Political risks have always been present in emerging debt markets and we’ve long taken them into consideration within our overall country risk process. However, economic and financial sanctions on emerging countries have increasingly become a realm of political risk we need to consider because of their recent proliferation and staggering impact on bond prices. From our perspective, the proliferation is due to a host of reasons, including the rising number of autocracies and dictatorships around the world; geopolitical realignments such as Russia’s declining great power status under Vladimir Putin and China’s rising power; and a tilt toward nationalism in many countries. Regardless of the reasons and although economic sanctions have been around for centuries, recent cases (e.g., Venezuela and Russia) have generated outsized losses for retail and other savers invested in emerging debt mutual funds, in large part because sanctions have been imposed on the secondary trading of bonds, not just the primary issuance. 1 In other words, sanctions have gone wider and deeper into the marketplace.

Estimating the likelihood of sanctions

In considering these new risks, we must address the issue from the vantage point of being a U.S.-based asset manager with funds domiciled in U.S. and European jurisdictions. There is no doubt that this inserts a bias, but it is unavoidable. Our basic methodology is to identify countries that, due to their geopolitical misalignment with the west, behavior, or political orientation, are more or less likely to be subjected to sanctions by the U.S. and Europe.

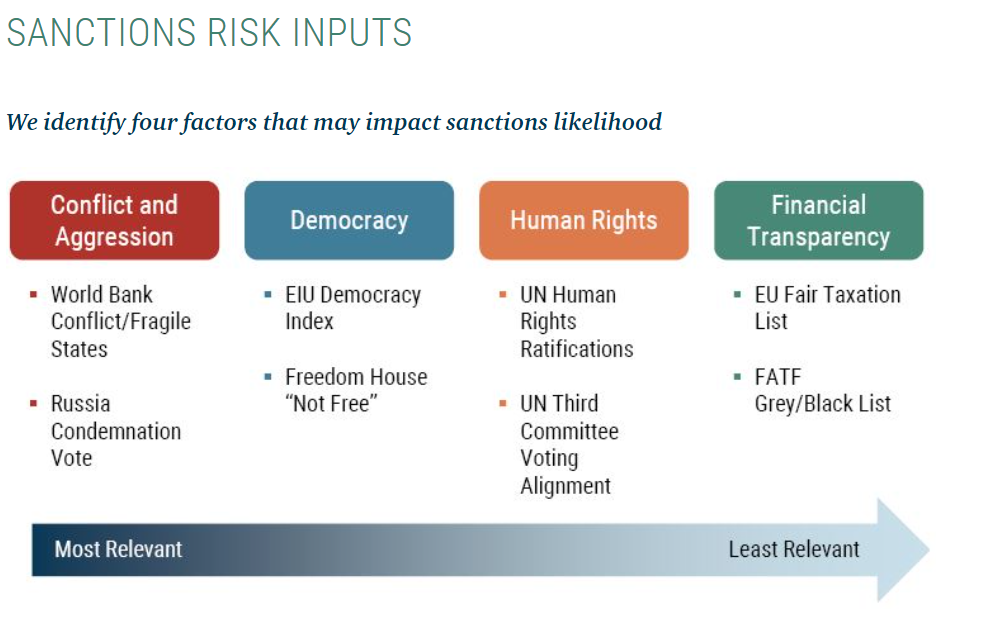

The graphic below identifies four factors of this risk assessment that we believe could have an impact on sanctions likelihood, arranged in the order that we view as most relevant.

Conflict and Aggression – Countries in conflict with neighbors or designated by the World Bank as “fragile states” are more likely to be subject to sanctions, in our view. In addition, given that Russia’s invasion of Ukraine is the most consequential act of aggression in the world today from a geographical and geopolitical perspective, we rate countries on their votes in the U.N. to condemn Russia (whether they vote Yes, No, or Abstain).

Democracy – As we’ve witnessed in recent years, democracies are not perfect. But we believe that the further away a country is from democracy, the more prone their rulers are to geopolitical miscalculations and hence, incurring sanctions. We rate countries in our investment universe on metrics from two independent sources, as seen in the exhibit.

Human Rights – We assume that the weaker a country’s human rights record, the more likely it is to face sanctions. In keeping with our theme of alignment with Western governments, we rate countries on their commitments to basic human rights under U.N. charters as well as their alignment with Western norms.

Financial Transparency – Finally, we consider countries’ adherence to Financial Action Task Force and EU norms on fair taxation and other anti-money laundering and anti-terrorism financing initiatives, commonly referred to as “grey” and “black” lists. This category has the lowest weight in our scoring system, but gives our framework more robustness by veering away from considerations of conflict, democracy, and human rights issues.

After applying a scoring system to the factors above, we segment the 92 countries in our investment universe into three categories of high risk, moderate risk, and low risk of sanctions. Generally speaking, we are likely to seriously limit exposure to high risk countries in our portfolios, subject moderate risk countries to enhanced monitoring vis-à-vis sanctions risk, and worry relatively little about the low risk countries.

Country risk implications

We offer the following observations 2 from our assessment:

1. Based on the underlying data, our model calibration, and our subjective overlay, the number of high risk countries is fairly small (8 countries representing about 5.2% of the EMBI Global Diversified benchmark), moderate risk countries are somewhat more numerous (16 countries representing about 8.7% of the benchmark), and the vast majority of the investment universe, we believe, falls within the low risk group. As of June 2023, our hard currency portfolios were significantly underweight the high risk cohort, and slightly overweight the moderate risk segment.

2. We do not see much correlation between sanctions risk and traditional country risk. In other words, countries across the credit risk spectrum, from investment grade to defaulted, appear in our high and moderate risk categories. We think this should enhance our risk assessment process by offering an uncorrelated risk lens.

3. Countries in the high risk category generally perform poorly on three of the four factors highlighted above, while countries in the moderate risk category may score poorly on two of the four. This helps us frame our analysis and discussions with policymakers, when we have the opportunity. It also becomes part of our ongoing ESG engagement with countries.

4. Due in part to how our risk factors are designed, countries in Russia’s geographic and geopolitical orbit display a higher risk of sanctions (they appear in the high or moderate risk categories). Among the countries in this group are Armenia, Belarus (of course), Uzbekistan, Azerbaijan, Kazakhstan, and Tajikistan. Mr. Putin has wreaked shear havoc on Ukraine, but he has put these countries in the awkward position of having to equivocate on condemning the war, thus leaving themselves somewhat more vulnerable to sanctions, in our view.

5. China appears in our high risk category. We have long argued the possibility that China should not even be considered an emerging country from a sovereign debt perspective, so our portfolios have always been light on China exposure in any case. But we also recognize that from the lens of a fund manager domiciled in the U.S. or E.U., China would naturally score poorly on some of our sanctions risk metrics.

6. Interestingly and perhaps counterintuitively to some, the Gulf countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and U.A.E.) appear in the low risk category. Although all of these countries lag Western norms in the areas of democracy and human rights, they do so moderately, not by extremes. Moreover, they have all voted to condemn Russia’s invasion of Ukraine. Therefore, while sanctions risk in these countries is not zero, we believe it is low.

7. Finally, what about the “good actors”? A number of countries have a perfect score in our model. These countries tend to be in Latin America and the Caribbean, where geopolitical alignment with the U.S. is relatively strong, and emerging Europe, where geopolitical alignment with the E.U. is stronger. This latter group includes many countries in Russia’s near-abroad that have definitively moved in the direction of Europe, such as the Baltic states and Georgia, among others.

As emerging market debt investors, we have long been attuned to the geopolitical risks of the asset class. But the recent proliferation of economic and financial sanctions in the marketplace, particularly those imposed on the secondary trading of bonds, has new implications for mutual fund investors that we believe warrant more careful analysis. At GMO, we have increased our awareness of these risks, and will more directly incorporate them as we manage exposures. Countries with heightened risk of sanctions will face a higher hurdle for inclusion within the portfolios.

1 Sanctions imposed by Western governments (albeit for horrific behavior) are a key reason that several countries have been forced into a default status, including Russia, Belarus, and Venezuela). I wrote about this recently in The Many Faces of Sovereign Default (March 2023).

2 We are happy to share a more detailed list with our clients upon request.

Disclaimer:

The views expressed are the views of Carl Ross through the period ending June 2023, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2023 by GMO LLC. All rights reserved.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© GMO

Read more commentaries by GMO