The GMO Focused Equity team has evaluated banks in the context of our Quality Strategy for 20 years, using both quantitative and fundamental analysis to invest in high-quality banks with healthy financials and in our opinion responsible management practices. We are not exposed to the banks currently in crisis, but with the industry in turmoil, we have been examining the triggers to measure risk levels across the global banking sector.

The Fall of SVB and the Threat of Contagion

In many ways, Silicon Valley Bank (SVB) was an oncoming train wreck hiding in plain sight. It faced a fairly unique combination of issues that were exacerbated by today’s similarly unique market environment:

- 52% of SVB’s deposits were from private equity and venture capital-backed start-ups. As growth companies melted down in 2022, these start-ups burned through cash, drawing down their deposits. As a result, deposit accounts at SVB had been falling sharply for nine months.

- With rates rising at the fastest pace in decades, SVB experienced rapid deterioration of its net interest yield (NIY). 1 Higher rates meant SVB had to chase deposits by offering higher yields, increasing its deposit yield by 2.2% in 2022. Meanwhile, it was invested heavily in fixed-rate, long-duration securities, with a smaller amount in higher-yielding loans, 2 and so its investment yields were only up 1.4%. As a result, SVB had a difficult time maintaining its NIY. In fact, in Q3 2022, a period when most banks had rising NIYs, SVB’s overall NIY actually started falling.

- A full realization of SVB’s Available-for-Sale (AFS) and Held-to-Maturity (HTM) securities losses would have roughly wiped out tangible book.

As has been widely reported, the tightly networked deposit base reacted to these worrying signs by accelerating deposit withdrawals in February, forcing SVB to sell its entire AFS portfolio and realize those losses, ultimately ending in the bank’s collapse.

In considering whether SVB’s failure might signal a contagion, we have reviewed other U.S. regional banks and found that those most at risk have similar attributes as SVB:

- High VC/PE/Crypto exposure,

- High average balances above FDIC insurance limits,

- Rapidly declining deposits over the past year, and

- A high percentage of assets invested in long-duration debt securities that have been generating unrealized losses as rates have risen.

The immediate issue for this group was resolved by the U.S. government’s backing of all SVB and Signature Bank (SBNY) deposits, showing a commitment to protect depositors. In an equally significant move, the Fed introduced the Bank Term Funding Program, whereby banks have unlimited access to the Fed discount window and are able to withdraw funds for up to one year using HTM securities at par value as collateral to help fund excess deposit draws. What this means is banks will not be forced to sell securities and realize losses if deposit withdrawals speed up.

These actions should inspire confidence and reduce the velocity of deposit outflows – and as a result reduce the threat of contagion. However, depositors and market participants alike continue to worry about these banks and the financial sector more broadly amid many unanswered questions about what might be next.

In our view, the U.S. government should go further. The Fed has blood on its hands. These banks were acting rationally by investing in long-duration assets at a time when the Fed was erroneously signaling that rates would stay low in the face of “transitory” inflation. We think a statement from the Fed and Treasury that they will temporarily back all domestic deposits would likely cease deposit migration and end the crisis, while costing the government little. There is precedent here – at the outset of Covid, the Fed pledged to buy unlimited corporate bonds, a $10 trillion promise. In the end, the Fed only had to buy $14 billion in bonds and was able to stabilize the market. Sometimes a statement of support can be more important than actual action.

Safety in High-Quality Banks

We look for high-quality banks with established track records of historical profitability and strong fundamentals, those with healthy financials that should be able to outgrow their peers with less risk. But all banks, even high-quality ones, have unrealized losses in their AFS and HTM debt securities portfolios, born of the Covid crisis. As deposits surged at banking institutions due to factors like stimulus payments and slowed spending, without loan demand to match, banks invested in long duration debt securities near the bottom in rates. Fast-forward to today, and rising rates have led to unrealized losses in these portfolios. For banks that have considerably larger securities portfolios relative to loan books, things could get tight as the inflation fight continues and short rates (deposit rates) are pressured higher against fixed-rate, long-duration securities portfolios.

Some argue that HTM unrealized losses, which are not included in tangible book or regulatory capital values, should be more actively considered. This would raise questions around the potential impact on leverage and regulatory considerations if banks were to face an event like a deposit run.

We subscribe to a less discussed, counter “economic reality” philosophy. This approach entails re-valuing deposits that have become significantly more valuable to banks in a 4-5% short rate environment. Bank of America, for instance, has $170 billion in tangible book value and $109 billion in HTM securities losses that are not factored into tangible book. But its $2 trillion deposit base is also not marked to market and on December 31 was yielding about 1% on average. Those deposits are probably worth a lot more than $109 billion and yet are not factored into tangible book. These are the types of considerations we analyze when evaluating high-quality banks.

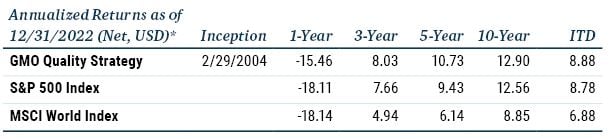

Overall, the GMO Quality Strategy has delivered defensive performance since the crisis came to a head on March 9, outperforming the S&P 500 by nearly 150 bps in the seven trading days from March 10 through the writing of this piece. Within the GMO Quality Strategy, our bank holdings have been under pressure since SVB collapsed, but they have significantly outperformed the more distressed and less well-diversified names. This reflects the downside protection associated with investing in high-quality stocks, even amid ongoing concerns about widespread banking contagion, potential for future regulation, and increased scrutiny on Fed moves. High-quality banks tend to be systematically important and typically have defensive characteristics that safeguard them against train wrecks like SVB.

Download article here.

Performance data quoted represents past performance and is not predictive of future performance.

Returns are presented after the deduction of a model advisory fee and a model incentive fee if applicable. Net returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. A GIPS compliant presentation of composite performance has preceded this presentation in the past 12 months or accompanies this presentation, and is also available at www.gmo.com. Actual fees are disclosed in Part 2 of GMO’s Form ADV and are also available in each strategy’s compliant presentation. Fees paid by accounts within the composite may be higher or lower than the model fees used.

1 NIY is a measure of the investment income a bank earns compared to the outgoing interest it pays.

2 Compounding SVB’s issues, over 60% of its loan book had been to private equity and venture capital firms.

Disclaimer: The views expressed are the views of Ty Cobb and Kim Mayer through the period ending March 21, 2023, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2023 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO