Bitcoin’s Rise To Prominence On Full Display At This Year’s Miami Conference

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOnce a year, Miami becomes a global mecca for Bitcoin enthusiasts and advocates when the city hosts the titular conference celebrating the largest digital asset by market value. With a $525 billion market cap, Bitcoin is currently the world’s 12th biggest asset, just behind Tesla ($550 billion) and ahead of Visa ($485 billion). As I told the audience during my keynote speech, it’s remarkable that Bitcoin has managed to do this, as it has no CEO, no marketing budget and no board of directors.

Although attendance was down this year compared to last—mostly because Bitcoin’s price is still off its record high of approximately $69,000, set in November 2021—there was nevertheless an impressive turnout of investors of all ages, industry leaders, policymakers and more.

It should tell you something about Bitcoin’s rise to mainstream prominence that this year’s conference boasts not one but two presidential candidates among its speakers (Robert Kennedy Jr. and Vivek Ramaswamy), a former presidential candidate (Tulsi Gabbard), a sitting U.S. senator (Cynthia Lummis of Wyoming) and a sitting U.S. representative (Patrick McHenry of North Carolina).

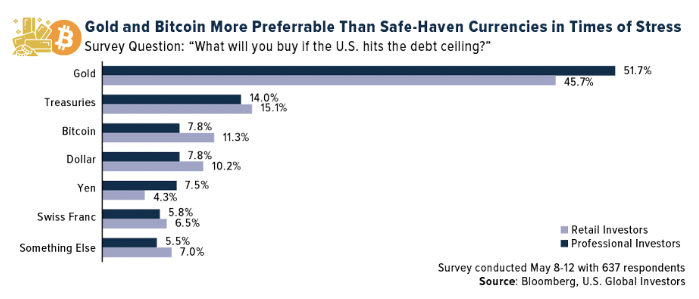

As you might expect, two of the most urgent topics of conversation at Bitcoin 2023 have been the U.S. banking crisis and the looming debt ceiling crisis. In both cases, Bitcoin has been held up as an asset that, like gold, could potentially help individuals and households shield their wealth in the event of a financial or economic meltdown.

But these are Bitcoin evangelists, so of course they would take this position, right? What about more general investors?

Here, too, Bitcoin comes away with very high marks. Bloomberg recently asked close to 640 investors which assets they would prefer if the U.S. hit the debt ceiling and defaulted on its obligations. Bitcoin was the number three asset on the list, with 7.8% of institutional investors and 11.3% of retail investors naming the digital currency. This was enough to put it ahead of traditional safe-haven currencies such as the dollar, Japanese yen and Swiss franc.

Gold Has Had A Much Lower Correlation With The Market Than Bitcoin

Perhaps unsurprisingly, gold topped Bloomberg’s survey list, with over half of institutional investors and nearly half of retail investors favoring the yellow metal in the possible event of a U.S. default. I’ve written many times about the similarities between gold and its digital cousin Bitcoin, the most important one being that they’re decentralized. Unlike fiat currencies, gold and Bitcoin have finite supplies that can’t be tinkered with by a central banker or finance minister, making them attractive diversifiers.

A huge premium that gold has over Bitcoin, as I see it, is its very low correlation with the market. For the five-year period through May 2023, gold and the S&P 500 shared a correlation coefficient of 0.04, meaning the two were almost completely agnostic as to what the other one was doing.

Bitcoin, on the other hand, has traded very much like stocks and other risk-on assets. Over the same period, the digital currency and the market had a very strong positive correlation of 0.88, meaning it often moved in the same direction.

The Mountain Of Debt Continues To Grow With U.S. Households Now Owing $17 Trillion

I believe one of the greatest investment cases for Bitcoin and gold right now is the news that debt continues to expand, not just at the government level but also at the household level. According to the Federal Reserve Bank of New York, the amount of debt owed by U.S. households topped $17 trillion for the first time in the first quarter.

In the chart above, I added the federal funds rate—now in the 5.00% to 5.25% range—to show that higher lending rates have so far had very little effect on Americans’ borrowing habits. Since March 2022, when the Fed tightened for the first time, consumers have added over $860 billion to the total mortgage balance, $145 billion in credit card debt, $93 billion in auto loans and $14 billion in student loans.

Credit card debt was the only measured component that didn’t move much between the end of 2022 and the end of March 2023, but at nearly $1 trillion, it stands at its highest point ever.

Carrying a balance on your credit card is now also the most expensive it’s ever been, with the average interest rate standing at a whopping 20.9% in February.

In short, this is an alarming amount of debt with high interest rates attached to it, at an uncertain time when many people are worrying about a potential recession in the coming months. As I see it, this makes gold and Bitcoin look very attractive as diversifying assets.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.38%. The S&P 500 Stock Index rose 1.65%, while the Nasdaq Composite climbed 3.04%. The Russell 2000 small capitalization index gained 1.89% this week.

- The Hang Seng Composite lost 1.10% this week; while Taiwan was up 4.34% and the KOSPI rose 2.52%.

- The 10-year Treasury bond yield rose 21 basis points to 3.68%.

Airlines And Shipping

Strengths

- The best-performing airline stock for the week was Air France, which increased by 10.6%. Azul estimates that its debt restructuring will result in a reduction of R$5.4 billion in nominal lease payments (R$1.9 billion in 2023 and R$1.2 billion in 2024). According to the agreement, lessors (those who lease the aircraft) and OEMs (original equipment manufacturers) will receive an unsecured tradable note that matures in 2030, amounting to R$2.3 billion with a coupon of 7.5% per year, as well as an equity instrument that can be converted into preferred shares valued at R$36 per share.

- Hapag Lloyd’s Q1 results exceeded the EBITDA consensus by 12%. The main reason for this outperformance compared to the consensus was an 8% higher freight rate. While freight rates were down 24% quarter-over-quarter (q/q), EBITDA was down 38% q/q, which was better than the equivalent figures at Maersk. Unit costs also showed significant improvement, declining by approximately 9% quarter-over-quarter, primarily due to reduced congestion.

- Based on the current scheduling data, the planned capacity for airlines in Q2 is expected to increase by 12% year-over-year (8% for domestic flights and 23% for international flights), compared to a 13% increase in Q1. The preliminary Q3 capacity is scheduled to increase by 14% year-over-year (11% for domestic flights and 21% for international flights).

Weaknesses

- The worst-performing airline stock for the week was Pegasus, which decreased by 2.5%. Virgin Atlantic has postponed its forecast for returning to profitability due to rising costs that hindered its ability to capitalize on the sharp rebound in air travel. The airline, owned by billionaire Sir Richard Branson’s Virgin Group, announced on Wednesday that it now expects to turn a profit in 2024, after previously predicting sustainable profitability in 2023. Chief Financial Officer Oliver Byers attributed the decline in profitability to persistently high inflation and a weaker-than-expected pound. Byers also mentioned that the rapid increase in interest rates, as central bankers sought to control inflation, has further increased the cost of repaying Covid-related debts. Virgin, after being denied access to government funds, was forced to raise over £1 billion from the private sector.

- The shipping industry is moving towards a greener future, but it entails additional costs in the range of hundreds of billions of dollars for carriers, shippers and end users. This assessment comes from UBS in a new report on shipping’s decarbonization, as reported by Danish business media Finans. According to UBS, the shipping industry, which accounts for around 3% of global CO2 emissions, will need to spend up to $300 billion to achieve the transition to green energy by 2050. UBS expects a significant portion of this cost to be borne by customers, resulting in higher freight prices for sustainable transportation.

- Bank of America’s Flight Signals, its proprietary indicator of airline unit revenues six months ahead, fell slightly to -3.4 for Q3 from -3.1 in the previous quarter. With airline capacity changes and revenues now normalizing post-pandemic, this indicator provides insight into the potential trend of unit revenues.

Opportunities

- According to UBS, the capacity of the U.S., Asia and Europe is tracking above the levels of the previous year but still below the levels of 2019. However, the U.S. and China are nearly at 2019 capacity levels, despite international capacity not fully recovering. Brazil has now reached 2019 capacity levels, driven by domestic capacity being higher than in 2019. U.S. domestic capacity remains stable at around 2019 levels, while Chinese domestic capacity is more than 20% higher than in 2019. Italy and Spain have surpassed 2019 levels in terms of domestic capacity. Chinese international capacity continues to increase (less than 40%), while the U.S. is above 80% for international capacity.

- Credit Suisse has reiterated its positive view on tankers for the following reasons: (1) they have the most visible demand catalysts and better resilience against global macro volatilities; (2) they enjoy the most favorable demand-supply dynamics; and (3) their valuations are undemanding. COSCO Energy is their top pick in this sector.

- Delta is reportedly in significant talks with Airbus regarding a wide-body aircraft order. According to Bloomberg, Delta is considering an order for a significant number of wide-body aircraft, including A350 and A330neo twin-aisle jets. Delta already operates both Airbus models, with 63 A330s and 28 A350s. The airline has 33 A330s and A350s on order and has hinted at the possibility of purchasing more A330s.

Threats

- Delta, United and American Airlines continue to operate at reduced levels to China due to Russian airspace restrictions that affect U.S. carriers. In 2019, there were 340 weekly flights between the U.S. and China, but currently, this number has decreased to about two dozen flights. The Russian airspace restrictions do not apply to China, allowing Chinese carriers to operate flights between China and the U.S. using shorter and more fuel-efficient routes over the Russian Arctic.

- USPS (United States Postal Service) is shifting its focus from air cargo to ground transportation and diversifying its carrier mix. As a result, USPS has reduced its spending on FedEx (FDX) services by 11% from FY21 to FY22, and it is expected to continue reducing its spend through FY23. As of February 2023, USPS was the largest customer of FDX’s Express segment. FDX has warned that it expects further volume reductions from USPS in Q4 and 2024, which could have an adverse effect on its results of operations and financial condition. FDX’s contract with USPS is set to expire in September 2024, with no guarantee of renewal on commercially acceptable terms.

- Southwest pilots have voted to authorize a strike. The Southwest Airline Pilots Association (SWAPA) announced that 99% of pilots, with 98% participation, have voted in favor of a strike after more than three years of negotiations. The strike authorization vote is seen as a gauge of sentiment regarding the progress of negotiations. Although the vote was intended to run through the end of May, SWAPA stated that the pilots of Southwest Airlines have already expressed their dissatisfaction with the operational challenges and lack of progress in negotiations over the past three years.

Luxury Goods And International Markets

Strengths

- According to filings released on Monday by Berkshire Hathaway, the company reduced its holdings in Chevron, General Motors, Amazon and Activision Blizzard, among other companies. Warren Buffet opened a new position in Capital One and maintained his position in Apple. Apple remains the largest position in Buffet’s portfolio.

- Richemont, the Swiss luxury giant, achieved record-breaking sales. In the latest quarter ending on March 31, 2023, the company reported an operating profit of €5.031 billion ($5.47 billion), a 34% increase compared to the operating profit of €3.75 billion ($4.08 billion) registered in the first quarter of last year.

- Aston Martin Lagonda Global Holdings, a car maker listed in London, was the best-performing S&P Global Luxury stock in the past five days, gaining 31.0%. Shares gained after Chinese carmaker Zhejiang Geely Holding Group doubled its stake in Aston Martin to 17%.

Weaknesses

- China released softer economic data this week. Industrial production, retail sales and fixed asset investments all fell below Bloomberg’s consensus forecasts. In the United States, retail sales data for April indicated weaker-than-expected consumer spending. The Commerce Department reported a 0.4% increase in retail sales for April, falling short of the estimated 0.8% increase.

- German Economic Sentiment experienced a significant decline, returning to negative territory for the first time since December 2022. The ZEW Survey Expectations Index dropped to -10.7 in May from a positive reading of 4.1 in April. The decline can be attributed in part to expectations of further rate hikes from the European Central Bank (ECB) and more restrictive credit conditions in the coming months.

- Canada Goose Holdings, an apparel, footwear and accessories designer, was the worst-performing S&P Global Luxury stock in the past five days, losing 16.0%. The company reported a revenue beat, but shares sold off on a weaker outlook.

Opportunities

- Overall, luxury companies have been reporting better-than-expected results for the first quarter of this year. The improvement is not only due to the rebound in China’s luxury market but also to faster growth in other regions, including the United States. Bank of America’s Luxury Research Team maintains a positive outlook on the sector as demand started strongly in the beginning of the second quarter. The brokerage firm expects continued strong performance from top-tier names such as Louis Vuitton, Richemont, Hermes and others.

- Global tourism is expected to increase. According to a study by Expedia, Hotels.com and VRBO, 2023 is anticipated to be a year of unconventional travel, a year of travel “like no other.” After years of restrictions, travelers will emerge and take trips whenever they desire. During the summer months of this year, leisure and travel-related companies are likely to outperform.

- The value of the dollar is once again rising. The price of the U.S. Dollar Index increased this week, surpassing the 50-day moving average, suggesting potential further upside for the dollar. A stronger dollar and weaker foreign exchange rates may provide an additional incentive for individuals with dollars to travel abroad, purchasing luxury goods and services in other countries at a lower cost.

Threats

- In China, the unemployment rate for individuals aged 16 to 25 rose to 20.4% in April, reaching the highest level since records began five years ago. China is expecting 11.58 million fresh graduates to enter the job market this year, and if demand for hiring does not pick up, more Chinese youths will be left without work. The overall urban jobless rate dropped 0.1% from last month to 5.2%, while the jobless rate for individuals aged 25 to 59 was 4.2%.

- The U.S. government is once again engaging in discussions about the rising debt ceiling. The deadline to raise it could come as soon as June 1. It is estimated that the United States will run out of money and be unable to pay its bills, including debts to bondholders and various expenses, from national parks to Social Security checks. In 2011, then-President Barack Obama and Republicans in Congress raised the ceiling just two days before the Treasury would have run out of money, which triggered a correction in the stock market.

- Bloomberg Economists are forecasting a weaker Manufacturing Purchasing Managers’ Index (PMI) in the United States. The manufacturing index is expected to decline to the 50-level in the preliminary reading for May, down from 50.2 in April. Manufacturing PMIs for China and the Eurozone are also likely to remain below the 50-mark in May, indicating contraction in the respective economies.

Energy And Natural Resources

Strengths

- The best-performing commodity for the week was natural gas, with a 14.52% increase, The tightening supply conditions for natural gas, driven by a smaller-than-expected increase in U.S. stockpiles and producer cutbacks, as well as optimism surrounding a US debt-deal lifted have boosted both natural gas and oil this week.

- The U.S. is planning to purchase up to 3 million barrels of sour crude oil to replenish its Strategic Petroleum Reserve (SPR), which has reached its lowest level since 1983. This comes after the Energy Department sold over 200 million barrels from the reserve last year to help control high energy prices. The move to refill the reserve aligns with the US government’s strategy to ensure energy security and mitigate the impact of supply disruptions, contributing to the stability of the oil

- The average Brent crude price has reached $75/barrel, prompting the Indian government to remove the windfall tax on crude oil production in its latest review. This is the first time since the inception of windfall taxes in July 2022 that all products are exempt from the tax.

Weaknesses

- The worst-performing commodity for the week was soybean futures, experiencing a 6.10% decrease along with corn and wheat also fell in price. Iron ore prices have dropped from $130/ton in March 2023 to $100/ton, despite China entering its typical peak construction season in the second quarter. The growth in iron ore supply is a key factor contributing to the downward pressure on prices in 2023, with India ramping up production and major players expected to add 30 million tons of supply in 2023.

- Chilean lawmakers approved a bill to increase taxes on copper producers, impacting companies like BHP Group and Anglo American, which could reduce investment attractiveness in Chile’s copper sector. The tax hike introduces potential weaknesses in Chile’s competitiveness as a mining destination, potentially affecting future investments in the industry.

- Copper prices have dropped and are trading near the lowest level of the year due to weak industrial output in China and rising exchange inventories. China’s factory production, retail sales and fixed investment grew at a much slower pace than expected in April, according to official data.

Opportunities

- The global shift towards electric vehicles (EVs) has created a growing demand for battery metals such as lithium, nickel, and graphite. Automakers are actively seeking to secure supplies of these battery minerals, investing in mining projects and forming partnerships with mining companies to ensure a steady supply. The transition to EVs has spurred a collaboration between the auto industry and the mining sector, with car companies playing the role of investors and customers, driving the expansion of mining operations.

- Credit Suisse believes that the long-term bullish outlook for aluminum is supported by China’s commitment to capping capacity at 45 million tons and limiting carbon emissions. They expect aluminum to experience compelling secular demand growth, driven by increased consumer preference for sustainable materials. Aluminum’s recyclability and its leverage in the electric vehicle and energy transition sectors are seen as underappreciated compared to copper.

- SQM, one of the world’s largest lithium producers, anticipates a tight market for lithium as customers restock and new supply is delayed. Optimism grows for a rebound in lithium prices, following a slump from record highs, as demand for lithium in electric vehicle batteries is expected to grow significantly. The restocking period and increasing customer activity suggest a recovery in lithium sales volumes, presenting an opportunity for suppliers to benefit from the rising demand and potentially higher prices.

Threats

- The number of drilling permits issued in April decreased sharply by 31% compared to the previous month. Significant losses were reported in the Permian Basin, Eagle Ford, Powder River Basin and DJ-Niobrara. Bloomberg reports that so-called disposal wells where oil companies have long pumped toxic saltwater back into the ground are unfortunately reaching their capacity limits making it more difficult to drill new wells in the region.

- The resurgence of wildfires in Alberta, Canada’s main energy-producing province, leads to production suspensions and increased risks for oil-sands production. Shifting winds, dry conditions, and the rising number of active wildfires cause unpredictable fire behavior, potentially worsening conditions in the coming days. The impact on oil-sands production poses threats to Alberta’s economy, oil exports, and tax revenues, reminiscent of the significant disruptions experienced during the 2016 wildfires that affected crude production and regional infrastructure.

- The surging demand for air conditioners in countries like India, China, Indonesia, and the Philippines due to rising temperatures contributes to global warming and poses environmental threats. The projected addition of 1 billion air conditioners by the end of the decade and the market nearly doubling by 2040 will have detrimental effects on the climate, especially without phasing out harmful coolants globally. The environmental consequences and potential inequity of access to cooling solutions are major concerns alongside the health and economic benefits provided by air conditioners.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Render, rising 37.72%.

- Litecoin has rallied almost 20% since May 8, when fees on Bitcoin reached a higher of $30 per transaction, compared with a decline in an index of cryptocurrencies writes Bloomberg.

- Hong Kong began testing a digital version of its currency as it joins other regulators exploring its use. Hong Kong, which is also pushing to burnish its image as a fintech hub, is the latest place to experiment with central bank digital currencies (CBDCs) in response to the rise of Bitcoin and other cryptocurrencies, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was XDC, down 4.2%.

- Coinbase has temporarily paused Ether staking reward payouts due to a technical issue. Coinbase says it is working to resolve the issue and adds that all accrued rewards will be paid out, writes Bloomberg.

- Bitcoin fell back below $27,000 with a dearth in market liquidity seen prompting more volatile price swings. Bitcoin declined 3.5% on Thursday in New York trading, according to Bloomberg.

Opportunities

- Coinbase Global was initiated with a recommendation of hold at Berenberg, as analyst Mark Palmer says there’s “too much regulatory risk” for the cryptocurrency trading platform, writes Bloomberg.

- Banks in Zimbabwe may offer loans using the newly released gold-backed digital tokens as collateral. The digital money that the central bank envisages as eventually being used in day-to-day transactions compels lenders to enable a third currency in their systems, writes Bloomberg.

- Bit Digital is expanding its operations to Iceland in a bid to hedge the Bitcoin-mining tax from the Biden administration. The company bought 2,500 new Bitcoin-mining machines for $5 million last week and will house them in Iceland, writes Bloomberg.

Threats

- Red Rock Secured LLC allegedly sold more than $50 million worth of “premium coins” by convincing hundreds of clients to sell existing securities by making misleading or false statements, according to a new lawsuit. The SEC said that Red Rock’s CEO Sean Kelly and two senior account executives, writes Bloomberg.

- FTX Trading sued Sam Bankman-Fried and other former leaders of the bankrupt crypto empire for allegedly using misappropriated funds to buy an “essentially worthless” stock-clearing firm in 2022 for $220 million, writes Bloomberg.

- Investors aren’t likely to see a Bitcoin-spot exchange-traded fund (ETF) offered in the U.S. anytime soon, according to VanEck CEO Jan Van Eck.

Gold Market

This week, gold futures closed at $1,996.60 per ounce, experiencing a decrease of $42.50 or 2.08% compared to the previous week. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.16%. The S&P/TSX Venture Index saw a decrease of 0.82%. The U.S. Trade-Weighted Dollar rose by 0.53%.

Strengths

- The best-performing precious metal for the week was platinum, showing a 0.44% increase. AngloGold is changing its domicile and primary listing location. The new corporate structure will have a primary listing on the NYSE and secondary listings on the Johannesburg Stock Exchange, A2X Markets and the Ghana Stock Exchange. The reasons for this corporate restructuring include enhanced access to global capital markets, improved competitive positioning and a corporate domicile in a leading, low-risk jurisdiction.

- The deal offers 0.4 Newmont shares per Newcrest share, along with a special dividend of $1.10 per share paid to Newcrest shareholders. The total consideration for the acquisition amounts to $19.2 billion, aligning with Newmont’s previous best and final offer announced on April 10.

- K92 reported Q1 financial results that exceeded consensus expectations due to lower operating costs. The company reiterated its guidance, with production weighted towards the second half of the year and targeting the lower end of the range following operational issues in Q1.

Weaknesses

- The worst-performing precious metal for the week was gold, showing a 2.08% decrease. Gold strung together three days of losses before rebounding slightly on Friday. Robust labor market numbers and optimism on a debt ceiling deal weighed on prices most of the week.

- The value of polished stone exports from India, which serves as a proxy for demand, declined by 39% year over year (YoY) and 17% month over month (MoM). Volumes also decreased by 32% YoY and 19% MoM, indicating broadly stable monthly prices but an 11% YoY decrease, possibly influenced by changes in product mix.

- Gold miners continue to face inflationary pressure on labor costs, which account for 47% of their cost structure. Cost guidance for 2023 includes embedded inflation levels of 3-6%. Companies have reported that recent inflation rates are running at 5-6%.

Opportunities

- Wheaton Precious Metals announced a financing package of up to $300 million for Lumina Gold. In return, Wheaton Precious Metals will receive a 6.6% gold stream on the Cangrejos project. The financing commitment will be made through spaced-out cash payments, starting with a $48 million upfront deposit, which will be divided based on transaction and project milestones. The gold stream will reduce to 4.4% after 700,000 ounces have been delivered, and Wheaton Precious Metals will also make ongoing production payments tied to the gold spot price.

- Scotia highlights Kinross Gold’s focus for 2023, which includes further de-risking key assets. This involves delivering on the Tasiast 24,000 mill expansion by mid-2023, conducting a preliminary economic assessment (PEA) at Great Bear in early 2024, de-risking the mine plan at Round Mountain, progressing on the Manh Choh satellite development project and advancing the Curlew pre-feasibility study, expected to be completed in Q2 of 2024.

- Agnico Eagle invested $25 million in Orla Mining at $6.27 per share, increasing its ownership from 10.65% to 11.76%. The agreement includes a “top-up right” that allows Agnico to acquire additional stock if dilution reaches at least 1%. With exercised options and warrants, Agnico Eagle had the opportunity to increase its ownership and can potentially go up to 15%.

Threats

- Automakers are increasingly substituting platinum for palladium in catalytic converters, resulting in a potential deficit in the palladium market for the first time in two years, according to Johnson Matthey. Demand from automakers is expected to exceed 3 million ounces, marking a shift in preference towards platinum and a decline in palladium usage. This poses a significant threat as both metals are used to reduce emissions from car exhausts.

- Centerra Gold faces near-term headwinds that could limit immediate-term upside. These include upcoming elections in Turkey, scheduled to conclude on May 28, uncertainty regarding the timing of the permit for the restart of their Oksut mine in Turkey (as mining permit issuance is typically low during election cycles), and the upcoming VanEck Vectors Junior Gold Miners ETF (GDXJ) rebalance on June 9, which may result in additional selling pressure.

- Scotia suggests that with some signs of relief in inflationary pressures on operating costs, investors should consider rotating from higher-valued streamers (which are less impacted by inflation) to lower-valued operators. The rationale is based on the expectation that operators’ 2023 cost guidance errs on the conservative side, easing inflationary pressures, and projected higher volumes in the second half of 2023, which should help reduce costs.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2023):

Azul SA

AP Moeller-Maersk SA

COSCO Shipping Holdings Co. Ltd.

Delta Air Lines Inc.

Airbus SE

United Airlines Holdings Ltd.

American Airlines Group Inc.

AngloGold Ashanti Ltd.

Newcrest Mining Ltd.

K92 Mining Inc.

Centerra Gold Inc.

Wheaton Precious Metals Corp.

Kinross Gold Corp.

Agnico Eagle Mines Ltd.

Amazon.com Inc.

Apple Inc.

Cie Financiere Richemont SA

LVMH Moet Hennessy Louis Vuitton

Hermes International

Expedia Group Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The ZEW Indicator of Economic Sentiment measures overall expert opinions on the direction of the German economy over the next six months. It is constructed based on a monthly survey of up to 350 analysts, financial professionals, and other experts.

The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All