Executive summary:

- Tax season isn't the only time advisors should think about how taxes may impact their client portfolios

- There are various strategies advisors can use year-round to ensure they are investing in a tax-efficient manner

- Helping your clients maximize their after-tax wealth is an important element of the value you provide

Here we are again, the time of year that brings many of us relief: Tax Day 2023 has arrived and that means tax season is done and gone! Or does it? When it comes to taxes, is our work ever truly done?

Just because we've made it to Tax Day doesn't mean we shouldn't be thinking about how to minimize the tax pain for clients going forward. There are still plenty of tax-smart ideas that can serve you and your clients well throughout the year. It's not always easy but focusing on tax management can result in higher after-tax returns for tax-sensitive investors.

Here are five tips that you can rely on at any time that can help improve your clients' after-tax wealth.

1. While using a "buy and hold forever" strategy is a frequent desire, the reality is you are likely to have to sell some of your holdings at some point. Pay attention to holding periods.

At Russell Investments, we talk a lot about the importance of having a long-term perspective, and this is especially relevant when considering the holding period of a security. When it comes to a tax-managed approach, the difference between a long-term and a short-term capital gain is huge.

Today, for example, long-term capital gains are taxed at 23.8% at the marginal federal tax level. But short-term capital gains are taxed at a whopping 40.8%. That's a significant difference. The thing is, the impact of these different tax rates on your clients is easily in your control.

The law defines a long-term holding period as 366 days while a short-term holding period is 365 days or less. So, one day can make a really big difference in the potential tax liability your client may experience.

2. Avoid wash sales.

We aren't talking about washing cars or laundry here. The wash sale rule is an Internal Revenue Service (IRS) rule. A wash sale is when you sell a security at a loss and then buy it – or a substantially similar security – back in 30 days or less. Doing this could generate a wash sale, which may either defer or sacrifice a loss in the client's portfolio.

It's relatively easy to avoid a wash sale. You just need to wait 31 days or longer to buy back that same, or a substantially similar, security you sold at a loss. Holding onto that loss is important because losses can be used as an effective tool to offset potential future gains in a taxable portfolio.

3. Markets move – often. While it would be easier if you only had gains to manage, losses do happen. Harvest losses when appropriate.

We've established that losses can represent an important lever in a taxable portfolio. Realized losses are a "tax asset." Harvesting losses in a portfolio can be a very effective strategy that allows a manager or advisor to essentially benefit from market volatility.

As the market and individual securities are moving up and down, there are often opportunities for managing – and potentially minimizing – the tax liability in a portfolio. It all comes down to understanding and monitoring your client's factor and sector positioning, the portfolio's individual tax lots, and the trading activity to carefully control the exposures in a portfolio.

When done well, harvesting losses could potentially lead to a better after-tax outcome for your clients.

4. It would be easier if all investment income was tax free, but that's not the case. Lean toward non-taxable interest and qualified dividends.

Investment income can often play an important role in the total return of a portfolio. In a taxable portfolio, it can pay to be aware of the tax implications associated with that income.

Income is generated by interest and dividends. On the fixed-income side, bonds pay interest. The vast majority of that interest is taxed as ordinary income. Now if a client is in the highest federal income tax bracket, ordinary income is taxed at 40.8%. That's a lot of potential return to give up to taxes!

But most municipal bonds have a zero percent tax rate, which means the income they generate is non-taxable. This can become an important consideration—especially for high earners.

On the equity side, there are two kinds of dividends. We want to focus on qualified dividends because they're the more attractive option for a tax-aware portfolio. Qualified dividends are taxed at 23.8%. That's a lot less than 40.8% and that's why each different source of income needs to be considered carefully.

At Russell Investments, we believe non-taxable interest and qualified dividends offer investors a more tax-efficient way to generate income for a taxable portfolio.

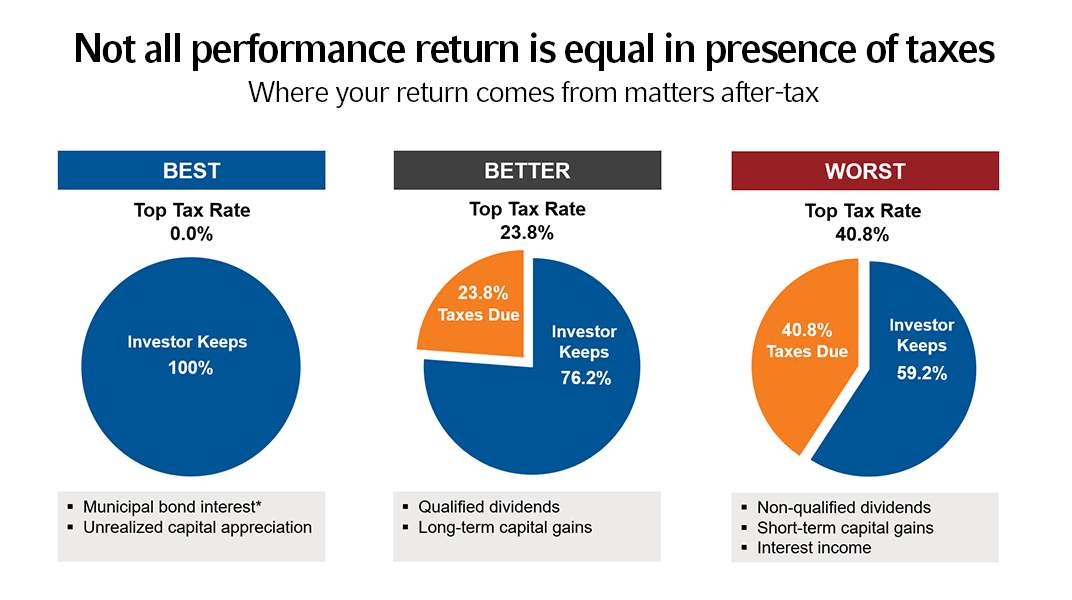

5. Understand the different tax rates that affect investment returns.

As we have already discussed, different tax rates are applied to different sources of investment return. The illustration below lays it out very simply.

Applies to federal taxes only. Source: Internal Revenue Service. Tax rates as reported by Internal Revenue Service as 2022. *Generally for municipal bonds, only interest from bonds issued within the state is exempt from that state's income taxes. Municipal bond interest income may impact taxation of Social Security benefits.

Be smart – tax smart! – in the way you invest. The cost of not investing in a tax-managed manner can be significant. Don't let it cost your clients when they need it most – in retirement. Proper investment tax planning today can save them a lot of money and stress, as well as potentially place them on a much better and smoother path to achieving their long-term goals.

The bottom line

Taxes can have a significant impact on your client's after-tax investment results. Tax smart planning and investing can put your client on firmer ground when it comes to preparing for their long-term needs and wants. And, importantly, it can be a key differentiator for your practice.

When you keep the strategies above in mind and take a tax-aware approach throughout the investment process, we think your clients stand a good chance of achieving a better after-tax return. And that's really what it's all about. Because at the end of the day, "It's Not What You Make, It's What You Get To Keep."

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

Russell Investments Financial Services, LLC, member FINRA, part of Russell Investments.

RIFIS-25545

© Russell Investments

Read more commentaries by Russell Investments