Key takeaways

- Higher central bank policy rates have increased the cost of capital for corporations and other issuers of debt.

- Asset classes that are experiencing those higher interest costs sooner, such as leveraged loans and certain real estate markets, may warrant caution.

- Our strategy for navigating higher interest rates is to take a measured approach. We are proponents of owning more high quality, defensive asset classes.

The cost of capital is up – your guardrails should be too

A direct repercussion of higher central bank policy rates is on the cost of capital for corporations and other issuers of debt. However, not all issuers feel the impact of higher rates at the same time, and we’re more cautious on asset classes that are experiencing higher interest costs sooner.

Why? First, the increased cost of making these higher coupon payments has to come from somewhere, i.e. higher costs on debt repayments can result in fewer dollars available to spend on investing in and growing their businesses. Second, in the more extreme example, issuers whose costs have risen beyond their capacity to pay their coupon requirements could face default, which would impair the price of the bonds to debt holders. Lets bring this to life with a few examples.

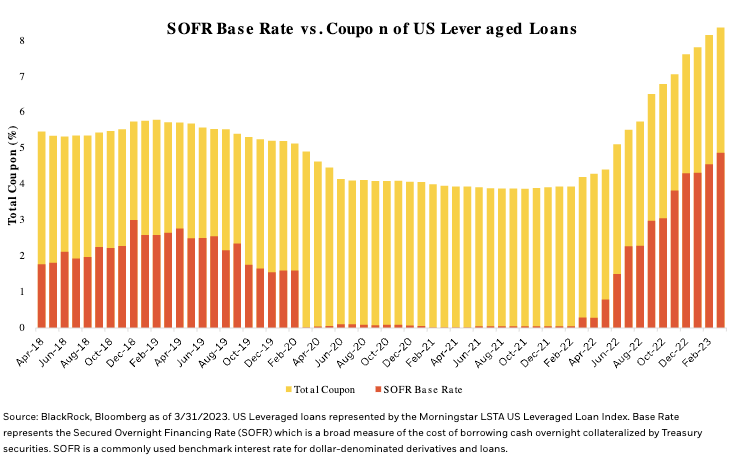

Leveraged loan issuers are prone to bear the cost burden

Take leveraged loans, commonly known as bank loans, for instance. One of the most attractive features of bank loans to investors is their floating rate coupon structure, which makes them very low duration bonds. Duration is a measure of interest rate sensitivity. The longer a bond’s duration, the more price sensitive it is to changes in interest rates. Thus, zero duration floating securities like leveraged loans are less vulnerable to rising rate-related price downside. This is exactly the benefit investors in bank loans experienced in 2022 as the Fed raised rates seven times. From the first Fed rate hike on March 17th, 2022 through year-end, the Morningstar LSTA US Leveraged Loan Index returned 0.75% compared to the much longer duration Bloomberg US Aggregate Bond Index, which returned -7.94% (source: Morningstar).

Fast forward to today, we believe the Fed will pause rate hikes later this year, and we anticipate worries around a growth slowdown to escalate.

In other words, we believe the benefit of bank loans’ floating rate structure has largely been realized and may turn into a hindrance instead. As interest rates have risen, bank loans’ all-in coupons – which consist of a fixed rate agreed upon at issuance plus a base rate that fluctuates according to a floating rate index such as the Secured Overnight Financing Rate (“SOFR”) – have increased dramatically, as the chart below illustrates. In fact, the average coupon for leveraged loans has nearly doubled since the first quarter of 2022.

Issuers of bank loans, the very large majority of whom are below-investment grade rated companies, are now facing all-in interest expenses of 8.4% (March 2023) versus a low 3.9% one year ago (February 2022). Compared with other below investment grade asset classes like High Yield bonds, this could be a source of serious stress on the issuer. High yield bonds, for instance, have seen their coupons stay relatively flat over the same period (5.7% in February 2022 to 5.8% in March 2023 according to Bloomberg data. High yield is represented by the Bloomberg US High Yield 2% Issuer Cap Index).

That’s not to say the all-in yield on High yield hasn’t risen as market worries have led spreads to widen out, bringing the yield to worst on the High yield Index to 8.5% as of the end of March 2023 (source: Bloomberg). However, spreads are a reflection of the additional risk premia required by investors for buying the credit risk of the issuer on the secondary market, and High yield issuers typically only face these higher interest costs when they need to issue more debt or refinance their existing debt. So far, most companies have not needed to do this and so their interest expense has only risen very gradually. Lastly, we’re particularly wary of issuers who are loan-only (i.e. all the their debt is floating rate in nature), who make up about 73% of the Morningstar LSTA Leveraged Loan Index as of March 31, 2023.

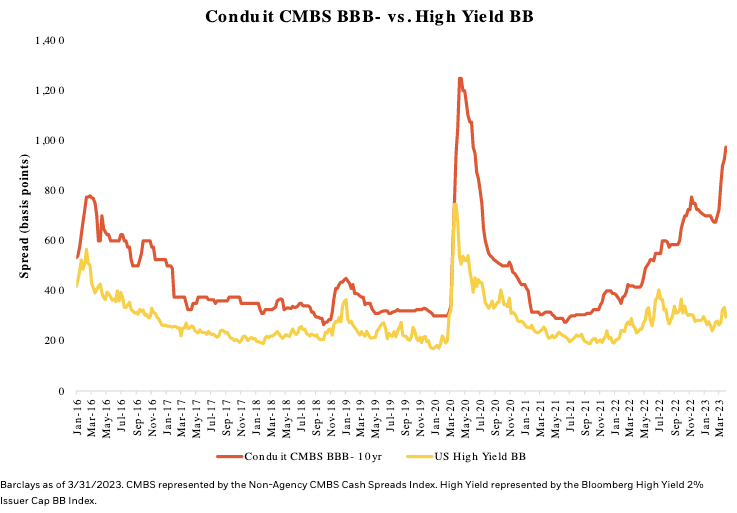

Real estate markets may also be challenged

Commercial real estate has come under fire over recent months as stress in the banking sector has put a spotlight on real estate funding. One of the key elements of our concern is the fact that $1.1 trillion in commercial mortgages are maturing in 2023 and 2024 and these properties are likely going to face far tighter lending standards (i.e. higher interest costs or difficulty getting loans at all) when they need to refinance. This risk is already being reflected in the price of Commercial Mortgage Backed Securities (CMBS). As the chart below outlines, the spread on BBB- rated conduit CMBS has widened by +2.7% year to date to 9.75%, and more than doubled year over year.

While public REITs are not reliant on one form of financing, they are also not immune from the broader perception of challenges in the commercial real estate space. We expect interest expense to rise over the coming year, which can negatively impact the cash flow and profitability of these businesses, even without the onset of recession.

Avoiding the landmines

Our strategy for navigating higher interest rates and the corresponding investing repercussions is to take a measured approach. We are proponents of owning more high quality, defensive asset classes like agency mortgages, investment grade corporate bonds, and dividend-paying stocks with stable cash flow features. We believe leaning away from areas most exposed to higher financing costs is a prudent decision.

Investing involves risks, including possible loss of principal.

This material is provided for educational purposes only and is not intended to constitute investment advice or an investment recommendation within the meaning of federal, state or local law. You are solely responsible for evaluating and acting upon the education and information contained in this material. BlackRock will not be liable for direct or incidental loss resulting from applying any of the information obtained from these materials or from any other source mentioned. BlackRock does not render any legal, tax or accounting advice and the education and information contained in this material should not be construed as such. Please consult with a qualified professional for these types of advice.

There is no guarantee that any investment will pay dividends.

Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Mortgage-backed securities ("MBS") and commercial mortgage-backed securities ("CMBS") are subject to prepayment and extension risk and therefore react differently to changes in interest rates than other bonds. Small movements in interest rates may quickly and significantly reduce the value of certain mortgage-backed securities.o the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK and ALADDIN are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

iCRMH0523U/S-2872521

© BlackRock

Read more commentaries by BlackRock