The Implications Of Fitch Ratings’ U.S. Credit Downgrade

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFitch Ratings sent shockwaves through the financial world this week when it unexpectedly announced a downgrade of the United States’ credit rating from AAA to AA+.

This represents only the second time in U.S. history that a ratings agency has downgraded the country’s debt, the first time being when Standard & Poor’s lowered its rating in response to the government’s handling of the 2011 debt-ceiling crisis.

The rationale for Fitch’s downgrade appears to be much the same. Among the reasons given are the U.S. government’s “repeated [debt] limit standoffs and last-minute resolutions.” The New York City-based agency also cited growing debt fueled by tax cuts and new spending, as well as the rising cost of entitlement programs such as Social Security and Medicare.

(For those keeping score, the combined cost of Social Security and Medicare in June was more than $2.3 trillion, or approximately 9% of U.S. GDP.)

Although the U.S. remains strong with its large, diversified economy and the U.S. dollar’s status as the primary global reserve currency (for now), challenges could lie ahead. Predictions of a mild recession toward the end of 2023 and early 2024, coupled with tightening credit conditions, suggest turbulence may lie ahead.

Repercussions Of The Downgrade

The credit downgrade has already had an impact on Treasuries and stocks, complicating investor sentiment about Treasury debt. Yields pushed higher post-decision, with the 30-year yield exceeding 4.3% on Thursday for the first time since November. (Bond yields rise when prices fall, and vice versa.)

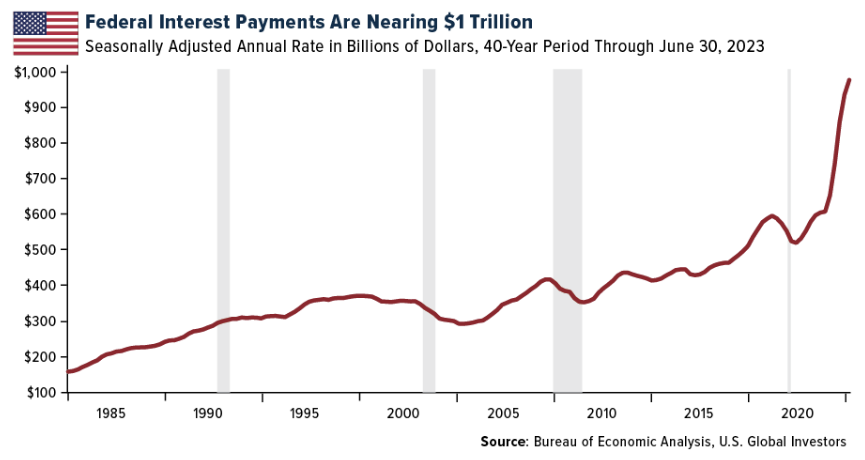

A credit rating downgrade can lead to a number of consequences, perhaps the most obvious being an increase in the country’s borrowing costs due to a perceived greater risk of default. As a result, the U.S. government may end up having to pay more interest on its new debt issues, further deepening its debt burden.

Currently, the government pays nearly $1 trillion in interest alone, or roughly a full third of what it collects in taxes. Meanwhile, the Treasury Department just announced it expects to issue over $1 trillion in new debt in the third quarter.

The downgrade could also lead to currency devaluation if foreign investors opt to sell off their holdings, thereby increasing the supply of the currency in foreign exchange markets.

We may also see short-term volatility in stock markets. When U.S. debt was downgraded in August 2011, the Cboe Volatility Index, or VIX, jumped to as high as 48.3, up significantly from 22.5 at the beginning of the month.

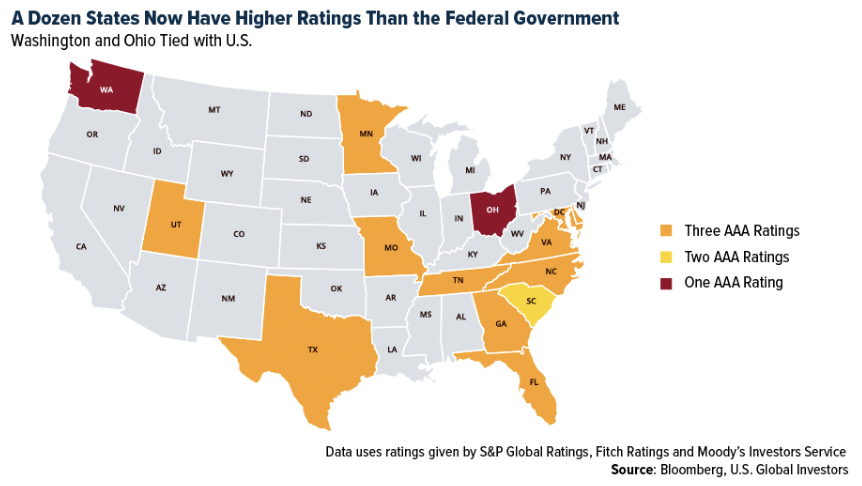

With the federal government downgraded, 12 U.S. states now boast higher credit ratings than the federal government, according to Bloomberg. They include robust, well-managed state economies such as Texas and Florida.

Changing Correlations And Investment Strategies?

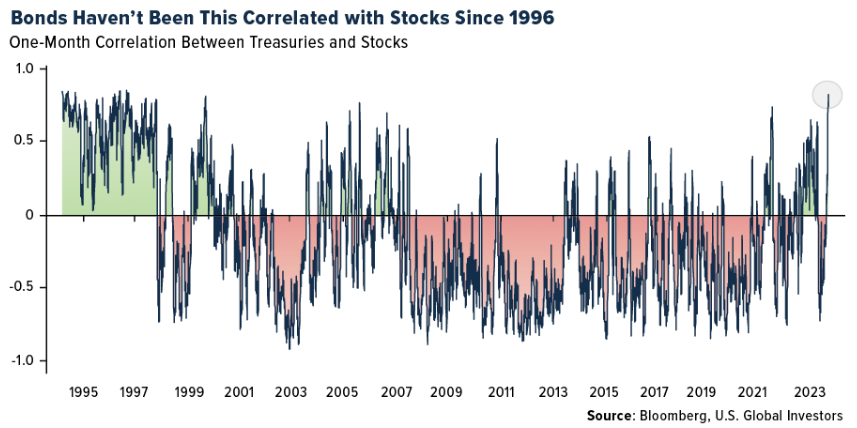

Treasuries have been prized for having a low to negative correlation with stocks, often making them an essential part of a traditional 60/40 portfolio. But in the past month, and especially since Fitch’s decision, government debt has become less effective as a stock hedge, a trend not seen since the 1990s. As you can see below, the correlation between the Bloomberg U.S. Treasury Total Return Index and the S&P 500 has strengthened to 0.82, the highest since 1996, indicating a weaker bonds hedge against equity risks. (A correlation of 1.0 would mean that the two assets consistently move in the same direction on a daily basis.)

These changes have left Treasuries on the verge of wiping out their gains for the year, frustrating those who may have expected a rally following the potential end of the Federal Reserve’s tightening cycle.

With yields heading higher, the equity-risk premium, a measure of the extra reward investors get for holding stocks over bonds, has also dropped to its lowest in two decades. According to the Wall Street Journal, the spread between the earnings yield of the S&P 500 and the 10-year Treasury yield has shrunk to approximately 1 percentage point, the narrowest reading since 2002.

Although low-risk premiums aren’t necessarily indicative of a market downturn, the consensus on Wall Street is that this cannot persist indefinitely. The closer we get to the end of the Fed’s tightening cycle, we should see a decline in bond yields, boosting the appeal of stocks and bond prices.

In the meantime, I believe gold and silver continue to look very attractive as portfolio diversifiers. Gold maintains a slightly negative correlation to the S&P 500, meaning it may move in the opposite direction of the market. As of today, silver has a negligible 0.06 correlation, suggesting it’s currently agnostic to the direction stocks are moving in.

Looking Ahead

Despite the concerns posed by the credit downgrade, there are always opportunities in the market.

Investors should remain vigilant, keep an eye on developing trends and adjust their strategies accordingly. The present situation is a testament to the dynamic nature of financial markets, with changes in credit ratings, correlations and market indicators calling for responsive investment strategies.

This fluidity is the very essence of investing and is what makes the world of finance so intriguing. As always, the key is to stay informed, stay adaptive and stay invested.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.11%. The S&P 500 Stock Index fell 2.27%, while the Nasdaq Composite fell 2.85%. The Russell 2000 small capitalization index lost 1.21% this week.

- The Hang Seng Composite lost 1.62% this week; while Taiwan was down 2.60% and the KOSPI fell 0.21%.

- The 10-year Treasury bond yield rose 8 basis points to 4.038%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Turkish Air, up 5.9%. Most European airlines’ messaging is more upbeat relative to U.S. airlines. IAG flagged no sign of weakness in forward bookings with 30% of fourth quarter booked so far. It has also flagged its more affluent customer base with 65% of British Air customers coming from London/Southeast areas with higher average incomes. easyJet sees summer revenue per seat up 10% year-over-year with the winter ticket yield and booked position ahead year-over-year. Air France commented that it sees no weakening with strong pricing momentum.

- Mitsui OSK reported F3/24 first quarter consolidated RP of ¥90.4bn, beating the ¥60.9bn IFIS consensus. The main divergences from forecasts included upside in dry bulker business, upside in energy business, and a shortfall in containership business.

- Allegiant Air posted a strong earnings beat with second quarter 2023 adjusted EPS of $4.35, well ahead of consensus of $3.62 largely on year-over-year revenue 4 ppts ahead of consensus forecast. Allegiant improved the 2023 EPS guide toward the upper end of the prior range on lower average fuel price and non-op costs. Specifically, the airline EPS was improved from $9.00-13.00 to $10.50-13.00 while reiterating the $1.25 drag from Sunseeker, for a total EPS of $9.25-11.75 versus consensus $9.25/$10.27 estimates.

Weaknesses

- The worst performing airline stock for the week was Sun Country, down 22.1%. Raytheon discovered a manufacturing problem with some of its P&W (GTF) engines delivered between late 2015 and early 2021. Airbus does not expect an impact on ongoing deliveries. This would affect airlines like Spirit/JetBlue that are already impacted by GTF issues.

- FedEx pilots voted down the tentative pilot agreement with a slight, 57% majority. The agreement rejection comes after a tentative agreement was reached in early June and the pilots authorized a strike vote in late May. The company stated the vote will not influence current operations and negotiations will resume under the supervision of the National Mediation Board. The rejected contract called up to a 30% increase in pay over the five-year contract, but pilots voted against the offer because the pay increases were less than pilots had seen at other airlines, and they argue there were weaker job protections in the face of cost cutting initiatives, back pay, and alternative pension options.

- Similar to the demand theme shared by JetBlue and Alaska, Frontier expects margins to be pressured by share shift to international travel (3-point margin headwind) plus a tough operating environment from weather and air traffic control constraints (another 3-point margin headwind). These issues drive second half 2023 pre-tax margins to the mid-single digits from previous guidance of in the double digits.

Opportunities

- Air France-KLM announced that it has entered exclusive discussions with Apollo Global Management regarding the potential financing of €1.5bn to a dedicated operating affiliate of Air France-KLM. This entity will hold the trademark and most of the commercial partner contracts related to Air France and KLM’s joint loyalty program (Flying Blue) and will become the exclusive issuer of miles for the airlines and partners.

- UBS expects ship orders to rebound into a +23% CAGR rally in 2024-26E, driving up share prices. China has outperformed Korea in orders year-to-date. However, UBS is not concerned as Korean yards are managing 2023 orders to one year of sales given limited capacity with backlog at near record 3.3 years as of the first quarter of this year. China’s backlog is up to 2.7 years (optimal 2.0-2.5 years), lowering price competition.

- JPMorgan reiterates its bullish view on Chinese airlines and airports, highlighting the latest developments/datapoints supportive of the investment case: 1) pricing power on the rise – August airfares are trending up, further showcasing robust travel demand during the summer peak season amid tight supply; 2) policy support on the rise – China is pledging to boost consumption, though the market is looking for more concrete measures, while the most recent Politburo meeting called for increasing int’l flights; and 3) tightening fleet capacity – in addition to Chinese airlines’ limited new aircraft orders on hand.

Threats

- JetBlue’s top-line/capacity guidance implies a September quarter unit revenue (“RASM”) decline of 12% year-over-year. This is the largest sequential underperformance that has been reported to date. JetBlue is facing the same pressure as its peers in the domestic network but is also facing headwinds associated with the termination of its Northeast Alliance (“NEA”) with American and outsized exposure to the Northeast region. On the latter, management noted that NYC margins are down high single digits versus 2019 whereas its ex-NYC margins have expanded.

- Pacific Basin faces an unseasonably weaker second half (2H) this year with a 2H23 profit forecast to decline to $55 million. So far, 2H23 rates have been secured at $-3k / $-1k HoH lower so far for handysize and supramax respectively. Easing congestion has caused weaker-than-normal 2H23 spot rates – with handysize rates hitting 2023 year-to-date lows in July. However, management hopes for some seasonal improvement into the fourth quarter with upside from the China stimulus and stabilizing U.S./European macro.

- According to Cowen, data from ARC shows that domestic trips are mostly flat with year-ago levels but are still down versus 2019. Cowen believes the difference is in managed business travel, which is still down year-over-year. Domestic airline ticket prices have been trending lower and are down versus 2019 and 2023, according to ARC data. Revenues are up for airlines because international fares are up versus both last year and versus 2019. Against that backdrop, airlines continue to restore capacity to their networks as they take delivery of new aircraft. The increase in capacity does not seem to be coming with a commensurate increase in traffic or pricing, leading to lower load factors.

Luxury Goods And International Markets

Strengths

- Hermes, the Birkin bag maker, experienced accelerated sales in the second quarter, demonstrating the robustness of demand for its high-end leather goods despite the uncertain economic situation. The group’s sales for the three months ending in June reached 3.32 billion euros ($3.65 billion), up 27.5% at constant exchange rates and surpassing market expectations. Unlike some luxury companies facing similar challenges, Hermes showcased its resilience and strong growth across regions, appealing to wealthier consumers and benefiting from a flight to quality in difficult times.

- Deckers Outdoor, the maker of popular HOKA shoes, reported impressive growth in the first quarter of fiscal 2024, with a 45% increase in earnings and a 10% rise in sales. The HOKA brand stands out with a significant 27.4% surge in net sales, contributing to the company’s strong position in the market. Deckers focuses on direct-to-consumer and international sales, along with improved gross margins and reduced inventory, adding to its promising outlook for the year.

- Shares gained as the company announced the start of the second production phase of the long-awaited car, the FF 91 2.0 Futurist Alliance.

Weaknesses

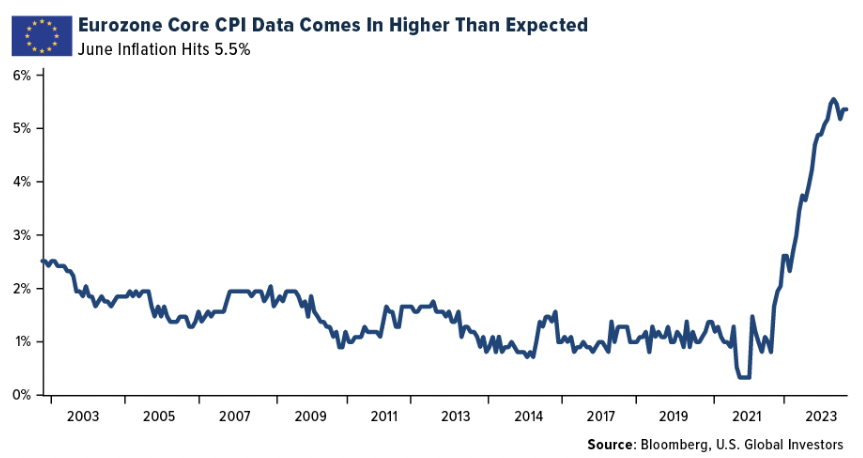

- Global economic conditions are worsening, with Eurozone core inflation (CPI) figures surpassing predictions at 5.5 percent compared to the projected 5.4 percent. In the EU, inflation remains persistent, impacting the cash flow and profitability of companies like Volkswagen, BMW, and Mercedes. In the United States, ISM manufacturing, durable goods orders, and ISM Services PMI all fell below expectations, indicating weaker economic conditions.

- BMW’s shares slumped due to higher expenses for electric vehicle development and supply chain challenges. The company now expects automotive free cash flow of over €6 billion ($6.6 billion) this year, down from €7 billion. Other carmakers are also facing logistics constraints, but BMW slightly raised its full-year earnings forecast with hopes of improved vehicle availability.

Opportunities

- Pernod Ricard, the French distiller, is exploring the introduction of high-end spirits like whiskies, rums, and gins in India. The company has already test-marketed an Indian single malt in Mumbai and Goa and are evaluating other premium categories like top-end rum and tequila, with a focus on mature whisky consumers. Pernod Ricard also plans to export these premium Indian brands to overseas markets with a significant Indian diaspora and aims for double-digit growth in India through strategic investments.

- Porsche Cars North America, Inc., has announced a multi-year agreement with Soho House in the U.S. The partnership will offer unique experiential events to Soho House members across the country, including activations at events like SXSW in Austin and Lollapalooza in Chicago, featuring art installations and workshops. The collaboration aims to elevate the membership experience and bring new luxury brand experiences to Soho House members in a fun and appealing way.

- Carnival Corp. recently sold a $1.31 billion leveraged loan and $500 million in junk bonds to replace expensive Covid-19 era debt, resulting in lower interest costs. The loan, led by JPMorgan Chase & Co., was upsized and priced at a tighter margin and discounted rate due to strong demand from investors. The proceeds from the new loan and bonds will be used to repay part of the company’s existing loan, with plans to further reduce its annual interest expense by redeeming other notes.

Threats

- U.S. regulators are investigating Tesla Inc. over driver complaints related to potential steering control loss in about 280,000 Model 3 sedans and Model Y SUVs. The National Highway Traffic Safety Administration (NHTSA) received 12 complaints, including one crash involving a fire, but no injuries or deaths have been linked to the issue. This probe adds to a series of investigations focusing on Tesla, its products, and its CEO, Elon Musk, which include scrutiny of seat belts, steering wheels, and driver-assistance features.

- Apple Inc. posted its third consecutive quarter of declining sales and expects similar performance in the current period, affected by a broader industry slowdown impacting demand for phones, computers, and tablets. The declining iPhone demand, coupled with foreign exchange headwinds, has contributed to this slowdown, but the company remains optimistic about its services division, driven by over 1 billion paid subscriptions, and hopes to improve iPhone performance in the upcoming quarter with the launch of the iPhone 15 models. However, the overall challenges in the smartphone market and the lack of significant new product releases have put pressure on Apple’s revenue growth and market valuation.

- Ferrari NV’s stock declined as investors were disappointed with the company’s revised guidance, which aligned with analysts’ expectations. The Italian sports-car maker now expects adjusted earnings before interest, taxes, depreciation, and amortization of up to €2.22 billion this year, slightly higher than the previous forecast. While the company’s second-quarter sales and operating profit exceeded analyst estimates, the luxury carmaker, like others in the industry, faces challenges in the supply chain and higher expenses for developing electric vehicles.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was uranium, as proxied by the change in price for the Sprott Physical Uranium Trust, up 7.65%. The move higher came on the back of a policy shift where Ontario announced new plans to expand an existing plant making it the largest in the world, and pledged to add three small modular reactors to a site where one is already built, as reported by Bloomberg. Uranium prices were already trending higher for the past four weeks. A military coup in Niger this past week created concerns over potential for stoppages of uranium exports, as Niger produces 5 million pounds annually and is a key provider to France. According to Reuters/WNA, the military junta reportedly has plans to halt uranium exports.

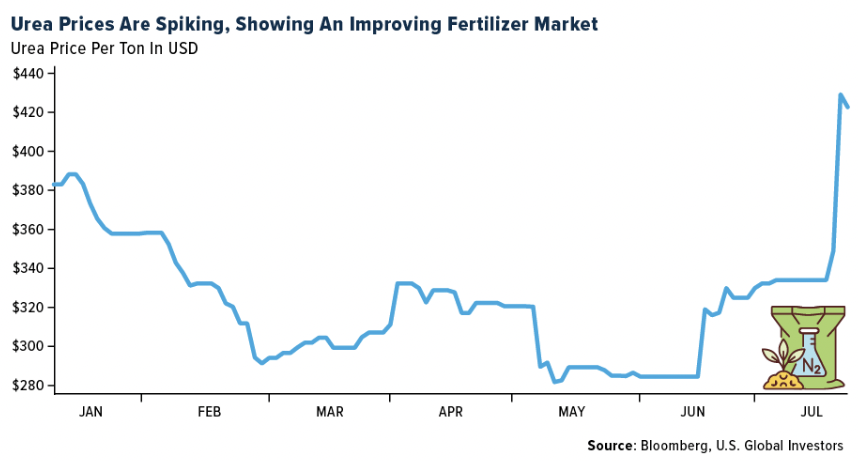

- The fertilizers are rising from growing potash demand and a sizzling summer nitrogen market. Urea has not risen this much in the month of July ever – the NOLA benchmark rose 27% or $80-85 per ton, only the sixth double-digit percentage rise in a July in 20 years (the previous record was 14% in 2009).

- Goldman estimates that global oil demand has risen to an all-time high in July of 102.8 million barrels per day and has revised up 2023 demand by around 550,000 barrels per day. This upgrade mostly reflects firm high-frequency oil demand and GDP estimates in India and the U.S., which more than offsets the slower growing Chinese economy.

Weaknesses

- The worst performing commodity for the week was wheat, dropping 9.83%, on sagging demand for U.S. supplies. Russia, the world’s biggest wheat exporter, is posed to have another bumper crop this year, noting its projections to expand the nation’s output going forward. Since they are blocking Ukrainian wheat exports by sea the Russians can take over this market and directly supply wheat to the countries that previously bought Ukrainian wheat.

- Oil exchange-traded funds (ETFs) posted their largest week of outflows for more than a year, led by a record withdrawal from the crude market’s biggest ETF. Investors pulled almost $200 million in a single day from WisdomTree’s Brent crude oil product, which in January became the biggest in the sector. That is the most since it began trading. There were also withdrawals from other similar instruments, with the United States Oil Fund seeing its biggest weekly outflow since December.

- The dockworker’s strike in Vancouver in early July and an outage of potash handling facilities at Portland’s port, have left loaded railcars sitting on the tracks waiting for their turn to be processed at port facilities. Nutrien Ltd. reported that “there is a meaningful backlog” of inventory and have halted their plans to expand production due to low prices.

Opportunities

- Oil is headed for its largest monthly increase in more than a year on signs the market is tightening, with estimates that crude demand is running at a record clip just as OPEC+ cuts back production. West Texas Intermediate traded slightly higher, above $80 a barrel, touching the highest since April. The U.S. crude benchmark has rallied almost 14% this month, putting it on course for the

biggest advance since January 2022. This is the best performance for July in almost two decades. - Sources familiar with the matter report that Exxon Mobil Corp. is in talks with Tesla Inc., Ford Motor Co., Volkswagen AG, and other automakers about supplying them with lithium as the company is moving forward on its goal of producing 100.000 tons of lithium per year. Exxon has pivoted to include lithium production as part of its future energy plans while the talks were said to be focused on securing buyers. Chevron and Schlumberger Ltd are among a handful of major petroleum companies that have expressed interest in entering the lithium production business.

- Saudi Arabia began its unilateral 1Mb/d voluntary cut in July. It extended it to August and is widely anticipated to extend it into September in the next few days, in line with expectations. Russia and Algeria will also remove 500,000 barrels per day and 20,000 barrels per day, respectively, from the market in August, on top of the existing voluntary cut made since May by some OPEC+ member states.

Threats

- Bloomberg reports that China’s appetite for fuels and other oil-derived products have peaked for this year as much of the buying was to replenish stockpiles while prices were lower. Beijing doesn’t publicly disclose its petroleum stockpiles but Vortexa Ltd. estimates China’s onshore stockpiles have expanded to a record 1.02 billion barrels. The U.S. Strategic Petroleum Reserves currently holds 347 million barrels, and the Biden administration is again delaying a replenishment of the nation’s oil reserves, citing the current price of oil being above $80.

- U.S. steel import volumes jumped 20% on the month in June amid higher shipments of rebar and semi-finished steel products, according to preliminary Commerce Department data. The U.S. imported a total 2.53 million mt of steel in June, marking a 20% increase from May’s final import count of 2.11 million tons, according to the preliminary data. The finished steel import market share was an estimated 23% in June and was estimated at 23% over the first six months of 2023, according to the American Iron and Steel Institute.

- Bank of America expects supply overhangs in 2024 and 2025 for lithium. A weaker fundamental backdrop is already visible in prices, with spodumene, carbonate and hydroxide falling sharply. That said, chemicals prices have partially been held up by elevated spodumene quotations.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was XDC, rising 28.12%.

- The crypto market rebound this year could have room to run if the U.S. economy manages to achieve a soft landing. A scenario of low inflation and steady growth would likely aid risk assets, including crypto, by allowing the Fed to lower real interest rates, according to Zach Pandl, the managing director of research at Grayscale.

- Coinbase Global asked a judge to dismiss a Securities and Exchange Commission lawsuit against it, pointing to a recent decision by another judge who ruled that Ripple Labs XRP was not a security when sold on exchanges. Coinbase filed its motion to dismiss Friday in federal court in Manhattan, arguing the SEC has no authority over its activities, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Compound, down 18.69%.

- GameStop said it’s ending support for its cryptocurrency wallets, citing “regulatory uncertainty.” The company will remove its iOS and Chrom Extension wallets from the market on November 1 according to its website, writes Bloomberg.

- Robinhood’s second-quarter crypto revenue was $31 million, falling 47% from a year ago amid lower trading activity in the cryptocurrency market, according to an article published by Bloomberg.

Opportunities

- The first licenses under Hong Kong’s new crypto regime went to HashKey Exchange and OSL, legalizing the retail trading of tokens in the city as officials seek to foster a global hub for the digital-asset sector, writes Bloomberg.

- Trading volume for President Donald Trump’s Trading NFT cards experienced a staggering 780% increase following his indictment, writes Bloomberg.

- Coinbase shares rose after the cryptocurrency exchange’s second quarter loss narrowed and revenue exceeded estimates, writes Bloomberg.

Threats

- The creator of the crypto token Hex illegally used millions of dollars of investors’ funds to buy a 555-carat black diamond known as “The Enigma,” according to the U.S. SEC. The SEC alleged that Richard Schueler raised more than $1 billion by selling unregistered securities, writes Bloomberg.

- The husband of a social media rapper who dubbed herself the “Crocodile of Wall Street” pleaded guilty to a money-laundering conspiracy tied to the theft of billions of dollars of Bitcoin in the 2016 hack of cryptocurrency exchange Bitfinex, writes Bloomberg.

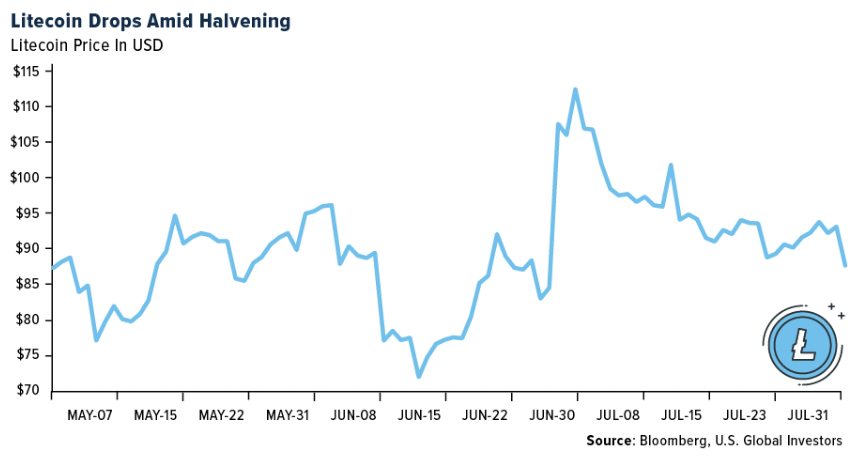

- Litecoin, the world’s 11th-biggest cryptocurrency, saw its price slide on Wednesday after it went through a so-called halvening, with the rewards paid to computers supporting its network dropping in half, reports Bloomberg.

Gold Market

This week gold futures closed the week at $1,977.00, down $22.90 per ounce, or 1.15%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.91%. The S&P/TSX Venture Index came in off 1.50%. The U.S. Trade-Weighted Dollar rose 0.40%.

Strengths

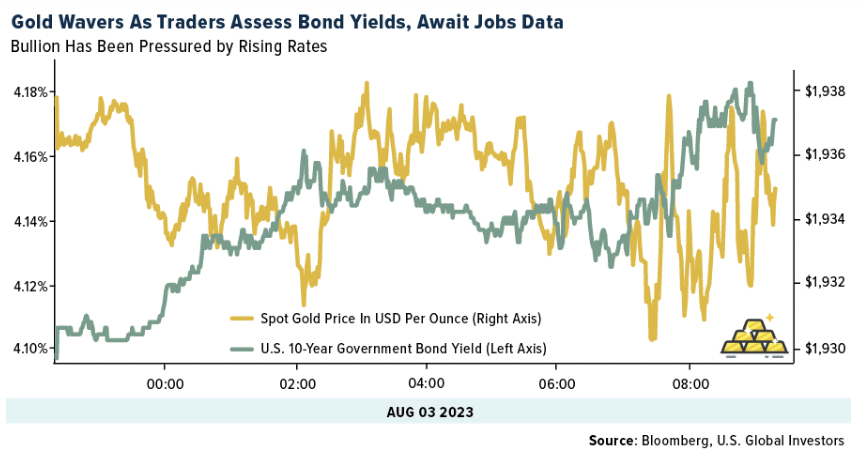

- The best performing precious metal for the week was palladium, up 1.24%, as Nornickel reported that it expects to see a moderated palladium deficit in 2023. Gold edged up as Fitch Ratings’ move to strip the U.S. of its top-tier sovereign credit grade triggered risk-off sentiment, sending global stocks falling. Both European stocks and U.S. equities futures declined, giving the precious metal a boost after its 1.1% drop on Tuesday. The dollar also inched higher, underscoring the greenback and bullion’s status as safe haven assets. Gold finished the next two days with losses but rallied on Friday with the change in nonfarm payrolls coming in lighter than expectations.

- Hochschild Mining has finally received the Environmental permit for the core Inmaculada mine (75% NPV) which will allow the mine to operate for an additional 20 years, removing a key overhang for the stock. The share price closed up nearly 18% on the news.

- Torex Gold reported a second quarter 2023 financial beat. Financial results include second-quarter adjusted EPS of $0.44, a beat versus consensus of $0.37. Quarterly CFPS of $1.07 also beat consensus of $0.84. Annual guidance ranges were maintained, and management indicated that it expects full-year costs to be at the high end of guidance ranges.

Weaknesses

- The worst performing precious metal for the week was silver, down 3.23%, as the historic 3-to-1 move for silver and gold were lockstep this week. AngloGold released a 1H23 trading statement guided to a 48-58% year-over-year decline in headline earnings per share (HEPS) to USc30-37, which is 46-56% below company compiled consensus of 68 cents per share. Management highlighted that HEPS were negatively impacted by a non-cash environmental provision of $38 million net of tax and the effect of continued industry-wide inflation which impacted operating costs by $111 million.

- SilverCrest detailed its updated technical report for its flagship Las Chispas underground mine, located in Sonora state, Mexico, with higher operating and capital costs and lower ounces than expected. The updated technical report envisions 42 million ounces silver and 423,000 ounces gold of production (10% below consensus) driven by silver head grade declining to 396 grams per ton silver due to higher mining dilution from a greater use of bulk mining methods.

- Centerra Gold reported second quarter 2023 EPS of -$0.20, a miss versus -$0.15 consensus, reports Reuters. Against consensus, the EPS miss was driven mainly by lower sales and higher production costs, though production was higher than expected.

Opportunities

- Pan American Silver announced the sale of its MARA, Agua de la Falda, Morococha assets and non-controlling equity interests for total cash consideration of $593 million, plus royalties on MARA and Agua de la Falda. PAAS noted that the divestments will save care and maintenance costs at MARA and Morococha; which represents annual attributable savings of $60 million out of PAAS’ $98-$109 million guidance for 2023, with closing expected to be completed in the third quarter of this year.

- According to Bank of America, the primary knock against Endeavor Mining is the jurisdiction risk (100% West Africa), although investors are primarily concerned about Burkina Faso. Beyond this sale, the company has several ways to further reduce exposure to the country including growth projects outside of Burkina Faso.

- Bloomberg reports that Saudi Arabia has held talks with Barrick about investing in Pakistan, while Barrick’s CEO has commented the company is not in talks to sell a share of its stake in the Reko Diq project in the country. Barrick’s exposure to Reko Diq has historically represented a key investor concern and overhang for shares due to the project’s high geopolitical risk exposure. A potential partnership to advance Reko Diq with a geographically strategic partner like Saudi Arabia, plus confirm its value, could be viewed constructively.

Threats

- Sibanye-Stillwater announced that the Kloof 4 shaft experienced an incident that will negatively impact H2/23 gold production. The Kloof 4 shaft produces 115-120,000 ounces annually, so for 2023 the impact could be around 50,000 ounces (6-7% of total gold production) assuming no further production for the year. The company is currently evaluating the extent of the damage and the production impact. The gold operations accounted for 10% of group EBITDA in the first quarter of this year.

- In a turnaround that has already taken it from one of the world’s biggest gold buyers to a top seller this year, Kazakhstan’s central bank is looking to cut the metal’s

share to as low as half of its $34.5 billion reserves. Alongside its counterparts in Turkey and Uzbekistan, the National Bank of Kazakhstan has emerged among the institutions that have contributed to a second straight quarter of decline in

bullion purchases from central banks, whose buying accounted for nearly a quarter of global gold demand last year. - Gold purchases in India this year are forecast to drop to the lowest since the Covid-19 pandemic hit the second-biggest consuming nation in 2020, with high domestic prices deterring buyers. Indians are expected buy between 650 and 750 tons of the precious metal in 2023, said P.R. Somasundaram, the regional chief executive officer for India at the World Gold Council. The range is lower than the 774 tons bought last year and the least since the 446 tons purchased in 2020, according to the London-based group’s data.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

easyJet PLC

Air France

Mitsui OSK

Airbus SE

JetBlue

FedEx

Alaska Air

Frontier

Hermes

Deckers Outdoor

BMW

Pernod Ricard

Carnival Corp.

Tesla

Exxon Mobil

Hochschild Mining

Torex Gold

AngloGold

Centerra Gold

Pan America Silver

Endeavor Mining

Sibanye Stillwater

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

A bond’s credit quality is determined by private independent rating agencies such as Standard & Poor’s, Moody’s and Fitch. Credit quality designations range from high (AAA to AA) to medium (A to BBB) to low (BB, B, CCC, CC to C).

The VIX Index is a financial benchmark designed to be an up-to-the-minute market estimate of the expected volatility of the S&P 500 Index, and is calculated by using the midpoint of real-time S&P 500 Index option bid/ask quotes.

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

A message from Advisor Perspectives and VettaFi: Advisors who don’t grasp the implications of artificial intelligence (AI) risk being left behind. Join VettaFi for an AI Symposium on August 30th at 11 am ET and hear from thought leaders and experts about how AI will transform the way investing works. Register here!

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All