Bitcoin Is A Key Component Of The Great Digital Transformation

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMany people may not have heard of SHA-256, but I believe it to be one of the greatest American inventions of the 21st century.

Developed by the National Security Agency (NSA) in 2001, SHA-256 is a secure hashing algorithm that, among many other things, is used by your iPhone to encrypt data, including the unique facial characteristics that many of you use to unlock your phone.

It also makes Bitcoin encryption possible. I won’t bore you with the details—you can read more about the algorithm here—but SHA-256 has never been hacked or compromised, making Bitcoin one of the most secure protocols on earth.

This is precisely why Satoshi Nakamoto, Bitcoin’s pseudonymous inventor, chose to build the digital asset on top of it. Writing in 2010, Satoshi said that SHA-256 “can last several decades unless there’s some massive breakthrough attack.”

That’s good news, as Bitcoin is designed to be mined and held for decades to come—and beyond. The very last available bitcoin is expected to be produced sometime in the year 2140. As of this writing, close to 92% of every bitcoin that will ever exist has already been mined, meaning approximately 1.7 million are still up for grabs.

Setting The Record Straight

So why am I telling you all this? Mainly to set the record straight on Bitcoin.

First of all, Bitcoin is a U.S. invention, despite the Japanese-sounding pseudonym of its creator(s). This is important because some people believe it was designed specifically to destabilize the dollar or the traditional monetary system.

That couldn’t be further from the truth, though many advocates believe Bitcoin could one day replace fiat currency. Even the Bank of International Settlements (BIS), one of the most vocal critics of Bitcoin, has issued guidance for central banks to potentially hold digital assets as reserve currencies.

I’m sure you’ve noticed that there’s been a lot of negative press about “crypto” since at least last summer, first with the implosion of Terra/LUNA and the bankruptcies of crypto lending firms Celsius and Voyager Digital. Then, of course, came the massive fraud scandal involving Sam Bankman-Fried and his crypto exchange FTX. And this week, crypto bank Silvergate announced it would shut its doors.

Due to its association with crypto, Bitcoin’s price suffered as a result of these setbacks, even though it has nothing to do with the firms in crisis, and even though its proof-of-work (PoW) protocol makes it far more secure than proof-of-stake (PoS) coins such as the now-worthless LUNA.

Bitcoin is the only crypto asset to officially be considered a commodity, according to the U.S. Commodity Futures Trading Commission (CFTC), citing its PoW protocol. All other coins and tokens may very well be classified as securities.

Part Of The Digital Transformation

Like face recognition, artificial intelligence (AI), mRNA vaccines and other modern technology, Bitcoin itself is neither “good” nor nefarious. Instead, it’s a key component of the ongoing, rapidly accelerating digital transformation.

I think the lightning-fast adoption of ChatGPT is proof of this hyper-acceleration. The AI chatbot, developed by OpenAI, may be the fastest-growing app of all time. Launched at the end of November 2022, it reached 100 million active users, in only two months, significantly beating other popular apps such as TikTok, Instagram and Pinterest. Last month, ChatGPT netted a staggering 1 billion visits to its website, according to Similarweb.

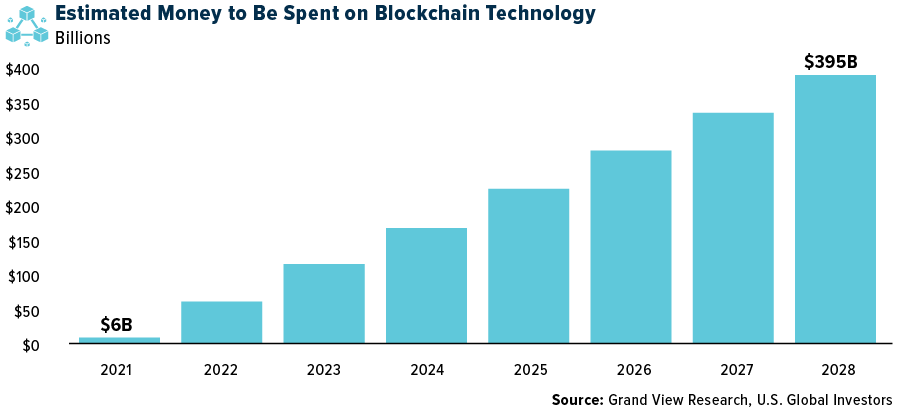

Take a look below. Spending on blockchain technology is expected to expand more than 65 times from 2021 to 2028, when it could hit $395 billion, according to one research firm. Due to its superior security properties, Bitcoin will be used to validate everything on these blockchains, which I believe will increase its value exponentially. As I often say, follow the money.

A Decentralized Asset Like Gold And Silver

Speaking of money, Bitcoin’s market cap now rivals that of Visa and Mastercard, which have millions of users and decades’ worth of name recognition. Bitcoin is decentralized, meaning it has no CEO, no board of directors and no marketing budget. And yet its total value is approximately in line with that of the two biggest credit card companies. When it was trading at $55,000 and $65,000, Bitcoin’s market cap completely eclipsed that of Visa and Mastercard.

As big as Bitcoin is, it’s nowhere close to the market value of gold and silver, two more decentralized assets. Gold’s total global value is currently a little over $12 trillion, roughly the size of five Apples, while silver’s is approximately $1 trillion, sitting right between Alphabet and Amazon at today’s prices.

To me, this bodes well for Bitcoin, whose market cap is around $433 billion right now. For the digital asset to have the same value as silver, each bitcoin would need to be priced at $60,000, which it’s achieved before and likely will do so again.

For it to have the same value as gold right now, Bitcoin would need to trade at an eye-popping $630,000.

Is that doable? Some people think so. Billionaire investor Tim Draper believes Bitcoin could hit $250,000 by the end of this year. Cathie Wood says it could go as high as $1.5 million in seven years.

I’ll refrain from making my own price prediction, but I will say that as the digital transformation advances, I expect Bitcoin’s price to advance alongside it.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.44%. The S&P 500 Stock Index fell 4.54%, while the Nasdaq Composite fell 4.71%. The Russell 2000 small capitalization index lost 8.12% this week.

- The Hang Seng Composite lost 6.45% this week; while Taiwan was down 0.53% and the KOSPI fell 1.54%.

- The 10-year Treasury bond yield fell 26 basis points to 3.686%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Azul Airlines, up 75.6%. In February, airline stocks declined 1.4%, but still outperformed the S&P 500 by 1.2%. This follows a strong January for the group and year-to-date, airline stocks have gained 16.9% compared to the S&P 500’s 3.4%.

- International Container Terminal Services (ICTSI) fourth quarter 2022 and fiscal year 2022 net profits were both a beat, driven by solid throughput growth and elevated yield. On the back of solid fiscal year 2022 results, ICTSI also declared a special dividend, bringing its full-year payout to 52% and a 3% dividend yield.

- Azul Airlines’ shares that have recently reflected liquidity concerns should react positively to the company’s announcement of having reached commercial agreements with lessors accounting for >90% of its lease obligations. The agreements replace: 1) Covid-related deferrals and 2) reduction in lease rates of some older aircraft to current market rates with “long-term debt” and “equity valued at a reset balance sheet”.

Weaknesses

- The worst performing airline stock for the week was Hawaiian Air, down 14.4%. Data from Cirium suggests that 22 Boeing 737s were delivered in February, compared with 35 deliveries recorded in January. This decline should not come as a surprise since last month, Boeing CFO Brian West announced at an investor event that he was expecting MAX deliveries to decline in February due to supply chain issues on the 737 line. However, year-to-date deliveries averaged a 29 monthly rate versus the 33-37 monthly delivery rate the company needs to reach its delivery target of 400-450 737s by 2023.

- Global air freight volume has been in a downcycle since March 2022, while the supply of cargo space has recovered to just 7% below the pre-pandemic level (as of December) on a rebound in passenger flights in the U.S. and Europe. With supply-demand thus softening, air freight rates were still high at the end of 2022, but falling increasingly fast.

- American Airlines has a limited orderbook today, and the airline forecasts just $5 billion of cumulative capex in 2023-2024. As a result, Treasurer Meghan Montana is only looking to finance about 12 737 MAX aircraft today. Instead, American is focused on its debt paydown goals of $15 billion in debt reduction by 2025, with a particular focus on 2025 maturities. Target liquidity today remains in the $10-12 billion range, and this could change over time based on the pace of the recovery.

Opportunities

- Based on current schedules, first quarter 2023 system capacity is showing a sequential improvement of 6.3% compared to fourth quarter 2022 capacity. However, second quarter 2023 system capacity shows the sequential improvement moderating.

- Generally, the rule of thumb is for every 1 million tons per year of U.S. LNG capacity, the shipping market needs an additional 2 to 2.5 new LNG ships assuming two-thirds of the volume move to Asia. Thus, the U.S. expansion should require about 88 new vessels by the time the three planned U.S. projects are complete in the next two years.

- Lufthansa remains interested in investing in TAP and is one of the favorites to enter the share capital of the Portuguese company. According to Bloomberg, cited by Negócios, during the presentation of annual results, Lufthansa assumed that the most interesting targets for mergers and acquisitions are TAP and the Italian ITA, formerly Alitalia. Lufthansa’s interest in TAP dates back to 2019, when the German company’s investment was almost complete. However, the process was suspended due to the Covid-19 pandemic.

Threats

- The Evercore ISI Airlines Survey ticked down from 71.3 to 68.8, as close-in domestic leisure demand has moderated, though it remains stronger than 2019. Business demand continues to recover. The international portion of the index remains at its all-time survey high of 92.5. Demand remains strong in 2023 and continues to be led by leisure, though business demand is gradually coming back. International demand is very healthy amid the easing of travel restrictions. Spring break demand looks strong, but not quite as strong as was seen in the fourth quarter holiday season.

- Carriers are managing shipping capacity by blanking sailings, which is supporting an environment of low rates, low utilization, and low reliability. This “wait and see” approach is consistent with a prisoners’ dilemma, as one carrier doesn’t want to cut capacity, helping balance the market at their own expense.

- The U.S. Justice Department (DOJ) filed an antitrust lawsuit seeking to block the JetBlue merger with Spirit Airlines, and separately, there are headlines that the Department of Transportation (DOT) will deny Spirit’s airline certificate transfer.

Luxury Goods And International Markets

Strengths

- According to Mizuho Securities Research, and published on Bloomberg, the Chinese consumer market is growing as a result of the economy’s reopening. A recent survey by China Business News found that there is pent-up demand for products in the leisure, entertainment, and luxury goods categories. More than 60% of those surveyed indicated they would be willing to spend money in these categories. This is good news for the luxury industry, as China remains one of its top markets globally.

- MBA Mortgage Applications in the United States increased by 7.4% from the previous week’s fall of 5.7%. This positive reading comes after several weeks of declining application rates and indicates an uptick in economic activity. However, homebuyers could still be wary of climbing mortgage rates.

- Prada was the best performing S&P Global Luxury stock for the week, gaining 3.9%. The company reported above-expectations earnings beat for the last year thanks to strong performance in Europe. Prada also sees solid revenue growth in 2023.

Weaknesses

- Kering, Gucci and Balenciaga are having a difficult time recovering from the pandemic compared to other luxury companies. The companies’ post-Covid results compared to Louis Vuitton (LVMH), Hermès, and Prada fell short of expectations. According to Bloomberg, since 2018, Kering’s share price has increased by almost 60%, while LVMH’s has tripled. One piece of evidence pointing to a slowdown in Balenciaga was the company’s runway show last weekend. Normally, the Balenciaga runway shows are extravaganzas with fake snowstorms, techno beats, etc., but this year’s event, which took place at a location beneath the Louvre pyramid in Paris, was contrary to the norm, with minimal eccentric decor and a subdued soundtrack.

- Factory orders in the U.S. decreased by 1.6% in the month of January. This print followed December’s increase of 1.7% and came in slightly better than the market’s expectation for a decline of 1.8%. According to Reuters, the January factory orders data weakened mostly due to a plunge in civilian aircraft bookings.

- MYT Netherlands Parent, which operates the e-commerce website Mytheresa (selling luxury fashion items to consumers), was the worst performing S&P Global Luxury stock for the week, losing 23.9%. Shares continued to sell off this week after the company reported weaker financial results on February 23.

Opportunities

- On March 3, the State-owned Assets Supervision and Administration Commission (SASAC) in China called a meeting of state-owned enterprises (SOEs), requiring them to be benchmarked against world-class enterprises in value-creation activities. The CITIC Securities research team expects the valuation of central and local SEOs to “be reshaped with continued improvement of capital operation, equity incentive, and other supporting systems.” According to the CITIC Securitas report titled, “Value Creation Action Is On,” published on March 5, 2023, the SOEs’ reform will make them focus on efficiency, innovation, and sustainable development.

- The Federal Reserve’s hawkish comments this week pushed yields and the dollar higher. The yield on 2-year government bonds crossed above 5% on Wednesday, a level last seen back in 2007. A stronger dollar could prompt Americans to travel to Europe to purchase luxury goods and services abroad for less.

- Bloomberg economists predict that U.S inflation will continue to fall. The CPI data will be released on Tuesday of next week, and we could witness a decrease in the year-over-year CPI to 6.0% from 6.4% in February. At 9.1% in June of last year, inflation may have reached its high point.

Threats

- Retail sales in the U.S., which track the resale of new and used goods for personal or household consumption, are expected to decrease considerably from 3% in January to 0.2% in February. This would represent a decrease of 93% on a month-over-month basis, negatively affecting the luxury goods sector in the United States, one of the leading luxury markets worldwide. Retail sales data will be released the following week, on Wednesday.

- Tesla is having a bad month so far. Month-to-date, Tesla shares are down more than 15% and further weakness could follow. In recent months, Tesla made a few announcements cutting car prices to increase demand. This week news came out that Tesla is under investigation by U.S. regulators over complaints that the steering wheel can fall off certain new Model Y cars while in use. The National Highway Traffic Safety Administration said that around 120,000 cars were delivered to owners without the retaining belt that holds the steering wheel in place, Bloomberg reported.

- Hong Kong, one of the world’s biggest luxury shopping destinations, is losing its appeal as upscale retail spaces become vacant and well-known international brands decrease their presence in the city (in favor of establishing new stores in mainland China). According to property management companies, glitzy Hong Kong shopping streets once packed with luxury stores that attracted 56 million visitors in pre-pandemic 2019, now have about half of their shop units vacant.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was lumber, rising 2.41%, perhaps on softer interest rate expectations closing out the week. Despite some pull back in the price of lithium carbonate, China is still dependent upon imports to build out its electric vehicle infrastructure. Increasingly, China is shifting battery chemistry to lithium-iron-phosphate, which is more economical for mass production and adoption.

- Peru, the second largest producer of copper and zinc, expects to start shipping concentrates within days upon finally clearing some of the nation’s worst protests in decades. Glencore Plc and Freeport-McMoRan Inc. have both had months of constraints on the transport of the metal concentrates to the ports and likewise to get supplies to the mines.

- The increase in U.S. spot steel prices accelerated over the last two weeks, driven by two rounds of price increases, with prices up 29.4% to $1,100 per ton. Spot steel prices are up $480 per ton, or 77% since November.

Weaknesses

- The worst performing commodity for the week was natural gas, dropping 19.14%, on news that domestic stockpiles rose to a six-year high for seasonal data, collapsing the prior two-week run-in prices. Lithium prices have corrected sharply over the past three months, as demand has stalled severely. The China spot price is down 37% to $45,600 per ton since early December. That said, this is still an elevated price level from a historical perspective, remaining well clear of cost support levels. Demand weakness is especially prevalent in China, where there is reportedly ample lithium carbonate salt available.

- First Quantum Minerals reached a draft tax deal with Panama’s government over the Cobre Panama mine; this mine will resume processing after a month-long dispute. The Cobre Panama mine accounts for about 1.5% of global copper production. The Panamanians extracted significant concessions from First Quantum, highlighting the risks of operating in certain jurisdictions.

- Zinc prices headed to their lowest close in more than three months with the prospect of Peruvian production coming back onto the market. Shanghai Metals Market reports that China’s output of zinc may grow by 13% this month as smelters using domestic concentrates are maximizing production amid elevated margins, Bloomberg reports.

Opportunities

- Australia has at least 250 planned battery development projects to store solar and wind energy as it shifts away from coal. With a potential capacity of almost 130,000 megawatt-hours planned, Australia’s pipeline of storage is second only to China. While it still gets over half of its power from the burning of coal, many of the major plants are set close in the next decade.

- For 2023, the World Platinum Investment Council raised its forecast deficit for platinum, on expectations for a surge in consumption by China’s glass industry. Automotive demand for platinum is also forecast to rise 10% in 2023 to 3.25 million ounces.

- UBS estimates adjusted total 2023 copper capex is 15% below the previous peak. However, in 2023, sustaining capex is expected to account for a larger proportion of total capex versus the peak of the last cycle in 2012/2013; as a result, adjusted growth capex is 30% below the previous peak versus a global mine supply base >30% higher than it was in 2012/2013.

Threats

- Morgan Stanley reviewed February data for the European gas market. Low demand and high LNG imports continue to risk over-stocking this summer. The group sees downside to TTF to €35/MWh in order to boost demand or, more likely, divert some LNG cargoes away from Europe. Gas consumption came in 14% below the five-year seasonal average in February.

- BMO believes most of the re-rating for energy equities occurred in the second half of 2022 and are now closer to fair value. The group estimates that producers discount mid $70Bbl WTI and ~$3.70MMBTU HH on P/NAV. Energy stocks on average trade near 20-year P/E multiples. BMO sees 2023 FCF yields of 8.1% (majors), 8.8% (large cap E&P), 12.5% (SMID E&P), and 6.1% (natural gas E&P).

- Bloomberg reports that Argentina, Bolivia, and Brazil are planning to coordinate efforts to propel themselves into the electric vehicle (EV) supply chain by channeling more of the regional output into a domestic battery and manufacturing hub for EVs. Boliva, Argentina, and Chile account for 56% of global lithium resources. Chinese carmaker Chery Inc. wants to build a $400 million EV and battery plant in Argentina. Lithium prices will ultimately fall with increased production, as it is not a rare metal, but suppliers will have to find economies of scale to reach stability.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Kava, rising 13.03%.

- Voyager Digital won court approval to sell itself to Binance.US, the U.S. arm of the world’s biggest crypto exchange, after four days of contentious bankruptcy hearings. U.S. bankruptcy judge Michael Wiles said he would give Voyager permission to try to close the Binance.US sale and related payout plan which may give customers about 73% of what they are owed, writes Bloomberg.

- Cathie Wood’s Ark Invest continues to add Coinbase shares to its funds with another estimated $20.5 million purchases this week, Bloomberg reports. Shares in the crypto exchange closed down 7.8% on Thursday.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Stacks, down 30.44%.

- Silvergate shares dropped as much as 4.7% Monday morning after the bank closed its flagship crypto payments network and Moody’s cut its rating on the company. Silvergate shares plunged 60% last week after the company said it was evaluating its ability to remain viable and key partners cut ties with the firm, writes Bloomberg.

- Unease is spreading across the financial world as concerns about the stability of Silicon Valley Bank prompt prominent venture capitalists to advise startups to withdraw their money, Bloomberg explains. The turmoil followed a surprise announcement that it was issuing $2.25 billion of shares to bolster its capital position after a significant loss on its investment portfolio.

Opportunities

- Shares in numerous private crypto startups are currently being offered at sizable discounts on Birel.io, a platform that specializes in secondary market transactions. Those startups include Alchemy, Blockchai.com, Chainalysis, Kraken and more worth about $70 billion, writes Bloomberg.

- Gemini, the cryptocurrency exchange owned by the Winklevoss brothers, said its banking relationship with JPMorgan Chase remains intact, according to a Bloomberg report.

- FTX’s CEO is seeking to pay $4 million in employee retention bonuses to a select pool of key employees to stay with the company through its Chapter 11 proceedings, writes Bloomberg.

Threats

- The crypto world’s eyes will once again turn to Washington on Tuesday as oral arguments begin in Grayscale Investment’s lawsuit against the SEC. The drama centers on the $14.8 billion Grayscale Bitcoin Trust, ticker GBTC, which has for two years been trading at a steep discount to the cryptocurrency, writes Bloomberg.

- Bitcoin is having its worst week ever since November as an equity selloff, fear over higher interest rates, and an escalating U.S. regulatory crackdown on crypto combine to hurt investor sentiment, reports Bloomberg. Bitcoin fell as much 3.2% on Friday, breaking down $20,000 for first time since January.

- China-born crypto mogul Justin Sun sought to counter concerns about the strength of the Huobi exchange, one of the largest trading venues in digital assets, after a flash crash in the platform’s native token. The virtual coin halved in price at one point before paring losses, writes Bloomberg.

Gold Market

This week gold futures closed at $1,872.70, up $19.10 per ounce, or 0.98%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.07%. The S&P/TSX Venture Index came in off 4.90%. The U.S. Trade-Weighted Dollar rose just 0.10%.

Strengths

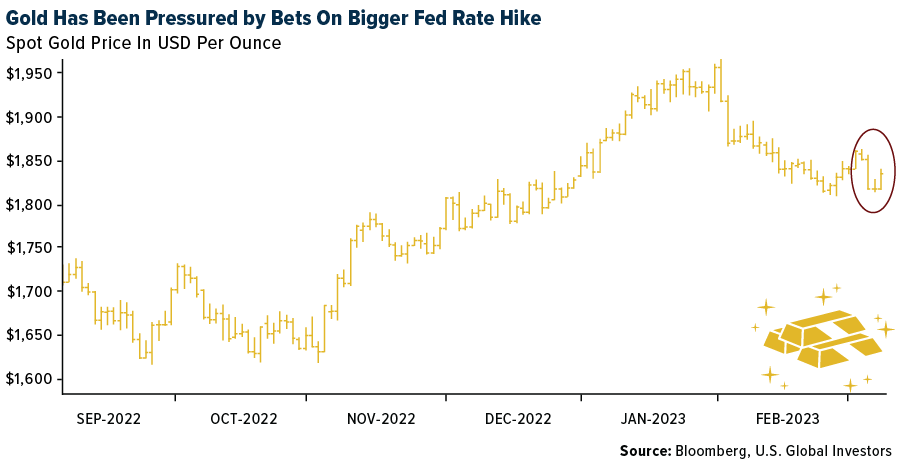

- The best performing precious metal for the week was gold, up 0.98%. Gold rose from near its lowest this year after a metric of U.S. unemployment came in higher than expected, reports Bloomberg, softening expectations that the Federal Reserve will keep aggressively raising rates. The dollar and bond yields extended declines following the report, pushing gold up as much as 1.2%.

- Despite retail gold ETF investors exiting bullion, the long-term money is making a contrary bet. The People’s Bank of China (PBOC) raised its gold holdings 25 tons in February, with current total holdings now at 2,050 tons, after the nation boosted its reserves by about 77 tons in January. Turkey purchased 23 tons of gold in January, becoming the second biggest buyer among central banks globally over this period. Singapore boosted its gold reserves by about 30% in January.

- World Gold Council data shows gold demand up 18% in 2022, to the highest level since 2011. This was second half weighted, the time when the yield relationship was changing the most. Central bank demand rose 685 tons or 150% year-over-year to a record high, offsetting ETF outflows.

Weaknesses

- The worst performing precious metal for the week was palladium, down 5.83%, in what has been a continuous slide in weekly price losses since early October. ADP Employment Change in the U.S. came in stronger than expected, strengthening the dollar against gold and gold companies. Jerome Powell’s hawkish speech on Tuesday made it sound as if the Federal Reserve is ready to be more aggressive on rate hikes in the future.

- According to UBS, gold producers have underperformed year-to-date as cash margins remain under pressure. Newmont’s scrip bid for Newcrest highlights the sector’s need to replenish inventories of wasting assets and the lack of new discoveries globally. This cycle could continue and suggests scarcity value in known operating mines and/or undeveloped deposits as grades decline and cash margins remain under pressure.

- Exchange-traded funds (ETFs) cut 392,165 troy ounces of gold from their holdings in the last trading session, bringing this year’s net sales to 1.68 million ounces, according to data compiled by Bloomberg. This was the biggest one-day decrease since December 5, 2022, and the fifth straight day of declines. As noted above, central bank buying completely offset gold ETF outflows.

Opportunities

- According to CIBC, Oceana Gold operations have significantly improved at Haile, with higher recoveries and higher mining productivity, underpinned by a labor turnover rate that has improved from 27% to 17%. Overall, CIBC observed a noticeable improvement in culture at both the site level and corporate level that it believes has been a key driver to a much more profitable operation. National Bank Financial also penned a positive review and expects that production from the underground mine will ramp up in the fourth quarter of 2023 and will start contributing ore to the mill, helping to boost production higher and lower operating cost per ounce.

- Agnico Eagle Mines is weighing what to do with its only Australian gold mine after landing two big takeovers within two years that turned the Canadian company into the world’s third-largest gold producer. Agnico gained an Australian mine as part of its combination with Kirkland Lake Gold Ltd., giving it a foothold into a region beyond its North American focus. Agnico’s latest deal, set to close this month, reinforces the Toronto-based firm’s homegrown roots by taking full control of the Canadian Malartic mine in Quebec.

- The collapse of Silicon Vally Bank falling under FDIC control, along with a number of other regional banks being heavily scrutinized, had a big influence on bond markets this week. Investors began transferring money from bank deposits to U.S. treasuries with much higher yields. The U.S. dollar lost all of its gains for the week, and on Friday, FED swaps fully priced in a 25-basis point rate cut by year-end. The beneficiary was gold and silver, where prices have grown, and will grow more if the Federal Reserve becomes less hawkish.

Threats

- Marathon Gold noted that the early works were completed in its new major expansion, but engineering was behind plan of 68% (at 61%) because of delays in process plant engineering due to resource availability and rework on construction packages and layouts. The company noted that the overall permitting progress was at 71% versus the plan of 93%.

- According to Morgan Stanley, gold did not fall as much as the rise in real yields would have implied. Using the 2018-2021 regression, the second half 2022 move in real rates from 0.67% to 1.57% would have taken gold down 18%. Instead, the price was flat. Rising safe haven demand may have played a part, but this really only drove inflows through the first quarter.

- Future economic data points, primarily those that impact the power of the U.S. dollar, along with the Federal Reserve’s decision about rates, continue to be risks for the gold market. Economic forecasts by Bloomberg also show the probability of recession at 60% currently.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

IAMGOLD Corporation

Newmont

Agnico Eagle Mines

Oceana Gold

Azul Airlines

Boeing

Deutsche Lufthansa

American Airlines

JetBlue Airways

Kering

Hermes

Prada

LVMH Moet Hennessey

Tesla

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All