Investing in a Changing World: From Carburetors to Compilers

Membership required

Membership is now required to use this feature. To learn more:

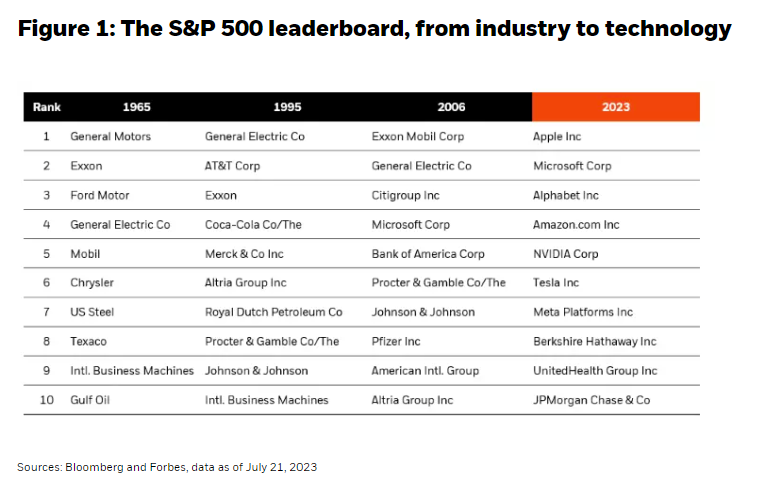

View Membership BenefitsFor the better part of the last century, the largest companies in the world were those that produced physical property – traditional transportation machines, the energy that powered them, or the capital that financed them. If someone born in the post-war Baby Boom were to have glanced at the largest companies in the S&P 500 just once a decade, they would have found familiar industrial names on that list from the 1950s through the early 2000s, but that person would find a completely unfamiliar list today. In just the last decade, the S&P 500 leaderboard has changed dramatically. Today, it is dominated by technology (see Figure 1).

Nonetheless, the reshuffling of the S&P 500 leaderboard can seem glacial in comparison to the pace of economic data and market price changes in a one-day-option world. It is not always easy investing around themes that play out over the course of years or decades, even if they can greatly enhance portfolio construction and create the potential for long-term success.

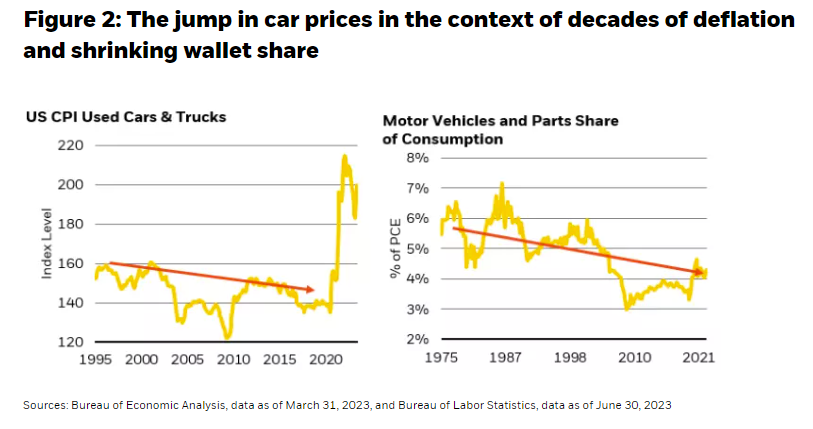

While each economic report is important to the markets in the near term, obsessing over incremental fluctuations in data risks missing the underlying structural context surrounding that data. Used car prices are one item in the consumption basket that has seized the spotlight in recent months for their outsized impact on inflation readings. Yet, even amidst a scary-looking spike in the used car CPI, following 30 years of deflation, the share of consumers’ wallets that is being spent on cars is only about 4%, down from about 6% in the 1970s and 80s (see Figure 2).

It doesn’t make sense to think about a compiler economy in the context of a carburetor

Taking a step back, the 100-year history of the carburetor began in 1893 and peaked in the 1970s, just before automobile prices went into decades of deflation, when the car was the dominant influence in suburban American life (General Motors was the largest company in the world through the ’50s and ’60s), and when the semiconductor industry was still in its infancy. The last carbureted engine was sold in the early ’90s, the technology having been replaced by fuel injection at that stage; just as the dot-com bubble was about to take off, which set the stage for technology industry companies to eventually usurp heavy industry by market capitalization in the S&P 500.

Nonetheless, we are all too often guilty of thinking about the world in the context of a carburetor – a physical, tangible good that once governed the intake of air and fuel into an engine, even when the global economic context is increasingly oriented around something more like a compiler – intangible lines of code that govern the communication between humans and machines (think artificial intelligence and machine learning). Autos themselves have moved from an expensive, commodity-powered, hard-asset mode of transport to a software-driven, services-delivering, efficiently communicating mobile office (some even replete with autonomous-driving features), all of which are geared toward improving one’s quality of life.

The economic data that gets collected, studied, and used to analyze the economy, has evolved much less quickly than the automobile industry, and in some cases seems to have gotten stuck in a carburetor world instead of adapting to a compiler world. The national accounts tend to view the U.S. economy through the lens of a factory, which made sense from the 1950s to the 90s. However, the goods sector’s share of consumption has almost halved over the last century, from just under 60% to just over 30% (in favor of much greater services sector consumption), while corporate investment, which used to be almost entirely made up of capital expenditures (capex), is now split almost in half between capex and research and development (or R&D – often to build out intangible IP).

Office desks that used to be chock full of staplers, calculators, fax machines, thesauruses and Rolodexes would be lucky to have more than a charging port and a widescreen monitor (or two or three) today. While we are not calling for a dismissal of economic data or methods from the post-war era, as they do contain useful information (their breadth and methodological complexity are unrivaled, and they are consistent to a fault), does it still make sense to place as much emphasis as the media and markets do on manufacturing or 1-year inflation surveys with sample sizes of as few as 12 people per state? It is easy for someone answering an inflation survey to compare the cost of a record in the 1980s to the price of an iTunes subscription today, but much harder to assess the quality-of-life impact considering even the largest mixtape collection in the world is a drop in the bucket compared to a cloud-based music library.

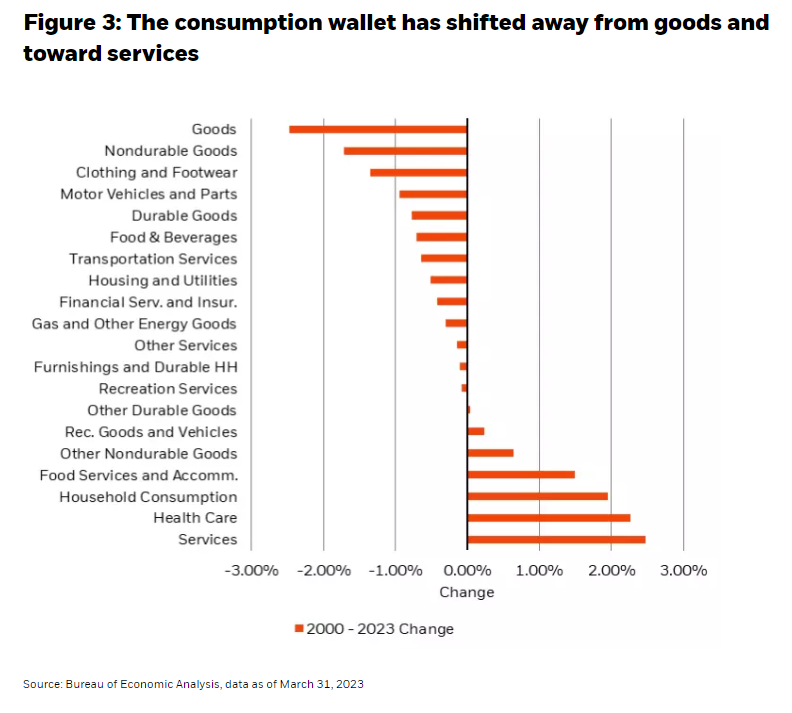

The very nature of consumption has shifted, ever so gradually, but clearly observable over years or decades, to the tune of trillions of dollars annually. Consumption dollars can afford to be channeled toward services, which often reflect a quality of life that goes beyond necessities, to some extent because goods are much cheaper than they used to be relative to net disposable income (see Figure 3).

In the U.S., this shift to services has created two unique effects that would seem out of place in a goods-centric world. First, a services consumption economy is a lot less volatile than a capital-intensive, debt-financed, physical goods-based economy. It is possible that outside of large idiosyncratic shocks like the Global Financial Crisis and the Covid Pandemic, the U.S. economy has left the typical investment-led boom-bust cycles of the 1950s to early 2000s behind. Indeed, the former two shocks are the only ones that managed to visibly depress the upward trajectory of nominal GDP since 1990.

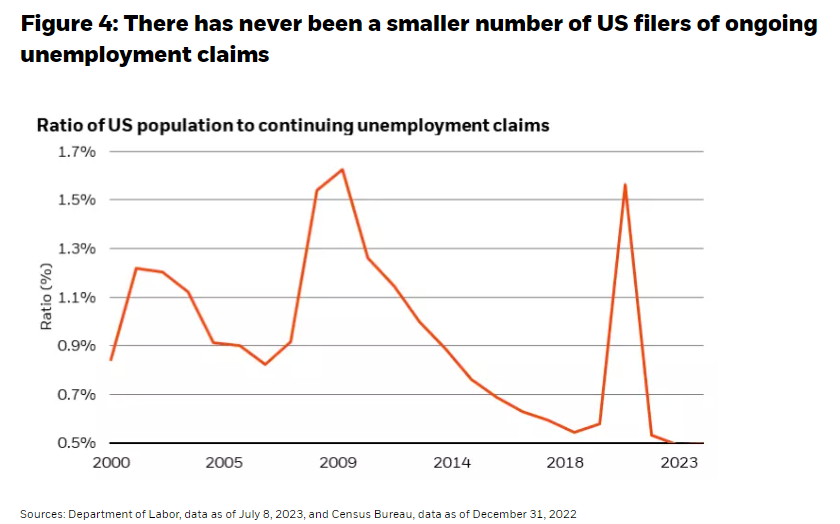

Second, a service-heavy economy is a labor-intensive one, creating a persistent need for workers. This relentless demand for labor is playing out in healthcare, education, restaurants, hotels, air travel and other service sectors. Even with strong working-age participation, the U.S. economy has a deficit of roughly 3 million jobs, as measured by payroll employment, commensurately leaving the smallest proportion on record of Americans filing ongoing unemployment claims (at about 0.5%, see Figure 4). Most of this labor deficit exists in sectors that are relatively insensitive to interest rate increases (people rarely look at the interest rate before a night on the town or a vacation). And because of this demand for workers, the lowest wage earners are enjoying the highest wage growth of any cohort, a dynamic we have long felt policymakers should look to preserve.

All this isn’t to say that the U.S. economy is impervious to slowdowns – in fact, both inflation and consumption are slowing to the point that monetary policy can now afford to take a more patient approach, in our view. The leading edge of core inflation, when adjusted for the idiosyncratic shocks in the shelter and used cars, has reached levels close to the Federal Reserve’s 2% target, having come down from run rates in excess of 9% in 2021. Deconstructing the goods supply chain to account for leads and lags in the timing of price swings offers further encouragement. Raw materials, logistics and freight rates, intermediate producer costs, and retail trade prices have all reached the deflationary territory. The inflationary burden now rests almost entirely on the end consumer, with wage growth being perhaps the last bastion of inflation. Wages are indeed growing at a faster than historically normal pace at 3.7% (in June), but it is hard to envision wages alone supporting a 4% headline inflation rate, especially when wage growth itself is trending down (from as much as 6-7% at its recent peak).

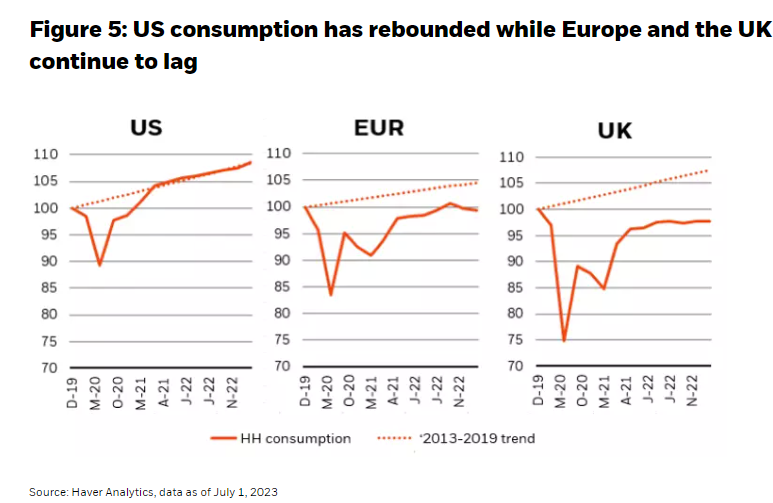

Consumption in the U.S. is also slowing, but it is doing so after having already recovered to a familiar pre-Covid trendline, a feat that few other regions can attest to (see Figure 5). Europe and the U.K., in contrast, have struggled to reach pre-Covid levels in household consumption, much less resume growing at trend. While U.S. inflation has been showing a clear downward trend and growth is expected to be moderate, Europe and U.K. inflation declines risk coming alongside declining growth, creating a nominal growth paradigm that could look materially weaker than that of the U.S. in the coming months. European manufacturing has also suffered one of the longest slumps on record in new orders. That certainly warrants close monitoring, as it may be more attractive to own duration in Europe and the U.K. (than in the U.S.), should the probability of an economic hard landing rise.

Investing in a Changing World

While the economy is going through major structural change, monetary policy seems to have become near-term data-dependent. Perhaps policymakers, having reached restrictive levels of rates that seem to be having their desired effect, albeit slowly, can afford to be spectators for the time being and observe the economy shifting, and markets reacting, to longer-term forces. Equity markets certainly seem to have moved on from policy rate discussions, especially sectors that are deep in the “compiler world,” like software services.

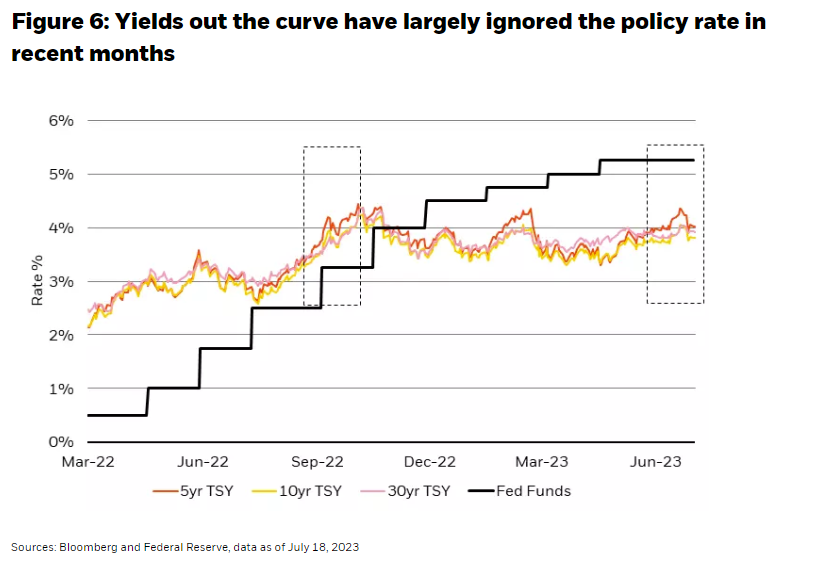

Even long-duration fixed income seems to have largely ignored changes in the policy rate over the past few months. From October 2022 to the recent FOMC policy meeting, 5-, 10- and 30-year U.S. Treasury yields have stayed relatively unchanged at around 4%, despite a 2% rise in the Fed Funds rate from 3.25% to 5.25%. If incrementally higher policy rates are not achieving their primary goal of incrementally raising longer-term borrowing costs, one must wonder whether more hikes are actually changing the economy in real-time, or simply padding the income streams of wealthy savers (see Figure 6). The more recent increase in long-end rates, by contrast, would seem to have more to do with a lack of interest in long-end interest rates as a portfolio utility given the inversion of the yield curve, lack of carry and correlation with risk assets, alongside the assumption of higher government supply over the coming quarters and years.

Suppose time became the primary tool of policymakers (holding rates at restrictive levels for longer) rather than the next 0.25% hike. This would remove a lot of uncertainty around the path of rates, and hence could potentially dampen interest rate volatility. It would allow inflation to continue its downward trajectory without creating new risks around labor market weakness, perhaps supporting a nominal growth environment of 4% to 6%; still solid and equally split between inflation and real growth.

In such a situation, cash and the front end of the yield curve would be much more attractive than the back end, since reinvestment risk would be reduced (after all, rates would be on hold). Besides carrying a lower yield (both real and nominal) and higher volatility, the back end has also proven to be positively correlated with risky assets over the last two years, undermining its value as a portfolio hedge.

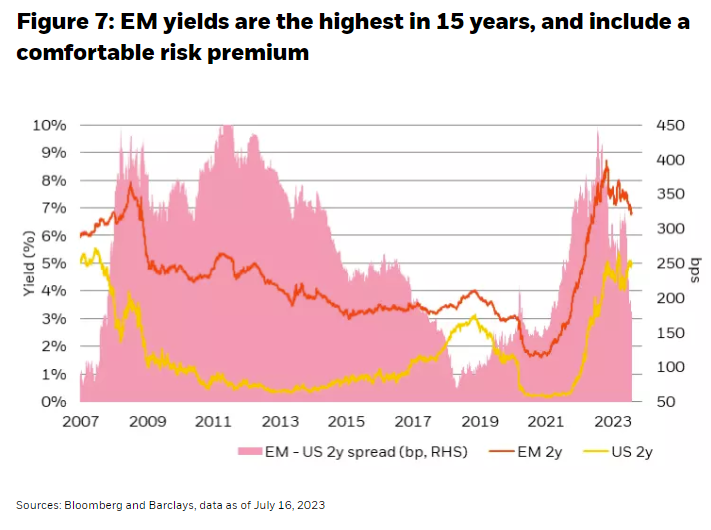

At the same time, lower risk-free rate volatility might make it possible to earn the risk premiums available in the riskiest parts of the capital stack – in emerging markets (EM) and equities. And in a best-case scenario, those risk premiums might actually continue to compress, as they have in 2023-to-date. Inflation continues to abate in EM, and the number of central banks expected to cut rates is mounting, contributing to the margin of safety in EM fixed income (see Figure 7).

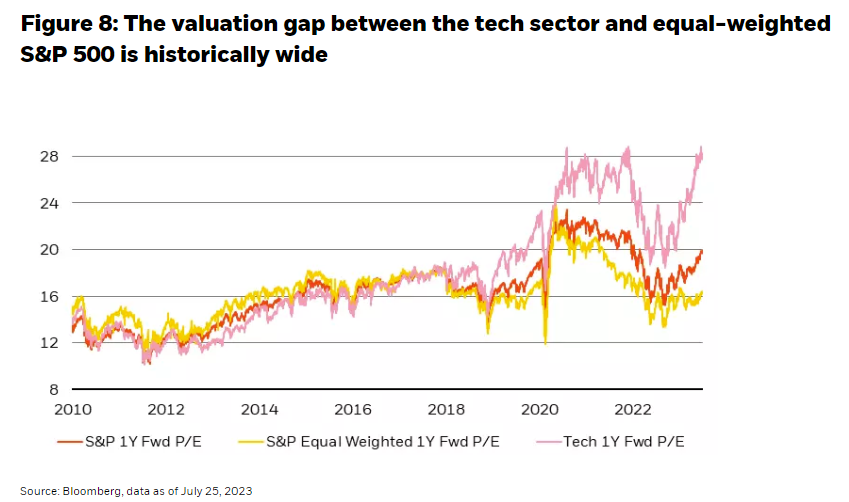

In equities, while technology stocks have reached valuations that are near previous highs, the same cannot be said for the rest of the market. The tech rally could arguably be justified by the supportive structural trends of a compiler economy, anticipated stability in the risk-free rate (which tends to benefit growth stocks), as well as the staggering amounts of research and development expenditure that tech companies are deploying in order to grow future cash flows (a phenomenon we detailed in a previous commentary, “Getting Paid Back”). Still, fuller valuations after a record-breaking rally in the first half of 2023 mean that investors may need to be more selective to realize similar returns in the remainder of the year. Indeed, cheaper equity valuations can be found in many sectors outside tech (many of which still benefit from a high nominal growth environment), such that the valuation gap between tech and the equal-weighted S&P 500 is the widest that it’s been in at least 12 years (see Figure 8).

Capturing the myriad complexities of megatrends, inflation, and monetary policy across asset classes and regions can sound like a difficult exercise, but constructing a portfolio to capture the disparate fundamental trajectories at play is far from impossible. In fact, a simple illustration of two vastly different portfolios is revealing of how we are thinking about asset allocation. Consider a naïve barbell portfolio that is invested equally (50/50) in cash and the equal-weighted S&P 500, compared to a portfolio made up of long-duration investment grade (IG) credit. While equities are often the most volatile part of the capital stack, simply pairing them naively with zero-vol, but (today) high-yielding cash, creates a barbell portfolio that currently yields almost half a percentage point more than the long IG portfolio, while experiencing less than two-thirds of the volatility.

This is a unique point in time where an investor’s objectives of stable income, capital preservation, and real capital appreciation can all be well represented through a thoughtful portfolio construct, particularly because high-quality, short-duration assets have the highest yields in more than 15 years. Investors who are able to build on that naïve barbell example to include emerging markets debt, private credit, or European fixed income can further enhance the carry and risk profile of a portfolio. And some selective equity risk, both inside and outside the tech sector, to balance both valuation and exposure to today’s megatrends, would be extremely complimentary from a capital appreciation perspective. As such, a diversified portfolio with generous yield and modest volatility is finally within reach today and is an option we believe will serve us best as we navigate both challenges and opportunities in our changing world.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of August 4, 2023, and may change as subsequent conditions vary. The information and opinions contained in this commentary are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents.

This commentary may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All