Quarterly Review and Outlook Second Quarter 2023

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMoving Further Down the Financial Cycle Curve

Monetary and fiscal indicators continued to tighten significantly in the second quarter pointing towards a material slowdown in the U.S. economy. Negative money growth, increasing fiscal deficit, rising real interest rates, and central banking guidance of higher short-term interest rates are creating a classic ‘credit crunch.’ This credit crunch comes as the economy progresses further down the current financial cycle, slowing growth and limiting upward pressures on inflation.

Credit Crunch at Hand

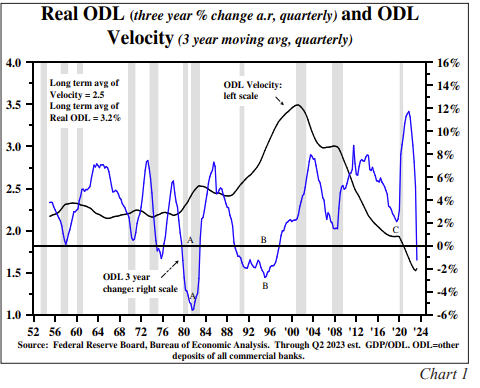

Money Supply and Velocity. Other deposit liabilities (ODL), in real terms, have turned negative for the latest 36 months, while the 12- and 24-month rates of contraction accelerated. The money mountain created in 2020-21, which supported spending and inflation, has been eliminated.

Historically, real ODL has increased at 3.2% per year. Although ODL velocity (ODL-V) rose in 2022, and in the first half of this year, the gain has been insufficient to offset the record contraction in real ODL over the last three years (Chart 1). As the quarterly data indicates, real ODL fell at a 1.2% annual rate over the past three years (the ending point for the blue line in this chart), compared to a 2.3% rate of increase in late 2019 just before the pandemic (‘C’ on Chart 1) and a 3.2% rate of increase since the early 1950s. Over the last three years, ODL-V averaged 1.7 (‘C’ on Chart 1), down from 1.9 when the pandemic hit and a 2.5 mean over the past seven decades.

Historically, it has been important to examine real ODL and ODL-V together as a complete unit. The Volcker Fed broke the inflation spiral that started in the 1960s as ODL-V remained stable (‘A’ on Chart 1). In the 1990s, real ODL went negative (‘B’ on Chart 1), but the economy continued to grow as ODL-V advanced sharply. From the 1950s to the early 1980s, fluctuations in ODL-V were so minor that the relationship between real ODL and nominal GDP was extremely tight. While ODL-V has increased over the past five quarters, the losses for 2020-21 have not been recovered, and ODL-V remains extremely depressed.

Even a stable ODL-V will severely limit the Fed’s capabilities to stimulate economic growth. Monetary policy could be thwarted even more if V’s dominant determinants (the bank loan/deposit ratio and the marginal revenue product of debt) turn down.

From its peak, ODL in nominal dollars fell $1.3 trillion in direct response to the liquidation of $792 billion of the Fed’s securities portfolio of U.S. Treasury notes, bonds and mortgage back securities (‘permanent reserves’). Although reserve requirements were eliminated in the early spring of 2020, the deposit multiplier (m), or ODL divided by permanent reserves, averaged about 2.1, meaning that each $1 reduction in permanent reserves has resulted in an average $2.10 decrease in ODL. All the other determinants of m are still operating to influence its direction, as was the case in the highly indebted economy of 2009-2012.

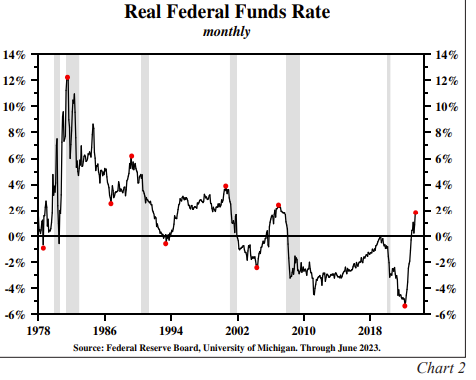

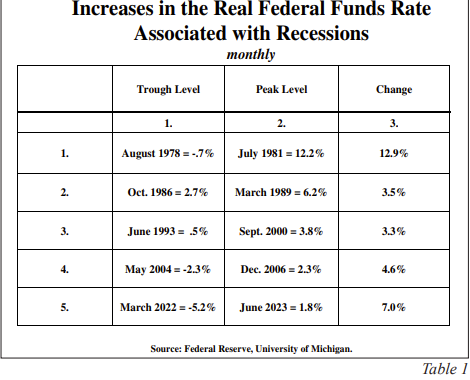

Real Interest Rates. The real Federal funds rate also indicates significant restraint. Using the University of Michigan’s survey of consumer sentiment one-year inflationary expectations as the deflator, the real Fed Funds rate (FFR) troughed and turned higher leading into all of the post-1978 recessions (for purposes of this analysis we treat the two recessions of the early 1980s as one recession). The lead times varied considerably as the initial conditions were different in each cycle. The real FFR reached a record low in March 2022 of negative 5.2%, then rebounded to plus 1.8% in June of this year, an increase of 7 percentage points in fifteen months (Chart 2). This was a larger increase than prior to the Great Financial Crisis (GFC) recession of 2008-09 and the mild recessions of 1990- 91 and 2000-01 (Table 1). The increases in the real FFR were similar for these two mild recessions (lines two and three in Table 1), but the lead times were considerably different. The varied degrees of change suggest that some combination of other monetary variables was present and the initial conditions were quite different.

Real Bank Credit. While money supply and real interest rates reflect a traditional tightening financial cycle, as is the case now, a contraction in real bank credit is unprecedented when real GDP is rising. Money supply leads to bank credit. In previous cycles, real bank credit did not turn negative on a one-year basis until the economy was already in recession. Even in the GFC recession, the 12-month change in real bank credit did not decrease until the end of the recession. In the case of the mild 2000-01 recession, the 12-month change never went negative and there are numerous cases when the 24-month and 36-month changes did not go negative. But the latest 12-, 24- and 36-month rates of change in real bank credit are all negative, respectively, -2.3%, -0.7% and -0.5%. Historically, real bank credit has increased at an average of 3.4% per year. As the second quarter ended, the contraction in bank credit showed the markings of an old-fashioned credit crunch.

Rising Budget Deficits

The U.S. Government budget deficit has taken a serious turn for the worse this year. The Inflation Reduction Act (IRA) and CHIPS and Science Act of 2022, as enacted, add over $1 trillion to the deficit over the next several years. The Penn Wharton Budget Model, however, indicates that due to the way instructions were written, the cost of the IRA is running three times greater than the amount appropriated by Congress. Interest expenses have risen dramatically higher as well. Part of this surge in the budget deficit reflects the fact that the Federal Reserve suffered an operating loss, which adds to the deficit, compared to an operating surplus in FY 2022 which reduced the deficit. Current year federal tax revenues have also fallen considerably below a year ago. This is consistent with real gross domestic income (GDI), which fell in three of the last four quarters. Even after excluding the Fed’s losses, real GDI was negative in three quarters and flat in another. Consequently, the deficit as a percent of GDP for 2023 is likely to be much worse than 5.5% in 2022 and 4.6% in prepandemic 2019. The actual problem is even greater as gross federal debt could continue to increase throughout the current fiscal year. Piper Sandler's policy group preliminarily estimates the FY 2023 deficit could be in the “$1.6 trillion to $1.9 trillion range.”

After taking into consideration the benefits of deficit spending, the lagged negative multiplier effects, and the way in which debt is being financed, the upcoming deficits are likely to have a negligible, if not contractionary, impact on economic growth this year and next. Increased interest payments and a shortfall in tax revenues both add to the deficit, but they do not boost economic activity. Neither produces a new job, a new road, or a new dollar of research and development. More importantly, the lagged effects of the huge budget deficits of FY 2020-21 are likely to be negative due to the government expenditure multiplier.

Estimates from econometric studies of highly indebted industrialized economies indicate that the government expenditure multiplier is positive for the first four to six quarters after the initial deficit financing, then turns negative after three years. This implies that a dollar of debt financed federal expenditures will, ‘at the end of the day,’ reduce private GDP. Ethan Ilzetzki, London School of Economics; Enrique Mendoza, University of Pennsylvania; and Carlos Vegh, University of Maryland found that the multiplier is “sharply negative” in highly indebted industrialized countries (“How Big (Small?) are Fiscal Multipliers?”, Journal of Monetary Economics, March 2013). This study does an excellent job of explaining the requirements for correctly estimating government expenditure multipliers and then develops estimates to meet those requirements.

The initial benefit from the deficits in FY 2020 and FY 2021 was greater than normal because the combined purchases of treasury securities by the Fed, the commercial banks, and the foreign sector directly funded approximately 70% and 100%, respectively, of the deficits in 2020 and 2021. But the 2020-21 process began reversing when the Fed began decreasing their treasury securities in 2022, which in June the FOMC confirmed would continue. When the domestic nonbank sector funds previously or currently issued U.S. debt, then resources are drained from the private sector and shifted from high to negative multiplier usage.

Successfully Time Tested

Two different rigorous studies, one completed in 2011 and the other in 2012, each using different methodologies, both concluded government fiscal policy actions that either increase the size of government relative to GDP or increase the government debt relative to GDP significantly weaken the trend rate of economic growth. The evidence, from more than a decade, since this research was published, confirms those findings and indicates that the government multiplier is becoming increasingly negative.

The passage of time is a spectacular vindication that the methodology of these studies is sound, and that the direct effect of fiscal policy action was properly isolated from the shifting initial conditions, feedback effects (known as endogeneity or the influence of economic activity upon government size/ debt) and movements induced by monetary and other non-fiscal policy actions.

Bergh and Henrekson. Andreas Bergh and Magnus Henrekson (BH), writing in the peer-reviewed Journal of Economic Surveys in 2011, determined that a one percentage point increase in government size reduces the annual growth rate in real per capita GDP by 0.05% to 0.1% per year. Increases in government size mean that more of the economy is being shifted away from the high positive multiplier private sector into the negative multiplier government sector.

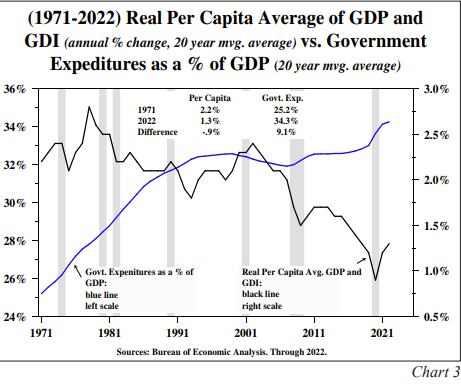

When President Nixon closed the Gold Window, the 20-year moving average of the ratio of government size relative to GDP was 25.2% while the real per capita GDP/GDI average growth rate was 2.2%, which coincided with the average real per capita GDP growth rate since 1870. Based on the comparable numbers in early 2023, government size was considerably higher 34.3%, and the growth in the real per capita GDP/GDI average was a much slower 1.3%. Thus, government size increased by 9.1 percentage points and the real per capita GDP/GDI average growth lost 0.9% per year (Chart 3). Thus, the actual results, twelve years of which were beyond BH’s publication date, means the negative impact on economic performance was within 0.1% of BH’s top-of-range.

Reinhardt, Reinhardt and Rogoff (RRR). The Reinhardt’s (Carmen and Vincent) and Kenneth Rogoff, published in the Journal of Economic Perspectives in 2012, found that when gross government debt exceeds 90% of GDP for more than five years, then economies lose 1/3 of the trend rate of growth. Gross U.S. government debt moved decisively above this 90% threshold ten years ago. As previously stated, the trend rate of growth of real per capita GDP since 1870 is 2.2%. Over the last twenty years, the average growth rate has fallen to 1.3%, a loss of slightly more than 1/3 of the yearly growth rate even though the last twenty years included some years in which the debt ratio was not above 90%. If the U.S. economy were on trend, real per capita GDP would be approximately $73,000, almost $13,000 higher than the actual level. RRR also argued that the deleterious effects of high debt levels would build even before reaching the 90% threshold, and indeed they did. This finding leads to the causal explanation that the overuse of debt reflects the law of diminishing returns.

Final Thoughts

Other major considerations indicate that the U.S. economy is far weaker than recognized. Productivity, or output per hour in the nonfarm sector, declined at a record pace over the past ten quarters. Neither a rising standard of living nor increasing corporate profitability is achievable over time without higher productivity. For the eleven quarters since the pandemic/recession ended, real average hourly earnings (which cover 119 million full-time wage and salaried workers) fell at a 2.9% annual rate. This is the largest decline registered in any economic expansion of comparable length since the earnings series originated. While firms continued to add employees, the rate of increase in wages has lagged behind inflation. Moreover, while establishments have continued to add employees, they have simultaneously reduced the number of hours that their staff are working. Since January, non-farm payrolls have increased by 1.2 million, but the average workweek has dropped from 34.6 hours to 34.4 hours, leaving aggregate hours worked virtually unchanged. To restore productivity, firms will need to rationalize their workforce, which will simultaneously reduce labor costs, inflation, and household purchasing power.

The continued tightening of financial cycle conditions with lower inflation and poor economic performance will mean that long-dated U.S. Treasury yields will continue to trend lower.

DISCLOSURES

Hoisington Investment Management Company (HIMCo) is a federally registered investment adviser located in Austin, Texas, and is not affiliated with any parent company.

The information in this market commentary is intended for financial professionals, institutional investors, and consultants only. Retail investors or the general public should speak with their financial representatives.

Information herein has been obtained from sources believed to be reliable, but HIMCo does not warrant its completeness or accuracy; opinions and estimates constitute our judgment as of this date and are subject to change without notice. This memorandum expresses the views of the authors as of the date indicated and such views are subject to change without notice. HIMCo has no duty or obligation to update the information contained herein. This material is intended as market commentary only and should not be used for any other purposes, including making investment decisions. Certain information contained herein concerning economic data is based on or derived from information provided by independent third-party sources. The charts and graphs provided herein are for illustrative purposes only.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of HIMCo.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All