Central Banks Are Buying Gold At A Record Pace So Far In 2023

Membership required

Membership is now required to use this feature. To learn more:

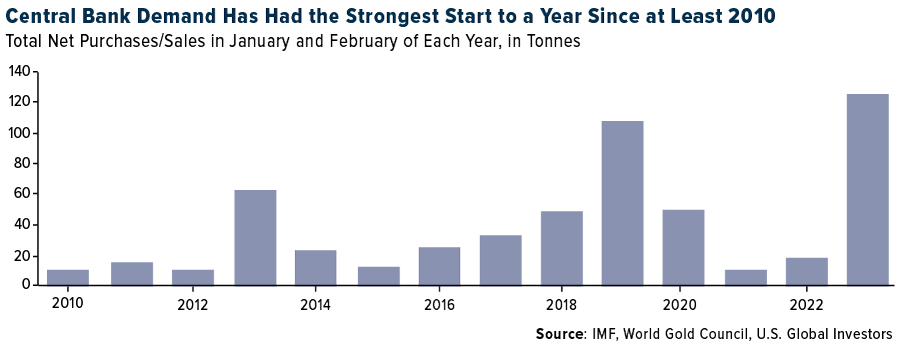

View Membership BenefitsCentral banks accumulated gold at the fastest pace on record in the first two months of 2023, according to a report by the World Gold Council’s (WGC) Krishan Gopaul. In January and February, central banks collectively bought a net 125 tonnes of the metal, the highest amount for the year-to-date period since banks became net buyers in 2010.

The countries reporting the largest purchases in the first two months were Singapore (51.4 tonnes), Turkey (45.5 tonnes), China (39.8 tonnes), Russia (31.1 tonnes) and India (2.8 tonnes). The Central Bank of Russia published an update on its gold reserves for the first time in about a year, so the 31.1 tonnes were likely accumulated over the course of several months instead of in January and February.

Meanwhile, very few countries’ central banks shrank their gold reserves. Net sellers were Kazakhstan, Uzbekistan, Croatia and the United Arab Emirates (UAE), though year-to-date purchases far outweighed sales.

BRICS Countries Will Continue To Be Huge Buyers

If you look back at the list of net buyers, you’ll notice that three are members of the BRICS countries (Brazil, Russia, India, China and South Africa). I point this out because, as I’ve been sharing with you for a couple of weeks now, we may be seeing the emergence of a multipolar world, with a U.S.-centric world on one side and a China-centric world on the other. For the first time ever, BRICS countries’ share of the global economy has surpassed that of the G7 nations (Canada, France, Germany, Italy, Japan, the U.K. and U.S.), on a purchasing parity basis.

Gold plays an important role in this multi-polarization. The BRICS need the precious metal to support their currencies and shift away from the U.S. dollar, which has served as the global foreign reserve currency for about a century. More and more global trade is now being conducted in the Chinese yuan, and there are reports that the BRICS—which could eventually include other important emerging economies such as Saudi Arabia, Iran and more—are developing their own medium for payments.

If this is indeed the case, the implication is clear to me that investors should be increasing their exposure to gold and gold miners. Gold is a finite resource. It’s expensive and time-consuming to produce more of it. At the same time, BRICS countries will continue to be net buyers as they seek to diversify away from the dollar.

Net Inflows Into Gold-Backed ETFs Turn Positive

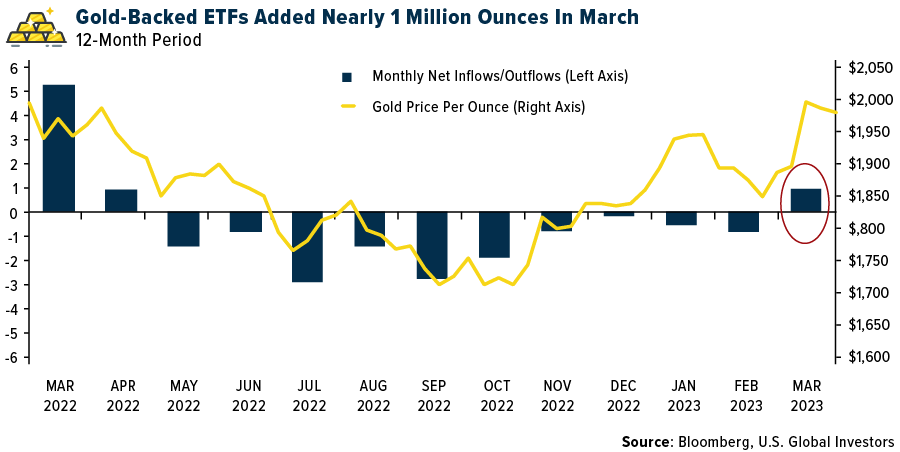

Net inflows into gold-backed ETFs turned positive in March after 10 straight months of outflows as the metal’s price flirts with a new record high. Investors added nearly 1 million ounces to all known physical gold ETFs in March, the highest monthly increase since March 2022, when investors added 1.4 million ounces. As of March 31, total gold holdings stood at 93.2 million ounces, according to Bloomberg.

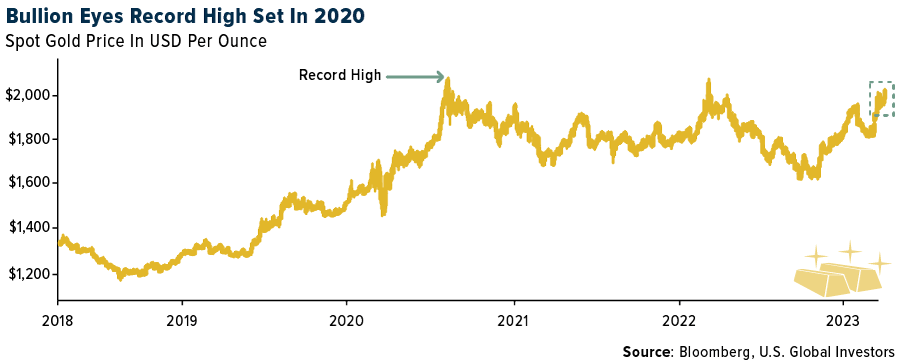

In light of weak economic news, ongoing inflation, rising rates, a shaky banking sector and geopolitical tension, gold is catching a strong bid as it seeks to make a new all-time high. On Thursday, the metal touched $2,032 an ounce, just $43 off its record high, set in August 2020.

Weak Manufacturing Data Points To Potential Trouble Ahead. Do You Have Your 10%?

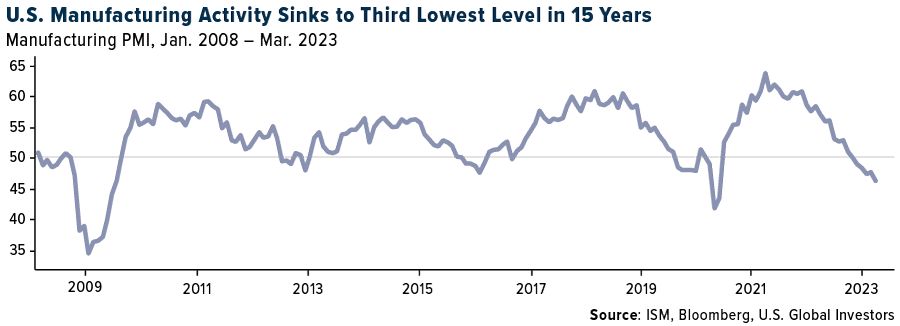

I believe accumulating gold and gold stocks is prudent and wise at this time, especially as recession signals are starting to flash. U.S. manufacturing activity contracted at a faster rate for the fourth straight month, with ISM’s Manufacturing PMI sinking to 46.3 in March. That’s the third-lowest reading in 15 years, following the financial crisis and pandemic lockdowns. What’s more, every category—from new orders to production to inventories—was in contraction mode.

The Federal Reserve’s actions to slow economic growth appear to be having the desired effect. We may be looking at the end of the most aggressive rate hike cycle in two generations, and this carries risks that investors should be aware of.

Over the past 70 years, a Fed pause was followed by an economic recession 75% of the time, with an average lag of six months, according to CLSA’s Alexander Redman and Della Chen. The two analysts believe the Fed has just one more hike to go before it pauses and begins to reverse course. The cycle should be complete by July, Redman and Chen estimate.

If their estimates are correct, we may be looking at a recession late in the fourth quarter.

The time to buy equities, they say, is when the Manufacturing PMI bottoms after the start of the recession. Doing so resulted in positive 12-month returns seven out of eight times, for an average return of 26%.

Timing these things is always tricky, and we’re talking about events that could be months in the future. If a recession is in the cards, it may make sense to ride it out with the help of gold. As always, I recommend a 10% weighting, with 5% in physical gold and the other 5% in high-quality gold mining stocks, mutual funds and ETFs.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.91%. The S&P 500 Stock Index rose 1.30%, while the Nasdaq Composite climbed 0.62%. The Russell 2000 small capitalization index lost 0.83% this week.

- The Hang Seng Composite gained 0.01% this week; while Taiwan was down 0.24% and the KOSPI rose 0.25%.

- The 10-year Treasury bond yield fell 24 basis points to 3.304%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Turkish Air, up 7.3%. The International Air Transport Association (IATA) reported February passenger traffic levels. Total domestic travel in February was up 25.2% year-over-year while international travel was up 89.7% year-over-year. As with the January results, China continued to have a substantial impact on global RPK growth as restrictions were lifted in the country. Relative to pre-pandemic levels, total domestic travel is at 97.2% while international travel is at 77.5%.

- According to ISI, first quarter energy shipping is usually one of the strongest periods of a year, owing to northern hemisphere winter demand and inefficiencies of operating in inclement weather. However, the magnitude at which first quarter rates have exceeded long-term averages confirms an incredibly tight supply/demand balance at present, whether it is winter or not. 2023 may well prove to be the best year for tanker rates since the turn of the millennium.

- For airlines, global capacity was back to 92% last week. Capacity in domestic markets was 6% above 2019 last week with international markets back to 85%. Notable in the data was: 1) Asia ex China domestic has recovered completely and 2) Middle East international is approaching full recovery with capacity now only 3% below 2019. Among other regions, Europe intra-region was down only 5% with international down 9%. North America domestic was up 2%, with international down 11%.

Weaknesses

- The worst performing airline stock for the week was Azul, down 10.3%. Pratt & Whitney engine problems have resulted in criticism and lawsuits due to aircraft being grounded. The issue at hand relates to the availability of functional engines and their corresponding parts. This has been a persistent challenge for the PW1000G series, which powers the Airbus A220, A320neo, and Embraer E2 aircraft families.

- The only risks to the strong tanker market backdrop and positive supply/demand outlook through at least 2024 would be a surge in capacity/ordering, a peaceful resolution to the war in Ukraine, a full-blown global recession, or an OPEC cut. The removal of nearly 1.0 million barrels per day of long-haul crude flows will undoubtedly hit VLCC demand and industry ton-miles.

- In March, airline stocks declined 8.9% and underperformed the S&P 500 by 12.4%. The softness comes after a strong start to the year for the group, and year-to-date, airline stocks have gained 6.5% compared to the S&P 500’s 7.0% move higher. The stock moves in March were driven primarily by multiple compression given the macro concerns and slowdown in bookings data while 2023 EBITDAR estimates were largely unchanged during the month.

Opportunities

- Chinese international traffic is at 20% of normal in the first half of 2023 and could be 50% of normal in the second half. International was only 15% of pre-Covid levels in the first quarter, but the Chinese airlines are aiming to ramp up to 35-40% of normal by summer 2023 and 50-70% of normal by the end of 2023 (with supply constrained by traffic rights, visa/passport delays, and global issues).

- Based on current delivery schedules and retirement expectations across DHL, FedEx and UPS, the integrators’ dedicated freight net capacity could increase by 0.7% in fiscal year 2023, 3.4% in fiscal year 2024 and 1.7% in 2025. Demand for Express would likely grow at a trend of 3-5% per annum over the cycle. A significant proportion of the aggregate active fleet by tonnage is 30 years old.

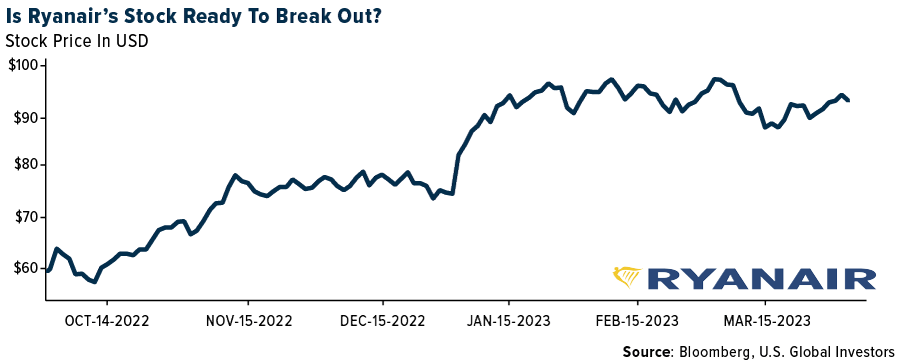

- Ryanair announced that it has responded to the U.K. government’s 50% APD cut for domestic travel from April 2023 with the opening of nine new domestic routes. However, this 50% reduction ignores international connectivity which is fundamental for the growth of the U.K.’s economy and tourism. Ryanair calls again on the U.K. government to fully abolish APD for all travel immediately, which would not only promote tourism, but also support job growth, and much needed connectivity to the U.K.

Threats

- Should the Department of Justice (DOJ) rule in favor of the JetBlue-Spirit merger, the Department of Transportation (DOT) could accept the decision, or it could attempt to block the merger under unfair and deceptive trade practices. While a DOT move could be challenged, it would further lengthen the process, potentially delaying funding.

- According to Goldman, as the demand-driven first phase of the current freight downcycle is drawing to a close in the first quarter of 2023, the bank sees capacity growth in Air & Sea accelerating from the second quarter through the first half of 2024, likely constraining pricing power across sub-sectors. At current spot freight rate levels, Goldman believes current 2024 consensus estimates remain generally too high across the space.

- Hawaiian Air and Alaska Air are exposed to longer-duration investments and higher-risk assets including equity exposure and collateralized loan obligations. Of Alaska’s total cash and short-term investments, 31% mature within a year compared to the 95% industry average. Further, the company is a bit more invested in corporate bonds and asset-backed securities than other airlines. Hawaiian has just 24% if its cash and short-term investments in securities that mature within a year while 50% are in investments such as CLO’s, equities, and other investments.

Luxury Goods And International Markets

Strengths

- According to a Vogue Business article, L’Oréal signed an agreement this week to purchase Aesop, one of the most popular cosmetic and hand soap brands in Australia, which reported $537 million in sales in 2022. The acquisition is worth $2.5 billion dollars. L’Oréal’s managing director, Nicolas Hieronimus, said, the company wants to support and accelerate its potential growth, especially in China. Aesop was owned by Natura (a Brazilian company); Puig and LVMH were potential buyers, too.

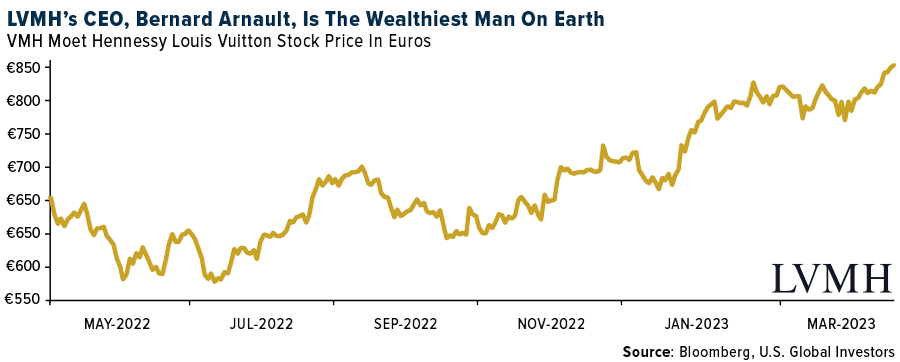

- According to the Bloomberg Billionaires Index, Bernard Arnault, the CEO of luxury conglomerate LVMH, is the wealthiest man on earth. His fortune is now worth over $200 billion for the first time, making him one of three people ever to reach that level of personal wealth after Elon Musk and Jeff Bezos, (but he is the first to do so outside of the U.S.). His fortune increased on Tuesday by $2.4 billion to $201.1 billion. According to Bloomberg, the company’s stock price is now at a record. LVMH reported record sales for 2022 of €79.2 billion. LVMH companies, Dior and Tiffany products, are seeing robust demand, Bloomberg explains.

- Lukfook Holdings, a high-end jewelry retailer in Hong Kong, was the best performing S&P Global Luxury stock for the week, gaining 8.4%. Lukfook Jewelry has once again been honored with the “Outstanding Jewelry Retail Service Award” in the “01 Gold Medal Awards”, in recognition of its outstanding achievements in promoting Hong Kong’s goodwill and corporate image and being a role model for the industry.

Weaknesses

- According to Reuters, McDonald’s, one of the leading fast-food chains in the U.S. and worldwide, announced this week the temporary closure of its corporate offices in the U.S. to prepare for the announcement of a massive layoff as part of its restructuring strategy. The company is following the trend seen in the tech sector, as witnessed with Amazon, Google, Meta, and Disney. This comes as a worrisome sign, suggesting the U.S. economy could be entering a new phase, where companies must make hard decisions such as layoffs.

- According to Bloomberg Economic releases, the Caixin China Manufacturing PMI for March was reported at 50 versus a previous month reading of 51.6. The Global U.S. Manufacturing PMI for March was reported at 49.2 versus last month’s 49.3. The United States and China are the leading luxury goods markets worldwide, and a slowdown in their economies could impact the luxury industry significantly.

- Faraday Future Intelligence was the worst performing S&P Global Luxury stock for the week, losing 19.5%. Shares of the electric car maker declined on Monday after first-quarter deliveries from several electric car makers disappointed. Faraday recorded its deepest decline this week, losing 15% of its value in a single trading day on Monday.

Opportunities

- Through its official LinkedIn profile, Prada announced the opening of the Prada Caffè at Harrods, the iconic shopping center in London, England. Prada aims to offer its clients a different experience with the brand, beyond fashion. The coffee shop is all Prada-distinctive, and customers will be immersed in the brand’s decor, atmosphere, and of course, menu. This is one way luxury brands are looking for new ways to reach clients and create awareness in the marketplace.

- The service sector in Europe is stronger in Europe than in the United States, according to the Service PMI reading. According to Bloomberg, the Global Eurozone Service PMI was reported at 55.0, while the S&P Global U.S. Service PMI was released at 52.6 in March. Both PMIs fell slightly, but Europe so far is recording stronger activity.

- According to an official announcement by Ralph Lauren, the company announced it has opened a new luxury concept store in Miami, in the well-known Design District, offering an experience of luxury, fashion, art, and culture. Additionally, this is the first Ralph Lauren store that accepts cryptocurrency as a payment method, thanks to the collaboration with the digital community Poolsuite. The brand wants to expand its presence in Miami by creating engaging experiences, including the use of Web 3.

Threats

- This week, Finland became the 31st member of NATO. Becoming part of this treaty means that an attack on one of its members means an attack on all of its members. Finland’s addition expands NATO’s border with Russia, considering that the country has the longest border with Russia. Sweden could follow in Finland’s footsteps and become the next NATO member, (most likely aggravating the President of Russia, Vladimir Putin).

- The International Monetary Fund (IMF) warned that its outlook for global economic growth over the next five years is the weakest it has been in more than three decades, caused by geopolitical tensions and a decline in productivity. Managing Director of the IMF, Kristalina Georgieva, expects the global economy to expand by about 3% in the next five years. This is the lowest medium-term growth forecast since 1990 and less than the five-year average of 3.8% from the past two decades. This year, the world economy will most likely expand by less than 3%.

- Luxury companies have had a great start to the year so far. Year-to-date, shares of Hermes are up 35%, Louis Vuitton has gained 27%, and CFR Financière Richemont is up 21%. The largest luxury company within the S&P Global Luxury group is Tesla, with a market capitalization of $587 billion, followed by Louis Vuitton with a market cap of $462 billion, while Hermes is valued at $219 billion. Quick periods of outperformance may create a buying opportunity after short-term price corrections.

Energy And Natural Resources

Strengths

- The best performing commodity for the holiday-shortened week was coffee, rising 7.68% with traders citing falling global exports, which could mean tighter supplies, reported Bloomberg. For gasoline demand, this is the highest seasonal level in three years. In fact, implied demand some eight weeks ahead of the “official” start of the driving season, is higher than most of the summer of 2022. This is worth watching because 2022 had >$5 average retail gasoline versus $3.49 currently. A large part of the delta is a $32 lower oil price, and it is that combination that allows higher gasoline cracks to co-exist with relatively low gasoline prices (potentially supporting one of the strongest driving seasons since Covid).

- JPMorgan remains constructive on European energy at this complex macro juncture for three reasons: 1) resilient balance sheets: the group expects European Union (EU) Big Oils to continue deleveraging with debt/equity at 9% by the end of 2023, compared to a long-term range of 15-30%; 2) resilient free cash flow (FCF) and ongoing capital discipline, with the sector still generating a 12% FCF yield in 2023E, at the current forward curve; and 3) underinvestment and supply tightness, suggesting a structural production decline in most non-OPEC and several OPEC countries.

- Following a prolonged surplus phase, beginning with Europe’s destocking from early third quarter last year and ending with China’s Lunar New Year (LNY) slowdown into late February, the aluminum market has now shifted into a deficit state. This tightening shift has primarily reflected trends in China’s domestic market where inventory draws have gathered velocity through March on positive demand momentum and policy-induced supply constraints.

Weaknesses

- The worst performing commodity for the holiday-shortened week was natural gas, dropping 8.75% on expectations of milder weather for mid-April and returning post-maintenance production coming back online. Despite a colder-than-average March, New York Mercantile Exchange (NYMEX) gas prices have sold off since the start of the month, with the April contract expiring at $1.99. The decline reflects an accumulating storage surplus, driven primarily by very warm weather in January and February but also by high production supporting below-average storage draws.

- U.S. steel demand declined 15% year-over-year in the fourth quarter and a further 11% decline year-over-year into January 2023. From here, the UBS Steel Demand Projector (~80% historically accurate, developed by UBS Empirical Scientific Approaches) signals continuously negative year-over-year demand through early second quarter.

- Chinese lithium prices continued their descent this week with carbonate/hydroxide prices down 15.8% as destocking efforts continue. Meanwhile, spodumene prices continue to hang in relatively well (down just 5% this week), so conversion margins have slipped further into negative territory causing various production cuts.

Opportunities

- Glencore started the week with a bid for Teck Resources that sent the share price up nearly 20% by the end of the day. The $23 billion proposal was rapidly rejected immediately. Analyst Danni Hewson of AJ Bell noted that Teck’s board wasn’t contemplating a sale of the business, yet there is a price for everything. It all boils down to how much Glencore is prepared to pay.

- Several members of the OPEC+ group announced a surprise output cut that could potentially reduce global supply by more than 1 million barrels per day. The voluntary cut is led by Saudi Arabia and importantly includes Iraq and the United Arba Emirates (UAE), the only other countries with spare production capacity. This has come as a surprise to the market, especially given the recent reduction in speculative net long positions and should be supportive for crude oil prices.

- NGEx Minerals reported the discovery of a significant new zone of high-grade copper, gold and silver mineralization at their 100%-owned Potro Cliffs project located in the mining friendly San Juan Province, Argentina. A drill hole intersected multiple zones of stacked massive- to semi-massive sulfide veins and breccias. One highlighted intercept included 60 meters at 7.52% copper equivalent grade (CuEq) starting at 212 meters down the hole. This is the first drill program conducted by NGEx, and the results are interpreted to be the first intercepts into the edges of a major new copper-gold system.

Threats

- In the last few years, refiners have traded a lot more closely with broader energy than they did in the past. While all energy names tend to trade up on the OPEC cut news, refiners could be the laggards. Only 18% of total imported crude was coming from OPEC+ countries. In the last year, Canada and Mexico have actually accounted for 75% of total imported crude.

- Morgan Stanley previously expected this oil deficit to be created by a fundamental tightening of the market, but now they look to be the outcome of OPEC cuts, which is less bullish. Still, Brent spreads are light relative to inventories, and are likely to tighten as inventory builds turn to draws. That still supports some upside in flat price as the year unfolds, up to $90 per barrel for Brent.

- According to UBS, iron ore prices remain elevated at >120 per ton, with robust demand so far offsetting strong supply growth. UBS sees downside risk to spot iron ore prices with the market to move into a growing surplus medium-term; the group expects this to push prices back to the cost curve as seen in 2014-2018.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Solar, rising 56.33%.

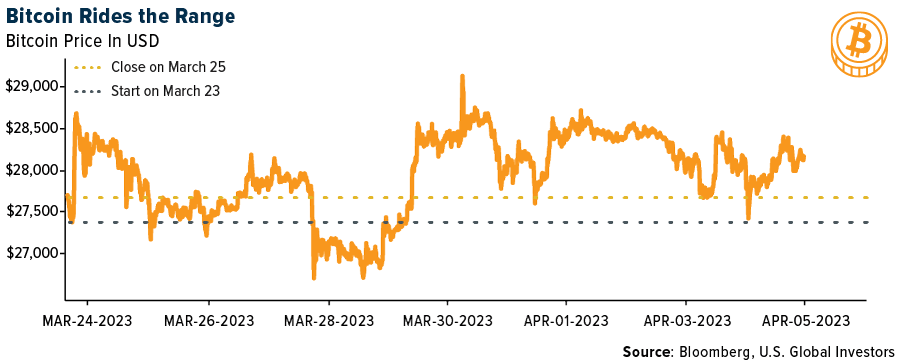

- Bitcoin trended toward the high end of its recent range of around $28,000 this week, while Dogecoin continued to benefit from Elon Musk’s flirtation with the meme token. Bitcoin rose by as much as 3.1% on Tuesday, its first session higher in three, writes Bloomberg.

- MicroStrategy bought 1,045 Bitcoin for $29.3 million between March 24 and April 4, reports Bloomberg. As of April 4, the company held roughly 140,000 Bitcoins in total.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Mask Network, down 12.54%.

- Paxful, an Africa-focused Bitcoin trading platform, is suspending its operations, the company’s co-founder, Ray Youssef said in statement, citing key staff departures and growing regulatory challenges, writes Bloomberg.

- Cryptocurrency exchange BAM Trading Services, and its identity-verification vendor Jumio Corp, must face a proposed class action, reports Bloomberg. The lawsuit alleges the exchange collected account holders’ facial geometry in violation of the Illinois Biometric Information Privacy Act.

Opportunities

- OpenSea has launched a new platform catering to the needs of advanced collectors as it seeks to stay competitive amid new market entrants. One of the key features of the new platform is the live cross-marketplace data function that allows collectors to track user and collection activity across various NFT trading venues, writes Bloomberg.

- On-chain analysis indicates that Mechanism Capital’s Andrew Kang purchased an additional 1.51 million Arbitrum tokens at $1.23 with approximately 1.85 million USDC. Another Arbitrum whale withdrew 5.85 million tokens from the exchange, worth approximately $21.5 million at current prices.

- Singapore banks are working with the city-state’s authorities to set uniform standards on screening potential customers from the crypto and digital assets sectors, writes Bloomberg.

Threats

- Tether Holdings doesn’t have direct access to the U.S. banking system, explains Bloomberg, but for a while it found at least one pathway through Signature Bank. Tether instructed crypto clients to pay for its stablecoins by sending dollars to its Bahamas-based banking partner Capital Union Bank via Signature’s Signet payments platform.

- The overwhelming majority of cryptocurrency owners aren’t paying taxes on their holdings, according to a study by a Swedish tech company. Globally, just 0.53% of cryptocurrency investors declared their cryptocurrency activity to their local tax authorities in 2022, writes Bloomberg.

- Jane Street Group, Tower Research Capital, and Radix Trading are the three unidentified trading firms cited as VIP clients of Binance Holdings in a top U.S. regulators lawsuit against the cryptocurrency exchange. The CFTC last week accused Binance of “sham” compliance with U.S. derivatives regulations including to keep Americans of the exchange as promised, writes Bloomberg.

Gold Market

This week gold futures closed at $2,021.70, up $35.50 per ounce, or 1.79%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.18%. The S&P/TSX Venture Index came in off 1.31%. The U.S. Trade-Weighted Dollar fell 0.58%.

Strengths

- The best performing precious metal for the holiday-shortened week was silver, up 3.64% and marking four consecutive weekly gains. Gold surged to the highest since March 2022 after weaker job opening data fueled expectations that the Federal Reserve may be nearing the end of its monetary tightening. Vacancies at U.S. employers dropped in February to the lowest since May 2021, suggesting a cooling in labor demand, but still indicative of a job market that’s too tight for the Fed.

- Canaccord expects inflation to be less of a headwind for producers in 2023, with expectations for mining all-in sustaining costs (AISC) to be relatively flat in 2023. Year-to-date, the royalties are up 11% as a group, ahead of the senior gold producers and gold bullion, but trailing the intermediate producers and junior producers. Royalty performance has been led by Osisko and Wheaton Precious Metals.

- Calibre Mining reported first-quarter gold production of 65,750 ounces (5% above consensus), comprising Nicaragua gold production of 54,997 ounces and Nevada gold production of 10,753 ounces. The first quarter includes the first ore production from the Pavon Central open pit as well, which the company began mining in January 2023.

Weaknesses

- The worst performing precious metal for the holiday-shortened week was palladium, down just 0.82%. Gold Fields corporate reserves largely reflect depletion and no meaningful additions, while resources declined more meaningfully. Overall, these changes have a limited impact to valuation, but reinforce long-term risks of depletion. Reserves as of year-end 2022, total 46.1 million ounces, a decrease of 2.3 million ounces year-over-year.

- Metalla Streaming reported a headline earnings per share (EPS) loss of $0.11 that included $2.0 million in impairment charges on the Joaquin and COSE royalties. Additionally, during the fourth quarter of 2022, the company determined depletion had not been appropriate at its Silverback investment and recorded a catch-up charge. This was well below consensus for a loss of $0.01.

- According to Bank of America, the commodities team is bullish gold, calling it to $2,200 per ounce by the fourth quarter of 2023. However, the gold price has reached substantial technical resistance ($2,000 – $2,078 as key resistance), and the bank sees potential seasonal weakness before the second half of the year.

Opportunities

- Bloomberg reports that Newcrest Mining and partner Harmony Gold have signed a Framework Memorandum of Understanding with Papua New Guinea (PNG) for the Wafi-Golpu project. This is a significant step forward in the process to ultimately the signing of a Mining Development Contract for Wafi-Golpu. Just at the end of March, Barrick Gold and its partners agreed to resume operations at the Porgera gold mine. K92 Mining has been operating in PNG for the past seven years and has enjoyed good relations with the government, and evidently the government desires to have the gold miners return to their mineral-rich country.

- The World Gold Council (WGC) reiterated its view that central banks will continue to build their official gold holdings. This is based on the WGC’s survey of central banks, but also the view that emerging and developing country central banks are inclined to purchase gold because of the metal’s appeal versus other asset classes – low or negative yielding sovereign debt, rising sanctions risks and a threat of currency wars. Gold is an important reserve asset that isn’t exposed to downside from geopolitical risks, cannot be de-based and lacks default risk.

- According to Scotia, in 2023, companies reported guidance for production 2% higher than 2022 production, with cost guidance 2-6% higher than 2022 reported figures. Although costs are expected to remain high, producers are seeing some easing of inflation (particularly fuel prices). Scotia believes the higher gold price environment, coupled with some relief in cost pressures, will lead to margin improvement.

Threats

- According to Canaccord, until Gatos is able to refile its backed financials and hold its annual shareholder meeting, it may be in violation of the extension granted by the TSX. Notably, the TSX has appeared to be more lenient than the NYSE throughout this process and has often followed the lead of the U.S. regulators. Therefore, Canaccord expects that it is possible the TSX will extend its March 31, 2023, deadline to align with the NYSE before halting the stock or commencing de-listing proceedings.

- While the proposed reform addresses some important points currently missing in Mexico’s mining law (e.g. the need of a social impact study and the approval of a mine restoration and mine closure plan), there are still two key concerns: 1) a considerably lower concession period (15 years vs. 50 years today), which may drastically change the economic viability in a capital intensive industry, and 2) lack of clarity on how the new rules proposed in the bill may be implemented, effectively reducing legal certainty for miners. Without new investments, mining activities could be negatively impacted in the long term. Silvercrest, Orla Mining, First Majestic and Torex Gold Resources have large Mexico exposure, and they will likely look to other countries to grow their operations in other countries.

- According to Bank of America, Kinross Gold has appreciated 23% year-to-date on the gold price rally, outperforming the S&P/TSX Gold Index by 16% and has reached the bank’s price objective. The group also thinks first quarter 2023 results could be operationally weak owing to the tie-in at Tasiast (a key mine) and sharply higher cost at the U.S. mines.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/23):

Osisko Gold Royalties

Wheaton Precious Metals

Gold Fields

Karora Resources

Kinross Gold

Airbus SE

FedEx Corp

Ryanair Holdings PLC

JetBlue Airways Corp.

United Parcel Service

Hawaiian Holdings Inc.

Alaska Air Group Inc.

LVMH Moet Hennessey Louis Vuitton

Hermes

CFR Financière Richemont

Tesla

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P/TSX Global Gold Index is designed to provide an investable index of global gold securities.

Delta is a ratio that shows how much the price of a derivative is likely to move based on the price change of an underlying asset.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All