Airline Stocks Are Soaring Over The Negative Headlines, Lifted By Positive Earnings

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Lufthansa is back.”

Those are the enthusiastic opening remarks of Carsten Spohr, CEO of Deutsche Lufthansa, in the European airline’s earnings report for 2022, released today.

I think it would be just as accurate to say that commercial aviation in general is back, with attractive investment opportunities.

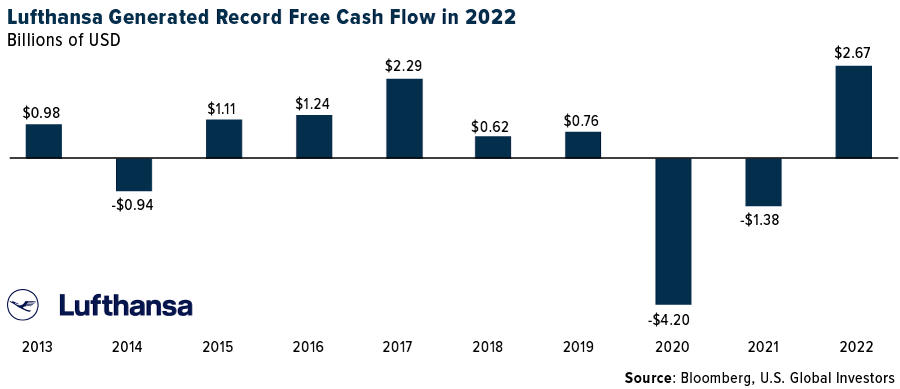

Spohr reported that Lufthansa, Europe’s largest carrier group by revenue, achieved an “unprecedented turnaround” in 2022 on the back of increasing demand for air travel. Revenue of USD$34.5 billion was almost double what it collected in 2021, while free cash flow came in at $2.6 billion, the highest annual amount in the German company’s history. Shares were up approximately 5.3% in intraday trading on the news.

Lufthansa went on to announce that it ordered 22 new long-haul aircraft from Airbus and Boeing, the company’s largest order since 2013.

As I’ve said before, as an investor, I like to see when a company invests in itself. It tells me that management is optimistic about the future and is positioning the company for growth.

That’s exactly what airlines are doing around the globe right now. According to Airlines for America (A4A), U.S. carriers are investing a record amount in new aircraft, equipment, information technology and more. Capital expenditures are forecast to hit $27.0 billion this year, which would be significantly higher than the $21.2 billion airlines are estimated to have spent in 2022.

More Bang For The Buck

Lufthansa’s blockbuster report is just the latest signal that commercial aviation, one of the hardest-hit industries during the pandemic, may be ready to make a landing again in investors’ portfolios.

Travel demand is surging as Europe, China and other key markets have dropped travel restrictions, and in the interim, carriers have adapted by streamlining operations, eliminating unprofitable routes and more.

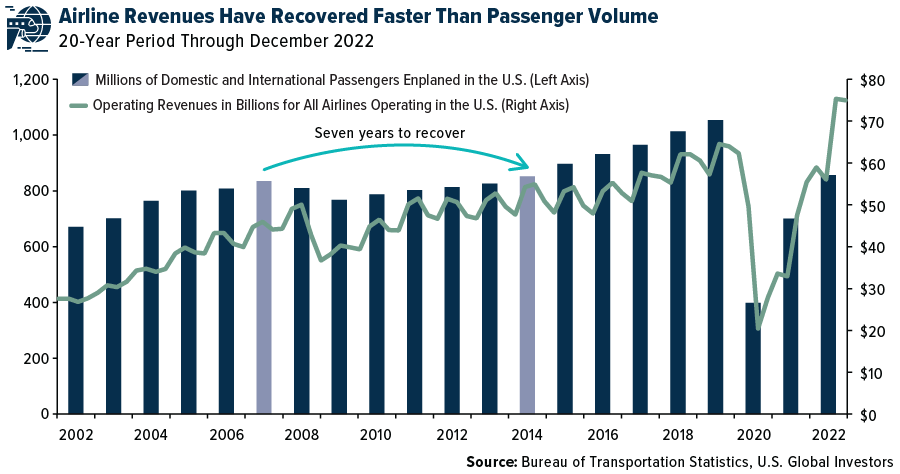

The actions appear to be working. Even though total passenger volume hasn’t fully recovered to pre-pandemic levels, operating revenues are soaring to new record highs, according to Bureau of Transportation Statistics (BTS) data.

Domestic airlines have managed this without having to cut jobs at the same pace as the tech industry. In fact, passenger airlines in the U.S. currently have the largest workforce in 20 years, according to A4A.

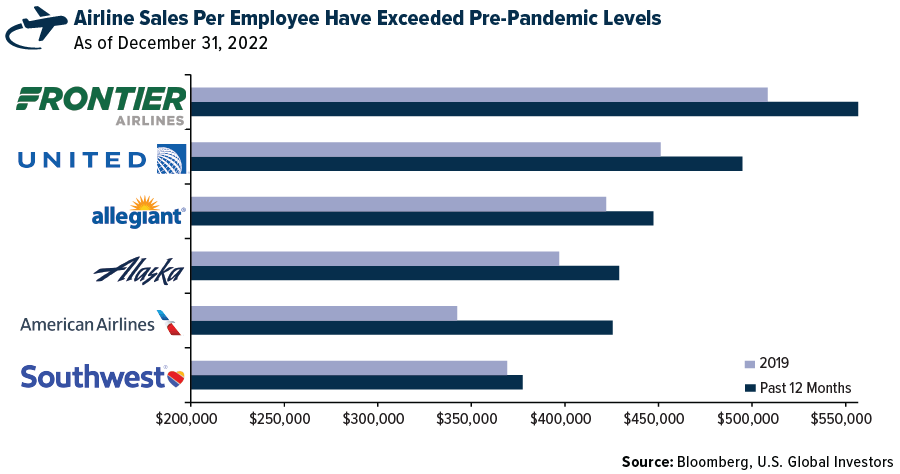

And yet staff are producing more bang for their buck. In the chart below, you can see that sales-per-employee for select carriers were higher in the past 12 months than in 2019, before the pandemic. This indicates that the decision not to sacrifice customer service in the name of cost-cutting has been financially rewarding.

To me, that’s a win-win-win-win: a win for airlines, win for employees, win for customers and a win for investors.

“Aviation Is Investible Again”

“Aviation is investible again,” says Jun Bei Liu, a portfolio manager at Sydney, Australia-based advisory firm Tribeca Investment Partners. Speaking to Bloomberg last month, Jun Bei said she believes Asian airlines “are going to go through the roof.”

I’ve highlighted Asian airlines in recent weeks, particularly after the Chinese government announced it was lifting pandemic-era quarantine requirements for travelers entering the country. I still agree with Jun Bei and others in forecasting a dramatic travel rebound in Asia this year, even though demand so far hasn’t been as strong as unexpected.

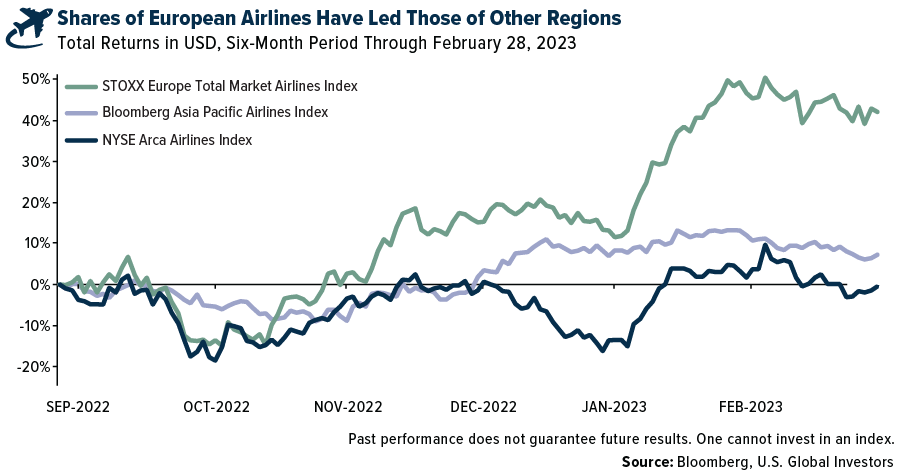

Perhaps surprisingly, shares of European carriers are leading those in Asia and the U.S. I say “surprisingly” because there are so many negative headlines about airlines right now, but often these headlines don’t accurately reflect what’s really happening. European airlines rose over 41% in the six months through the end of February, compared to Asian airlines, up 7%, and U.S. airlines, down slightly at negative 1%, over the same period.

Record-High Premiums On American Eagle Silver Coins

Switching gears, I want to briefly address something that came to my attention in the past couple of days. Kitco News’ Neils Christensen wrote a thought-provoking piece on American Eagle silver coins, sales of which slumped last year compared to sales in 2021. The U.S. Mint sold less than 16 million one-ounce silver coins in 2022, or 43.5% less than it did in the previous year.

As Neil points out, this decrease can’t be due to a lack of investor demand since silver bullion sales were solid elsewhere around the world in 2022. Australia’s Perth Mint, for instance, sold a record number of ounces.

Instead, the sales slump can be attributed to the 70% premium for the American Eagle coins. According to Neil, that’s a record-high premium. At today’s prices, then, a one-ounce American Eagle coin that contains $21 worth of silver is really priced at $35.

Neil explains why this is happening. To make its coins, the U.S. Mint buys silver “blanks” from private mints, and supply can be limited. Some people have suggested that the Mint should make its own silver blanks.

I’ll go a step further and suggest that precious metal miners should get in on this business. Imagine if they began pressing blanks and selling them to the U.S. Mint at a 70% premium. Would their share prices go up 70% as a result? I can’t say, but what I do know is that producers, particularly the juniors, are extremely undervalued right now.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.75%. The S&P 500 Stock Index rose 1.87%, while the Nasdaq Composite climbed 2.58%. The Russell 2000 small capitalization index gained 1.99% this week.

- The Hang Seng Composite gained 3.00% this week; while Taiwan was up 0.67% and the KOSPI rose 0.35%.

- The 10-year Treasury bond yield rose 1 basis point to 3.959%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Wizz Air, up 13.6%. According to JPMorgan, systemwide booked revenue for the first quarter remains ahead of 2019 by a comfortable double-digit margin, though forward momentum has eased from the torrid rate heading into year-end holidays. Domestic revenue exhibits a similar trend, while Latin American and Atlantic revenue are the most impressive.

- Contrary to the continuing downtrend in spot rates, share prices of Japan’s “Big 3” shippers have outperformed TOPIX by 10% in the past month. The reasons behind this are: 1) relatively close interest in dividend yields which are much higher than for Japanese stocks in other industries, and 2) the current turnaround in dry bulk market prices, which is due to the positive effects of China reopening.

- According to JPMorgan, Chase daily card spend on air travel (a lesser but still relevant metric) remains robust. While the ink on first quarter guides has barely dried, revenue data implies guides remain comfortably within reach (with the potential to be exceeded).

Weaknesses

- The worst performing airline stock for the week was Azul, down 4.9%. Intra-Europe net sales were down 6 points to -21% versus 2019 levels. International net sales declined by 19 points to -6% versus 2019 but were up 1% this week. Intra-Europe volumes were down by 4 points to -29% versus 2019, while international volumes declined by 10 points to -19%.

- Express volume in January in China dropped 17.6% year-over-year from +1.2% in December 2022, due mainly to an earlier Chinese New Year in 2023. All four major players in China saw negative volume and revenue growth year-over-year due to an earlier Chinese New Year holiday in January 2023.

- Alaska Airlines had the highest percentage of cancelations occur over the past week at 7% of captured flights (this compares to 1% the week prior), which is not surprising as the major winter storm last week significantly impacted the West Coast.

Opportunities

- Goldman Sachs believes Chinese airlines and airports will experience a three-phase recovery: 1) a V-shape recovery for domestic air travel; 2) a gradual ramp-up for international air travel; 3) maintain airfare hike versus 2019’s level (ex. fuel surcharge) under mid-term supply shortage. Given domestic air travel has recovered to 85% of 2019’s level, performing well on track for a V-shape recovery, Goldman believes the market debate will be concentrated on international traffic recovery and airfares.

- According to Morgan Stanley, tanker effective supply growth in 2022 was 2.6%. The group expects effective capacity to grow by 2.6% and 1.0%, in 2023 and 2024, respectively, with a low orderbook to fleet ratio. In addition, scrapping and impact of environmental regulations could further help remove effective capacity.

- United Airlines noted “January and February were a little bit soft,” albeit consistent with its expectations of a soft build, like December, due to the holiday timing. Conversely, March bookings are back to October levels, which was a “gangbusters” month for the industry. Business demand, which was 80% recovered by year-end 2022, reached 97% over the last three weeks.

Threats

- The Federal Aviation Administration (FAA) confirmed Boeing 787 deliveries have been halted. Boeing temporarily halted deliveries while conducting further analysis on the fuselage quality issue discovered last summer. However, now documentation issues related to the analysis will require the FAA to provide clearance for deliveries to resume.

- UBS is updating the macro correlation data that was introduced late last year and refreshed ahead of UPS’s fourth quarter 2022 earnings. This should help identify trends and inflection points for the important fundamental drivers of domestic and international revenue lines for the parcel companies under their coverage. The correlation data points to possible downside to its U.S. Express volume forecast.

- With ANA’s new medium-term business plan pointing to significant cost increases in the medium term as a result of ongoing yen weakness and for maintenance and parts, the focus from here will be on whether top-line growth can offset the impact of higher costs.

Luxury Goods And International Markets

Strengths

- The world’s luxury real estate market is led by New York, followed by Los Angeles and then London. However, Dubai is emerging as a key player, now ranking as the fourth-busiest luxury real estate market in the world. Luxury home prices in the city are expected to increase 13.5% this year after a surge of 44% last year, according to property consultant Knight Frank LLP. Dubai sold 229 properties worth over $10 million last year, versus New York at 244, Los Angeles at 225, and London at 223. Dubai has become a global travel hub, attracting wealthy investors and crypto millionaires. The city is also attracting hedge funds and traders because of the ease of doing business and the tax-free status.

- China’s Manufacturing PMI increased in the month of February. The number was reported at 52.6 versus 50.1 in the previous month, and above consensus of 50.6. China’s Service PMI spiked to 56.3 versus 54.4 in the previous month, and above consensus of 54.9. The Composite PMI reached 56.4, well above the 50 level that separates growth from contraction.

- RealReal Inc, an American marketplace for luxury goods, was the best performing S&P Global Luxury stock for the week, gaining 25.38%. This week the company released its fourth quarter results which met the average estimated. The company saw revenue of $159.7 million versus a Bloomberg consensus of $158.1 million.

Weaknesses

- February’s final S&P Global Eurozone Manufacturing PMI was reported at 48.5, confirming a slowdown in Europe’s economic activity (January’s Manufacturing PMI was 48.8). The final U.S. Manufacturing PMI for February was reported slightly lower than the preliminary reading, at 47.3 versus 47.8.

- Inflation in Europe increased 0.80% month-over-month, above the expected 0.5%. On a year-over-year basis, prices spiked 8.5%, above the expected increase of 8.3%. The increase in inflation levels could give the European Central Bank (ECB) a green light to keep raising rates in Europe. This week, the ECB started quantitative tightening, selling 15 million euros a month, on average, until June.

- Wynn Macau Limited, an Asian company which owns and operates casino resorts, was the worst performing S&P Global Luxury stock for the week, losing 5.50%. This week the company’s shares fell 3.8%, the lowest since December 7, after it announced a plan to sell $600 million of convertible bonds at a coupon of 4.5% due in 2029.

Opportunities

- LVMH announced its plan to repurchase around $1.59 billion of its own stock through July 20. As a result, the stock rose 2% on Wednesday, increasing the gain this year to 18% and reaching the company’s market valuation of about €404 billion, the highest in Europe, Bloomberg said.

- According to Bloomberg, Hong Kong retail sales could increase year-over-year by around 27% in 2023, exceeding 2019’s levels. In addition, 80% of growth will be supported by tourists from mainland China. Hong Kong is expecting more than 34 million visitors in 2023.

- According to S&P Global Ratings, luxury sales bounced back to pre-pandemic levels by the end of 2021, after Covid drove the industry to the worst decline in 2020. In a report released on Thursday, the ratings company said it believes the industry is well placed to maintain its positive growth features and good profitability levels moving forward.

Threats

- Factory orders in the United States, which track new orders received based on legal agreements between producers and buyers, are expected to decrease considerably. Bloomberg economists expect factory orders to drop from positive 1.8% in December to negative 1.5% in January. This would represent a decrease of 183% that could impact the luxury goods sector in the U.S., one of the leading luxury markets worldwide. This data will be released next week on March 6.

- This weekend, China will hold its first National People’s Congress (NPC) meeting post the zero-Covid era. Investors are waiting for new economic incentives to be announced that would further support the economy. However, according to FactSet, the Chinese government could decide to remove some stimulus programs thanks to surprised economic recovery post-removal of some of the country’s strict zero-Covid policies.

- In the past three years, the working population in China has considerably decreased by around 40 million workers as the population ages. More specifically, 733.5 million people were employed in 2022 versus 774.7 million in 2019, reported Bloomberg. The situation may force the country to increase the official retirement age.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was natural gas, rising 17.58%, after falling below $2.00 per mcf in the prior week. The price of molybdenum, the obscure commodity that’s used to help toughen steel, has reached $45 per pound in recent days, (surging 2.5X as compared with mid-2022 and climbing well above the 2022 average of $19 per pound). Supply concerns drove prices higher in an already tight market. Civil unrest in Peru impacted supply of molybdenum concentrates and customers were prepared to pay elevated prices to avoid interruptions in the production of specialty steel, according to AMM.

- According to RBC, fertilizer equities found some traction this past week and outperformed the broader market as fourth quarter reporting helped reset expectations and fertilizer prices may be stabilizing in the near-term. RBC thinks fertilizer markets have likely moved past the worst of the last 6-9 month sell-off and prices are finding some signs of stabilization at still-elevated levels. However, there may still be some volatility ahead as re-emerging demand remains hesitant and supply gradually eases.

- European Union oils had a quarter of strong free cash flow (FCF) generation, which for the group amounted to $20 billion plus $13 billion working capital release, remaining well above the five-year historical average, (albeit lower than exceptionally high second and third quarter levels). This was the seventh consecutive quarter where EU oils beat consensus in aggregate, with operating income and adjusted net income 5%/14% above company-compiled consensus.

Weaknesses

- The worst performing commodity for the week was coffee, dropping 5.25%, with Bloomberg citing higher rainfall in Brazil potentially helping cherry growth, and perhaps a larger crop. Commercial crude inventories built for the ninth straight week, by 7.647 million barrels, while the SPR was flat for the sixth straight week. The build was driven by lower refinery runs, partially offset by lower net imports and flat production.

- Hardwood shipments decreased year-over-year in most regions, with lower shipments in North America (-12.4%), Western Europe (-21.0%), Eastern Europe (-26.4%), Latin America (-6.8%), Japan (-3.0%), and China (-1.0%). This was slightly offset by increased shipments in Oceania and other Asia/Africa regions. The hardwood operating rate decreased seven points to 76%.

- Chinese lithium prices were down by nearly 10% this week as demand has still failed to rebound (domestic inventories are building too as a result) and last week’s news is digested. At this point, market participants are now holding back as they wait for a new point of stability to be found, so prices are likely to remain pressured in the short term.

Opportunities

- Last week, front-month natural gas prices breached $2/Mcf, a level not seen since late 2020. However, investors are not being shy and looking at the gas equities given a view that the bottom is near. This is somewhat supported by a forward natural gas curve that is still $3/Mcf. There are few gas macro catalysts remaining into winter’s last efforts, but the worst could be over for the commodity price.

- JPMorgan remains bullish on energy fundamentals and continues to see oil prices over $150 per barrel in 2024/2025, as outlined across several installments of the group’s Supercycle thesis from March 2020-April 2022. Moreover, ongoing price volatility and continued preference by industry to return cash rather than invest in future oil supply should sow the seeds for steep contango, higher highs on oil prices, and a longer upcycle into 2030 and beyond.

- According to RBC, the energy sector has modestly underperformed the market in recent months, with more modest, but still robust, commodity prices alongside some extremely strong performance in 2022 driving rotations to other sectors. RBC believes the sector remains set up well for a multi-year period of outperformance relative to the wider market, with robust commodity prices supporting above-average returns to shareholders, and fortress balance sheets providing defensiveness during times of weakness.

Threats

- First Quantum’s Cobre Panama has been forced to suspend ore processing operations given its inability to load copper concentrate at its port, following orders from the Panama Maritime Authority to suspend loading, which has led to a lack of concentrate storage area. The suspension of operations could last up to a few months.

- Lithium names are seeing a bid as the Chinese government has ordered some lithium mining/processing facilities that account for 10% of global supply to be shut down on environmental violations. Recall China’s biggest electric vehicle (EV) battery manufacturer CATL recently cut EV battery prices to win market share via longer-term battery supply contracts with automakers, but that price cut likely assumed lithium prices would remain flat-to-down from here.

- Tesla commented that its future models will use permanent magnet motors that will not use rare-earth metals. Share prices of Chinese rare-earth miners were off 7% on the news. China dominates the world in the production of rare-earth metals and perhaps Tesla is trying to find a way to shore up this potential weakness in their supply chain.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Maker, rising 30%.

- Goldman Sachs’ digital asset team signaled it’s open to bolstering staff strength and flagged the potential for blockchain technology to improve the functioning of markets such as private equity, explains a Bloomberg article.

- Crypto investors are scooping up call options betting on a Bitcoin rebound to $30,000 even as momentum in the digital asset market stalls, reports Bloomberg. Bitcoin options open interest rose in February to $9 billion. The last time it was at this level the coin had been trading around $45,000, whereas it is currently hovering around $23,700 and is seeing the largest 14-day rate of change in its history, the article continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Conflux, down 24%.

- Bitcoin’s two-month rally contains a warning for investors if history is any guide, reports Bloomberg. The February jump in the largest digital token has withered to about 2% compared to the 39% seen in January. When Bitcoin has climbed over two straight months, but with smaller gains in the second month, the third month it has retreated at an average of 5.8%, the article explains.

- The superior court of the District of Columbia rejected a motion by MicroStrategy to dismiss a lawsuit that he failed to pay income taxes despite living in the district for more than a decade. In addition, the court dismissed a claim by Washington DC alleging that Saylor and MicroStrategy conspired to violate the districts False Claims Act, writes Bloomberg.

Opportunities

- The creators behind Bored Ape Yacht Club are launching their first collection of Bitcoin NFTs. Yuga Labs plans to auction a collection of 300 generative pieces on the Bitcoin blockchain called TwelveFold in what could be the kind of event Bitcoin purists say will slow down the network, writes Bloomberg.

- Jack Dorsey’s digital payment company Block Inc. said it will be using its own Bitcoin reserves to provide liquidity to Bitcoin’s Lighting Network, a protocol meant to make transactions on the blockchain more efficient, writes Bloomberg.

- A crypto hedge fund overseeing $400 million is looking to Swiss banks to help plug the gap created by the unraveling of a key payments network operated by ailing U.S. lender Silvergate Capital, reports Bloomberg.

Threats

- The SEC has proposed a custody rule to include digital assets and could make it harder for crypto platforms to hold customer assets, reports Bloomberg. The proposal written would make it almost impossible for some crypto platforms (those that aren’t considered qualified custodians) to accept and hold clients’ digital assets, the article continues.

- Founders of BlockFi Inc. should be held liable for digital assets lost while in BlockFi investment accounts, a class suit says. Founders Zac Prince and Flori Marquez allegedly made misleading statements about how the platform worked, falsely assuring investors that their cryptocurrency wouldn’t transfer to BlockFi, writes Bloomberg.

- Silvergate Capital fell 58%, to its largest drop in in its history, as crypto players abandon the crypto bank, according to an article published by Bloomberg.

Gold Market

This week gold futures closed at $1,861.00, up $43.90 per ounce, or 2.42%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.44%. The S&P/TSX Venture Index came in up 4.33%. The U.S. Trade-Weighted Dollar rose 0.64% and Bitcoin dropped 3.46%.

Strengths

- The best performing precious metal for the week was platinum, up 8.29%, on a falling dollar and a pullback in yields. Partially driven by recent deal activity, gold M&A has become more topical. Many companies suggest they are open to the right opportunities but remain disciplined. There are fewer non-core assets flagged for divestment. Companies are growing mindful of hanging on to everything in the pipeline, considering limited organic growth opportunities otherwise.

- Gold is poised for its best week since mid-January, reports Bloomberg, as the dollar weakens on signs that China’s economic recovery is gathering pace. Bullion climbed higher Friday as a gauge of the dollar extended what would be its first weekly decline in five, making the precious metal cheaper for most buyers. China’s economy is rebounding rapidly, the article explains, while Euro-area inflation is proving hotter than expected, raising the prospect of more tightening from the bloc’s central bank.

- Lundin Gold provided a reserve and resource update for its Fruta del Norte (FDN) mine, and it was ahead of consensus. Since the operation achieved its first production in 2019, a total of 1.38 million ounces of gold has been depleted through mining and milling operations. With this update, Lundin added 1.58 million ounces to reserves, more than replacing all the mining depletion to date.

Weaknesses

- The worst performing precious metal for the week was silver, but still up 1.91%. Argonaut Gold released fourth quarter 2022 financial results with adjusted EPS of -$0.05 (versus consensus of -$0.01) driven by lower production and higher costs, slightly offset by higher realized selling prices. Production during the quarter was 42,500 ounces with AISC of $2,266 per ounce.

- K92 Mining provided an operational update for its Kainantu Gold Mine. During the month of February, the process plant has experienced two notable unplanned maintenance events that together, management says, will have an impact on February and first quarter 2023 production. One of the mill trunnion bearings failed, requiring immediate replacement. Then, a limited electrical fire in a cable tray resulted in damage to several cables feeding the wet section of the process plant. The processing plant has now successfully restarted.

- Sibanye Stillwater’s 2022 production and earnings (headline EPS of 40 cents per share versus consensus of 44 cents per share) missed estimates on the back of a challenging year for the company. AISC for the year was high, reflecting lower metal outputs and inflationary pressures.

Opportunities

- Superior Gold (SGI) has entered into an all-share agreement with Catalyst Metals (CYL) where SGI shareholders will receive 0.3571 of one Catalyst share for each SGI share. The deal values SGI at C$0.44 per share, which represents a 62% premium. This transaction would result in SGI shareholders receiving an immediate bump in value but potentially missing out on some benefit due to accepting the deal after reporting a challenging year in 2022.

- Newmont sees the NEM/NCM combination providing the following advantages: 1) ESG – being a leader in this field, 2) creating a world-class portfolio (gold/copper) with the optionality for portfolio rationalization and project sequencing, 3) synergies to be gained from scale, global supply chain, access to talent and technology and 4) driving capital allocation (disciplined strategy).

- RBC expects a relatively neutral reaction from I-80 Gold following the announced acquisition of Paycore Minerals for C$60M in total implied consideration. Paycore owns the FAD property, which lies immediately south of I-80’s Ruby Hill project in Nevada, helping to consolidate the property land package. I-80 had previously indicated potential for increased emphasis on Ruby Hill within the asset portfolio following up on recent high grade polymetallic drill results and potential for gold/base metal processing via existing infrastructure on-site.

Threats

- Most companies under coverage are assuming inflationary pressures seen in 2022 will persist into 2023, but slowly taper off thereafter. Newmont’s five-year outlook, which saw long-run cash costs increase $50 per ounce or around 7% from the prior guide and sustaining capex up $175 million annually (or up around 14%) from the prior guide. Higher gold prices will be needed to offset this.

- RBC sees a negative reaction from Argonaut shares following 2023 guidance, with the announced suspension of the company’s Mexican operations in part due to higher costs and pending resolution of land access/permitting issues. At Magino, capex was increased modestly by C$60M as anticipated with first gold targeted in mid-May and appears to be funded with $243 million in liquidity at year-end.

- St Barbara has received requests for information from the Nova Scotian Minister of Environment and Climate Change in response to the environmental assessment of the proposal to deposit tailings into the Touquoy open pit. As stated in the second quarter report, any delays in approvals to in-pit tailings would trigger cessation of production early in fiscal year 2024. The compilation of the information required to answer the Minister’s questions would indeed take more time than is available before the capacity of the existing tailings management facility is reached in early 2024.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

Sibanye Stillwater

K92 Mining

Argonaut Gold

Superior Gold

Newmont Gold

Alaska Air Group

Boeing Co/The

United Parcel Service

LVMH Moet Hennessey

Deutsche Luftsansa AG

Frontier Group Holdings Inc.

United Airlines Holdings Inc.

Allegiant Travel Co.

Alaska Air Group Inc.

American Airlines Group Inc.

Southwest Airlines Co.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The STOXX Europe Total Market Airlines Index tracks the performance of shares of listed airlines in Europe.

The Bloomberg Asia Pacific Airlines Index is a capitalization-weighted index of the leading airlines stocks in the Asian Pacific Region.

The NYSE Arca Airline Index is an equal-dollar weighted index designed to measure the performance of highly capitalized companies in the airline industry.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All