At the CMT Association’s 2023 Annual Symposium in New York last week, I had the incredible opportunity to interview legendary trend follower Jerry Parker for Episode #29 of the Fill the Gap podcast. Jerry is arguably the most successful trader to have emerged from the infamous “Turtle” trading experiment of the early 1980s, underwritten by Richard Dennis and Bill Eckhardt in an effort to resolve a debate about whether successful trend following was an innate ability or if anyone could learn to do it. After being taught the critical tenets of trend following, Jerry went on to start Chesapeake Capital, becoming one of the most successful trend followers in modern times. Apparently, it was settled. It can be taught, no natural talent necessary. Or was it?

At the CMT Association’s 2023 Annual Symposium in New York last week, I had the incredible opportunity to interview legendary trend follower Jerry Parker for Episode #29 of the Fill the Gap podcast. Jerry is arguably the most successful trader to have emerged from the infamous “Turtle” trading experiment of the early 1980s, underwritten by Richard Dennis and Bill Eckhardt in an effort to resolve a debate about whether successful trend following was an innate ability or if anyone could learn to do it. After being taught the critical tenets of trend following, Jerry went on to start Chesapeake Capital, becoming one of the most successful trend followers in modern times. Apparently, it was settled. It can be taught, no natural talent necessary. Or was it?

To me, the most interesting observation about the turtle experiment is that Jerry was one of 20 original turtles, all smart, driven individuals who were taught directly by the two “Masters of the Trend Following Universe”. Each turtle was taught the same exact entry and exit rules, the same exact risk management scheme, and all twenty traded from the same exact office. With such a level playing field presented to all twenty turtles, why is it that Jerry Parker is the only one to have emerged from that experiment as a truly successful trend follower? Clearly, it’s not just the trading rules or risk management scheme. If it were, all twenty turtles would be successful today.

Our conversation was therefore focused on proper mindset, which I believe is the most overlooked ingredient in successful investment outcomes. While mindset management is critical to the portfolio manager’s ability to execute a strategy through both good times and bad, Jerry and I finished our discussion about mindset with a focus on the manager’s clients, and the importance of making sure their mindset was just as fine-tuned as the manager’s. We all know the unfortunate but true story about how Peter Lynch delivered returns in excess of 20% during his tenure on the Fidelity Magellan Fund, but due to performance chasing and panic selling, the average investor’s return in the very same fund was closer to 10%. Why? Improper expectations, which led to a clouded mindset and poor buy and sell decisions during periods of outperformance and underperformance, respectively.

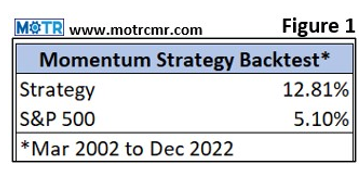

Trend following and momentum investing have been among the best performing investment strategies throughout history. There are many empirical examples that support this statement (Jerry Parker being just one), along with volumes of academic research all condoning momentum and trend following as valid inputs to an investment process. In Figure 1, I am showing the returns of a simple momentum model backtest from 2002 to 2022. Clearly, anyone interested in maximizing their returns over the long-term would be interested in learning more about this strategy.

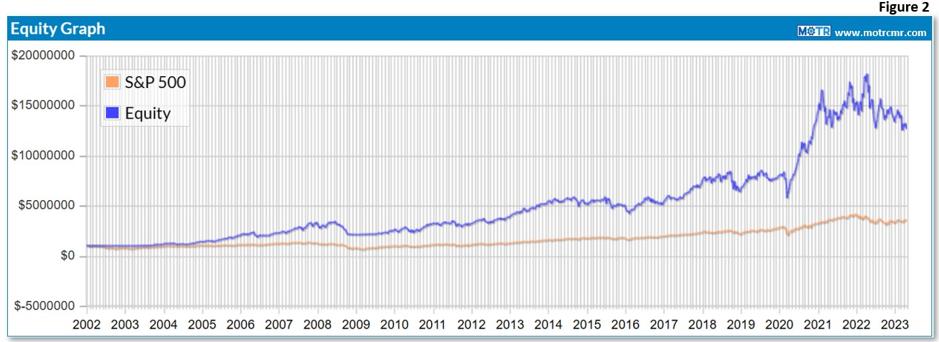

To make things even more alluring, I might use a chart to demonstrate the strategy’s long-term performance relative to the S&P (Figure 2). One might look at this chart and conclude, “Sure, there were brief periods when the strategy struggled, but it was worth it, because the long-term returns were so good! And I know for sure I’d be able to stay invested in the strategy during those hard times.”

Then, the inevitable happens. The strategy not only starts to underperform, but it goes down while the market goes up! In fact, year-to-date, this strategy is down nearly -5%, while the S&P is up over 8%. Because this is just a hypothetical discussion, and we are not actually experiencing this “pain” in reality, we might still be able to confidently say “no problem, I would remain committed.” However, the reality is that this is precisely the moment when successful strategies begin to experience outflows, ala my earlier real life example with Peter Lynch.

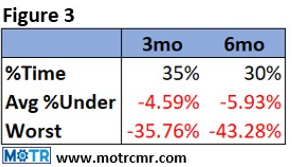

Without proper expectations, our mindset will not be adequately prepared to endure the inevitable periods of discomfort that accompany even the best active investment strategies. Figure 3 shows that this strategy underperformed the S&P roughly 1/3 of the time over both rolling 3 month and 6 month periods. If you’re not expecting this, you will struggle to stay focused on the long-term. Worse yet, if your clients aren’t expecting this, they will abandon your strategy on the slightest sign of underperformance.

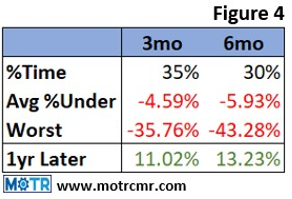

The cost of poorly managed expectations, resulting in an improper mindset driving inopportune buy and sell decisions cannot be overstated. Figure 4 updates Figure 3 with what happens over the next 12 months following a 3 or 6 month period of strategy underperformance. Clearly, liquidating an investment during periods of short-term underperformance by a strategy that works over time is debilitating to long-term returns. Desiring to achieve those long-term results while being unwilling to endure the necessary short-term pain has no impact whatsoever on the strategy’s long-term performance, only the investor’s experience relative to it.

During my discussion with Jerry, I made the observation that even the calmest and even keeled mindset will not make a bad strategy good. Clearly, the strategy must “work” over time. That said, even having both a “Zen-like” manager and a winning strategy is still not enough. All parties involved–the portfolio manager, company management, the sales team, the marketing team, and finally, but most importantly, the client–must share the same commitment to the strategy, a commitment anchored to proper expectations.

Read more commentaries by MOTR Capital Management & Research, Inc.

At the CMT Association’s 2023 Annual Symposium in New York last week, I had the incredible opportunity to interview legendary trend follower Jerry Parker for Episode #29 of the Fill the Gap podcast. Jerry is arguably the most successful trader to have emerged from the infamous “Turtle” trading experiment of the early 1980s, underwritten by Richard Dennis and Bill Eckhardt in an effort to resolve a debate about whether successful trend following was an innate ability or if anyone could learn to do it. After being taught the critical tenets of trend following, Jerry went on to start Chesapeake Capital, becoming one of the most successful trend followers in modern times. Apparently, it was settled. It can be taught, no natural talent necessary. Or was it?

At the CMT Association’s 2023 Annual Symposium in New York last week, I had the incredible opportunity to interview legendary trend follower Jerry Parker for Episode #29 of the Fill the Gap podcast. Jerry is arguably the most successful trader to have emerged from the infamous “Turtle” trading experiment of the early 1980s, underwritten by Richard Dennis and Bill Eckhardt in an effort to resolve a debate about whether successful trend following was an innate ability or if anyone could learn to do it. After being taught the critical tenets of trend following, Jerry went on to start Chesapeake Capital, becoming one of the most successful trend followers in modern times. Apparently, it was settled. It can be taught, no natural talent necessary. Or was it?