Chapter 1 – The success story

The competitiveness of China compared to the western world has been widely discussed in several areas such as semiconductors, EVs or 5G technology. However, one additional area where China has become a big success story is the development of a domestic internet ecosystem. The Chinese internet space is the only real competitor to the global hegemony of the US internet behemoths, as even the self-grown internet platforms in countries such as Korea or Japan can hardly be considered equal. There are multiple structural reasons why China has succeeded where most others have not – these reasons include the considerable size of the Chinese market (the most populous country in the world and the world’s 2nd largest economy), distinctive language and writing system, different preferences of consumers and, very importantly, the reluctance of the US internet behemoths to localize their products (which were successful in the west) to the specifics of the Chinese market – Google was a prime example of this.

The resounding success of the Chinese internet juggernauts has also led to massive gains for many investors, especially in the initial phases, such as for the South African Naspers – the company which has built its fortunes around its early investment in Tencent, the largest Chinese gaming and messaging company. The Chinese internet space gained wider attention in the western investment community back in 2014, at the time of the US IPO of the largest Chinese e-commerce platform Alibaba. The IPO heralded the advent of the ‘golden age’ of the Chinese internet. In the years that followed (notable 2016 to 2020), the Chinese internet platform stocks rallied and led the emerging market’s returns. The weight of the Chinese internet platforms in the MSCI EM index even exceeded 20% and and one could often find a simple strategy to beat the index among the top-performing EM funds – holding large weights in the big Chinese internet platforms, hoping that the Chinese internet rally would continue. At the same time, the first cracks in the Chinese platforms success story started appearing. Several segments of the Chinese internet space had already entered the maturation phase (e.g. the Chinese e-commerce penetration level became the 2nd highest in the world, only lagging South Korea – raising doubts about additional growth potential) and the founders of the Chinese internet behemoth became increasingly bold after amassing huge wealth, which necessarily leads to rising influence, which could step on the toes of the country leadership in Beijing. We believe some index-beating EM funds of the 2016-2020 era could have built their success on going big on the Chinese internet platforms, and did not see these potential risks brewing, or worse, ignored them as they were unable or unwilling to find a different way to outperform the index focusing on stock selection. In the meantime, the boom part of the Chinese internet sector story was coming to an end.

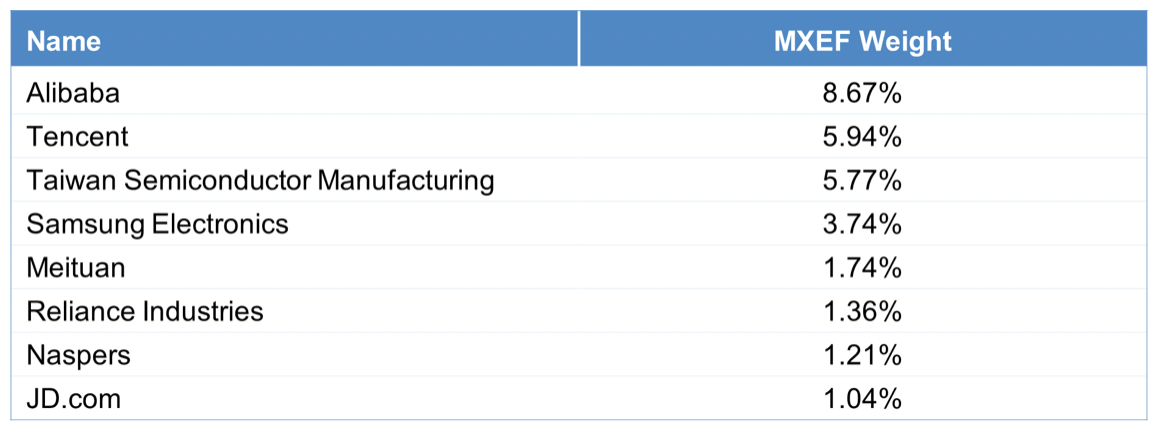

Chart 1: The largest MSCI Emerging Markets index (MXEF) weights as of September 30 2020 (around the top of the Chinese internet rally) – the MXEF index was heavily dominated by the Chinese internet names as 5 out of the 8 top names were related to the Chinese internet platforms and the overall MXEF weight of Chinese internet platforms exceeded 20%

Source: Bloomberg as of September 30, 2020

Chapter 2 – The bust story

The Ant Group’s IPO was supposed to be the capital markets event of 2020. The financial and payments arm of Alibaba targeted to raise $34bn (implying a total valuation of over $300bn) in what was set to become the world’s largest IPO ever. The IPO seemed to be progressing well, with books several times oversubscribed. However, only two days before the IPO was supposed to happen, the deal took a shocking turn because the Chinese regulators suspended the IPO offering. The official reason for suspending the IPO was a regulatory overhaul of the financial arm’s business as the Chinese regulators became concerned with the rising systemic risks. Ant Group effectively became one of the largest consumer lending and payments companies in China, but several key regulations applicable to financial companies did not apply to it due to its internet platform status (eg the vast majority of its lending was not funded through its own balance sheet but through 3rd party banks). What hardly helped Alibaba’s case was that Jack Ma, the billionaire founder of Alibaba, publicly criticized the Chinese regulators for being inflexible, insinuating that they do not fully understand the internet sector development, a message which might have been seen as dangerously close to criticizing the top country’s leadership in Beijing.

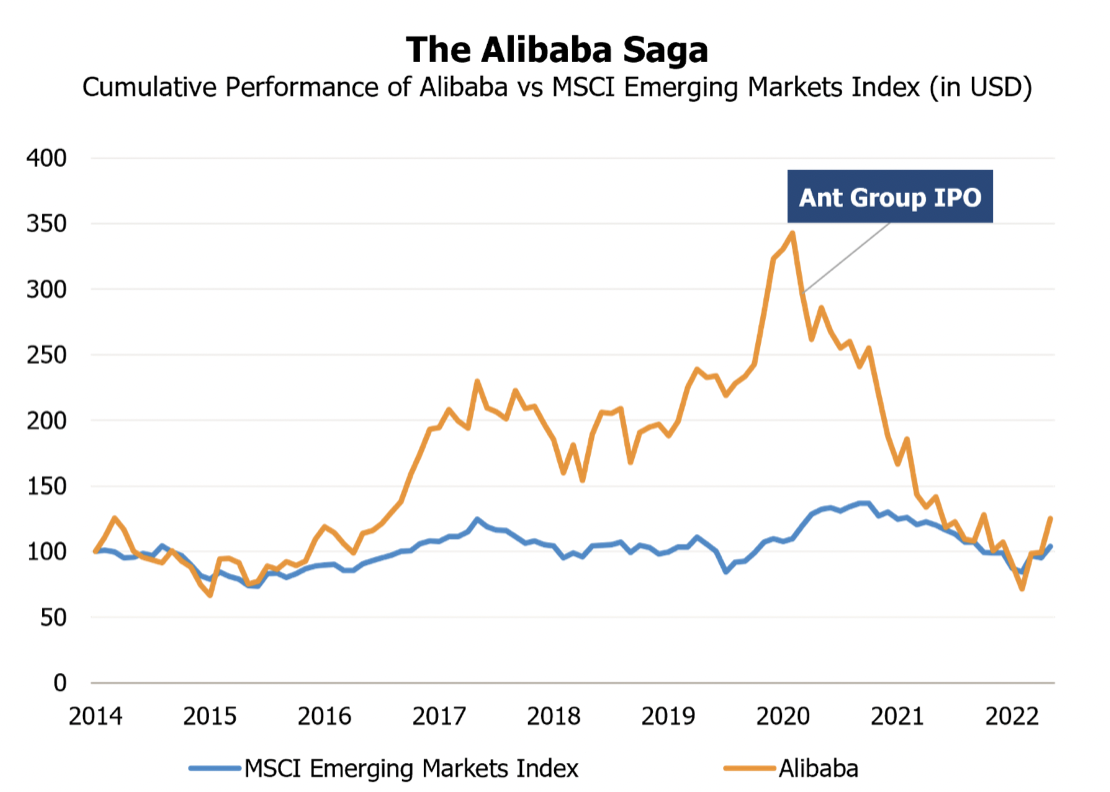

Chart 2: The suspension of Ant Group’s IPO in late 2020 marked the end of multi-year outperformance of the Chinese internet space – the boom cycle (and was followed by a 2-year period of under-performance – the bust cycle)

Source: Bloomberg September 30, 2014 - January 31, 2023

In the following weeks and months, it turned out that the last-minute suspension of Ant Group’s IPO was the opening shot in a much wider crackdown on the Chinese internet platforms, which went far beyond Ant Group. Soon after the suspension, an antimonopoly investigation into Alibaba and the Chinese e-commerce sector started. Alibaba was gradually forced to face allegations and investigations into its presumed monopolistic behaviour, calls to slash its payments fees and e-commerce take rates to support the Chinese SMEs and broader economy, new regulations to open up its ecosystem to competitors (particularly to WeChat Pay from Tencent), its algorithms came under scrutiny, the Chinese State-owned Enterprises (SOE) were warned against using 3rd party cloud software (including AliCloud) and Alibaba’s ties to Hangzhou’s local government officials were investigated. Jack Ma was not seen in public for months. The other major Chinese internet platforms faced similar fortunes to a large extent. Several regulatory initiatives hit Tencent, and its business was particularly heavily hit by an effective freeze on new game approvals, which lasted for several months. A particularly unsettling case was the story of Didi, the leading Chinese ride-hailing app, which faced an outright ban on acquiring new users due to regulatory concerns shortly after its IPO – the ban lasted for over a year. ByteDance, the Chinese owner of TikTok, decided to walk away from its IPO plans – a move which seemed to be sensible with the stories of Ant Group and Didi in fresh memory. The US efforts to audit working papers of the Chinees companies listed in the US or face delisting and the Chinese unwillingness to allow this also added to the pressure.

These developments force emerging market investors to contemplate their approach to the Chinese internet platforms. We grew cautious about the Chinese internet platforms during the exuberant years before 2020. The rising regulatory risks (described above) were the first reason, but adhering to our philosophy was equally important. Our investment approach is to generate alpha by investing in structural growth stories and recovery growth stories, and we think that most alpha in EMs can be created for investors by nimble stock selection, often in the under-covered areas of the market – none of which applied to the Chinese internet platforms during the rally before 2020. Some investors could argue that the Chinese internets were still structural growth story at this point, but our view was that the high penetration rates combined with regulation question marks posed serious risks to the growth argument. And by no means could these stocks be considered to belong to the ‘recovery’, ‘timely’ or ’under-covered’ category at the time as they were already well-researched, and the stock moves were extended. After the full-scale crackdown on the Chinese internet started in late 2020, we decided to cut our positions further and stay underweight for the following two years. The bust cycle in the Chinese internet sector went into full swing in the 4th quarter of 2022; the Chinese internet stocks reached multi-year lows after they were hit by the Chinese macro woes along with the rest of China, largely caused by the stubborn zero covid policy.

Chapter 3 – Are the fortunes turning again?

While the markets seem to have given up on the Chinese internet sector, we are beginning to see an opportunity, a potential recovery growth story. With valuations at very depressed levels and following a massive foreign investor exodus, the termination of the zero covid policy is a big positive macro driver for the whole of China. And very importantly, we have seen signs of the improving regulatory and political approach to the Chinese platforms, starting from the very top. The top Chinese regulatory and government bodies have recently publicly recognized the importance of the healthy development of the Chinese internet sector for the economy. This is a logical step from an economic perspective, and the Chinese leadership is looking for ways to support the economy after nearly three years of lockdowns, and easing the regulatory crackdown on one of the largest Chinese sectors seems to be one of the easiest and least costly paths to take.

The top-level message has also resulted in specific regulatory measures easing the pressure on the Chinese internet stocks. The Chinese internet juggernauts have largely been able to address the main regulatory concerns in the areas such as monopolistic practices (we have seen opening up of ecosystems) and conglomerate structure (in case of Ant / Alibaba). New game approvals have started being reissued, in fact, dozens of new game licenses were issued in December 2022. Alibaba was even able to sign a cooperation agreement with the Hangzhou local government on online platform economy development, and Jack Ma has been busy publicly meeting prominent financial figures in Hong Kong; implicitly suggesting that the door to cooperation with both the public and private sector is opened once again for Alibaba. Talks of new IPOs in the sector have started circulating in the media again. And finally, China has also shown a willingness to cooperate with the US in allowing access to the audit working papers to keep the Chinese ADRs listed in the US.

Perhaps surprisingly for some, we would say that the attractiveness of the Chinese internet space has also been increasing globally. We do not doubt that regulatory risks are here to stay in the case of the Chinese internet platforms and the Chinese government will retain its ‘quasi-veto’ power through both formal (eg golden shares and regulatory approval processes) and informal means (eg prospects of angering Beijing will keep most platforms from implementing measures unpopular with the government). However, the regulatory risks of the Chinese internet space are well-known among investors at this point and, we believe are mostly priced in. We do not think the same can be said about the internet space in many other countries, particularly in the US. Time might show that investors are putting an excessive premium on the ‘safer’ perception of the US internet space. In fact, the regulatory downside for the US internet behemoths might outweigh the geopolitical risks of investing in Chinese internet stocks.

Chapter 4 – What are the lessons?

What does the future hold for Chinese internet platforms in the long term? Our view is that the long-term structural growth outlook for the sector is not particularly rosy due to high penetration levels and structural regulatory risks (even if they are already well understood by investors at this point). However, as investors, we do not only invest in ‘structural growth’ stories. The Chinese internet story has become interesting for the second leg of our dual-approach philosophy, which is recovery growth. We can see most, if not all, ingredients essential for the success of recovery growth present in the Chinese internet sector now, with fundamentals bottoming out and showing early signs of improvement (easing regulation after a two year long crackdown and a rebound in consumer spending after nearly 3 years of a zero covid policy), and the first EPS estimates upgrades after a long period of downgrades. At the same time, most of the investor community is still overly negative and underweight in the sector. This is the reason why we have been increasing our weight in the Chinese internet space over the past few weeks.

And what do we think the recent developments in the Chinese internet space mean for emerging markets in general? Some investors would simply argue that the weak performance of the Chinese internet sector during the past two years has been ‘bad’ for emerging markets investing in general due to the high EM benchmark index weights of these names. We think that this view is overly simplistic. The past 2 years have simply uncovered the positive added value of stock-picking and bottom-up approach as opposed to ‘benchmark-hugging’ and trying to outperform competitors by having huge weights in the largest benchmark stocks.We think we are well-positioned in this new environment due to our bottom-up stock-picking approach, added focus on under-covered small- and mid-cap stocks, robust philosophy and rigorous process.

Source for all data JOHCM/Bloomberg (unless otherwise stated)

An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing or sending any money. This and other important information about the Fund can be found in the Fund’s prospectus or summary prospectus, which can be obtained at www.johcm.com or by calling 866-260-9549 or 312-557-5913. Please read the prospectus or summary prospectus carefully before investing. The JOHCM Funds are advised by JOHCM (USA) Inc. and distributed through JOHCM Funds Distributors, LLC. The JOHCM Funds are not FDIC-insured, may lose value, and have no bank guarantee.

Past performance is no guarantee of future results.

RISK CONSIDERATIONS:

The Fund invests in international and emerging markets. International investments involve special risks, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. Such risks include new and rapidly changing political and economic structures, which may cause instability; underdeveloped securities markets; and higher likelihood of high levels of inflation, deflation or currency devaluations.

Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

The small- and mid-cap companies in which the Fund may invest may be more vulnerable to adverse business or economic events than larger companies and may be more volatile; the price movements of the Fund’s shares may reflect that volatility.

The views expressed are those of the portfolio manager as of February 2023, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice.

Read more commentaries by J O Hambro Capital Management