Key points

-

Dilemma to trilemma: Banking system stress has added a third dimension of financial stability to the existing policy challenge of balancing inflation and growth objectives.

-

Decoding the market disconnect: Alternative data indicators show signs of continued labor market strength amid shifting consumer confidence. Are bond markets accurately predicting a recession or does the persistent strength of equities suggest that expectations of a hard landing are misguided?

-

Equity market positioning: Positioning has turned more defensive, with a preference for quality, large cap companies. A data-driven, systematic approach may help investors capitalize on opportunities in security selection amid heightened dispersion.

The sudden collapse of two US regional banks and the forced acquisition of Credit Suisse in Europe introduced a third dimension to the existing policy dilemma of balancing inflation and growth objectives: financial stability. The swift policy reaction from government officials appeared to stem widespread contagion and systemic issues across the banking system. Now, markets are reassessing the economic outlook given the new constraint that banking stress puts on the policy framework to fight inflation and the potential economic impact of tighter lending standards. These dynamics, along with the trajectory of inflation and growth, are at the center of the new policy trilemma.

As the bank run episode unfolded, market focus shifted from inflation and policy direction for much of 2022 to growth and recession fears in 2023. Rate volatility soared as bond markets priced in a higher likelihood of recession and the end of the hiking cycle. Conversely, equity markets have shown greater resilience on the surface with strongly positive returns throughout the start of 2023.

Divergence in market pricing across asset classes raises questions over what lies ahead for investors. Is bond market pricing of a recession justified? Is the rotation away from value and in favor of large cap equities a recessionary canary in the coal mine? If we are headed for a recession, why have equity returns held up so strongly? To help answer these questions, this outlook explores alternative data measures across each element of the policy trilemma: financial stability, growth, and inflation—to gain a better understanding of what they may mean for markets and portfolios.

1. Financial stability

To tame inflation, it’s been said that central banks can freely tighten policy until something breaks. One year into the fastest tightening cycle since the 1980s, bank failures and takeovers sent shockwaves through financial markets on fears that something had broken. Regulators in the US quickly responded with implicit deposit guarantees and liquidity facilities to backstop the banking system. In Europe, authorities rushed to help structure a deal for the takeover of Credit Suisse by UBS.

With systemic banking risks seemingly under control, the effects of banking stress on credit conditions have come into focus. Market pricing of rate cuts could imply that tightening from stricter lending standards will substitute for future rate increases. As shown in Figure 1, we haven’t seen significant levels of tightening in US credit conditions in the weeks following the bank failures. This isn’t a surprise given the time it can take for changes in credit issuance to go into effect. For example, during the Great Financial Crisis (“GFC”), sustained tightening trends only began to surface roughly three months after the collapse of Lehman Brothers and the tightening impulse didn’t peak until a year later.

Figure 1: US credit conditions haven’t significantly changed in response to bank failures

Percentage change in bank credit vs. March 8, 2023

Early signs of tightening following the banking turmoil have been concentrated in commercial loans, which also acted as a leading indicator for broader credit markets during the GFC. While more credit tightening is expected, the notion that a significant change in credit conditions will occur quickly enough to substitute for near-term rate hikes appears unlikely. As the US Federal Reserve (“Fed”) faces upcoming policy rate decisions, an absence of obvious tightening in credit conditions may result in continued hawkish guidance if the outlook for inflation doesn’t improve.

2. Inflation

In the weeks since banking system stress began, developed market central banks have continued their fight against inflation while acknowledging economic stability risks. The Fed, for example, announced their ninth straight interest rate increase in March, underlining their intention to use separate tools to combat financial stability versus price stability issues.

Recent data releases have shown that inflation remains persistently high, despite peaking near the end of 2022. This has shifted the Fed’s focus away from headline figures and towards the sticky core services ex-housing portion of inflation. In other words, they’re looking for evidence of labor market normalization, as wages make up a large portion of cost in delivering services. Core services ex-housing inflation has closely tracked the pace of wage growth since the post-COVID economic reopening began.

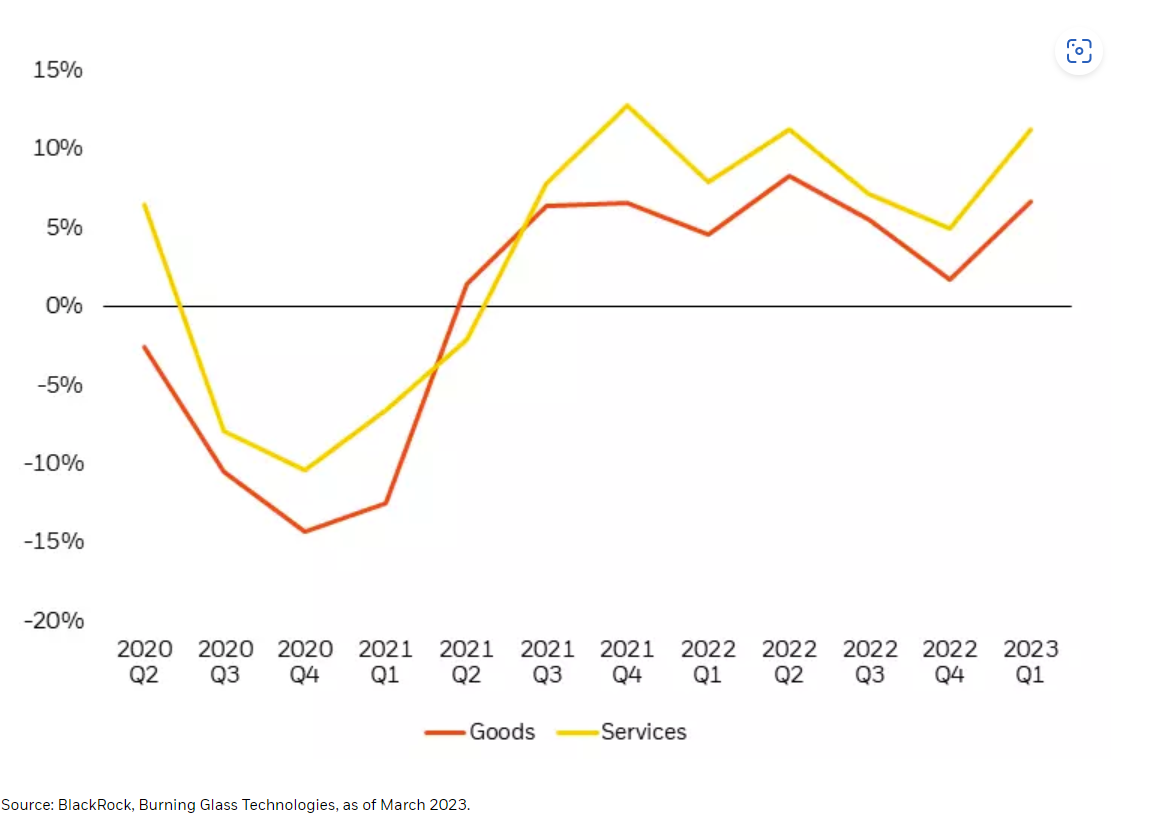

To forecast wage growth ahead of official data releases, we analyze real-time wage data from online job postings. This provides a differentiated view into the direction of wage inflation, and in turn, services inflation. Figure 2 shows that based on our analysis, we expect upcoming realized figures to show an increase in wage growth led by services roles, likely forcing the Fed to maintain their hawkish stance.

Figure 2: Wage growth is expected to remain elevated across goods and services sectors

Year-over-year wage inflation, goods vs. services, occupation weighted

Shelter is another component that plays a key role in shaping the inflation outlook. Shelter makes up 60% of the services category within the core Consumer Price Index (“CPI”)—even larger than the core services ex-housing portion that coincides with labor markets. While the shelter component of CPI appears to have peaked, it may take longer to normalize than investors expect. We analyze a combination of current and lagged changes in rental growth from online aggregators to forecast the Owners’ Equivalent Rent (“OER”) component of CPI (Figure 3). If the growth rate of online rental prices continues declining at the current pace, the expected decline in official OER in the coming months is unlikely to be significant enough for the Fed to change course.

Figure 3: While shelter inflation has likely peaked, declines in rental growth are unlikely to be significant enough to allow for rate cuts

Expectations for the Fed to deliver on the recently priced rate cuts may be somewhat overstated in the current environment of stubbornly high inflation and lagged credit tightening. Until progress in restoring price stability is more evident, interest rates may need to remain higher for longer than markets expect.

3. Growth

Throughout the policy tightening cycle, the strength of consumers has helped to keep a growth downturn at bay, despite looming fears of recession. Pandemic stimulus measures have bolstered household balance sheets and helped build a reserve of excess savings. The post-COVID economic reopening unleashed pent up demand for services and kept spending robust throughout the last year. Labor market strength also contributed to sustained spending power as consumers benefited from higher income growth.

Now, the challenges of the banking system may be driving a shift in consumer behavior. Excess savings still provide consumers with the ability to spend, but bank failures and growth concerns may be impacting consumers’ willingness to spend. We see evidence of this in consumer spending data which has started to weaken (Figure 4). Declines in activity have been the most severe within the lowest income cohort.

Figure 4: Consumer spending has started to decline, with the sharpest pullback in the lowest income cohort

Year-over-year consumer spending by income cohort (%

Putting it all together

While policy measures to support banks and depositors have helped prevent a widespread banking crisis, alternative data indicators point to evolving economic challenges ahead. The recent pullback in consumer activity signals a shift in consumer confidence and a potentially weakening economic growth outlook. It seems unlikely that near-term credit tightening will be significant enough to substitute for upcoming rate hikes. In the meantime, sticky inflation is likely to require a higher path for policy rates and expectations for rate cuts may be premature.

What does this mean in the context of market pricing? Figure 5 shows the current disconnect between equity and bond investors—with bond markets pricing in a much higher probability of recession than equity markets. Historically, in rare periods where the implied recession probability of bonds has exceeded equities by the current magnitude, bond markets have been proven correct more often than not in predicting a recession over the next year. This outcome opposes current equity market pricing, which raises the possibility of headwinds for equity beta and a further market rotation in the near future.

Figure 5: Historical evidence suggests that equity market pricing may not reflect recent economic developments

Equity and bond market implied recession probability for the next 12 months

If history is a guide, investors may want to bet with bond markets. However, there are nuances to the current situation that make it less clear cut. The call for a recession is the consensus view in the fixed income market and it has been the consensus view for some time—yet equities continue to deliver strong performance year-to-date. This begs the question: are recessions always bad for risky assets, or furthermore, is there still a narrow path to avoiding a recession? In our view, the consumer would be the key to avoiding a recession in 2023 by reversing recent declines in spending, supported by still robust excess savings and a strong labor market.

Equity market positioning and opportunities

In response to the evolving economic and market outlook, our global equity portfolio positioning has shifted to a more defensive stance than market consensus. We see opportunities in security selection with a preference for high quality, large cap companies. Within the style dimension, we’ve adopted a more cautious view towards value as economic growth concerns have increased.

From a security selection perspective, the recent shift in market focus from inflation and policy to growth and earnings has made company-specific factors a more relevant driver of performance. We’ve seen this dynamic playing out across the banking sector in recent weeks. The non-systemic nature of the banking crisis created divergence in performance between banks with high unrealized portfolio losses and high uninsured deposits and those with the opposing quality characteristics (Figure 6). This heightened level of security dispersion has created new opportunities to exploit relative performance differences across companies.

Figure 6: Banking stress created divergence between “good banks” with higher quality characteristics versus those with potential liquidity concerns.

Bank performance by characteristics including high commercial real estate exposure, high unsecured deposits, high unrealized losses to total deposits, and “good banks” with high quality characteristics.

A data-driven, systematic investment approach can provide an informational advantage in security selection, enabling granular analysis of companies across a broad opportunity set. With traditional asset classes facing continued pressure, implementing these insights in a market neutral structure that seeks to take advantage of dispersion and quickly recalibrate portfolios in response to evolving market dynamics may help to build portfolio resilience.

Conclusion

Financial stability considerations have turned the previous policy dilemma of balancing growth and inflation objectives into a trilemma. This introduces another layer of complexity to the economic and market environment. While bonds have historically been more accurate at recession forecasting than equities, the persistent strength of equity markets presents potential alternative scenarios that may be more supportive of risk assets. The use of alternative data allows us to explore the contradiction in current market dynamics and the full range of potential outcomes as they evolve in real-time. In our view, uncovering alpha opportunities in today’s challenging environment requires a data-centric, systematic investment approach—allowing us to remain nimble as investors during a time where dynamism matters most.

© BlackRock

Read more commentaries by BlackRock