The Top Three Catalysts For Higher Gold Prices In 2023

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGold appears to be well-positioned for a strong pump that could carry it to new all-time high prices in 2023—and beyond. As you know, I’ve been following and writing about the precious metal market for a very long time, and I see a number of unique catalysts at the moment that could contribute to higher gold prices. If you’re underexposed or have no exposure, it may be time to consider changing that.

Below are just three potential catalysts.

Emergence Of A Multipolar World And Rapid Dedollarization

I’ll begin with what I believe to be the biggest risk that could be beneficial for gold prices: dedollarization. In last week’s commentary, I wrote about the end of the petrodollar and the possible emergence of a multipolar world, with U.S. on one side and China on the other.

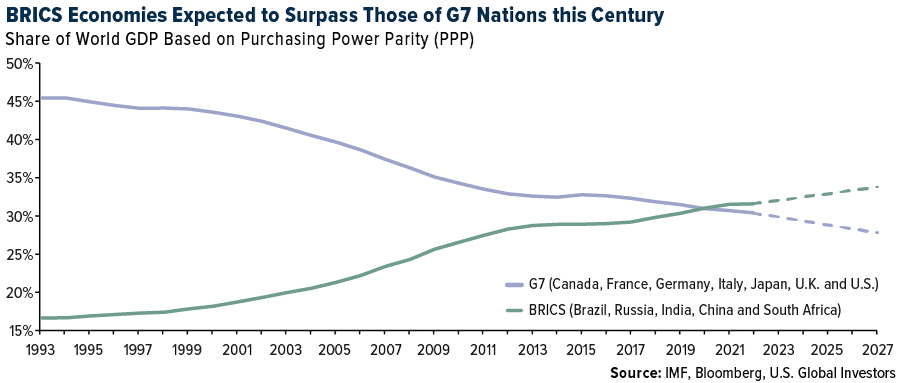

Take a look at the chart below. The purple line shows the combined economies of G7 nations (Canada, France, Germany, Italy, Japan, the U.K. and the U.S.) as a share of global GDP, in purchasing parity terms. The green line shows the same, but for BRICS countries (Brazil, Russia, India, China and South Africa). As you can see, G7 economies have steadily been losing their economic dominance to the BRICS—China and India, in particular. Today, for the first time ever, the leading developed countries contribute less to global GDP than the leading emerging countries.

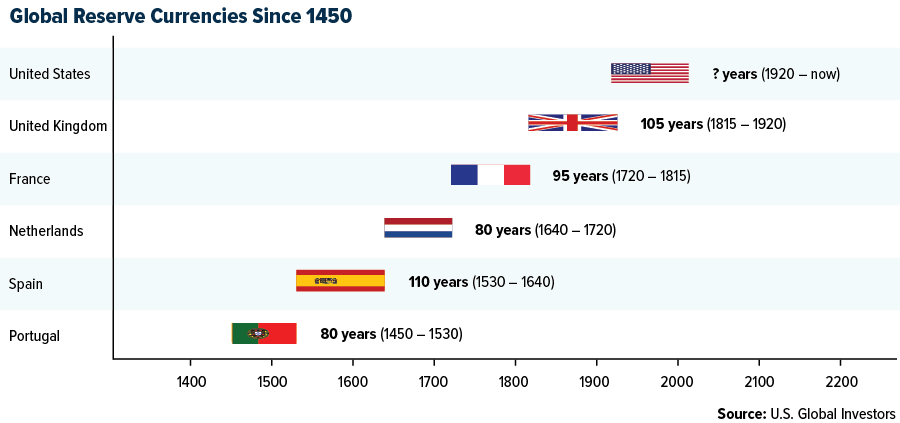

The implications of this could be multi-faceted, but for our purposes here, let’s focus just on currencies. Since the end of World War I, the U.S. dollar has served as the world’s reserve currency, and since the 1970s, crude oil and other key commodities—including gold—have traded globally in greenbacks.

That may be set to change with the rise of a multipolar world in which half of all commodities are traded in U.S. dollars, the other half in another currency—the Chinese yuan, perhaps, or a BRICS currency of some kind, or a digital currency such as Bitcoin.

An increasing share of commodities is already being settled in non-dollar currencies. This week, China settled a liquid natural gas (LNG) trade with France in yuan for the first time ever as the Asian giant seeks to expand its economic influence around the world. Since Russia’s invasion of Ukraine last year and the international sanctions that followed, Russia’s de facto reserve currency has been the yuan, according to Kitco News.

Some economists believe the time is right for a major competitor to the dollar to step up. Jim O’Neil, the former Goldman Sachs economist who coined the acronym BRIC, wrote an essay last weekend urging BRICS nations to challenge the greenback’s dominance, saying that shifts in U.S. monetary policy create dramatic fluctuations in the value of the dollar that affect the rest of the world.

Gold would be a direct beneficiary of dedollarization since it’s priced in the greenback. Gold is trading at or near all-time highs in a number of currencies right now, including the British pound, Japanese yen, Indian rupee and Australian dollar, and it would likely be hitting new highs in USD terms as well were the dollar to be devalued.

Acceleration Of The Liquidity Crisis And Return Of Quantitative Easing (QE)

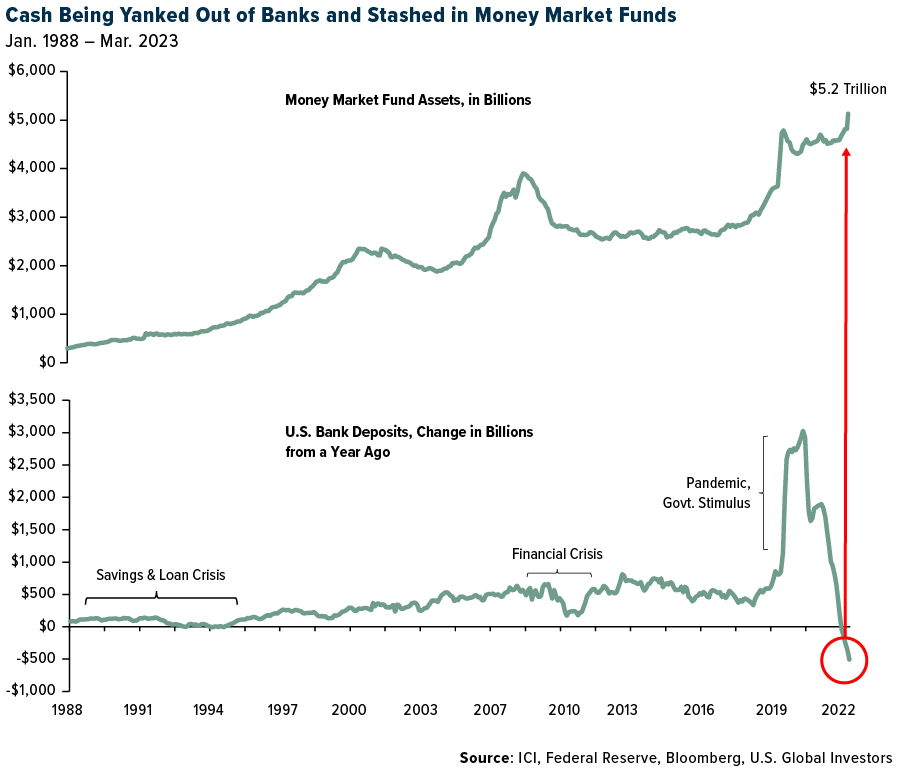

The next potential catalyst has to do with the ongoing shakiness of certain segments of the traditional financial sector. Pressured under an estimated $620 billion in unrealized losses, the U.S. banking industry has seen the failure of two large firms this year—Silicon Valley Bank (SVB) and Signature Bank—and a significant erosion in depositors’ confidence.

As a result of these failures, people and companies have withdrawn tens of billions of dollars from banks. In March, bank deposits were down more than $500 billion compared to the same month in 2022, a more dramatic year-over-year change than the savings and loan crisis in the 1980s and 1990s and the financial crisis.

Where is all this capital going? Money market funds, which are perceived to be safer and, in many cases, deliver higher yields than savings accounts right now. A record $5.2 trillion now sit in these funds, according to the Investment Company Institute (ICI), and the stockpile is expected to get much higher.

Many regional and community banks were already facing a liquidity crunch due to massive unrealized losses, and the sudden withdrawals will only amplify things. As reserves drop, banks will become less and less willing to lend to households and businesses, slowing the economy even more than the Federal Reserve’s rate hikes.

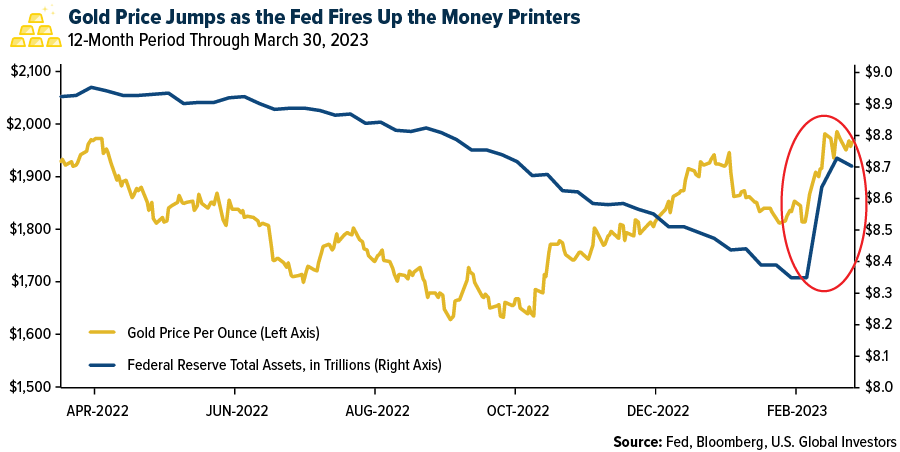

In the event that the liquidity crisis expands into a full-blown recession, the Fed will have no other choice than to pivot and begin another cycle of quantitative easing (QE). The central bank has been trying to unwind its balance sheet, but in an effort to stabilize the banking sector, it added nearly $400 billion in the two weeks ended March 22. Over the same period, the price of gold jumped 8.6%, reversing its 2023 losses.

Two Cold Wars

The final catalyst on my list involves worsening diplomacy between the U.S. and its allies and Russia and China. Relations between the West and the East are about as bad as I remember them ever being, and they could get way worse before they get better.

In recent interviews and webcasts, I’ve been saying that the U.S. is facing two Cold Wars right now with Russia and China. I hope that these conflicts remain “cold,” but there’s always the possibility that they become something more—in which case, I would want to have exposure to gold.

I won’t spend a whole lot of time on this topic, but I want to point you to a recent article that appeared in Foreign Affairs. According to the article’s two contributors, Chinese Leader Xi Jinping appears to be shoring up his country’s military readiness by increasing the defense budget and building new air-raid shelters in key cities and “National Defense Mobilization” offices. “Something has changed in Beijing that policymakers and business leaders worldwide cannot afford to ignore,” the piece reads.

Whether the military build-up is a precursor to an invasion of Taiwan or something else remains to be seen.

What I do know is that investors have put their trust in gold in times of geopolitical risk and uncertainty. I’ve always advocated for the 10% Golden Rule, with 5% in physical gold (bars and coins) and the other 5% in high-quality gold mining stocks, mutual funds and ETFs.

Index Summary

- The major market indices finished up. The Dow Jones Industrial Average gained 3.22%. The S&P 500 Stock Index rose 3.13%, while the Nasdaq Composite climbed 3.37%. The Russell 2000 small capitalization index gained 3.59% this week.

- The Hang Seng Composite gained 72% this week; while Taiwan was down 0.29% and the KOSPI rose 2.56%.

- The 10-year Treasury bond yield rose 0.103 basis points to 3.48%.

Airlines And Shipping

Strengths

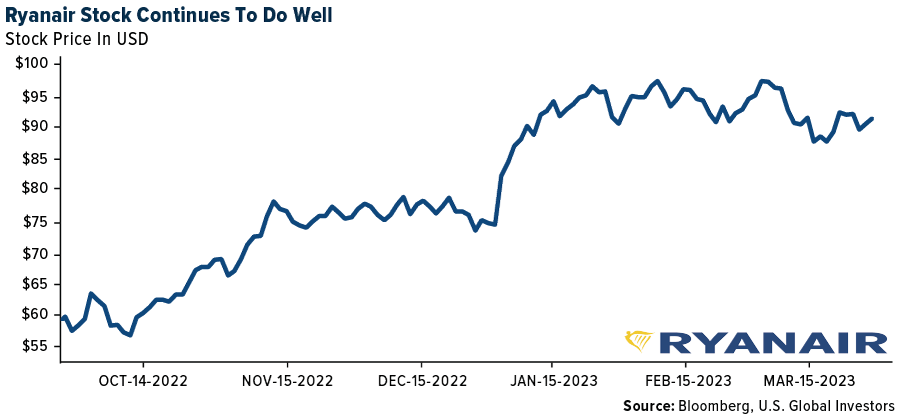

- The best performing airline stock for the week was Hawaiian Air, up 17.4%. Ryanair CEO Michael O’Leary gave comments to The Telegraph last week that average summer fares could be up 10-15% year-over-year, given the continuing recovery in demand and limited capacity growth in Europe. Mr. O’Leary sees “no evidence of people not spending at all. And that is not confined to the UK, [it is] all over Europe.”

- Maersk isn’t idling any of its ships yet because the company expects to be able to deal with overcapacity in the container shipping market by reducing vessel speed, so-called slow steaming, CEO Vincent Clerc says. Maersk has been able to effectively lower its capacity by 7-8% through slow steaming so far and expects to reach a reduction of 8-9%, Clerc says in a Copenhagen briefing after the AGM. “This means there’s no need to idle ships,” Clerc says, and Maersk “would look at some of the ships we have charted as the next step” if the shipping line needs to further cut capacity. Maersk is ready to change tactics if market conditions change for the worse, he says.

- European airline bookings as a portion of 2019 levels improved significantly to +3% in the week. Total net sales were up +2% this week. Intra-Europe net sales was up 19 points to -4% versus 2019 (versus -23% in prior week) and were +4% higher this week. International net sales improved by 21 points to +6% versus 2019 (versus -15% in the prior week), and were up +1% this week. Intra-Europe/international volumes increased by 12 points/18 points to -16%/-10% versus 2019. Pricing remains above 2019 levels with intra Europe/international prices at +15%/+17% above 2019 levels respectively.

Weaknesses

- The worst performing airline stock for the week was Turkish Air, down 7.7%. Earlier this week, Fitch Ratings revised GOL’s Long-Term Foreign and Local Currency Issuer Default Ratings to ‘C,’ following the airline’s debt restructuring plan, which Fitch deems to be indicative of a distressed debt exchange.

- Navigator reported 4Q22 continuing earnings per share (EPS) of $0.08, below consensus of $0.22. FY22 EPS came in at $0.32 versus $0.35 in FY21. Ethylene throughput at the Marine Export terminal came in below guidance (270,000 tons), totaling 262,835 tons in 4Q22 (+12% YOY); for FY22, total ethylene throughput volumes were 987,529 tons, close to nameplate capacity of 1,000,000 tons per year. The company estimates that 1Q23 ethylene export volumes will be 260,000 tons (above nameplate capacity of 250,000 tons), as ethylene exports remained strong in the first months of the year.

- System net sales fell 3.0% versus 2019 for the week compared to -1.2% last week. The decline was driven by pricing (+9.5% versus 2019 compared to +12.3% last week) while volumes modestly improved (-11.5% versus 2019 compared to -12.0% versus 2019 last week). Last week, the regional banking headlines could be driving a near term softening in booking trends, and the most recent data shows corporate channels are softer than leisure channels. Net sales through leisure channels were mostly unchanged versus last week while net sales in large corporate and SME channels decelerated 130 basis points and 340 basis points, respectively.

Opportunities

- India remains one of the fastest-growing aviation markets across the globe. The market is significantly under-penetrated. India’s airline seats per capita stand at 0.13 versus 0.49 for China and 3.1 for the U.S. Further, India has 700 aircraft operating currently (versus China at >4,000 aircraft), and by 2027, demand is likely to be around 1,100 aircraft, per the India Brand Equity Foundation. Government support through building new airports (target of 220 airports by 2025 from 140 currently), upgrade of existing airport infrastructure, Regional Connectivity Schemes and reduction of VAT on jet fuel by state governments is supporting growth in the industry.

- The inventory-to-sales ratio (1.23x) remains below the normal ratio of 1.45x seen during 2010-19. Furthermore, analysis of freight rates indicates that current rates are close to 2018-19 levels, which implies limited downside risk of 3-10% across major shipping routes. The above reaffirmed the perspective that the container shipping sector is clearly turning the corner following the sharp spot freight rate correction, with Chinese ports witnessing a sequential pickup and poised to gain further momentum in 2H23.

- American Airlines is increasing its flights to Europe this summer by 14% YOY, according to Business Traveler. According to the article, American will offer up to 64 daily flights to European destinations, and nearly half of those will operate into London Heathrow airport, which according to management is a good place to be right now. Management also recently noted that they expect further improvement in demand for long-haul international travel this year as they continue to grow back their capacity.

Threats

- According to AEROIN, Colombian authorities have approved Viva Air’s acquisition by Avianca; however, the former indicated that the integration with Viva is still uncertain, with the conditions not reflective of those that were in place when the original request for the process was made, signaling a potential discontinuation of the deal. In that sense, Avianca comments that the diminished capabilities of Viva Air, including its route network, aircraft and workforce, due to the suspension of operations should be thoroughly evaluated to assess the viability of the requirements set by Civil Aviation. Lastly, Avianca indicates that the resolution is not final as this decision is subject to appeal and reintegration not only by the parties involved, but also by interested third parties recognized by the authority.

- According to Morgan Stanley, the volume of newly-built container ships so far in 2023 stands at only about 11% of their forecast for new supply arriving this year. They expect concerns about supply/demand deterioration due to pressure from supply of new ships to kick in fully at some point.

- China’s economic rebound is weaker than expected as consumers emerge “stunned” from pandemic-led disruptions and a real estate meltdown last year, according to the head of Maersk. This implies the risk that air travel growth may be stunted in the future in China.

Luxury Goods And International Markets

Strengths

- Luxury stocks continue to move higher, recording a strong weekly and quarterly performance. On the weekly basis, the S&P Apparel & Accessories Composite Index rose as much as 7.53%, this week outperforming the broad S&P 1500 Composite Index, which increased by 4.22%. On a quarterly basis, the S&P Apparel & Accessories Composite Index gained 7.19% while the S&P 1500 was little change, gaining only 0.55%.

- Tesla’s January sales were up 34% compared to a year ago, while BMW’s were up just 2.5%, Mercedes’ 7.3%. Lexus saw a 6.6% sales drop. According to Experian data from January 2023, the electric carmaker recorded nearly 50,000 new registrations in the U.S., which is a massive lead over second-place BMW, with around 31,000 registrations.

- PVH Corporation was the best-performing S&P Global Luxury stock for the week, gaining 20.71%. Shares of the Tommy Hilfiger and Calvin Klein’s parent company jumped 19% midday Tuesday after the company reported fourth-quarter earnings that significantly beat. Jay Sole from UBS said the company is now prepared to boost earnings per share by a double-digit compounded annual growth rate.

Weaknesses

- In the United States, the Conference Board Consumer Confidence Index was reported at 104.2 in March vs. the expected reading of 101.0 and February’s 102.9. Consumer confidence in Germany, Europe’s largest economy, improved slightly as well. The GfK Consumer Confidence index was reported at a negative 29.5 vs. an expected negative 30.0, and the prior month’s negative 30.5.

- The Kuwait Investment Authority sold shares worth about 1.4 billion euros in Mercedes-Benz Group AG after the carmaker’s equity quadrupled over the last three years, Bloomberg reports. The sale, which represents about 1.9% of Mercedes’s share capital, was priced at 69.27 euros. The price was a 3.6% discount to the stock’s Tuesday closing price.

- Faraday Future Intelligence was the worst-performing S&P Global Luxury stock for the week, losing 10.81%. Shares fell sharply despite the company announcing production start for the long-awaited FF 91 Futurist car on March 29. This model will compete with high-end luxury cars like Ferrari, Maybach, Rolls Royce and Bentley.

Opportunities

- Luxury brand Gucci announced a multi-year partnership with Yuga Labs to develop Web3 applications. Gucci sees Web3 as a long-term opportunity to develop a relationship with young customers, drive customer loyalty and ultimately generate revenue. According to a 2021 JPMorgan report, metaverse and non-fungible token (NFT) games could account for 10% of the luxury goods market by 2030. This will create a 50 billion euro revenue opportunity with a total market growth of around 25% per annum.

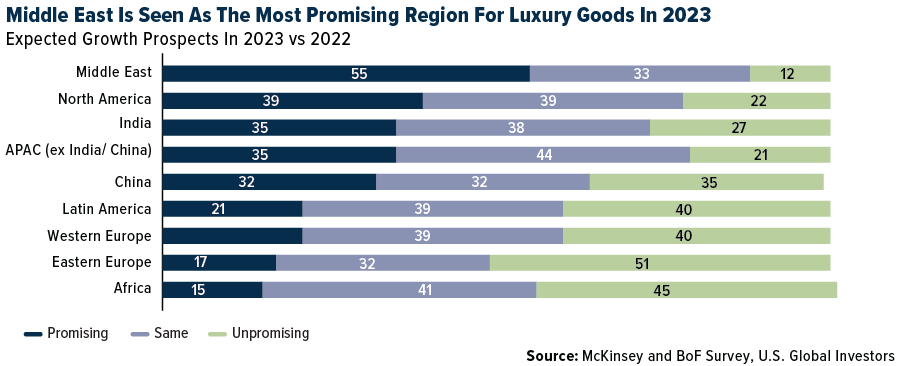

- Barclay’s research team projects that the Middle East luxury goods and services buyer will be key to the luxury sector’s growth in 2023. Luxury sales in the Middle East over the next month should benefit from a return of Chinese tourists and from increased spending over Ramadan, a key gifting period. Tourism has already recovered well since the pandemic in the United Arab Emirates (UAE), and more Chinese tourists are expected after China reopened its economy. China was the fifth largest source market for Dubai in 2019, with the city welcoming 989,00 Chinese tourists that year – vs 177,000 in 2022 (82% below 2019).

- The European Union (EU) will allow sales of new internal combustion engine (ICE) cars on e-fuel beyond 2035. Previously, the EU Parliament voted to ban sales of carbon-emitting vehicles, but in a final decision, cars that run on e-fuel will be permitted. Ferrari and Porsche will benefit from plans to exempt cars that run on e-fuels from the European Union’s planned 2035 phase-out of combustion engine vehicles. Porsche, which is part of the VW Group, has been developing e-fuel in Chile for a couple of years, intending to mix it with regular gasoline.

Threats

- Luxury stocks had a good start this year, recording a gain of more than 17% year-to-date (as measured by the S&P Global Luxury Index). Short-term correction may follow. Investors may become cautious if inflation does not start to ease further, as is expected. Eurozone March preliminary inflation eased this week, but the underlying inflation (core CPI) posted the highest reading on record, suggesting the ECB may still need to hike rates.

- The luxury market may see consolidation in the coming months. According to a Bloomberg survey of 17 M&A desks, fund managers and analysts, the sector appears ripe for a mergers & acquisitions wave. Hugo Boss and Burberry were mentioned as potential takeover candidates in the survey, alongside Italy’s Tod’s SpA. Many stocks doubled in value since the early days of the pandemic and bidders will likely have to offer top prices.

- The Chinese state oil and gas company, CNOOC, and French TotalEnergies traded 65,000 tons of liquefied natural gas (LNG) this week, settling the transaction in yuan, the Shanghai Petroleum and Natural Gas Exchange said on Tuesday. France is one of the world’s top LNG trades and it was the first transaction that was completed in Chinese currency, challenging the United States dollar.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was West Texas Intermediate (WTI) crude oil, rising 9.02%, largely on disruptions to Iraqi exports of 400,000 barrel a day over a conflict with the Kurdistan region. At prices near the current strip ($70 WTI), free cash flow (FCF) yields average nearly 10% in 2023 for many oil producers. While this is lower than last year, it is still two times the S&P 500. At $80 per barrel WTI, yields would average 12%, while at $90 per barrel they would grow to 16%. Strong balance sheets and low break-evens also bolster the sector’s resilience at lower prices, especially relative to prior cycles. At $60, FCF yields would fall to 6%, while at $50 they would be 4%.

- Air Products announced $130 million in hydrogen contract sales to NASA covering multiple facilities. Some contracts/sales appear already in place, but are still an incremental positive. Assuming a 30% incremental margin, sales could add $0.15 to earnings per share (EPS), or 1% to FY23. The press release indicates a target to invest at least $15 billion in clean energy mega-projects globally.

- Despite the receding lithium carbonate prices in China, lithium Giant Albemarle made a $3.7 billion cash offer for Liontown Resources, which was immediately rejected by the Australian developer, sending shares in the target up almost 70% and fueling expectations of wider consolidation. U.S.-based Albemarle is seeking growth to meet future demand, as reported by Bloomberg. Liontown owns one of the most promising early-stage lithium projects in Australia, the world’s top exporter of the battery metal, and has supply agreements with major automakers including Tesla and Ford Motor.

Weaknesses

- The worst performing commodity for the week was molybdenum, dropping 18.50%, continuing its pullback that started in the first week of March with a 20% decline from prices that had risen to a 17-year high. Natural gas prices remain subdued near-term, but forward pricing remains constructive at $3 per million cubic feet (Mcf) and $4 per Mcf for the 12-month period. The National oceanic and Atmospheric Administration (NOAA) recently released its spring weather outlook that includes above average temperatures in the Southern and Eastern U.S. and below average temperatures in the northern Midwest.

- Pulp shipments were down 3.6% year-over-year (hardwood -4.3%; softwood -2.7%) in February. Shipments were also down 0.2% month-over-month (but were up 0.3% after adjusting for seasonality), with lower softwood shipments (-3.1%) partially offset by increased hardwood shipments (+1.3%).

- Spot lithium prices in China have been breaking down for the better part of five months. Carbonate prices have outpaced hydroxide to the downside, though both are under pressure. There has not been weakness extend outside of China, though given cross border purchases, global markets will soon be under pressure as well.

Opportunities

- Bloomberg reports that giant wind turbines are poised to get even bigger, according to Ming Yang Smart Energy Group, a manufacturer that already offers equipment fitted with vast 140-meter-long blades. Deploying larger equipment can reduce the number of turbines needed at each wind farm site, lowering project costs. Giant-sized products are also seen as likely to be in increased demand as the world builds more and more offshore project, and for use in massive clean-energy hubs like those planned by President Xi Jinping for China’s vast interior.

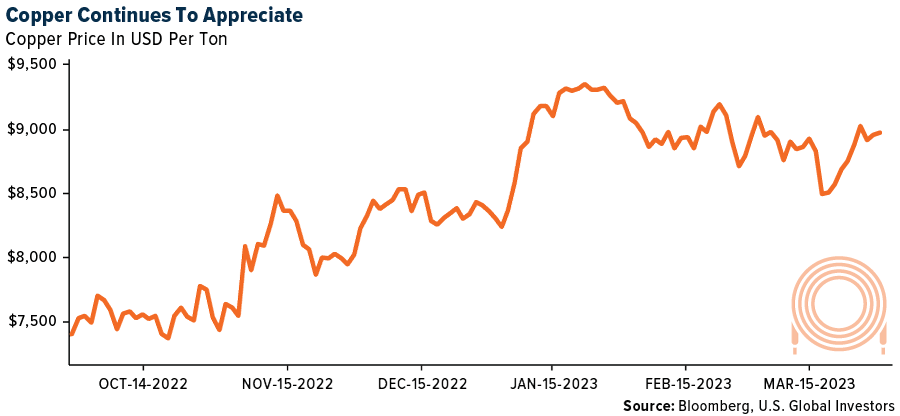

- This week, the Financial Times highlighted Trafigura’s bullish view on copper. They see copper prices surging to a record high this year as a rebound in Chinese demand risks depleting already low stockpiles, the world’s largest private metals trader has forecast. Global inventories of the metal used in everything from power cables and electric cars to buildings have dropped rapidly in recent weeks to their lowest seasonal level since 2008, leaving little buffer if demand in China continues to pace ahead. The benchmark three-month copper contract is trading at $9,000 a ton, having gained 30% since falling sharply in the three months after Russia’s invasion of Ukraine when investors fretted that soaring energy prices would dent metals demand.

- The Department of Energy (DOE) projects green hydrogen production in the U.S. will increase to 10 million metric tons per year by 2030, 20 million metric tons per year by 2040 and 50 million metric tons per year by 2050. The World Bank believes hydrogen is a key part of a carbon-free world solution and will account for 12-22% of final energy demand in 2050. Not to be left behind, Bloomberg reports China’s capacity to manufacture electrolyzers – the equipment used to make green hydrogen – could grow about 20 times by 2028 as costs of the clean energy source plunge, according to the China International Capital Corporation (CICC). Local electrolyzer demand could be 40 gigawatts by 2028. The zero-emissions fuel, produced by using renewable energy to extract hydrogen from water, is on track to achieve cost parity with other methods fueled by natural gas or coal as soon as the end of this decade, which will drive rapid deployments, CICC analysts wrote in a note.

Threats

- A group of institutional investors who together oversee $11 trillion in assets is placing new limits on fossil-fuel spending it will tolerate as reported by Bloomberg. The Net-Zero Asset Owner Alliance, whose signatories include Allianz SE and the California Public Employees’ Retirement System, is advising members to halt direct funding of any new investments in fields, pipelines or power plants that are fueled by oil or gas, according to a report on Wednesday. They also said oil and gas companies must set science-based targets to include so-called Scope 3 emissions, follow science-based pathways and stop lobbying against action on climate.

- The U.S. is unlikely to start buying crude for the U.S. Special Petroleum Reserve (SPR) this year despite lower prices due to a pending drawdown, Argus Media reported Energy secretary Jennifer Granholm said today. Granholm added that another challenge is that two SPR facilities — the Bayou Choctaw site in Louisiana and Bryan Mound storage site in Texas — are under maintenance. Crude in the SPR currently stands at 371.6 million barrels at four storage sites, the lowest level in 40 years.

- Supply increases from the U.S. shale producers, traditionally the most responsive to changing market conditions, are expected to more than halve from 0.9 million barrels/day this year to 0.4 million barrels/day in 2024 with crude and condensate production increasing only 300 kbd and NGLs contributing only 144 kbd. Current drilling inventory guidance suggests U.S. public shale producers have 8-15+ years of economic drilling remaining at current rates.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was XRP, rising 25.81%.

- Crypto Exchange Kraken signed a multi-year global pact with Formula One team William Racing, marking the trading platform’s first major sponsorship deal even as sports tie-ups with digital asset firms become increasingly unpopular. Kraken’s logo will be placed on the halo and rear wing of William’s car for the rest of the 2023 season, writes Bloomberg.

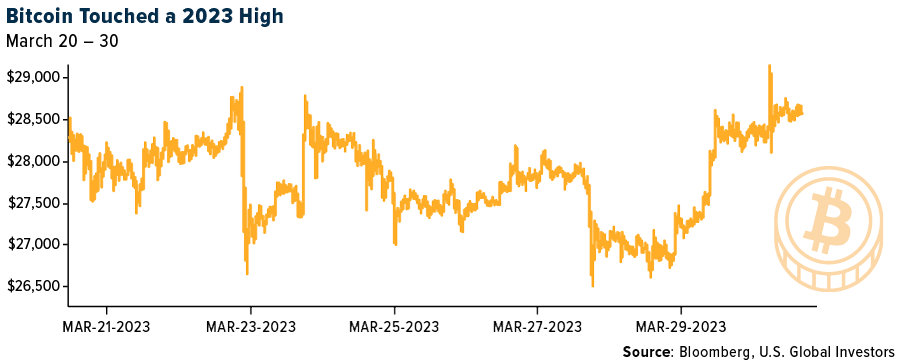

- Bitcoin renewed its climb toward $30,000 with risk appetite rising across global markets and concern about the fallout from Binance’s legal woes waning. Bitcoin rose as much as 4.9% to $28,638 on Wednesday, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Stacks, down 15.48%.

- Galaxy Digital, the company founded by Michael Novogratz, posted a fourth-quarter loss but said that the company’s liquidity position remains intact after the recent turmoil in the banking sector. The net loss was $2.8 billion, compared with net income of $521.3 million in the year-earlier period. The loss was primarily attributed to unrealized losses on investments in its investment portfolio during the slump in token prices, writes Bloomberg.

- Sushi Swap CEO Jared Grey is no longer feeling “inspired” after a wave of regulatory crackdowns on crypto exchanges, including the DEX that he manages, has put immense pressure on the crypto industry.

Opportunities

- Michael Novogratz, the founder of crypto financial services firm Galaxy Digital Holdings, said crypto markets “feel strong” this year, due to sellers’ exhaustion and the easing of restrictions in China, with Hong Kong warming up to the digital-asset sector. Even though trading crypto has been banned in mainland China, the city of Hong Kong last year unveiled a plan to make itself as a center for digital assets and so-called Web3 firms, writes Bloomberg.

- A new Hong Kong-based fund plans to raise $100 million this year to invest in digital asset startups, as the city seeks to become a regional fintech hub. The fund will be led by Ben Ng, a venture partner at the Asian private equity firm SAIF Partners, and longtime tech investor Curt Shi. The two have secured at least $30 million in funding commitments, writes Bloomberg.

- As much as $5 trillion may transition to new forms of money such as central bank digital currencies and stablecoins by 2030, of which roughly half could be linked to blockchain technologies, according to a Citigroup research study.

Threats

- The U.S. took its most forceful move yet on Monday to crack down on crypto exchange Binance Holdings and its CEO, Changpeng Zhao. The CFTC alleged in federal court in Chicago that Binance and its CEO routinely broke American derivatives rules as the firm grew to be the world’s largest trading platform. Binance should have registered with the agency years ago and continues to violate the CFTC’s rules, writes Bloomberg.

- Sam Bankman-Fried was charged with bribing Chinese officials, adding a new dimension to the U.S. government’s case against the FTX co-founder. The new charge was unsealed Tuesday in a revised indictment by federal prosecutors in Manhattan. Bankman-Fried is accused of authorizing the payment of $40 million to one or more Chinese government officials in order to get them to unfreeze accounts at Alameda Research, writes Bloomberg.

- U.S. banks already hesitant to work with crypto customers are now even warier of providing services to the industry after a string of regional-lender collapses. The closure of crypto friendly Silvergate and seizure of Signature Bank has left crypto firms struggling to find new banks for depository and payment services, Bloomberg says.

Gold Market

This week gold futures closed the week at $1,987.70, down $14.00 per ounce, or 0.70%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.66%. The S&P/TSX Venture Index came in up 3.68%. The U.S. Trade-Weighted Dollar fell 0.54%.

Strengths

- Everything is playing in gold’s favor: A banking crisis, falling rates, high inflation, pressure on the dollar, hot Asian demand and technical momentum as it flirts with breaching the $2,000 an ounce level for the first time in over a year.

Weaknesses

- The worst performing precious metal for the week was gold, down 0.70%. Gold prices in India, the second largest consumer, are up 15% from the prior year and that has led to a pullback in demand going into next month which is a key demand period. The cash market for gold is currently trading at a discount.

- Galiano Gold reported Q4/22 financial results with adjusted earnings per share (EPS) of -$0.03 (versus the consensus estimate of $0.01) on a lower realized gold price and higher finance costs from production of 34,100 ounces gold with an all-in sustaining cost (AISC) of $1,191 an ounce.

- Overall, inflation pressures were significantly underestimated in 2022 with only 30% of producers achieving original guidance and average AISC coming in +$100 an ounce higher than expectations. For 2023, companies have rebased costs higher, outlining an additional +3% increase in guided costs versus 2022.

Opportunities

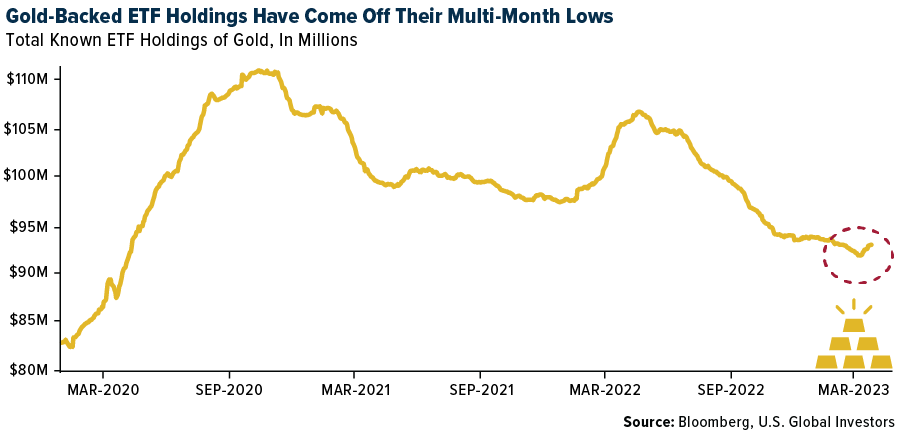

- With investors shifting to accumulate gold over the past two weeks as evidenced by net inflows into physical gold ETFs, the chief economist and global strategist at Euro Pacific Capital believes investors may be running out of time to purchase gold below $2,000 per ounce. Banking stress, a weaker dollar, and falling bond yields are driving investors to follow the lead of many central banks around the world that bought record amounts of gold.

- Gold is near its highest price in nearly a year, with the copper/gold ratio declining by 4% year-to-date. Historically, this ratio has exhibited a close correlation with the cyclical/defensive ratio; however, the latter is +12% YTD. Gold equities should continue to benefit at this point in the cycle.

- Barrick Gold and the Papua New Guinea government and partners have agreed to resume operations at the Porgera gold mine at the earliest opportunity according to Bloomberg. Upon operational restart, the plant and operations have been on care and maintenance since 2020, the mine is expected to ramp up to around 700,000 ounces per year. This should be a positive as it brings a second operating gold mine to the Papua New Guinea outside of the presently established operations of K92 Mining. Barrick has the confidence to return to this jurisdiction.

Threats

- Analysts are taking down their platinum group metals (PGM) basket price forecasts by 20% on average between 2023-2030 to reflect a faster-than-expected decline in ICE vehicle sales through 2030 and a growing perpetual palladium/rhodium surplus that emerges by 2025. Recalling ICE vehicles are one of the primary demand drivers for platinum/palladium/rhodium (given use in ICE vehicle catalytic converters), and growing penetration of EV’s poses a strong demand-side threat to PGMs.

- Only 33% of operations were able to execute on mine site cost guidance in 2022 with average miss of $50 per ounce gold. Company-wide, producers saw average AISC of +$100/oz above original guidance, with only 30% of producers able to achieve guidance, representing a record low versus the prior five-year average of 75%.

- CoinDesk data shows that the top cryptocurrency by market value rose almost 72% to $28,500 this year, its best quarterly gain in two years. The cryptocurrency’s market value is $542 billion after the rally. After falling 76% since November 2021, some experts predicted Bitcoin could fall to $12,000 this quarter three months ago. The rebound has put Bitcoin ahead of Ether, the second-largest cryptocurrency by market value, which is on track for a 50% quarterly gain. Gold has uneventfully only gained 8% this year, reflecting it hasn’t seen a major jump in price due to current stress, but people are noticing.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/30/22):

Tesla Inc.

Bayerische Motoren Werke AG

Mercedes-Benz Group Inc.

Ferrari NV

Volkswagen AG

Hugo Boss AG

Burberry Group PLC

Northern Star Resources Ltd.

Barrick Gold Corp.

K92 Mining Inc.

Hawaiian Holdings Inc.

Ryanair Holdings PLC

AP Moller-Maersk A/S

American Airlines Group Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Standard and Poor’s 500 Apparel & Accessories Index is capitalization-weighted index.

The Consumer Confidence Index reports how consumers feel about the current situation of the economy and about where they feel it is headed. Conducted by the Conference Board, the survey consists of five questions about the present situation and three questions about their expectations for the economy in the future.

GfK’s Consumer Confidence Index (carried out on behalf of the European Commission) measures a range of consumer attitudes, including forward expectations of the general economic situation and households’ financial positions, and views on making major household purchases.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All