Shifting expectations

Market pricing of peak and end-2024 ECB policy rate, 2022-2023

Euro area stocks have outperformed U.S. peers by about 14% in local currency terms since the end of September, MSCI index data shows. That’s partly because the economy has withstood the energy crunch even as the war in Ukraine drags on. Plus, export-centered sectors also look set to benefit from China’s restart. Yet good news on growth now means the ECB has more work to do to cool inflation later, as we said for the U.S. We think that’s bad news for Europe’s risk assets. We see policy rates already on track to tip the economy into recession this year after growth stagnated at the end of 2022. Data last week showing core inflation rising and services activity improving may push the ECB to hike more. Market pricing now expects rates to peak around 3.9% (orange line in chart) versus about 3.2% in February, with fewer rate cuts seen in 2024 (pink line).

Europe’s cooling goods inflation and lower gas prices have driven a drop in overall inflation. We think elevated services inflation will prevent inflation from falling to the ECB’s 2% target on its own – similar to the U.S. That’s because wage inflation is bleeding into the services sector. The reason: European firms are raising pay to recruit new hires given a surge in workers jumping to the public sector. That labor marker tightness looks set to persist. Data last week confirmed euro area unemployment is near a record low. The ECB faces a stark trade-off between pushing up unemployment or living with persistent inflation. ECB officials seem determined to do “whatever it takes” to get inflation down to target, in our view, as that is their only objective. We expect the ECB to raise rates through midyear and not cut them until the second half of 2024.

Income opportunities

We think this backdrop of higher rates and persistent inflation boosts the appeal of high-quality European credit and short-term government bonds. Yields have jumped from their ultra-low levels reached during a decade of negative interest rates. Strong corporate balance sheets limit the risk of credit defaults when recession hits, in our view. We’re overweight both on a tactical horizon of six- to 12-months. We also turn to credit for income from a strategic horizon of five years and beyond.

Equity view

We don’t think European stocks are pricing in the economic pain we see ahead even as valuations look inexpensive relative to the past and regional peers. Stocks could also lose support if foreign investors’ attention shifts, as it historically has. We’re tactically underweight developed market (DM) stocks, including Europe. Within Europe, we favor the financial sector as rates rise. We also like the energy sector given the energy shortage, stronger balance sheets and better return on equity than in the past. We favor healthcare on its relatively steady cash flows in economic downturns and strong growth potential from long-term trends like aging populations. Plus, we like the consumer discretionary sector as European brands benefit from ramped up demand for luxury goods from China’s restart. Our preferences underpin why we’re neutral on Swiss stocks compared with our overall underweight in Europe. The financial, healthcare and consumer staple sectors dominate the index. We are strategically overweight DM stocks and expect earnings to recover once recessions end. We also see returns surpassing bond returns as yields rise due to investors demanding more compensation for risk amid high inflation and heavy debt loads.

Bottom line

European risk assets have outperformed so far this year. But we think that trend will end as recent data pushes the ECB to raise rates and keep them higher for longer. We prefer income from credit and short-term government bonds. We’re underweight European stocks but like the financial, energy, healthcare and consumer discretionary sectors.

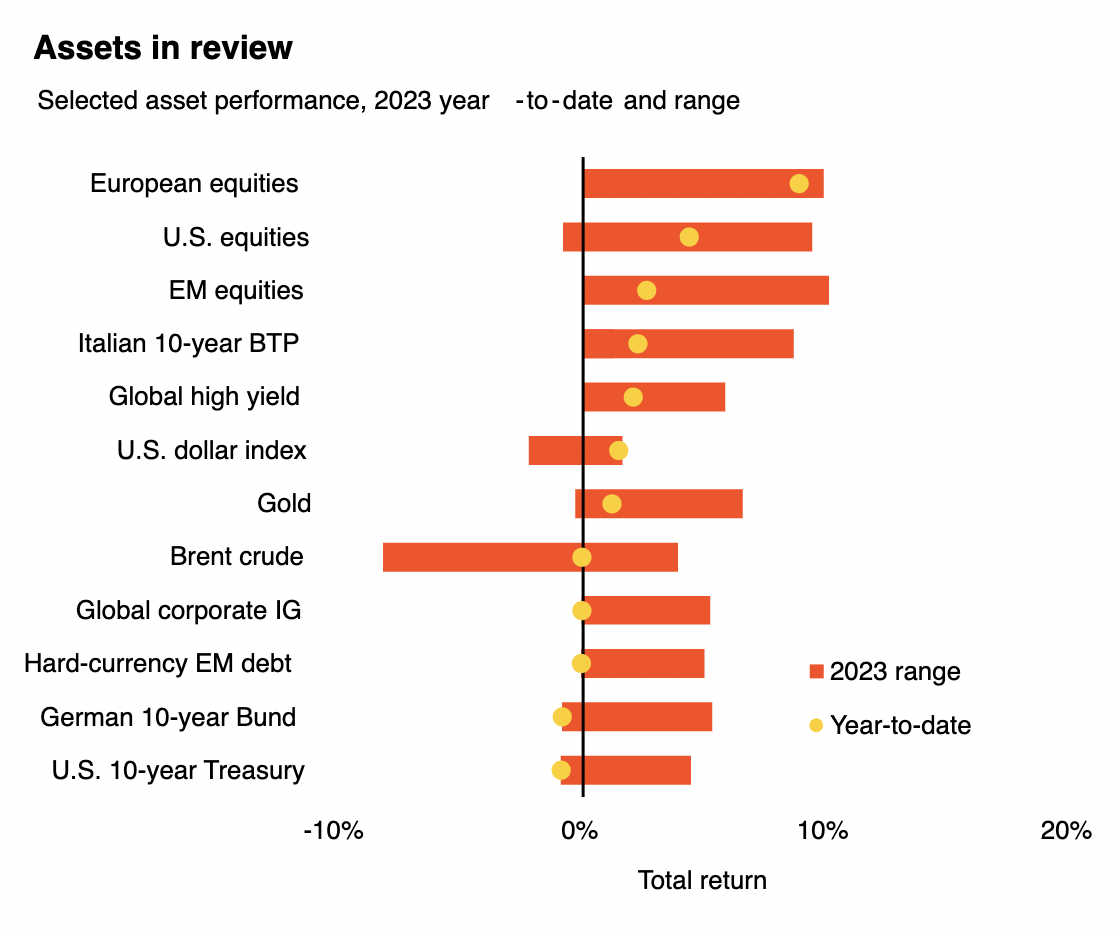

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv Datastream as of March 2, 2023. Notes: The two ends of the bars show the lowest and highest returns at any point in the last 12-months, and the dots represent current year-to-date returns. Emerging market (EM), high yield and global corporate investment grade (IG) returns are denominated in U.S. dollars, and the rest in local currencies. Indexes or prices used are: spot Brent crude, ICE U.S. Dollar Index (DXY), spot gold, MSCI Emerging Markets Index, MSCI Europe Index, Refinitiv Datastream 10-year benchmark government bond index (U.S., Germany and Italy), Bank of America Merrill Lynch Global High Yield Index, J.P. Morgan EMBI Index, Bank of America Merrill Lynch Global Broad Corporate Index and MSCI USA Index.

© BlackRock

Read more commentaries by BlackRock