Final Approach: May 2023 Economic Update

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive summary:

- The U.S. economy is likely slowing down, and a recession seems likely in the 12-18 month time horizon

- The economic and market path won’t necessarily be linear, and there can be uncertainty in the outlook

- The potential recession would likely lean more toward the mild-to-moderate side

The bottom line: Don’t be worried about hard landings. Staying disciplined and sticking close to your strategic beliefs can help you better manage this challenging investment landscape.

Introduction

There has been a lot of discussion in the media about whether the U.S. Federal Reserve (Fed) can pull off so-called soft-landing—cooling inflationary pressures without significantly hurting economic growth. With the lagged effects of monetary policy kicking in and signs of weakening emerging in the economy, we think it prudent to revisit some key economic indicators and themes as the U.S. economy makes its likely final approach for this cycle.

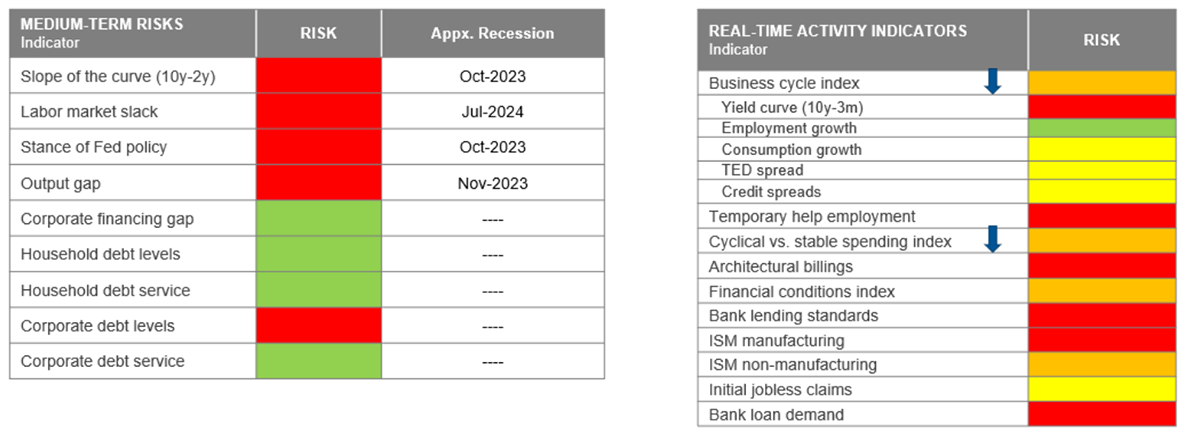

One helpful lens for analyzing the economy is our Economic Indicators Dashboard, which we wrote about in this November 2022 article. The snapshot below shows where the dashboard stands as of May 2, 2023.

Source: Russell Investments, May 2023

In our Q2 2023 Global Market Outlook, we noted that we viewed a recession in the next 12-18 months as being more likely than not. We still hold that view. Although there is a wide range of indicators that can be used to assess recession risk, we believe that our recession dashboard offers a useful window into what might lie ahead.

Source: Russell Investments, May 8, 2023. Down arrows indicate higher risks month-over-month or deteriorating conditions. We apply a color-coding scheme to denote levels of risk. In order from lowest to highest risk: green, yellow, orange, and red.

In this article, we'll outline some of the key themes across our two dashboards and what they might signal.

Theme # 1: The Fed can't rely on an ILS: Uncertainty in the economic outlook

Modern aircraft carry a plethora of onboard navigational instruments that can help with the final approach and landing process. In fact, depending on the aircraft and airport, pilots can potentially use a CAT III Instrument Landing System (ILS) to guide the plane all the way to the runway.

The Federal Reserve unfortunately does not have access to such sophisticated guidance systems. While there are some clues, like the Taylor Rule, that might provide a rough estimate of where interest rates should be set to achieve policy objectives, these calculations come with a high degree of uncertainty.

Many developed market countries have been battling high inflation caused by an overheated economy. Textbook economics would suggest that countries need to raise interest rates to cool down the economy and the inflationary pressures.

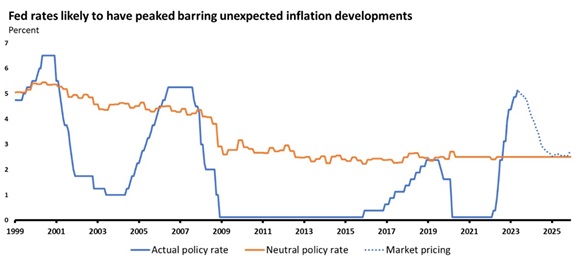

To effectively set monetary policy, policymakers need to know where the neutral rate of interest is –the level of interest rate that theoretically neither aids in economic growth nor restricts it. The Federal Reserve must then take interest rates above this level to cool economic growth.

Unfortunately, this is a theoretical concept that cannot be observed directly. There is no magic elixir. Our best estimate of the neutral rate of interest for the U.S. is approximately 2.5% in nominal terms. With the Fed raising the target interest range to 5% to 5.25% in early May, we believe that the central bank has taken interest rates well above the neutral rate. This significantly restrictive monetary policy creates a high risk to economic growth (hence the red color coding in our recession dashboard), and could very well cause the U.S. economy to tip into a recession.

Source: Refinitiv Eikon and Refinitiv Datastream, May 2023

Since the neutral rate of interest is unobservable, there might be a fair amount of uncertainty around the estimate. While we and the Fed both believe that the neutral rate of interest is around 2.5% at the moment, it’s possible that the actual neutral rate is higher or lower than our estimate.

If the actual neutral rate is closer to 1%, for instance, then interest rates could be even more restrictive than we think. This would increase the probability of recession even more.

On the other hand, if the actual neutral rate is closer to 4%, then the economy may continue to chug along for some time, potentially reducing recession risk in the near term but amplifying the risk of inflation remaining persistent.

The uncertainty is one reason why, although we view a recession as the most likely outcome, we have also built other alternatives into our investment models and forecasts.

Theme #2: The economy is likely in the final approach phase

A plane’s final approach speed is slower than its speed at cruising altitude. Similarly, despite some of the impressive job creation numbers in the U.S. and the fact that the unemployment rate continues to remain below both the non-accelerating inflation rate of unemployment (NAIRU) and the typical unemployment rate, there are still notable signs that economic activity may be weakening.

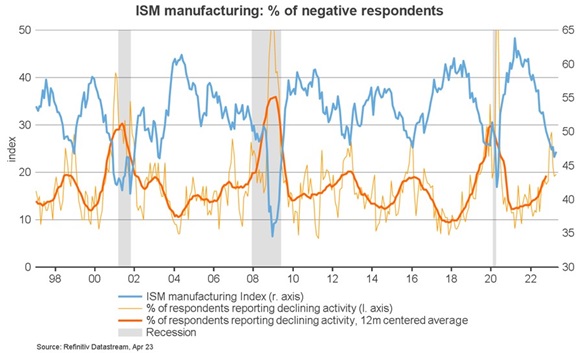

First, let’s take a look at the manufacturing sector. The ISM Manufacturing Index, a gauge of manufacturing activity in the U.S., has remained below 50 for several consecutive months now, suggesting that manufacturing activity is already in contractionary territory. Simultaneously, the percentage of respondents to the ISM Survey reporting declining activity on a 12-month smoothed basis (thick orange line) has been steadily trending upward.

Some economists may argue that the weak ISM merely reflects a transition away from goods spending toward services spending in the aftermath of the pandemic. While this may reduce the strength of the ISM signal, we believe it doesn’t fully mute the signal—and that the ISM remaining in negative territory for such a long time period still points to a slowdown, albeit potentially a smaller slowdown than would otherwise be implied by this signal.

Source: Refinitiv Datastream, April 2023

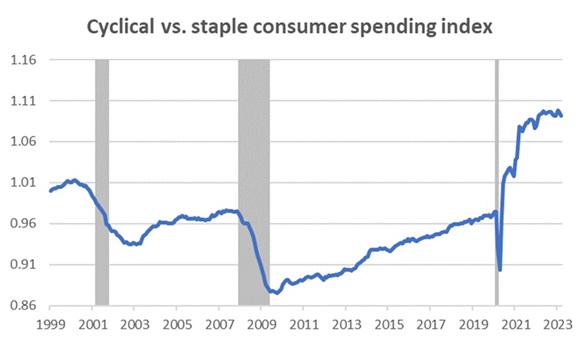

We can also see signs of potential cooling in consumption patterns. Even though consumer spending overall has still been somewhat resilient, the proportion of spending on cyclical categories vs. on staple categories appears to have plateaued. In the face of softening economic conditions, cash-strained consumers tend to cut back on cyclical spending first before cutting back on staple spending. Thus, if this indicator continues its plateau or even begins to dip, it serves as a strong harbinger of a softening in economic activity or even a recession.

Source: Russell Investments calculations based on consumer spending data from Refinitiv Datastream through March 2023.

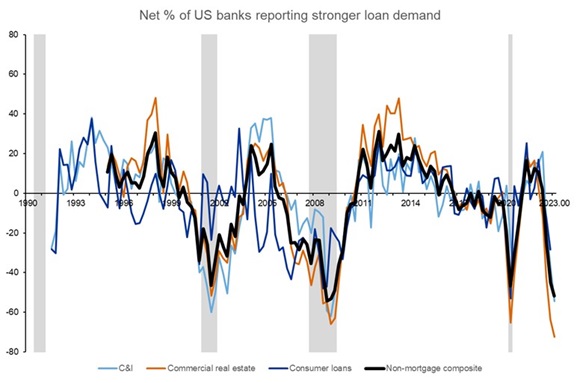

In addition, data from the recently released Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) shows that bank loan demand has fallen precipitously. In fact, our composite index based on SLOOS data shows that the percentage of banks reporting stronger loan demand has now fallen to levels typically seen during recessions. And for the commercial real estate side, loan demand has fallen beneath 2008 low!

Source: Russell Investments calculations based on data from the Federal Reserve Senior Loan Officer Opinion Survey, released May 2023.

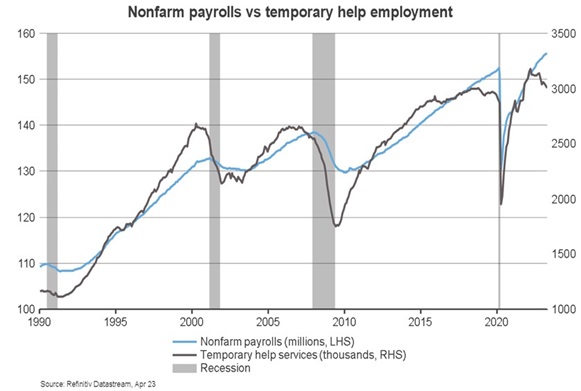

Finally, even though job creation numbers still seem robust, we have already seen a peak in temporary help employment. Generally speaking, it’s easier to let employee contracts lapse instead of cutting permanent employees, and so companies tend to choose this as a first step. But if economic activity continues to soften and corporate profits remain under pressure, then companies may have no choice but to reduce permanent headcount too, which creates a feedback loop that leads to reduced consumer spending, further weakening the economy.

Source: Refinitiv Datastream, April 2023

Theme # 3: Final approaches come in all shapes and sizes

The final approach course varies depending on the airport and runway in use. Some approaches are relatively straightforward—for instance, making a straight-in approach to one of LAX’s four parallel runways. Other times, the approach course can be non-linear: the famous River Visual Approach to Runway 19 at DCA involves a sharp turn at a low altitude.

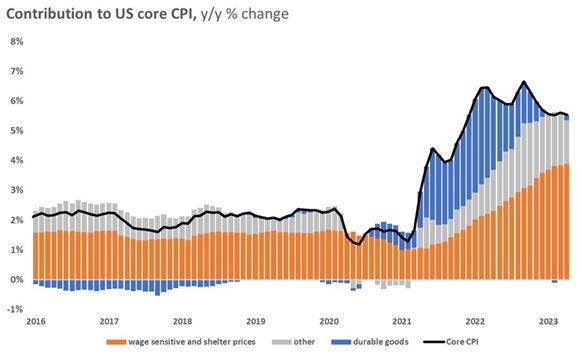

As the U.S. economy makes its final approach to this cycle, we must also recognize that the path will not necessarily be a linear one. Consider, for example, the recent trend in core inflation. While year-over-year CPI and core CPI inflation rates have moderated from their peaks, the path of the deceleration in inflation has not been constant. We have seen some months where the inflation rate actually appears to briefly climb again, before continuing its downward trajectory.

Source: Russell Investments calculations and data from Refinitiv Datastream, April 2023

If the final approach of the economy is often non-linear, the final approach of the equity markets can be even more so. With the S&P 500 hovering above 4,100 as of early May 2023 and with the VIX Index less than 20, it might be tempting to rule out the possibility of a recession. Yet even if gusty winds briefly lift a plane’s altitude, the plane will ultimately descend as it continues its final approach. Equity markets could remain elevated as a result of investor sentiment in the near term, but as economic conditions further deteriorate, markets are likely to trend lower.

Theme #4: Landing on a short runway: The economic risk management tradeoff

Billy Bishop Airport in downtown Toronto has a main runway that’s less than 4,000 feet long and is surrounded by water on both sides. While propeller aircraft can still land safely at the airport, pilots do not have a large margin of safety, especially when the runway is wet. While pilots might enjoy getting compliments about the smoothness of their touchdown, they need to make sure the plane doesn’t go off the end of the runway and may err on the side of a firmer touchdown if needed.

As of early May 2023, market participants have priced in some moderate rate cuts by the Fed toward the end of 2023. We think that Fed officials need to see meaningful evidence that they are making progress toward their inflation-fighting goals before they can start easing off their deeply restrictive stance. The experience of the 1980s has shown the dangers of letting up on inflation too early, and we think the Fed would rather cause a bumpier touchdown (e.g., recession) than risk letting the plane slide uncontrollably and allowing inflation to remain persistently elevated.

On the other hand, there is also a marked difference between permitting the plane to land somewhat firmly versus letting a plane fall uncontrolled to the ground. If a recession ends up materializing and the inflationary pressures dissipate as a result of demand destruction, the Fed will have every incentive to cut rates aggressively to prevent a widespread economic meltdown. The historical record shows that in response to recessions, the Fed typically cuts rates by around 500 basis points (bps), meaning that we could find ourselves near the zero lower bounds again. The timing of those rate cuts (2023 vs. 2024) will depend on when the recession materializes, but we do expect that in a recession, the Fed will be forced to cut rates. For this reason, we think that U.S. Treasuries can serve as an important diversifier in a portfolio.

Theme #5: A good landing is one you can walk from Final thoughts about recession risk

I remember my first time flying into DCA. The winds were gusty, and the pilot touched down in a way that let the entire plane know we landed. It wasn’t fun, but it does happen from time to time. While the word recession may strike fear in those that remember the 2008 financial crisis, we think it’s important to remember that the upcoming recession likely won’t be a repeat of 2008.

As of this writing, consumer and corporate balance sheets in the U.S. still look reasonably healthy. Debt service ratios remain manageable. And even though a significant chunk of consumers’ COVID-era savings have already been depleted, there might still be some excess savings left.

Moreover, regulators have learned the lessons from the 2008 financial crisis. Regulators in several countries adopted the Basel III requirements, forcing banks to set aside more buffers to help them weather economic storms.

These factors should help make the impending recession more on the mild-to-moderate side. Outside of the U.S., higher consumer leverage in some countries (for instance Canada) might make the recession severity more intense compared to the U.S., but once again, we are not expecting a repeat of what happened in 2008.

Even though a recession won’t be painless, we think that investors should avoid panicking. There’s no need to parachute from the plane just because the landing might be bumpy. Investors don’t need to go to an all-cash allocation. In challenging times, we think investors would benefit from staying disciplined and sticking close to their strategic beliefs.

Aviators sometimes joke that “a good landing is one you can walk away from, and a great landing is one where the plane can be reused.” The recession will eventually come to an end, passengers will look around, and realize the plane is still intact despite the bumpiness of the landing. And after they get off the plane to explore the Smithsonian museums, the plane will load up with new passengers, and take off once again.

Disclosures

These views are subject to change at any time based on market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation, or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of the principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits