louis Cartier in 1917, the Tank Watch. By simply moving around their phone, users can travel to the Alexander III Bridge in Paris in 1917, then jump to 1977, and finally to 2023 to virtually try on the last version of the watch launched last month.

- Yields continue to move higher in the United States pushing the U.S. dollar upward. Once again, luxury stores in Europe could see increased traffic from Americans, as consumers will be more willing to travel abroad to purchase high-end products for less.

Threats

- According to the PwC Global Consumer Insights Pulse Survey released this week, which took responses from 25 countries worldwide, including the U.S. and China (both leading luxury markets), 96% of respondents have intentions of applying cost-saving measures in the next six months. This could impact the luxury industry because 53% of people said they will spend less on designer products and fashion items even though the PwC´s Mainland China and Hong Kong Luxury Market Report said that China´s luxury market will generate revenue of $119.6 billion in 2025.

- Durable goods in the U.S., which measures the cost of orders received by manufacturers of goods meant to last at least three years, is expected to decrease dramatically from 5.6% in December 2022 to -3.7% in January. This would represent a decrease of 166%.

- This week, U.S. President Joe Biden visited central emerging Europe. He traveled to Poland and visited Kiev to meet with the President of Ukraine, Zelensky. The war in Europe started a year ago (February 24, 2022) and there are still no signs of peace negotiations. A high-level Chinese diplomat was also visiting Russia this week. Perhaps this is a coincident that President Biden was visiting CEE and China was talking to Putin in the same time period. There is a growing speculation that China is providing support for Russia’s war in Ukraine.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was natural gas futures, rising 7.74%, after hitting 28-month lows in the prior week. Headlines of the bargain pricing prompted India, China, and several smaller Asian countries to contract for spot market prices of natural gas this week, reports Bloomberg.

- Lithium producers in Australia are bucking the trend of major miners showing some weakness. Profits surged more than 10-fold for Pilbara Minerals Ltd. and Allkem Ltd. in 2022 versus the prior year, as reported by Bloomberg.

- According to Goldman Sachs, iron ore has outperformed the rest of the metals complex this past quarter, rallying 50% from its October trough of $78 per ton. While part of this move has been driven by the shift in positioning, due to China’s reopening, it has been reinforced by a pocket of tightness onshore, in contrast to copper and aluminum.

Weaknesses

- The worst performing commodity for the week was wheat, dropping 7.31%, to its lowest level in a month as the U.S. Department of Agriculture forecast that U.S. farmers may plant 49.5 million acres of grain, higher than market expectations.

- According to CIBC, in the copper market after significant anticipation of a demand recovery with the China re-opening, initial statistics point toward weak demand as inventory continues to stockpile, currently up 250% year to date.

- In the paper market, industrial action across Finnish logistics sectors continued on as negotiations between unions and employer associations failed. UPM, in order to manage these impacts, has increased storage capacity outside the ports and raised inventories outside Finland.

Opportunities

- According to Bank of America, Europe’s Big Oil names have paid out a total of $75 billion in shareholder distributions in 2022. Improving shareholder generosity epitomizes one of the sector’s key signposts on its “redemption roadmap.” Yet, CFFO payout ratios are still low by historical standards – averaging around 30% in 2022 and in the bank’s view, will approach 40% as commodity prices provide more headwinds this year.

- Shell presented its annual LNG outlook this week, with a summary of 2022 developments and the market’s evolution. The company unsurprisingly forecasts a tight global LNG market in the near term because of the loss of Russian gas supply and it expects the supply gap to persist. Particularly in Europe, Shell sees a supply gap of 140 tons to be met by LNG imports.

- Pioneer Natural Resources CEO expects global oil prices to climb to more than $100 by the end of the year, as reported by Bloomberg. China’s pick up in growth and the slow down in supply growth in the U.S. will lead to tighter markets. Oil drillers in the Permian Basin are delaying their drilling programs due to local pipelines that are full to the brim. Southwest Energy Co. is also joining the list of natural gas producers slowing down on their drilling, as prices for heating and power generation fuel plunge. Fortunately, Chenier Energy Inc., the largest LNG exporter, has initiated the permitting process for a major expansion of its Sabine Pass terminal in Texas to bring more land stranded gas to international markets.

Threats

- The EIA reported a 100 Bcf storage withdrawal, which compares to the five-year average draw of 150 Bcf and last year’s 190 Bcf withdrawal. Gas storage is now at 2.3 trillion cubic feet, which is 6% above the five-year average and 19% above prior year levels. This should support falling natural gas prices.

- The underlying underinvestment in refining – exacerbated by closures and disruptions – remains unresolved. In fact, despite a large increase in refining capacity this year, persistent delays and upward revisions to the demand path mean higher utilization rates over 2023 and 2024-25 to 84.7% and 84.5%, respectively.

- Why has aluminum underperformed versus major industrial metals in 2023? UBS has some ideas, including: 1) energy cost deflation has shifted supply risks from cuts to reactivation in Europe; 2) material build in LME inventory in February and stronger than “usual” seasonal inventory builds in China; 3) lackluster demand.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Stacks, rising 114.41%.

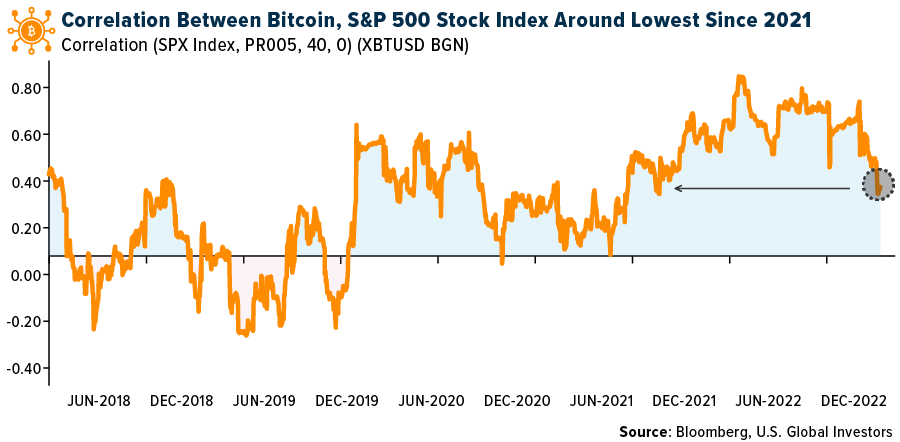

- Bitcoin’s year-to-date gain has now reached 50% after a further jump in February, reports Bloomberg, contrasting with a retreat in global equities this month courtesy of a macroeconomic environment replete with growth and inflation concerns. This divergence has dented a positive correlation between shares and crypto that sprouted during the pandemic.

- Music streaming service Spotify is testing a new service called “token-enabled playlists,” reports Bloomberg, which allows holders of NFTs to connect their wallets and listen to curated music.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Fantom, down 17.14%.

- Liquidators of bankrupt hedge fund Three Arrows Capital said they will take steps to sell some of the firm’s NFTs as part of their recovery efforts, reports Bloomberg. The document did not provide details of the NFTs up for sale but clarified that these do not include the popular “Starry Night” portfolio, the article continues.

- Coinbase Global Inc., which laid off staffers twice in the last year, could be cutting more if it becomes necessary, CFO Alesia Haas said. This would be to improve the company’s financial performance, according to Bloomberg.

Opportunities

- Nigeria is in talks with potential technology partners to develop a new system to run and manage its central bank digital currency, the eNaira. The central bank of Nigeria wants to develop its own software for the digital currency so that it can keep full control of the effort, Bloomberg explains. They are currently in talks with New York-based tech firm R3.

- Coinbase Global is launching a blockchain, expanding the largest U.S. cryptocurrency exchange’s reach deeper into the world of decentralized finance and nonfungible tokens. Coinbase has been introducing new products and services to lessen its dependence on retail-driven trading revenue, writes Bloomberg.

- Bitcoin is on pace for its second monthly advance, reports Bloomberg, breaking with stocks and other riskier assets that have slid amid renewed concern about rising interest rates. Bitcoin has advanced more than 4% so far in February.

Threats

- California lawmakers, on Wednesday, expressed frustration with how Governor Gavin Newsom’s administration has tackled cryptocurrency regulations, arguing for the need of state legislation to help further rein in the industry. At hearings, two panels asked for information from the state Department of Financial Protection and Innovation on its efforts to protect consumers, writes Bloomberg.

- A fresh indictment of FTX co-founder Sam Bankman-Fried features a pair of co-conspirators the U.S. says helped illegally seek to influence the regulation of cryptocurrency by donating millions of dollars to both the Democratic and Republican parties. The U.S. didn’t identify the co-conspirators in the indictment nor has either been charged, writes Bloomberg.

- The top U.S. banking regulators stepped up their warnings to banks on the liquidity risk tied to stablecoin-related reserves and other funding sources from crypto firms, writes Bloomberg. The three watchdogs pointed to deposits that include stablecoin-related reserves as notably susceptible to unpredictable, large, and rapid outflows in crypto markets.

Gold Market

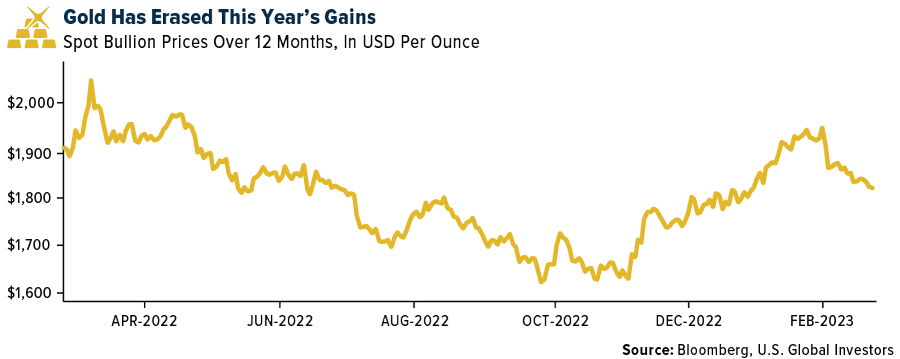

This week gold futures closed at $1,817.90, down $32.30 per ounce, or 1.75%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.89%. The S&P/TSX Venture Index came in off just 1.74%. The U.S. Trade-Weighted Dollar rose 1.32%.

Strengths

- The best performing precious metal for the week was platinum, but still down 1.20%. Dundee Precious Metals reported fourth-quarter earnings per share (EPS) of $0.18, above consensus of $0.14. The beat to consensus was driven by a combination of lower-than-expected costs in the quarter as well as higher revenue, driven by higher realized metal prices, which averaged $1,752 per ounce gold and $3.65 per pound copper in the quarter.

- Northern Star announced an $0.11 per share interim dividend, representing 27% of cash earnings and a slight increase from the $0.10 per share dividend in the first half of fiscal year 2022. With the payment of this dividend on March 29, 2023, Northern Star will have paid approximately A$1.1 billion back to shareholders since fiscal year 2012, demonstrating its commitment to returning capital to its shareholders.

- Newmont, the world’s top gold miner, announced this week that in 2022, the company produced 6 million gold ounces and 1.3 million gold equivalent ounces from other metals, reports Kitco News. This means the company achieved its original production guidance range set in December 2021.

Weaknesses

- The worst performing precious metal for the week was palladium, down 7.10%. Overall, investors are likely to view Agnico Eagle’s recent fourth quarter 2022 release as disappointing. While the quarterly results were a slight miss versus consensus, largely on higher costs, the company’s 2023 and 2024 gold production guidance is 6% below consensus and below its previous guidance.

- Sibanye Stillwater released a trading statement guiding to a 46%-51% decline year-over-year in its fiscal 2022 earnings per share, to between R6.19 and R6.84, missing consensus EPS by 29% (based on the midpoint of its guided range). Management highlighted that the company’s earnings were negatively impacted by the industrial action related to wage negotiations in the South African gold sector and severe weather at the U.S. PGM operations, which resulted in a seven-week shutdown.

- Pan American Silver reported fourth-quarter adjusted EPS of negative $0.02, below consensus of $0.05. The earnings miss to consensus was driven by higher-than-expected taxes, depreciation and expensed exploration in the quarter. Pan American expects the closing of the Yamana transaction later in the first quarter, subject to the receipt of approval from the Mexican Federal Economic Competition Commission.

Opportunities

- Management reiterated that Royal Gold’s main priority is to allocate cash for acquisitions that add value for shareholders and increase cash value from 1x NAV to over 2x NAV. The current pipeline for M&A transactions is primarily for gold assets; however, the company is also looking at assets with precious metals by-products as these have the potential for longer mine lives.

- According to JPMorgan, Northam Star Resources’ underlying net profits after taxes (NPAT) of $55 million came in 5% better than its estimate on lower D&A (underlying EBITDA was a miss). The dividend of $0.11 per share represented a solid 27% cash earnings payout. Over the next 18 months, NST will realize tax synergies from the merger with Saracen.

- Resource Capital Funds announced plans to raise $250 million for a new fund to invest in mining companies as it sees a shortage of capital deployed to active money managers to back up and coming mining companies and new sector opportunities. A predecessor fund dedicated to the same strategy wrapped up in 2018 with $106.3 million. The firm invested that fund across 38 deals, with 15 exits as of last September, and says the vehicle has so far produced a net internal rate of return of 20.9% and returned 1.6 times invested capital. Smart money is coming back for another opportunity to profit.

Threats

- As reported by Bloomberg, gold extended its decline to the lowest level this year as traders assessed the Federal Reserve’s interest-rate path. “Gold remains anchored as investors anticipate the market is getting close to agreeing on how high the Fed will take rates,” said Ed Moya, senior market analyst at Oanda. “The risk that the Fed could do more is elevated” after the data prints. “That should prevent gold from mustering up any significant rallies” until next month’s jobs and inflation data releases.

- Sibanye Stillwater management has cited the following as its rationale in acquiring New Century: 1) concerns about current New Century management and the change in the strategic direction, diverting focus away from its tailings reprocessing business; 2) consideration that New Century’s balance sheet may struggle with the repayment of its A$180M environmental bond facility and potential project funding requirements for Silver King and Mt Lyell, in addition to general low shareholder liquidity.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

Dundee Precious Metals

Northern Star Resources

Newmont Corp

Agnico Eagle Mines

Sibanye Stillwater

Yamana Gold

Air France-KLM

Copa Holdings

Air Canada

United Airlines

Ryanair Holdings

AP Moeller Maersk

Singapore Airlines

Cathay Pacific

Deutsche Lufthansa

Wizz Air Holdings

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All