Consisting of 60% stocks and 40% bonds, this classic investment portfolio has historically been a trusted way to generate returns and diversify investor portfolios. However, we believe the 60/40 allocation may now be working against investors.

In addition to elevated inflation and fluctuating interest rates, the potential for positive correlation between stocks and bonds could undermine the advantages of a 60/40 portfolio. And, while bonds will continue to play a vital role in a balanced portfolio, we believe it’s time to consider a 60/20/20 investment allocation.

Bonds are Vulnerable to Fluctuating Interest Rates

Bonds have largely provided balance in investment portfolios. Their role as a diversifier in a 60/40 portfolio has been a successful formula for attractive risk-adjusted returns* that has worked well over the last thirty years in a period of declining interest rates. Today, with interest rates rising, we believe the 60/40 portfolio is subject to interest-rate risk. Consider these scenarios:

- Should interest rates go down, the value of currently held bonds rises. However, reinvestment from maturing bonds would be at lower interest rates, diminishing returns.

- Should interest rates rise, reinvestment of any maturing bonds would be at higher interest rates; however, the value of currently held bonds within the portfolio would decrease, stoking investor uneasiness.

- Stable interest rates may be the best scenario for portfolios, assuming interest rates stay relatively high. The portfolio value is relatively stable, and reinvestments will be made at relatively attractive rates. However, rates will likely rise and fall over time, and predicting these changes is difficult.

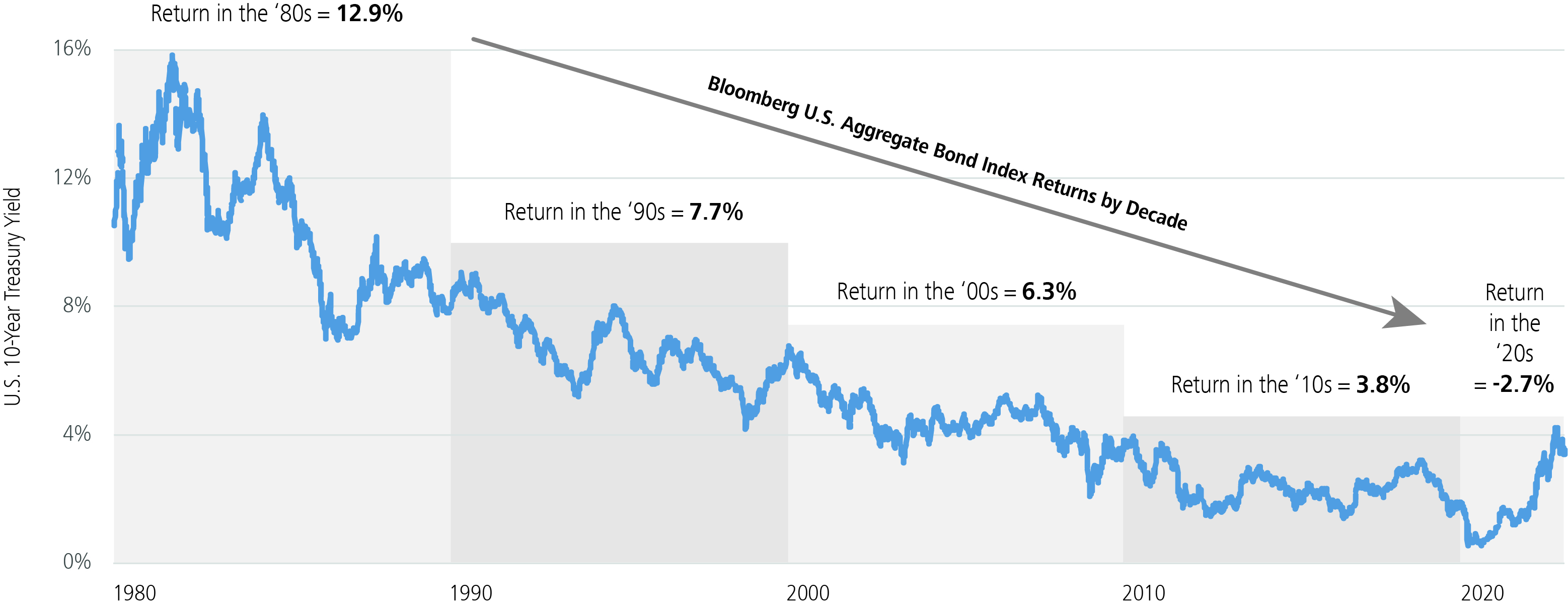

Bonds are Less Compelling Given Historical Performance

For decades, a 40% allocation to bonds was additive to a portfolio. More recently, however, as interest rates dropped, bond returns have declined.

Source: FRED, Morningstar Direct. Past performance is not a guarantee of future results.

U.S. 10-Year Treasury Yield, January 1, 1980 – December 31, 2022.

Despite suffering the worst year (2022) since its inception in 1980, the Bloomberg U.S. Aggregate Bond Index still returned 6.85%, a very respectable number. Is it possible for bonds to deliver anything close to this in the future?

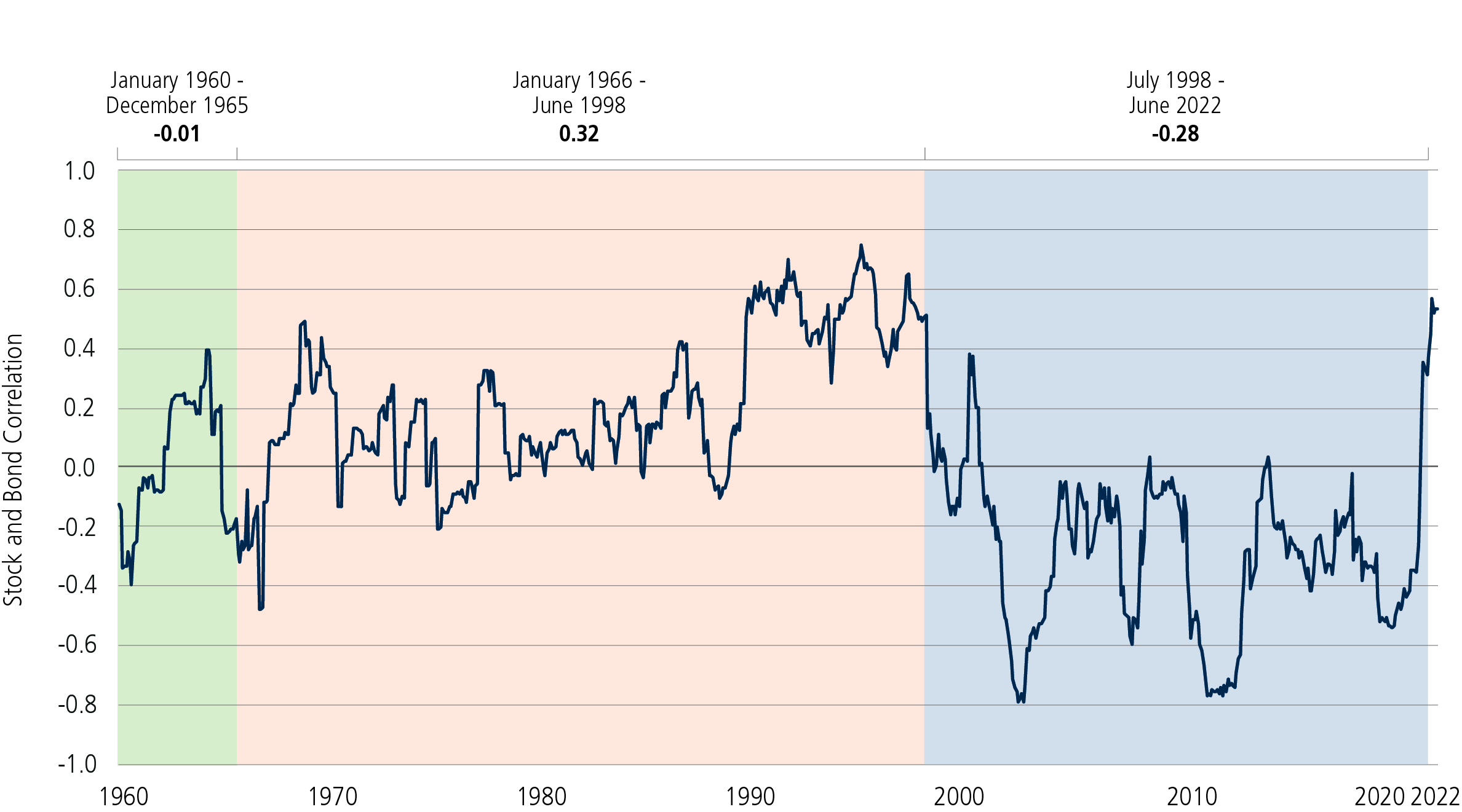

Stocks and Bonds Have Not Always Been Uncorrelated

In recent years, stocks and bonds have generally moved in opposite directions allowing bonds to serve as ballast in portfolios. More recently, the two have started to move in tandem as they've become positively correlated as they have in the past. A positive correlation between stocks and bonds doesn't bode well from a diversification standpoint, and underscores the potential benefits of adding strategies historically uncorrelated to each of them.

Figure 2. Correlation Between Stocks and Bonds has Fluctuated Over Time

Source: LoCorr Fund Management. Data as of December 31, 2022. Correlation: S&P 500 Index with SBBI U.S. Long Government Bond Index. Time period January 1, 1960 – December 31, 2022.

Consider the 60/20/20 Investment Allocation

With bond returns declining over the last 40 years and (now) moving in sync with stocks, we propose a 20% allocation away from bonds and into assets with a low correlation to both fixed income and equities.

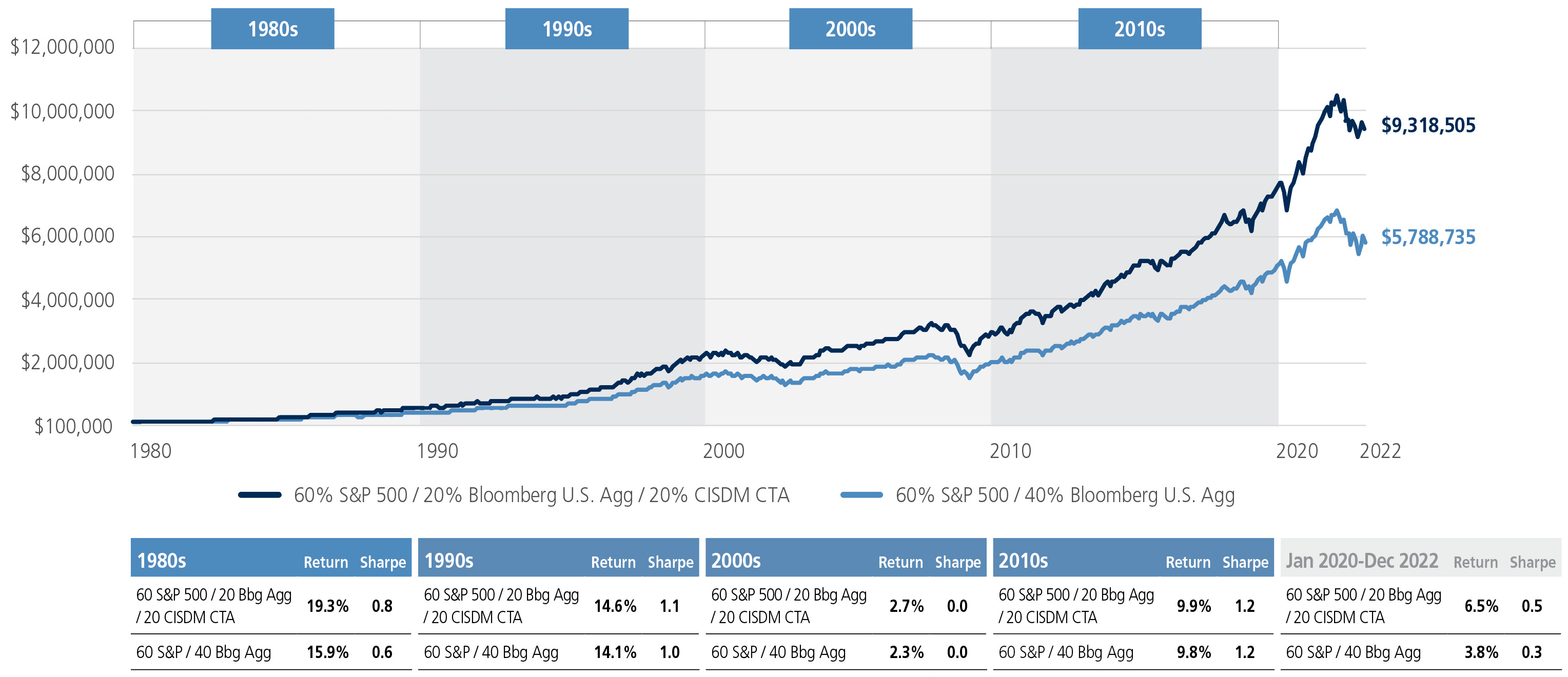

Over the last four decades, including a 20% allocation to a low-correlating sleeve would have been additive from both a return and Sharpe Ratio standpoint.

Figure 3. The 60/20/20 Allocation Outperformed over Historical Periods

Source: Morningstar Direct. Past performance is not a guarantee of future results. Time period is 1/1/80-12/31/22.

As shown above, using a managed futures index, the CISDM CTA Index, as a proxy for a low volatility, low correlation sleeve, a hypothetical 60/20/20 allocation would have bettered that return at 19.3% and provided an improved Sharpe Ratio.

While we cannot predict how the future will unfold, in the 40+ year period shown above, the 60/20/20 portfolio outperformed by more than 1%, and with a higher Sharpe Ratio.

Building More Resilient Portfolios for the Long-Term

With interest rate uncertainty, inflation, and the potential for positive correlation undermining the benefits offered by bonds, such as diversification and stable return streams, investors may wish to rethink a 40% allocation.

How should they modify the portfolio's investment components? Think about a 60/20/20 mix that includes a 20% strategic allocation to strategies uncorrelated to both equity and bonds.

As our analysis shows, portfolios with allocations to low-correlating sleeves outperformed over the long term, added beneficial levels of diversification, and improved traditional portfolios' overall risk/return profile. A low-correlating sleeve could be a critical component in keeping clients invested during times of stress and help them achieve their financial goals regardless of what lies ahead.

*Risk-adjusted return is a measure of the return on an investment relative to the risk of that investment, over a specific period.

Diversification does not assure a profit or protect against loss in a declining market. Correlation measures how much the returns of two investments move together over time. Sharpe Ratio measures the amount by which a set of values differs from the arithmetical mean, equal to the square root of the mean of the differences’ squares.

Bloomberg Capital U.S. Aggregate Bond Index is the most common index used to track the performance of investment grade bonds in the United States. S&P 500 Index is a capitalization weighted unmanaged benchmark index that includes the stocks of 500 large capitalization companies in major industries. This total return index includes net dividends and is calculated by adding an indexed dividend return to the index price change for a given period. SBBI U.S. Long Government Bond Index measures the performance of a single issue of outstanding US Treasury bond with a maturity term of around 21.5 years. It is calculated by Morningstar and the raw data is from Wall Street Journal. CISDM CTA Index is designed to broadly represent the performance of all CTA programs in the Morningstar database that meet the inclusion requirements.

Past Performance does not guarantee future results. Index performance is not indicative of fund performance. For current standardized fund performance, please call 1.855.LCFunds or visit www.LoCorrFunds.com. The performance of various indices is shown for comparison purposes only. The performance of those indices was obtained from published sources believed to be reliable, but which are not warranted as to accuracy or completeness. Unless noted otherwise, index returns do not reflect fees or transaction costs and reflect reinvestment of net dividends. One cannot invest directly in an index.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 1.855.LCFUNDS, or visiting www.LoCorrFunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. The Funds are non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Funds are more exposed to individual stock volatility than a diversified fund. The Funds invest in foreign investments and foreign currencies which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investing in commodities may subject the Funds to greater risks and volatility as commodity prices may be influenced by a variety of factors including unfavorable weather, environmental factors, and changes in government regulations. Investing in derivative securities derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks, and, depending upon the characteristics of a particular derivative, suddenly can become illiquid. Derivative contracts ordinarily have leverage inherent in their terms which can magnify the Fund’s potential for gains or losses through increased long and short position exposure. The Fund may access derivatives via a swap agreement. A risk of a swap agreement is the risk that the counterparty to the agreement will default on its obligation to pay the Fund. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset Backed, Mortgage Backed, and Collateralized Mortgage-Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The LoCorr Dynamic Equity Fund may invest in small- and medium-capitalization companies which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in lower-rated and non-rated securities which present a greater risk of loss to principal and interest than higher-rated securities. ETF investments are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are subject to specific risks, depending on the nature of the ETF. The Spectrum Income Fund’s portfolio will be significantly impacted by the performance of the real estate market generally, and the Fund may be exposed to greater risk and experience higher volatility than would a more economically diversified portfolio. Property values may fall due to increasing vacancies or declining rents resulting from economic, legal, cultural, or technological developments. Investments in Limited Partnerships (including master limited partnerships) involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the Limited Partnership, risks related to potential conflicts of interest between the Limited Partnership and the Limited Partnership’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. Underlying Funds are subject to management and other expenses, which will be indirectly paid by the Fund.

The LoCorr Funds are distributed by Quasar Distributors, LLC. © 2023 LoCorr Funds