How The Airline Industry Is Responding To A Potential Pilot Shortage

Membership required

Membership is now required to use this feature. To learn more:

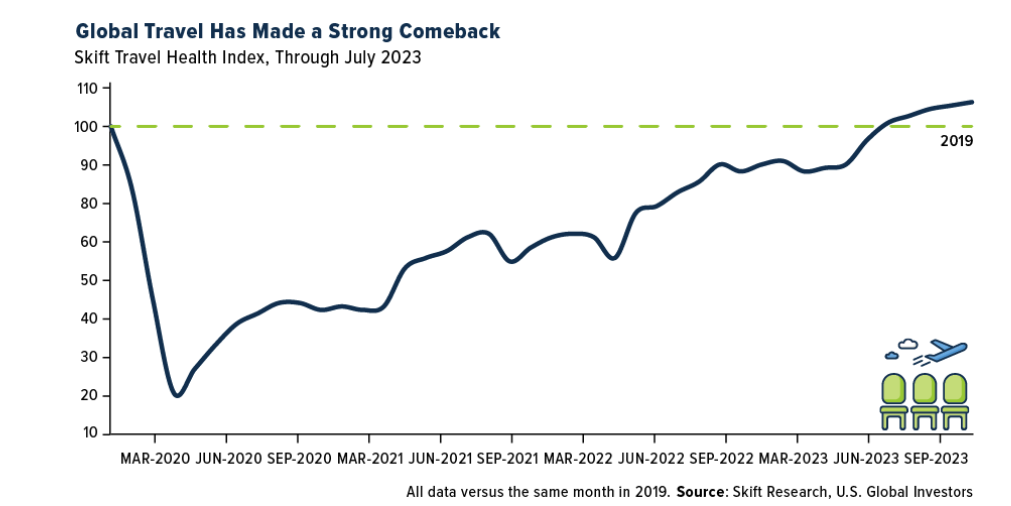

View Membership BenefitsLast month, I shared with you that this summer is expected to mark a new historic high in commercial airline passenger volumes, breaking the previous record set in 2019. One of the unforeseen side effects of the current travel boom has been flight delays, mostly because of staff shortages, and this has raised the issue of pilot retirements.

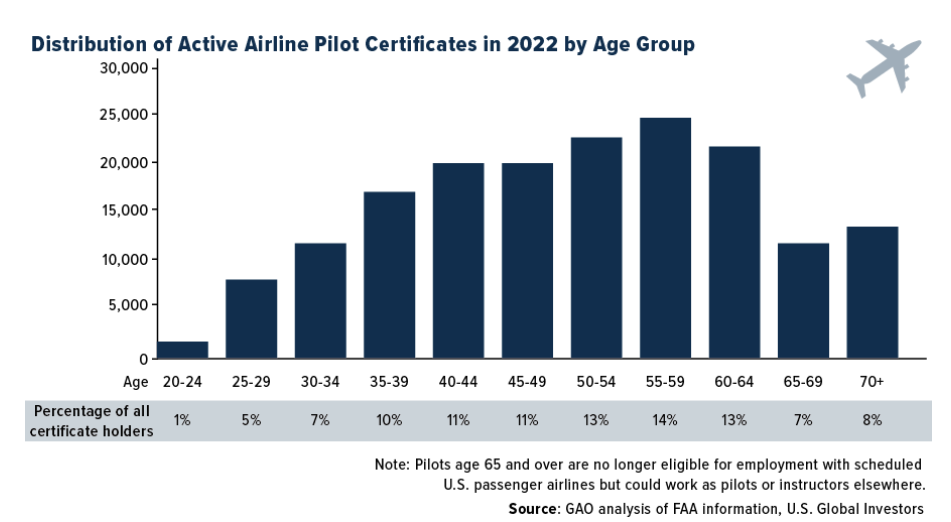

Not too many people are aware that pilots in the U.S. must retire at age 65, due to federal regulations. That may be set to change, however, if a just-passed bill succeeds in becoming law.

On Thursday, in a bipartisan vote, the House of Representatives approved the Federal Aviation Administration (FAA) reauthorization bill, which, among other things, authorizes more than $100 billion for airline operations, equipment and airports over five years. It also (controversially) raises the pilot retirement age from 65 to 67.

The new legislation will now need to be negotiated between the House and the Senate to move forward. If it doesn’t pass by the end of the fiscal year on September 30, when the current FAA law expires, crucial aviation programs could be at risk of being shut down.

I’ve written before about the pilot shortage, arguing that a reasonable supply deficit could actually encourage airlines to demonstrate capacity growth discipline and focus on the most profitable routes. I still support this idea, but others see a potential crisis brewing.

A “Tsunami” Of Pilot Retirements?

Testifying before the House Transportation and Infrastructure Committee in April, Regional Airline Association (RAA) President and CEO Faye Malarkey Black warned of a “coming tsunami of pilot retirements.” The shortage has resulted in more than 500 regional aircraft being grounded, Black said, and a 25% reduction in flights at 308 airports, mostly smaller ones.

Further, the shortage of pilots, particularly captains, is forecast to be exacerbated as approximately 50% of the workforce will retire in the next 15 years.

These headwinds come despite increased enrollments in pilot training schools and rising numbers of pilots since 2017, according to a May report by the Government Accountability Office (GAO). In the same report, though, the GAO discloses that aviation businesses have reported difficulties in maintaining sufficient numbers of mechanics.

How are the airlines weathering these crosswinds? In response to workforce supply concerns, airlines are increasing pay for pilots and mechanics. Some regional airlines made significant pay hikes in 2022. Airlines are creating flight schools, and the FAA is supporting industry workforce development initiatives, including grants to attract young people to aviation careers.

To be fair, not everyone agrees that there’s a pilot shortage. The Air Line Pilots Association (ALPA) suggests that the idea of a pilot shortage isn’t factual and is an attempt to detract from airlines’ mismanagement, particularly in the wake of the pandemic.

The spread between views on the pilot shortage could suggest two different investment implications. If the shortage is real and worsening, it could represent a challenge that airlines must address to ensure operational stability. However, if it’s a narrative spun to distract from mismanagement, as the ALPA suggests, it could raise concerns about the governance and risk management of certain airlines, affecting their investment attractiveness.

American And United Airlines Surpass Expectations Amid The Travel Boom

Amid these swirling winds, we’ve seen an updraft. This week, American Airlines increased its earnings forecast for 2023 in response to the travel boom. The Fort Worth-based airline now predicts earnings of $3.00 to $3.75 per share for the year, potentially higher than Wall Street expectations of $3.10.

In the June quarter, American outperformed expectations, reporting adjusted earnings per share of $1.92 and total revenue of $14.06 billion, against the anticipated $1.59 per share and expected $13.74 billion. Furthermore, the airline reported net income of $1.34 billion, up from $476 million in the same period a year earlier.

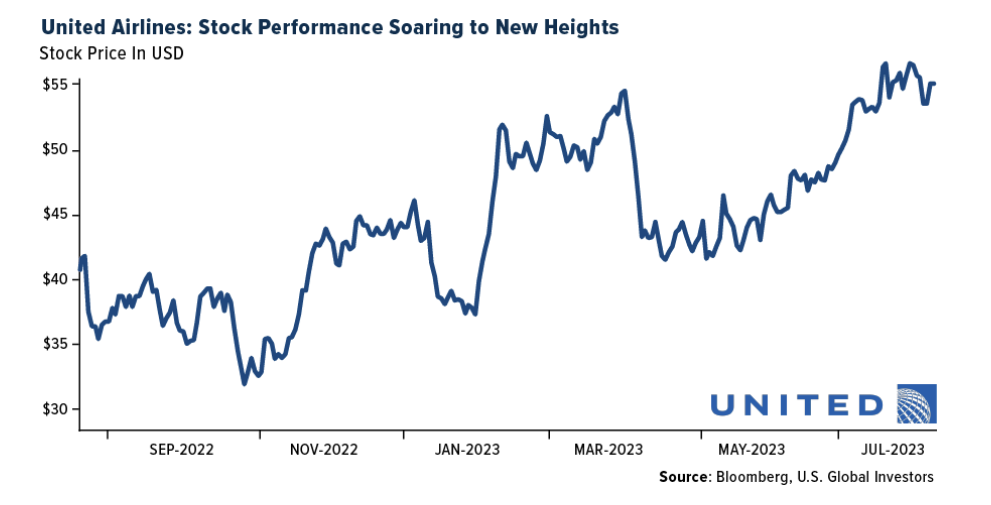

United Airlines also reported record quarterly earnings, surpassing estimates due to a surge in international travel demand. Despite disruptions, the airline managed a strong financial performance, with shares rising more than 1% in Thursday morning trading. In the third quarter, United projects capacity growth of around 16% and an estimated revenue increase of up to 13% compared to the same period in 2022.

Both American Airlines and United Airlines show us that there are opportunities to be had even amid the challenges. They’re also leveraging the ongoing international travel boom, as evidenced by United’s plans to offer direct flights from the U.S. to Manila in the Philippines, starting in October. This expansion into Asia is part of a broader strategy that seeks to leverage the upsurge in international travel bookings after the pandemic slump.

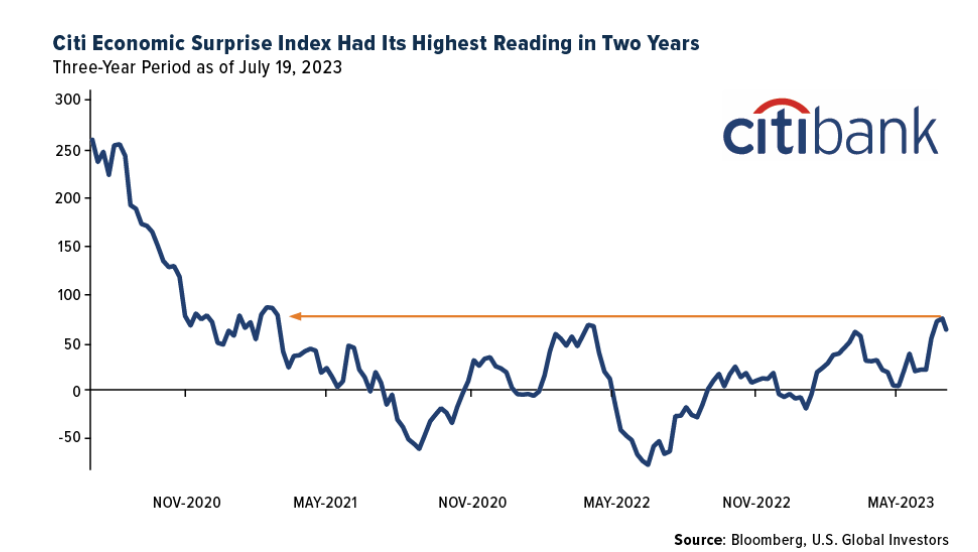

Indeed, recent economic news has been more positive than anticipated, as indicated by the Citi Economic Surprise Index reaching its highest point in the last two years. The index provides a snapshot of how the economy is performing against expectations, with higher numbers signifying better-than-expected results. This uplift has been attributed to favorable recent reports, including decreasing U.S. consumer price inflation, reduced wholesale price increases, lower import prices and fewer-than-expected jobless claims.

A year ago, the same index warned of a potential economic slowdown as the Federal Reserve increased interest rates significantly, while inflation remained persistently high. This led many economists to predict an upcoming recession.

However, they’re now retracting those predictions as economic data continues to exceed expectations.

But for airline investors, I believe this is a landscape of opportunity. Amid the turbulence, there are pockets of clear air. There are legislative tailwinds, innovation in training and recruitment, international expansion strategies, and an overall robust economy that favors travel. As always, remember to keep your portfolios diversified and your eyes on the long-term horizon.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 2.08%. The S&P 500 Stock Index rose 0.77%, while the Nasdaq Composite fell 0.57%. The Russell 2000 small capitalization index gained 1.56% this week.

- The Hang Seng Composite lost 1.73% this week; while Taiwan was down 1.46% and the KOSPI fell 0.71%.

- The 10-year Treasury bond yield was flat at 3.83%.

Airlines And Shipping

Strengths

- The best-performing airline stock for the week was Azul, up 10.1%. Cathay Pacific guided its first half of the year (H123) profit to be in a range of HK$4.0-4.5 billion, of which HK$1.9 billion is related to the one-off, non-cash gain from the deemed disposal of Air China. Adjusted for this, the company’s guidance for the H123 underlying profit would be HK$2.1-2.6 billion, significantly better than the consensus expectation. This guidance reflects a solid passenger demand environment, which translates into higher-than-expected passenger yield and load factor.

- The strike at the Canadian West Coast ports is over after the union and employers agreed to a four-year collective agreement drafted by a federal mediator, according to a joint statement by Ministers O’Regan and Alghabra. RBC’s Digital Intelligence Strategy analyst, Mike Tran, had flagged July 14 as a critical date because, between July 11 and July 13, only three ships were set to arrive at BC ports, followed by an expected 10 more inbounds on July 14 and 15.

- United Airlines' second-quarter adjusted earnings per share (EPS) of $5.03 came comfortably above the $3.50-4.00 mid-April guide and consensus of $4.03. The beat was largely driven by a 17% year-over-year revenue gain.

Weaknesses

- The worst-performing airline stock for the week was American Air, down 3.9%. American Airlines and JetBlue have been ordered by Judge Sorokin to provide clarification by July 19 on their joint/separate positions on the NEA and are due back in court on July 26, (with an injunction set to take place 21 days after the court issues a final judgment). JetBlue announced that starting July 21 its customers will no longer be able to book new codeshare flights on American.

- Year-over-year growth in container ship movements improved throughout the second quarter of 2023, although momentum was increasingly slowing down. Nonetheless, overall second-quarter growth was around 6%, according to UBS Evidence Lab data with growth, once more, skewed toward Asia. In contrast, global container imports decreased by around 1%/3% in April/May, implying continued use of blank sailings to protect freight rates.

- This past weekend was a tough one, operationally, for airlines with sizeable operations in the northeast. All three New York airports experienced cancellation rates in excess of 20% with Boston not far behind at 18%. JetBlue canceled 30% of July 16 flights.

Opportunities

- Spirit Airlines increased September capacity by 23.3% and October by 300 basis points, with both domestic and Latin American flying seeing increases as the airline finalizes its September schedule. New flights added tend to benefit Orlando, with Philadelphia-Orlando, Philadelphia-Charlotte, Phoenix-Baltimore, Phoenix-Chicago, and Atlanta-Miami seeing some of the newest flights.

- According to a Lloyds article “Carriers’ bid to raise transpacific rates mid-July has gained traction, supported by improved capacity utilization levels and a 14% month-on-month reduction in capacity,” said analysts at Linerlytica. “Sentiment has turned positive for a mid-July rate increase, which is supported by high vessel utilization and the bottlenecks around the ILWU Canada strike.” Vespucci Maritime chief executive Lars Jensen attributed some of the gains to the now-resolved strike at Canadian ports.

- United Airlines expects third-quarter revenue to increase 10-13% year-over-year (versus consensus of 10% year-over-year) on capacity up 16%. This expectation results in EPS of $3.85-4.35 (versus consensus of $3.85). United is also seeing an elongated summer peak, with September/October expected to be stronger.

Threats

- Major airlines will often elect to cancel a relatively lower revenue regional partner flight before grounding one of their own. For example, Delta’s 3% cancellation rate (representing 135 flights) was overshadowed by its wholly owned Delta Connection partner Endeavor, which cut 26% of its departures (representing 174 flights).

- Longer-term, the challenge remains too much supply versus normal (or perhaps below-normal) levels of demand. The order book is currently equal to 27.7% of the existing fleet and despite the weaker market and large order book, new orders have continued to come in with over 900,000 TRU of capacity ordered year-to-date, which is about 3.4% of the current fleet. So maybe there is some room for near-term improvement.

- United Airlines reached an agreement in principle (AIP) with Air Line Pilots Association (ALPA). Per the WSJ, the first-year pay increases range from 14-19% with a cumulative increase over the four-year contract of 35-40%. The wage increase appears consistent with expectations. Just as importantly, the AIP is said to include changes to work rules.

Luxury Goods And International Markets

Strengths

- BMW achieved a significant milestone in India by announcing record car sales in the first half of 2023. During this period, the company sold 5,687 units, reflecting a remarkable 5% increase in overall sales compared to the previous year. The success can be attributed to the company’s highest-ever half-year sales, which were driven by impressive record volumes.

- Kering announced that Marco Bizzarri, the CEO of its flagship brand Gucci, will step down in September. Jean-Francois Palus, the current managing director of Kering, will step in and serve as interim CEO. Gucci’s growth has fallen behind that of its counterparts in recent years, forcing Bizzarri’s resignation. The market has reacted well to this news, with shares moving higher.

- Sleep Number Corporation was the best-performing S&P Global Luxury stock in the past five days, gaining 25.71%. Shares started to move higher this week after a Wedbush analyst boosted his price and trading volume highly increased.

Weaknesses

- China reported disappointing year-over-year GDP statistics, with the previous GDP growth rate at 4.5%. The projections were optimistic, expecting a growth rate of 7.1%, but the actual data revealed a lower growth rate of 6.3%. Retail sales, which is a crucial indicator for the health of the luxury industry, were predicted to increase by 3.3% year-over-year, but they only saw a modest rise of 3.1%.

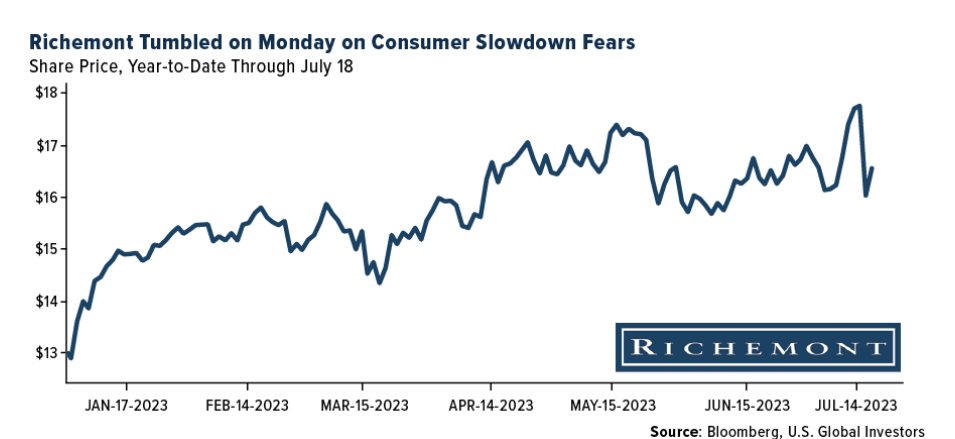

- Richemont shares fell this week after the company reported first-quarter sales that were 2% lower than expected, with the primary shortfall coming from the U.S. market, where revenue at constant currency rates was -2% while expectations were +5%. Revenue in the Asia Pacific region was up, however, with results of +40% achieved versus +39.1% expected.

- Farfetch was the worst-performing S&P Global Luxury stock in the past five days, losing 12.00%. As volumes increased above normal on the past five trading days, the price accelerated.

Opportunities

- Ferrari’s transition to an electric future may raise its average transaction price and supplement its massive €157,000 Ebitda per vehicle. Ferrari is well positioned to withstand the likelihood of an economic slowdown and preserve elite business metrics that back best-in-class risk perspectives, thanks to the potential for better margins, significant market share, and a famous brand.

- Tesla announced over the weekend that its much-anticipated Cybertruck has rolled off the assembly line in Texas. The long-awaited introduction of the futuristic-looking pickup truck comes before Tesla’s second-quarter 2023 earnings call.

- According to Bloomberg’s Mark Gurman, Apple’s first M3-powered Macs might be available as early as October. According to Gurman’s monthly Power On newsletter, an October event will follow Apple’s iPhone 15 series announcement in September, and the present status of Apple’s product range implies it will center on new Macs with M3 CPUs.

Threats

- The absence of VAT-free shopping for overseas tourists in the UK poses a significant threat to the luxury goods sector and businesses in general. The current tourist tax and the elimination of tax-free shopping have made the UK less competitive, negatively impacting retailers, cultural institutions, and overall trade. This threat puts pressure on the government to reconsider the decision and reinstate VAT-free shopping to mitigate the adverse effects on the economy.

- Tesla posted great second-quarter numbers, but the stock fell as Elon Musk warned of further blows to profitability. Musk stated that if interest rates continue to climb, Tesla would have to continue cutting the pricing of its electric automobiles. Last quarter, the automotive gross margin excluding credits fell to 18.1%, the lowest level since the second quarter of 2019.

- The percentage of Americans who say they were denied a loan has risen to its highest level in five years. According to a New York Fed survey, the average likelihood of a credit applicant needing $2,000 within the next month rose to the highest level since February 2021, while the average likelihood of being able to come up with $2,000 fell to the lowest level since February 2022.

Energy And Natural Resources

Strengths

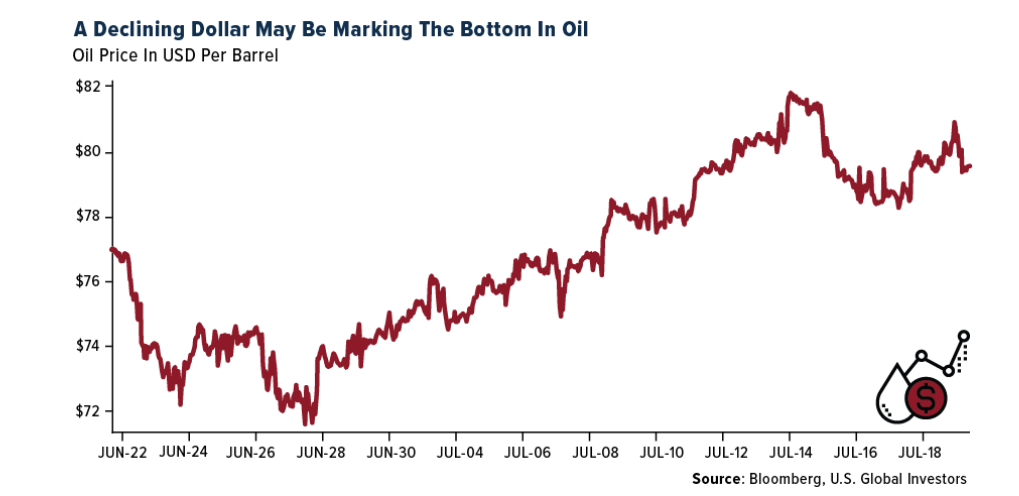

- The best-performing commodity for the week was natural gas, rising 6.81%, as forecasts for persistent heat triggered renewed buying. According to Bank of America, oil is rallying due to the continued weakness of the U.S. dollar. As a U.S. dollar-dominated commodity, the bank believes periodic step changes in the dollar can impact oil markets that otherwise have stronger influences derived from fundamental supply and demand, OPEC intervention, inventory levels, etc. In recent weeks, increased volatility in the dollar around mixed signals from the Fed has seen a rapid deterioration in the currency, which has coincided with a short-term rally in oil prices. In summary, the group suggests that the recent rebound in oil prices is less about oil markets ‘finally tightening’ than it is about other exogenous effects- namely the influence of the dollar.

- China’s CMOC Group will pay Congo’s state-backed miner a $800 million settlement between 2023 and 2028 and at least $1.2 billion in dividends to end a dispute over royalties at one of the world’s biggest copper and cobalt mines.

The disagreement over CMOC’s Tenke Fungurume mine began last July when Congolese mining company Gécamines ordered a halt on exports from the site and claimed the Chinese company had been lying about its mineral reserves and owed $7.6 billion in royalties and interest.

Weaknesses

- The worst-performing commodity for the week was lumber, dropping 5.69%, on the core CPI and housing starts data released on Wednesday. JPMorgan sees supply pressure from a growing share of Russian aluminum in LME warehouses, which made up 80% of total inventories as of the end of June and has grown for five consecutive months as many end-users continue to prefer non-Russia metal. Meanwhile, primary aluminum demand remains subdued, as evidenced by June year-to-date Chinese aluminum product exports falling.

- Coal prices are likely to remain weak for the next few months as stockpiles in Europe and Asia are plentiful and alternatives like natural gas are currently cheap, according to exporter Whitehaven Coal Ltd. Thermal coal is expected to “remain subdued during the Northern Hemisphere summer period,” the Australian miner said in a statement on Monday, as it confirmed its average received price fell 34% in the three months to June 30.

- Carmakers are trying to get some clarity on the new rules from U.S. policymakers around qualifying American-made EVs eligible for the tax credit incentive without the use of any critical minerals that were extracted, processed, or recycled by so-called foreign entities of concern (FEOC), namely Russia and China. Russia is not as much of a concern as China is for the carmakers. Chinese companies play a huge role in the EV supply chain and automakers doubt the 2025 deadline for compliance as it is virtually impossible to produce EV batteries without some Chinese ownership today.

Opportunities

- Exxon Mobil is planning to build a 75,000 to 100,000 metric ton lithium carbonate processing facility not far from Magnolia, Arkansas, which would equate to about 15% of all finished lithium produced globally according to a recent Wall Street Journal report. Tetra Technologies and Standard Lithium are already working on lithium extraction around Magnolia and have plans for lithium carbonate plants too.

- After languishing for months, crude surged above $80 a barrel in London last week as fuel demand in China and elsewhere recovers from the pandemic to reach new highs. That is happening just as production cutbacks by Saudi Arabia and its OPEC+ allies are set to rapidly drain storage tanks around the world.

- Based on Kimberlite’s research, international and offshore drilling markets are expected to experience strong growth in 2024, with over 70% of survey respondents indicating expectations to raise spending in 2024 following several years of underinvestment. Meanwhile, after robust 2021 and 2022 growth in North American (NAM) land, wells drilled are forecasted to creep higher by an estimated 2.3% in 2023 and 2.9% in 2024.

Threats

- Right now, U.S. Strategic Petroleum storage is half empty. It only took about six months for the Biden administration to sell off 180 million barrels from the federal stash in the fastest withdrawal on record. However, refilling it to capacity will

likely take decades, if it happens at all. Experts say that a lack of funding and aging infrastructure will plague the process, even as the Energy Department has pledged to keep buying. - After Texas passed all the record energy costs from 2021 freeze onto consumers to pay for likely several decades, Kansas and now Oklahoma are pushing back on that solution and are considering filing a lawsuit alleging natural gas market manipulation during Winter Storm Uri. If Texas was to join in the suit, it would raise a lot of eyebrows in the state where the petroleum industry is treated as a close partner in the generation of tax revenue for the state.

- Macquarie Group Ltd. notes the nickel market is at a “turning point” as it forecasts a wave of nickel deliveries to the London Metals Exchange will push down prices. New plants in China and Indonesia could add 200,000 tons of nickel. Indonesia typically produced intermediate nickel products like nickel pig iron or ferronickel, but the new plants will be able to up-process those products to nickel metal, capable of being used in batteries for EVs.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Compound, rising 149.63%.

- Coinbase CEO Brian Armstrong will meet with House Democrats behind closed doors on Wednesday morning. Armstrong will speak privately with lawmakers from the New Democrat Coalition about digital-asset legislation and related issues including tax, national security, privacy, and climate, writes Bloomberg.

- A Bitcoin spot-based ETF could bring $30 billion in new demand for the world’s largest digital asset, according to crypto trading firm NYDIG.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Rocket Pool, down 26.20%.

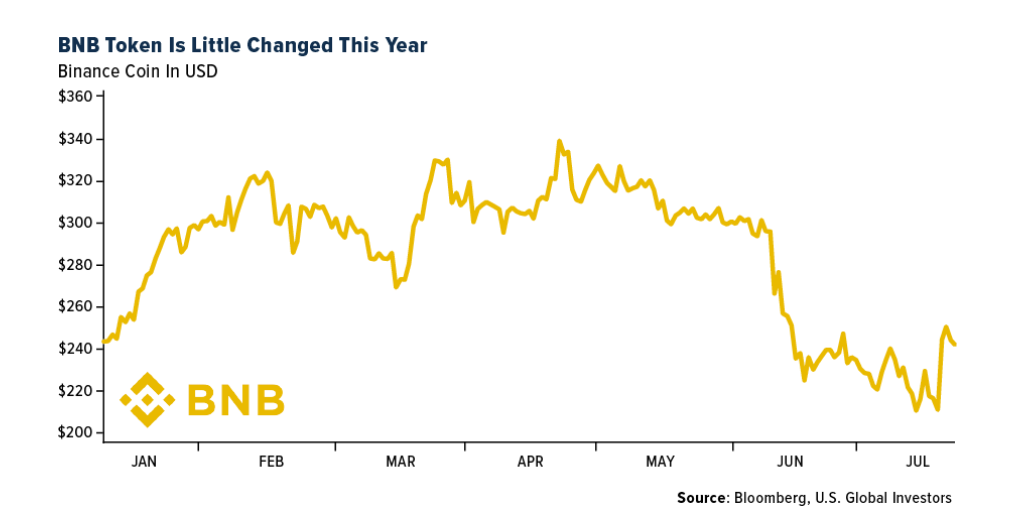

- Crypto traders are turning increasingly bearish on the BNB token that serves as the centerpiece of the embattled Binance digital-asset trading platform. The negative sentiment is most reflected in the perpetual swap market, a type of futures contract used in crypto markets that do not expire, writes Bloomberg.

Opportunities

- Crypto trading platform Bitget plans to expand into the Middle East and hire up to 60 new members of staff. The company said it has already opened an office in downtown Dubai to support the expansion and will explore opportunities in Bahrain and the UEA, writes Bloomberg.

- Elon Musk posted a Scooby-Doo meme this week and in response, Dogecoin added $320 million in just 15 minutes. The cryptocurrency based on the Doge meme quickly jumped in value by 3% after the tweet, writes Bloomberg.

- The aggregate total of active loans in the crypto lending sector has increased to $5.5 billion since the beginning of the year. Aave is the current market leader with about 50% of the market in active loans, writes Bloomberg.

Threats

- A North Korean government-backed hacking group breached U.S. IT management company JumpCloud to use it as a springboard to target an unknown number of cryptocurrency companies, writes Bloomberg.

- SEC chairman Gary Gensler doubled down on his promise to crack down on “the Wild West” cryptocurrency industry. The industry is “rife with fraud, scams, and abuse,” he explained, writes Bloomberg.

- Crypto fund fraudster Eddy Alexandre was sentenced to nine years after pleading guilty to swindling $249 million from investors through his EminiFX cryptocurrency scheme, writes Bloomberg.

Gold Market

This week gold futures closed the week at $2,003.10, up $0.10 per ounce, or 0.00%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.94%. The S&P/TSX Venture Index came in off 1.87%. The U.S. Trade-Weighted Dollar rose 1.16%.

Strengths

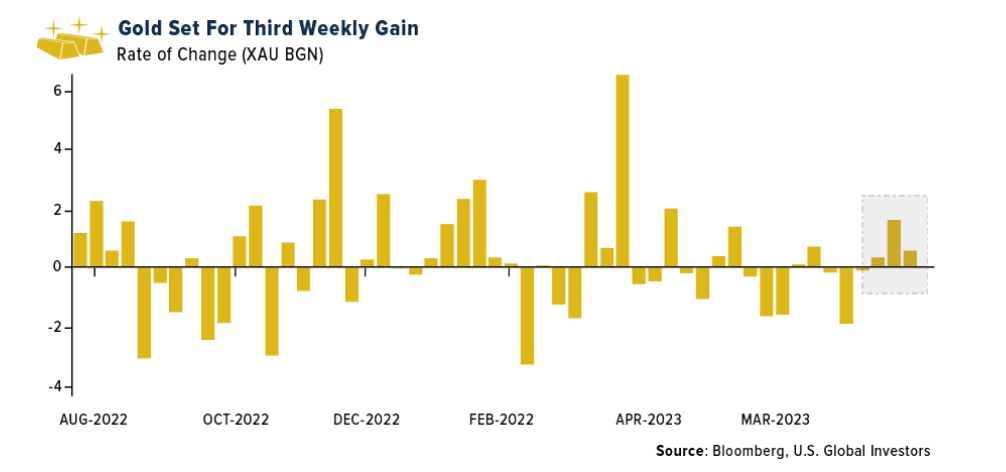

The best-performing precious metal for the week was palladium, up 1.71%. Gold is set to eke a third weekly gain despite going into next week’s likely 25-basis point lift in interest rates. Markets expect the Federal Reserve to pause again on further hikes. Northam Platinum chose to tender its 34.5% stake in Royal Bafokeng Platinum (RBPlat) by finally accepting the mandatory offer from Impala Platinum (Implats), which comprises R90 in cash and 0.30 Implats shares per RBPlat share held. Based on the last closing price for Implats, this implies an offer price of R131/share or R13.1bn for Northam’s stake.

-

- According to Scotia, Q2/23 gold production is expected to be 7% better than Q1/23. They are forecasting group Q2/23 production of 6 million ounces, 7% higher than Q1/23 of 5.6 million ounces but 5% lower than Q2/22. Most companies are guiding for a stronger 2H/23, especially Q4/23, due to grade sequences and fewer maintenance shutdowns.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 1.1.12%. Evolution Mining cut its 2024 gold production forecast to 770,000 ounces, down from 800,000. Sustaining capital was raised by A$10 million but the range for major capital expenditures was broadened to A$320 million to $380 million from A$325 million to A$350. Production for the second quarter was down 2.5% quarter over quarter and missed analyst estimates.

- The value of polished stone exports from India – a proxy for demand – was down 31% YoY (20% MoM), while volumes decreased by 29% YoY (10% MoM), implying aggregate prices declined MoM and YoY, possibly due to a mix change. Polished diamond export volumes and value came in below the 5-year average.

- Anglo American Platinum (Amplats) released a trading statement guiding to a 65-75% decline YoY in its 1H23 headline earnings per share (HEPS) to between R25.44-35.69/share, missing Visible Alpha consensus earnings of R47.42 by 36%. The key driver of the miss could be due to higher than forecast unit costs and therefore the market will likely view this trading statement in a negative light.

Opportunities

- GovMint.com, a coin dealer that is now selling the coins, valued a single gold dollar from the collection at roughly $1,000. With GovMint.com

selling several double eagles in the hoard for more than $100,000, the total

value of the treasure could exceed $1 million. - A Globe and Mail news article quoted a CEO saying many are “definitely looking for opportunities” to acquire producing assets, particularly those that are spun off from big producers undergoing consolidation. This could include some of the struggling Canadian mines that are widely expected by investors to be spun out from Newmont’s (NEM) merger with Newcrest (NCM). Pan American Silver is also asset-rich, post the Yamana transaction.

- The macro driver for future silver demand is being supported by Chinese solar cell production. Bloomberg reported that China’s record-setting solar surge is set to grow even faster than expected this year. Decarbonization and extreme weather are driving the push forward. China has added 74.8 gigawatts of new panels in the first six months of the year which is almost as much as they added in all of 2022. In addition, they lifted their forecast for installations this year to 120 to 140 gigawatts, which was previously 90 to 120 gigawatts.

Threats

- The Organization of Economic Co-operation and Development (OECD) confirmed near-global cooperation to advance its Global Minimum Tax (GMT) framework. A phased introduction of tax changes is planned over 2024-25, which most meaningfully includes the introduction of a 15% minimum tax rate across all jurisdictions. Under the current OECD framework, Franco-Nevada and Wheaton Precious Metals would both be classified as multi-national corporations which operate in lower-taxation jurisdictions. FNV operates its streaming model in Barbados, and WPM in the Cayman Islands, both low-taxation jurisdictions. Under the OECD framework, a minimum 15% tax would now be applicable to these jurisdictions.

- Newmont reported a second-quarter production miss and the share price had its biggest single-day fall in a year. Free cash flow came in at $40 million while analysts’ expectations were $227.5 million. Quarterly production was down 17% from a year earlier. Newmont suffered from a strike at the Penasquito mine in Mexico and weaker-than-expected mine performance at the Akem mine in Ghana and the Cerro Negro mine in Argentina. Newmont is still set to close on its Newcrest Mining Ltd. purchase to cement its place as the largest gold producer in the world but has a mountain of issues to sort through for the rest of this year if they expect to achieve full-year guidance. They are only 44% there to the bottom end of guidance at 5.7Moz to 6.3Moz.

- According to BMO, Lucara Diamond announced an update to its flagship Karowe mine (Botswana) where the company is undertaking the underground expansion project (UGP). Initial production has been delayed until H1/28 from H2/26 and capex has increased by 25%. While they do not anticipate any near-term funding concerns, they expect that the company will need to restructure its debt facilities.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate for every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

American Airlines

JetBlue

Cathay Pacific

United Airlines

Air China

Delta Air Lines

Tesla

Ferrari

Lucid Group

Kering

BMW

Azul SA

Northam Platinum Holdings Ltd.

Impala Platinum Holdings Ltd.

Karora Resources Inc.

Pan American Silver Corp.

Frank-Nevada Corp.

Wheaton Precious Metals Corp.

Lucara Diamond Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on the Stock Exchange of Hong Kong, based on the average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped at 25 percent, and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining of gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is a market capitalization-weighted and, at its inception, includes 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utility sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries, and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Skift Travel Health Index is a real-time measure of the performance of the travel industry in 22 countries. The Index tracks 84 indicators to assess the health of the travel industry in each country.

Citigroup's Economic Surprise Index represents the sum of the difference between official economic results and forecasts. With a sum over 0, its economic performance generally beats market expectations. With a sum below 0, its economic conditions are generally worse than expected.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All