Value equities have faced years of tough sledding, outside a run of outperformance following “vaccine day” and the lift-off from zero rates. Broadly, this has left value stocks extraordinarily cheap relative to growth.1 However, looking closer, the cheapest 20% of stocks – what we call “deep value” – trades unusually cheap today despite offering surprisingly attractive fundamentals.

We have commented on this phenomenon in the U.S.,2 and we see a similar dislocation in developed ex-U.S. equities. As of May 31, 2023, that group traded near its widest discount to the market over its history (4th percentile dating back to 1983).

We said cheap, not junk...

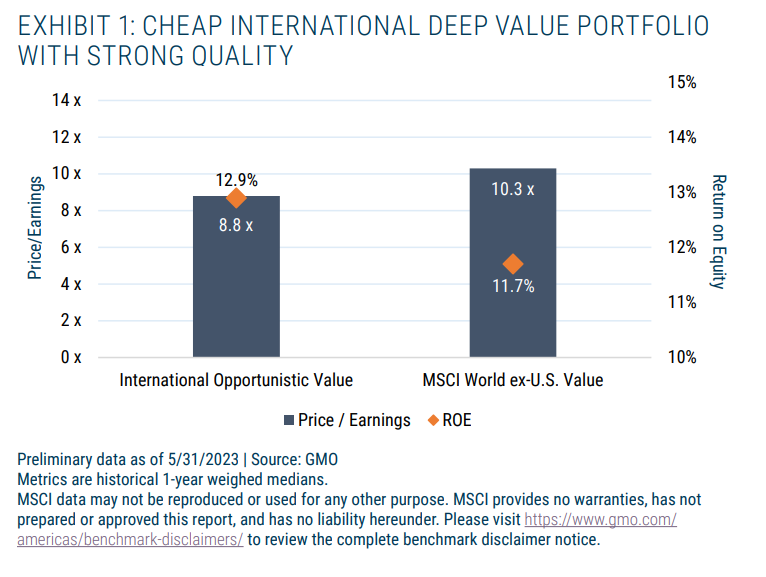

Investors should not rely solely on reported financials and index definitions of value to dial into this compelling opportunity, as we believe doing so could misjudge it. GMO recently launched the International Opportunistic Value Strategy, which uses proprietary valuation models to select a portfolio of international deep value stocks. At the end of May, this portfolio was priced at significant discounts to the market and was also cheap relative to broad value, trading 15-25% cheaper than MSCI World ex-U.S. Value across valuation metrics.

Importantly, leaning cheap does not mean leaning into junk. Our portfolio has higher-quality characteristics than the broad value index, with less leverage (0.6x versus 0.8x debt/equity) and 10% higher ROE. The P/E and ROE measures in Exhibit 1 exemplify how we can build a cheap but relatively high-quality portfolio in international deep value.

...And not a trap

It may be natural for investors to question if this group is cheap for a reason or if it is more prone to recession risk than other equities.3 We do not believe international deep value is a value trap first and foremost because of the quality and profitability of this group today. Its consistently strong fundamentals over time gives us further confidence that the cohort is unlikely to deliver a major fundamental disappointment.

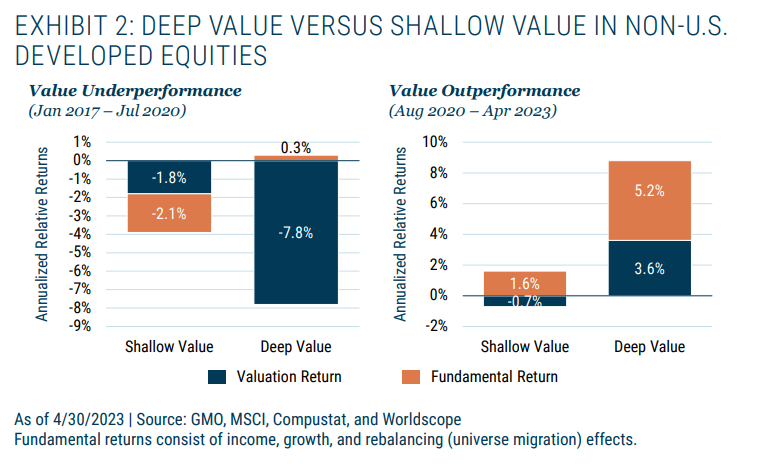

International deep value equities have historically delivered stronger relative fundamental returns than “shallow value” (the remaining 30% of the broad value half of the market) in both good times and bad. To illustrate, in Exhibit 2 we examine two recent periods: value winning (August 2020-April 2023) and value losing (December 2017-July 2020). We decompose the relative performance of international shallow and deep value into returns from valuation (blue) and returns from fundamental drivers (orange). Valuation returns stem from changes in the price investors are willing to pay (i.e., relative multiple expansion or contraction). Fundamental returns are the combination of growth,4 income, and rebalancing (the effect of companies entering and leaving each universe). Deep value companies do “undergrow” shallow value (and of course the market), but they more than make up for it by consistently providing higher income and rebalancing returns.

As the left bars suggest, both flavors of international value struggled in the years before and just after Covid hit. But deep value’s worse relative performance was driven primarily by a valuation return that was meaningfully more negative than shallow value’s (in blue, -7.8% deep value versus -1.8% shallow value), as deep value got to its current historic levels of cheapness. While investors shunned value during this period, they absolutely hated the cheapest cohort.

Was this harsh relative re-rating justified? Hardly. Deep value stocks delivered fundamental returns (in orange) that were in line with the overall market. Meanwhile, shallow value’s fundamental returns underperformed the market by -2.1%, annualized.

On the flip side, when value wins, deep value really wins. Over the past two and a half years, as value outperformed the market (see the bars on the right in Exhibit 2), international deep value trounced shallow value. This was primarily due to much stronger fundamental returns, which were driven by rebalancing, benefiting from the wide spreads back in July 2020.

Deep value has repriced modestly after outperforming the market for the past two-plus years, but spreads remain wide, leaving us with a continued extraordinary opportunity. With top-decile valuation attractiveness versus history and strong fundamentals versus index value, we believe investors should be adding an allocation to underappreciated international deep value equities.

1 As regular readers know, GMO has been pounding the table that value is priced for significant outperformance versus growth, summarized in Value vs. Growth: The Unwind Continues. Our long value/short growth Equity Dislocation Strategy implements this view and has delivered strong returns since we launched it in late 2020.

2 Ben Inker introduced the concept of U.S. deep value in his 3Q 2022 GMO Quarterly Letter, and we revisited the valuation case earlier this year in Memo to the Investment Committee: A Hidden Gem. GMO’s long-only U.S. Opportunistic Value Strategy seeks to profit from this research by actively investing in the most undervalued U.S. stocks.

3 For those hesitant about the timing element of rotating into deep value ahead of a recession, see Ben Inker’s recent piece, Value Does Just Fine in Recessions.

4 This is growth of fundamental measures such as book value, economic book value (a proprietary GMO measure), sales, and gross profits.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

© GMO

Read more commentaries by GMO