Over the past few decades, investors have become conditioned to expect that rising interest rates will trigger broader US financial market crises. There’s history to support this view: the savings and loan crisis of the late 1980s and early 1990s, the mid-1990s Mexican peso crisis (as well as Orange County, California’s default), the bursting of the tech bubble and the housing-market meltdown 15 years ago.

Each of those episodes was preceded by Federal Reserve policy-tightening cycles. Yet despite a very fast—and very aggressive—policy-tightening cycle over the past year, financial markets continue to function well today. Does it make sense for investors to worry that the other shoe will eventually drop and produce a bigger downward spiral?

We don’t think so.

Excess Leverage: Tinder for Past Crises

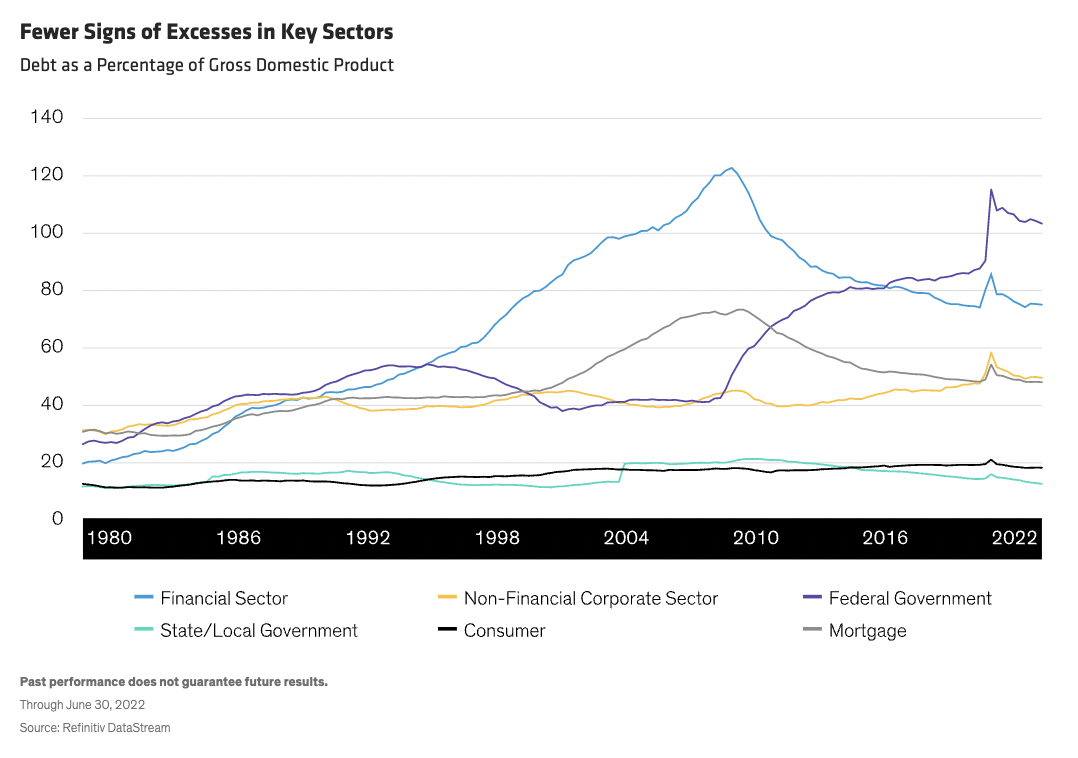

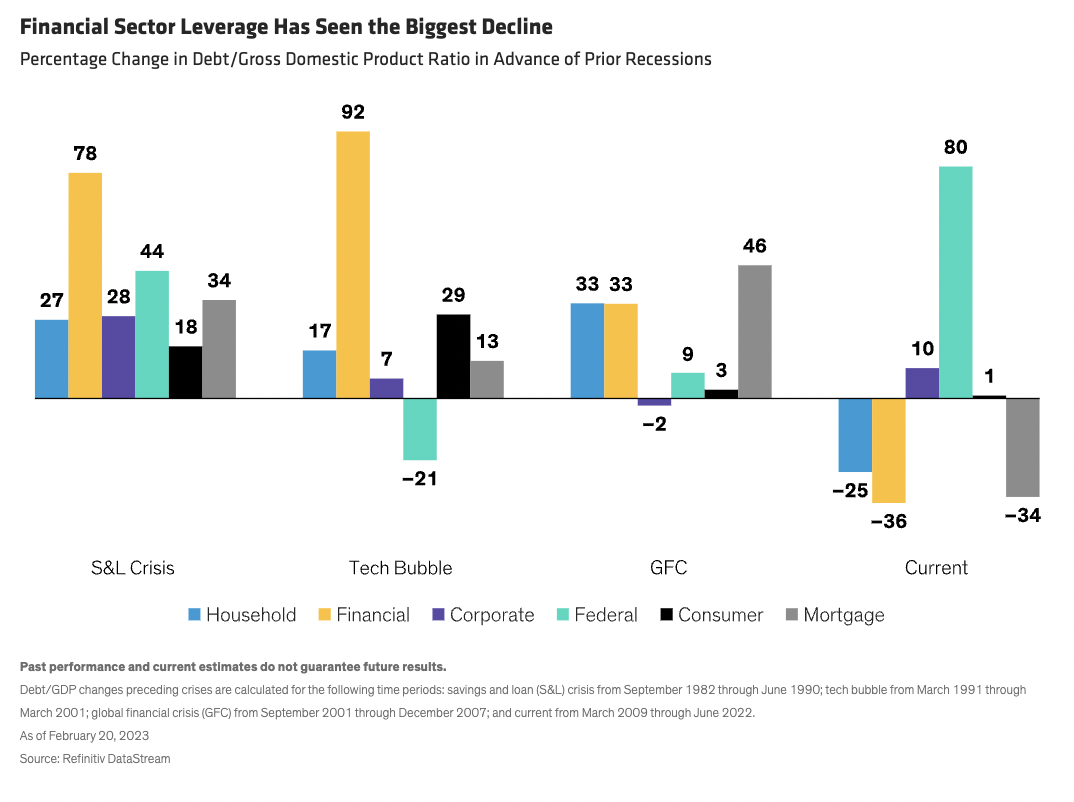

While it’s true that rate hikes have preceded past financial crises, the underlying causes have actually been broader. Rising rates have only caused fractures when accompanied by an underlying vulnerability: banks and other economic actors exploiting low rates and favorable market conditions to leverage balance sheets in pursuit of higher returns (Display). The noteworthy surge in financial and mortgage sector debt in the years leading up to the global financial crisis created plenty of tinder that ignited a profound crisis.

Indeed, every prior cycle saw leverage increased in ways that made rate hikes more likely to magnify pockets of excess.

The financial sector’s role can’t be overstated: it’s where small fires become big ones given that it’s the most direct link to markets and the conduit for transmitting crises to the real economy. In the current cycle, the financial sector debt/GDP ratio has seen the sharpest decline of any sector (Display), so leverage in that segment is not as excessive as it’s been in previous cycles.

Combine a more resilient financial sector with a more robust regulatory regime, and we think there’s a much lower probability that banks will cause or accelerate a wider crisis. Banks aren’t the only ones who’ve tightened their belts: other sectors have made strides in reducing their debt burdens, most notably households—primarily in the form of mortgage borrowing.

The federal government is the obvious exception—federal debt is up by a whopping 80%. But federal borrowing has a vastly different risk profile than other borrowers in the US economy. Unlike any other borrowers, the US Treasury can’t go bankrupt and, barring a debt-ceiling accident, can’t default. That makes government borrowing far less likely to trigger a broader crisis than private sector borrowing.

15 Years of Deleveraging Has Improved Resilience

Past history suggests that markets should always be on the lookout for pockets of excess leverage that may be revealed by interest-rate hikes, but we think the odds of that sort of crisis are much lower now than in past episodes. Prior rate hikes have come on the heels of significant run-ups in debt/GDP across sectors; the current cycle comes on the heels of nearly 15 years of deleveraging.

None of this means a crisis is out of the question, but in our view, a less vulnerable system means that there’s less likelihood of the system breaking. We’ve seen one stress test play out favorably already: the collapse of crypto assets might have had much wider consequences if other economic actors were exposed to crypto in a levered way. That the damage didn’t spread further is a real-time example that today’s financial system is better fortified.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein

Read more commentaries by AllianceBernstein