"With the exception of the Great Depression of the 1930s, the Great Inflation of the 1970s is generally viewed as the most dramatic failure of macroeconomic policy in the United States since the founding of the Federal Reserve." Athanasios Orphanides, Professor, MIT Sloan School of Management

What went wrong last year?

According to one estimate (see here), households worldwide lost about $23Tn of wealth last year – mainly because of falling property and equity prices. That exceeds the losses suffered during the Global Financial Crisis (GFC). Losses back then were approximately $18Tn worldwide. I bring this up, as it shows how important liquidity has become in financial markets. The GFC did much more damage to the global economy than anything we endured in 2022, but liquidity last year was very tight.

The cost of capital (i.e. interest rates) is another way to think of liquidity and its importance to the wellbeing of financial markets. When interest rates were close to zero, plenty of borrowing took place for financial investment purposes, and that drove up risk asset prices. At the same time, households and corporates were reluctant to park excess capital with banks or in money market instruments, as the expected return was nil. Instead, they invested in risk assets.

Now, if you look back on the post-GFC era – an era I prefer to call the QE era – it is little wonder that household wealth grew so much during those years. Think about it. The cost of capital was non-existing. There was plenty of liquidity in the system thanks to central banks’ appetite for QE, and you couldn’t earn a dime on your capital, unless you were prepared to take some risk. And to cap it all – Wall Street were busy telling private investors that, as long as they followed a 60/40 investment strategy, they would never lose out, as equities and bonds are always negatively correlated (they said).

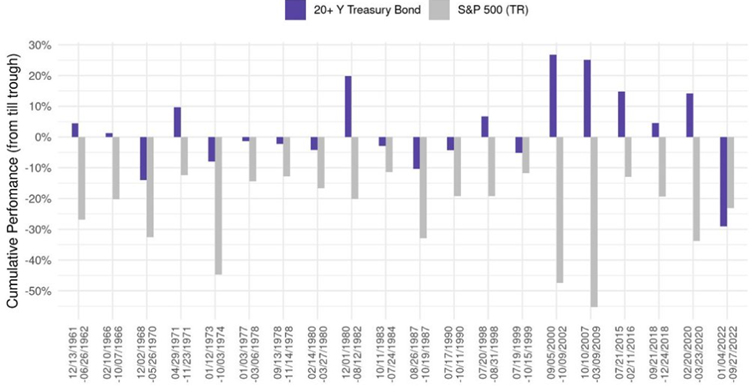

Reality turned out to be very different, though. The correlation between bond and equity returns, which had been negative for many years, suddenly turned positive (Exhibit 1), and all those ’wonderful’ 60/40 funds that investors had put their savings into began to deliver negative returns. And, to add insult to injury, for the first time ever, bonds losses were bigger than equity losses last year.

The positive correlation between bond and equity returns was not the only reason investment conditions were so challenging in 2022. For example, here in the UK, Liz Truss did her best to make life miserable for investors, UK pension funds in particular, and that had a meaningful, and negative, impact on UK household wealth. In fact, her semantics last autumn had such a dramatic impact on bond yields that the Bank of England was forced to re-introduce QE to save UK pension funds from total collapse.

More insight, more advice, more in-depth.

Exhibit 1: Performance of 20-year+ T bonds & S&P 500 Note: Performance calculated as cumulative performance over periods indicated Source: Sound Money LLC

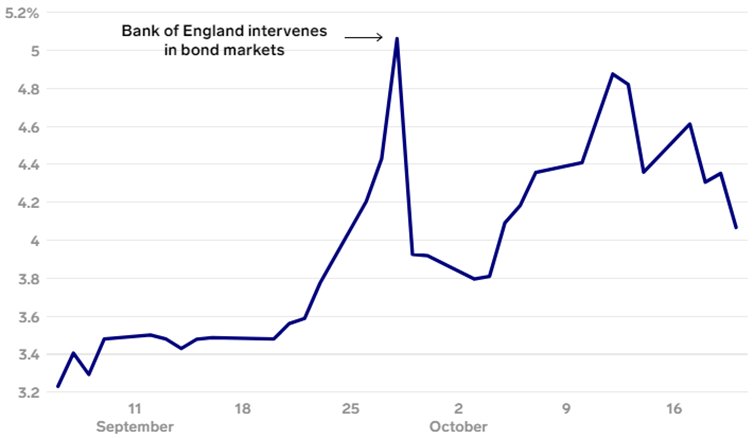

As you can see in Exhibit 2 below, over a few short days in late September last year, UK bond yields rose sharply and quickly. Because bond yields rose so rapidly, many DB pension plans couldn’t meet the higher collateral requirements to support their hedging programmes and had to reduce the hedge ratio. The Bank of England intervened, and Liz Truss was pushed out, but it was all too late. British DB pension plans were now partially unhedged against interest rate declines, which caused their liabilities to rise when interest rates began to fall again. Consequently, the funding ratio deteriorated to the detriment of their members.

Exhibit 2: Yield on 30-year Gilts during Liz Truss’ premiership Source: Business Insider

What’s next?

I have no idea precisely when and where the next crisis will show up. Having said that, I can assure you there will be another one at some point in the not so distant future. Therefore, I can say with a great deal of confidence that the QE era is not over yet whether QE proper or in stealth, but what do I mean by that?

Even if we were to escape a serious crisis for many years, the global economy is quite clearly slowing down at the moment. That can, at best, end in a soft landing or, at worst, in a recession. If you are an ARP+ subscriber and have not yet read our new research paper on this topic (called Is It Time to Turn Bullish?), I suggest you do so. You can find it here.

Given the Fed’s dual mandate (to foster economic conditions that achieve stable prices whilst, at the same time, aiming for maximum sustainable employment), assuming inflationary concerns continue to fade, we are not, in my opinion, that far away from a return to QE. You could argue that the high current level of consumer price inflation leaves the Fed in a bit of a pickle but I will argue that, as long as PPI is lower than CPI (as it is), CPI will almost certainly continue to decline, and that will probably be enough for most central bankers to take action.

Core PPI in the US is down to +3.4% year-on-year as of the latest count, and I don’t think 3.4% will lead to many sleepless nights in the Fed camp. I also think the Fed is quite happy for inflation to be somewhat higher than 2% for a few years. After all, inflation destroys debt, and we need some debt to go away after having built a colossal mountain of it over the last few decades. And I am not only pointing fingers at the Fed. Other countries are drowning in debt too and could do with some debt destruction.

The problem is that QE is essentially inflationary. To begin with, it may only be asset inflation that is affected but, as we have learnt over the past couple of years, consumer price inflation will also be affected eventually. It is therefore no mean task confronting the Fed and other central banks inclined to use QE to stimulate economic activity.

Niels C. Jensen 28 April 2023

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

In 2018, Harriman House published The End of Indexing, Niels' first book.