Dear fellow investors, As a young stockbroker in the 1980s, I was very enamored with T. Boone Pickens. Pickens recognized the huge value that built up in common stocks in the inflationary 1970s and began to use the financial backing of the Junk Bond King, Michael Milken, to become an activist on Wall Street. His little company, Mesa Petroleum, started investing in undervalued large cap oil stocks and threatened to do large leveraged buyouts (LBOs) with the assistance of Milken’s firm, Drexel Burnham Lambert (my employer). Pickens said, “It is cheaper to drill for oil on the New York Stock Exchange than it is to drill directly.” After reading Pioneer Natural Resources CEO Scott Sheffield’s comments recently, we at Smead Capital Management believe we’ve reached that point again:

“Crude oil prices likely will climb to ~$100/bbl by this summer and end the year in the low 90s, Pioneer Natural Resources (NYSE:PXD) CEO Scott Sheffield said Thursday during the company’s post-earnings conference call. Sheffield nevertheless reiterated that capital discipline will remain the priority, and Pioneer’s (PXD) shareholders have not changed their view on that.”

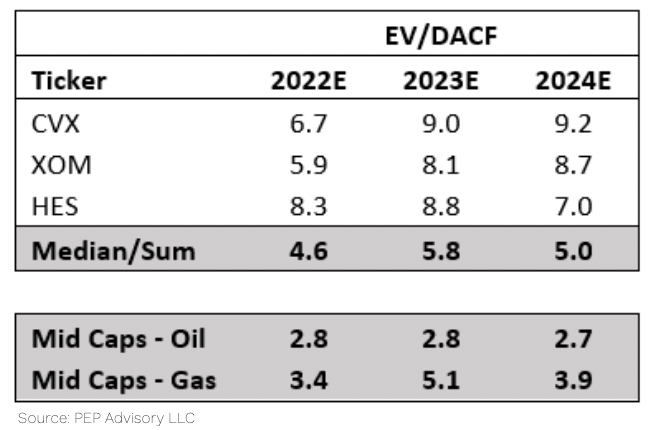

Intense political pressure from Federal and State levels of government is scaring oil and gas companies away from drilling for environmental reasons! Since common stock investors want to benefit from scarcity, Sheffield is not alone in this attitude. If he is correct, the largest capitalization oil companies should be on the hunt to replenish oil reserves via acquisition. The larger oil stocks are more popular primarily because the large investment pools came hunting for oil stocks in 2021 and 2022, but only the largest of the bunch could absorb the massive capital. My co-portfolio manager, Cole Smead, liked to say, “it is like blasting a fire hose into a teacup.” The entire energy space bottomed in 2020 at a measly 2.4% of the S&P 500 Index and now sits at a still very depressed 4.79% of the index. It produces a much bigger part of the S&P’s total profit. If Sheffield is correct on oil prices and the inverted yield curve has its usual effect on the economy, oil and gas profits could become one of the only games in town, like last year.

“We had a record year in 2022... about $8.4B in free cash flow,” the CEO said on the call. “We returned $8B of it back to the investors in regard to both dividends and buybacks... [so] no change at all."

This attitude toward shareholder friendliness is very economic. Nothing could be better than producing addictive fossil fuel energy at higher and higher prices for the next decade. Just look at what Philip Morris did in the U.S. from 1970-2010, when they were vilified, divested and saw adult smoking decline radically. With local, state and federal taxes along for the ride, the price of a pack of cigarettes went from 20 cents to $5. Big “Mo” was the best performing NYSE stock over those 40 years. It was Peter Lynch’s largest position in Fidelity Magellan from 1977-1992 when he retired.